copy the linklink copied! Chapter 1. Colombia in the digital transformation: Opportunities and challenges

The statistical data for Israel are supplied by and under the responsibility of the relevant Israeli authorities. The use of such data by the OECD is without prejudice to the status of the Golan Heights, East Jerusalem and Israeli settlements in the West Bank under the terms of international law.

Colombia has been growing fast and converging to higher living standards since the early 2000s. Growth has been among the strongest in the Latin America and Caribbean (LAC) region and much higher than the OECD average. Between 2008 and 2017, the poverty rate fell from 42% to 27% and the unemployment rate dropped from 11.3% to 9.4%, although both remain high by international comparison. Reforms have reduced informality and improved the business environment. The peace agreement is expected to further boost economic growth over time.

Notwithstanding this remarkable performance, Colombia is facing a number of important challenges, some arising from the international environment, others specific to the domestic economy. A drop in commodity prices has been eroding Colombia’s exports and calls for strengthening its comparative advantage in different sectors, mainly services. Seizing the opportunities from the world market requires greater participation in global value chains (GVCs). Productivity remains low, with large variations among sectors, firms and regions. Skills are lower than in most OECD countries. A high level of informality in the labour market lowers incentives to innovate and reduces the tax base to finance public policies. Financial inclusion remains low, with negative consequences on individuals and firms.

Tackling these issues requires a variety of complementary measures. Among them, policies to enhance digital transformation have a key role to play. Digital technologies are an enabler for innovation and productivity in firms. They make it possible for businesses, including small ones, to manage productive activities across different locations and to connect to GVCs. Digitalisation may help foster financial inclusion and reduce informality. It can also increase the efficiency of the taxation system, therefore providing more resources for public policies. The deployment of high-speed broadband infrastructure gives individuals and firms access to government services and international markets, thus helping to reduce regional disparities. Online educational resources offer new tools for teaching and provide individuals and workers with opportunities for training and skills upgrading.

At the same time, the digital transformation may exacerbate existing inequalities, in particular between high- and low-skilled individuals, large and small firms as well as urban and rural regions. Policies are key to ensure that the potential benefits from the digital transformation are shared throughout the economy and society.

copy the linklink copied! Fostering advanced services via digitalisation

Between 2008 and 2017, gross domestic product (GDP) in Colombia grew by an average of 3.8% in real terms, more than double the OECD average (1.7%). Sound macroeconomic policies and structural reforms contributed to this performance (OECD, 2019c). However, growth was mainly driven by the sharp rise in commodity prices, which boosted the value of exports and attracted a large share of total investment to the mining sector. In 2015, oil and its derivatives accounted for over 40% of total exports (DANE, 2018) and 21% of GDP (OECD, 2018a). The boom in mining generated a strong real appreciation of the currency, reducing the comparative advantages of other tradable goods, particularly in agriculture and manufacturing. It also attracted resources to non-tradable sectors, such as housing and construction.

The external environment, however, has changed significantly over the last few years: growth in the global economy has slowed down, international trade has weakened and commodity prices have fallen. These changes have reduced growth in Colombia, which is currently adjusting to the most severe terms-of-trade shock in Latin America (OECD, 2017c).

With the slowdown of international prices for commodities, the Colombian economy is now in search of new sources of growth. The digital transformation might offer such a catalyst for growth, by helping the commodity sector to become more competitive as well as enabling new business models to emerge in all economic activities.

In particular, digital transformation provides Colombia the opportunity to diversify its activities from a commodity-based to a high value-added services economy (see Chapter 4). The service sector plays a major role in the Colombian economy, accounting for nearly 60% of GDP and 70% of the workforce (DANE, 2019). Firms in the service sector innovate more than those in manufacturing, although productivity growth in services remains well below that of OECD and the large Latin American countries (OECD, 2017c).

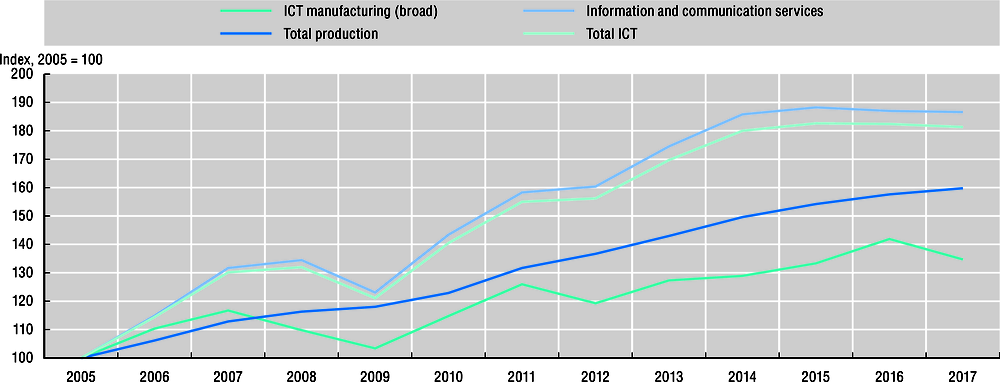

Unlike most OECD countries, in Colombia, telecommunications account for the largest share of information and communication technology (ICT) services. Yet, the country has slowly begun to diversify its ICT services sector (Figure 1.1). While still small by international comparison, production and exports of ICT services (e.g. computer programming, consultancy and related activities) have been highly dynamic in recent years, with relatively high growth in content-related industries and audiovisuals.

Notes: ICT = information and communication technology. Classification: CIIU Rev. 4 A.C. (60 groups). ICT manufacturing includes manufacturing of computer, electronic and optical products as well as electrical equipment (C52). ICT services include telecommunication services, IT services and consulting, broadcasting and media (J81-J84). Data for 2017 are preliminary.

Source: DANE (2019), “Principales agregados macroeconómicos, base 2015”, https://www.dane.gov.co/index.php/estadisticas-por-tema/cuentas-nacionales/cuentas-nacionales-anuales (accessed on 15 April 2019).

More broadly, world trade in ICT-enabled services – i.e. services that can be delivered remotely over ICT networks (UNCTAD, 2015) – are likely to increase substantially over the coming years. Building on ICT-enabled services could be a good strategy to diversify Colombia’s export portfolio (MinTIC, 2014, 2015). For instance, exports of financial services are growing fast and the creation of Fintech start-ups in Colombia has been very dynamic compared to other LAC countries (IDB and Finnovista, 2017).

Most of the ICT services value added produced in Colombia is absorbed domestically rather than exported. This is in sharp contrast to other emerging market economies (EMEs) that have successfully specialised in exporting ICT services. In order to foster Colombia’s role as a provider of high value-added services to the world, policies have been put in place to establish an effective enabling environment for the development of the services sector.

However, regulation in Colombia appears to be overly burdensome. For instance, regulation on broadcasting, telecommunications and insurance services remains restrictive (OECD, 2019c). Performance with advance rulings, appeal procedures, fees and charges, automation, the streamlining of procedures, external border agency co-operation and governance, and impartiality continue to be below best practice (Kowalski et al., 2015). With regard to the transfer of personal data across borders, interoperability of its data protection regulations with those in other countries would help dispel uncertainty about data localisation requirements for cloud computing services (Cory, 2017).

copy the linklink copied! Fostering integration in global value chains through advances in digital technologies

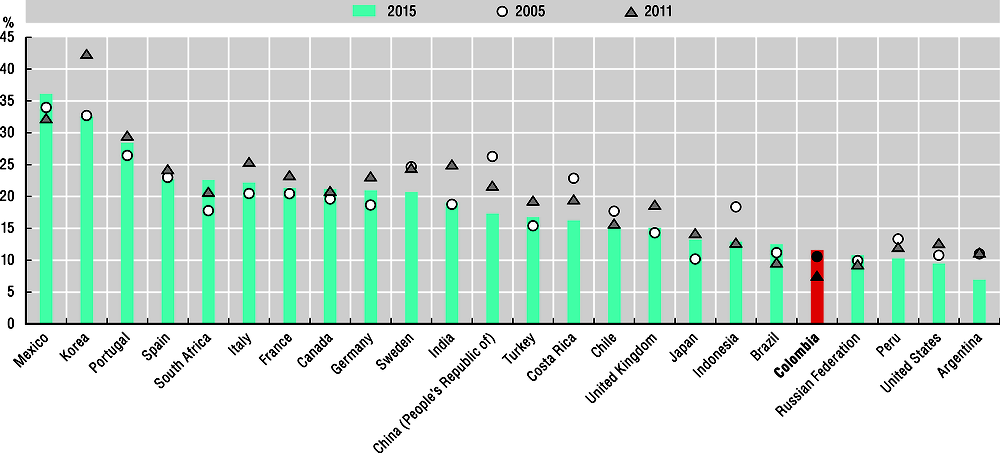

Colombian participation in GVCs is lower than in other EMEs. The country’s role in GVCs is mainly to supply primary inputs via downstream linkages, which reflects the large share of commodities in exports. Colombia participates little in sectors typically associated with dynamic GVCs like motor vehicles, electronics and offshoring of services (OECD, 2017c).

Participation in GVCs is particularly low for backward integration, which measures the share of foreign value added embodied in a country’s gross exports (Figure 1.2). While low backward integration is normal for large countries like Argentina, Brazil or the United States, for smaller economies like Colombia, better integration into GVCs could significantly improve access to higher quality inputs, with potentially large effects on productivity overall (see, for example, Criscuolo, Timmis and Johnstone [2015]).

Notes: Backward integration is measured by the share of foreign value added in domestic gross exports. Forward integration is measured by the share of domestic value added in foreign gross exports.

Source: OECD (2019f), “Trade in value added”, https://doi.org/10.1787/data-00648-en (accessed on 23 May 2019).

Facilitating participation in GVCs requires reducing the costs of production and improving product quality (DNP, 2018). Tariffs are low, but high non-tariff barriers and restrictive practices in many service sectors remain significant. Costs of exporting/importing, such as transport and logistics, are also high due to poor infrastructure. High costs of quality certification, due to the small number of internationally certified laboratories, are an important barrier to participating in GVCs with countries with high-quality standards, such as in North America and Europe (Central Bank of Colombia, 2014; CONPES, 2019a).

Colombian firms have recently been slowly refocusing their backward linkages towards more advanced economies, which may be regarded as a gradual shift up the GVC. Business services and creative industries, in particular, have been increasing their contribution to OECD countries’ final demand in value-added terms, although their level remains low. These services have a high degree of digitalisation, rely heavily on data and data analytics, and are likely to be deeply transformed by fast developments in artificial intelligence (AI) in the forthcoming years. Further development of advanced services is therefore essential to sustain growth in Colombia and to strengthen its integration in GVCs (see Chapter 4).

copy the linklink copied! Increasing productivity through digital uptake

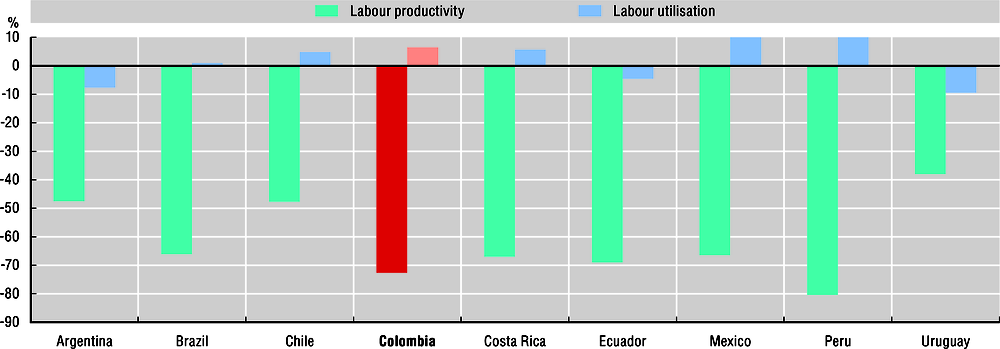

Colombian firms suffer from low productivity, which implies low wages and living standards. In 2018, the productivity gap with the OECD was larger in Colombia than in any other LAC country except Peru (Figure 1.3).

As part of the National Development Plan (Plan Nacional de Desarrollo [PND]), the government is promoting the use of ICTs in firms in order to raise productivity. Although ICT statistics show that adoption is in line with other OECD countries for medium-sized enterprises, this masks the fact that Colombia has a large number of microenterprises (firms with less than ten employees), which are not reported in OECD statistics.

Low competitive pressure seems to weaken incentives for firms to adopt ICTs. Over 90% of microenterprises that do not make use of ICTs report a lack of necessity as the reason for not using them (DANE, 2017). In addition, the particularly large dispersion of productivity between large and small firms and among subnational regions, as well as the low share of medium-sized firms (MGI, 2019), suggest inefficient allocation of resources and a lack of competitive forces to push out less-productive firms (Brown et al., 2016). In 2016, on average, labour productivity of micro, small and medium-sized enterprises (SMEs) in LAC countries was, respectively, 46%, 23% and 6% of large firms’ productivity (OECD, 2019b).

Notes: Labour productivity is measured as GDP per hour worked. Labour utilisation is measured as the ratio of total hours worked to total population.

Source: OECD, based on Conference Board, Total Economy Database, https://www.conference-board.org/data/economydatabase/TED1 (accessed on 4 June 2019).

Although investment has been steadily increasing since 2000, Colombia suffers from poor infrastructure and high transport costs (DNP, 2018). Recent increases in investment can mainly be attributed to the mining sector. Despite significant improvements over recent years, the transport and logistics infrastructure remains less developed than in OECD or other Latin American countries (OECD, 2017c).

Investments are particularly needed in the telecommunication sector to expand and upgrade networks, increase access to the Internet, and improve the overall quality of the communication infrastructure (see Chapter 2). Indeed, broadband infrastructures are the backbone for trade in services and integration in GVCs.

Colombia has the lowest fixed broadband penetration among OECD countries. Most fixed broadband subscriptions are cable subscriptions and, despite a sharp increase in fibre connections in recent years, fibre penetration in Colombia (13% of all broadband connections) still lags well behind the OECD average (25%). This is reflected in the average connection speed for fixed broadband networks, where Colombia ranks well below the OECD average and its Latin American peers. Investments in mobile communication infrastructure rose until 2011, but have been declining since. There is a need to encourage investment to increase the availability of mobile services, especially in relation to 4G networks and their future upgrading to 5G.

To reduce these large infrastructure gaps, Colombia needs to sustain and amplify its public investment effort. Public investment to GDP has increased over the last decade and since 2012 has been above the OECD average. However, the level of investment per capita remains less than the OECD average. To foster infrastructure development and productivity growth, public investment in Colombia needs to be better articulated in coherent territorial strategies (OECD, 2016c). Greater horizontal co-operation is required, as for many development and investment projects the relevant scale goes beyond administrative boundaries. The lack of financial incentives to support cross-jurisdictional co-operation appears to be a significant obstacle.

copy the linklink copied! Using digital opportunities to tackle informality

Informality has important implications for productivity, economic growth and income inequality (Jütting and de Laiglesia, 2009; Loayza, Serven and Sugawara, 2009; Dougherty and Escobar, 2013). To reduce high informality rates, policies should aim at further reducing non-wage labour costs; simplifying the complex procedures for the registration of companies and the affiliation of workers to social security (CONPES, 2019b).

Digitalisation can help to reduce informality. Colombia has already used technology to simplify business and worker registration (see Chapter 3). Continuing this simplification, with initiatives such as the Ventanilla Única Empresarial (one-stop shop) for licencing and business registration, could further foster formalisation (OECD, 2017c). In addition, technology can be used to enforce tax collection, as shown by the positive experience of other countries. For example, in Hungary a requirement for businesses to have electronic cash registers led to a significant increase in tax revenues. Finally, the use of algorithms to analyse the data collected by the tax administration can improve the detection of tax evaders (OECD, 2018b).

More efficient tax collection would increase the revenues from personal income taxes and make it possible to lower the relatively high corporate income tax rates, thus fostering growth and productivity (OECD, 2015a). It could help Colombia to increase the redistribution of income through the tax and transfer system. Little redistribution is currently taking place compared to OECD and many Latin American countries after considering taxes and transfers (OECD, 2017c).

Cash payments are at the core of informality. Promoting the uptake of digital tools of payment would reduce the scope for cash transactions and help informal economic activities to be unveiled. In particular, diffusion of e-wallets and other innovative payment methods could reduce the use of cash even for small transactions and at a negligible cost for the users (DNP, 2018).

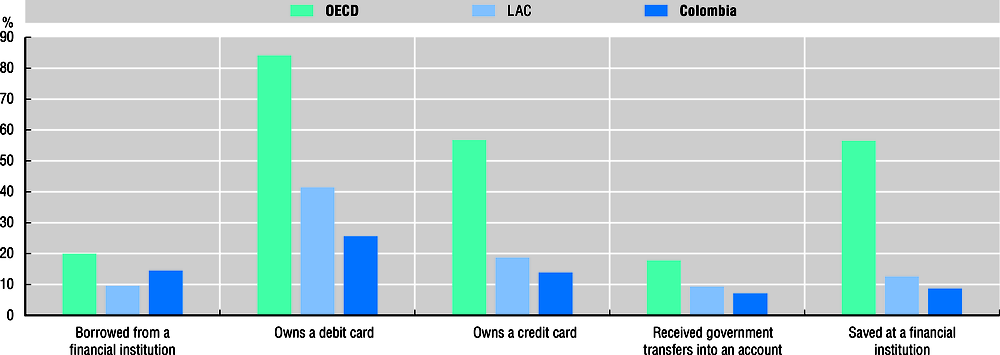

Financial inclusion has been an important priority for the government for a number of years. Policies have mainly aimed at providing microcredit to the poor; spreading the use of the formal banking system; enhancing the use of electronic payments; and making financial services more affordable (Karpowicz, 2014). Despite steady improvements, financial inclusion is still relatively low (Figure 1.4), contributing to income inequality (Park and Mercado, 2015). The use of financial services is low and costs are high.

Notes: OECD aggregate excludes Hungary, Iceland, Latvia, Mexico and Turkey. LAC refers to 23 countries and territories in Latin America and the Caribbean.

Source: World Bank (2017), Global Findex Database 2017, https://globalfindex.worldbank.org/#data_sec_focus (accessed on 4 June2019).

Digital platforms could help boost labour market formality. The use of online platforms to formalise word-of-mouth transactions can allow tax authorities to gain data on such transactions (OECD, 2018d). Countries take a variety of approaches to facilitate data sharing and reporting to labour inspection and taxation authorities. The development of a platform economy also requires clarification of the regulatory framework (see Chapter 5).

copy the linklink copied! Enhancing skills for the digital transformation

Education and skills development play a key role in making growth more inclusive and raising productivity. Skills are also the most important and cross-cutting asset for effective use of digital technologies.

At present, many Colombians seem to lack the foundational skills to take advantage of the digital transformation. Only half of adults have an upper secondary education, compared to about three-quarters in the OECD (OECD, 2017a, 2016b). While there have been significant improvements in attainments in the past decade, many younger Colombians continue to leave school without the skills necessary for the future. More than 60% of students enrolled in secondary education do not have the basic skills necessary to participate in the formal labour market (OECD, 2015c). In addition, the urban-rural divide in school enrolment is wide for both lower and upper secondary education.

Increased sophisticated use of ICTs will require greater skills among users. Many computer users lack some basic computer skills, with a quarter of them unable to send emails with attachments, and a third unable to attach additional devices, such as printers (see Chapter 3). Colombia has a large number of computers per student, higher even than advanced countries such as Denmark and Sweden. However, only two-thirds of these are connected to the Internet.

The success of firms in the digital era depends not only on having workers with good literacy, numeracy, problem solving and generic ICT skills used at work, but increasingly on ICT specialists and data specialists.

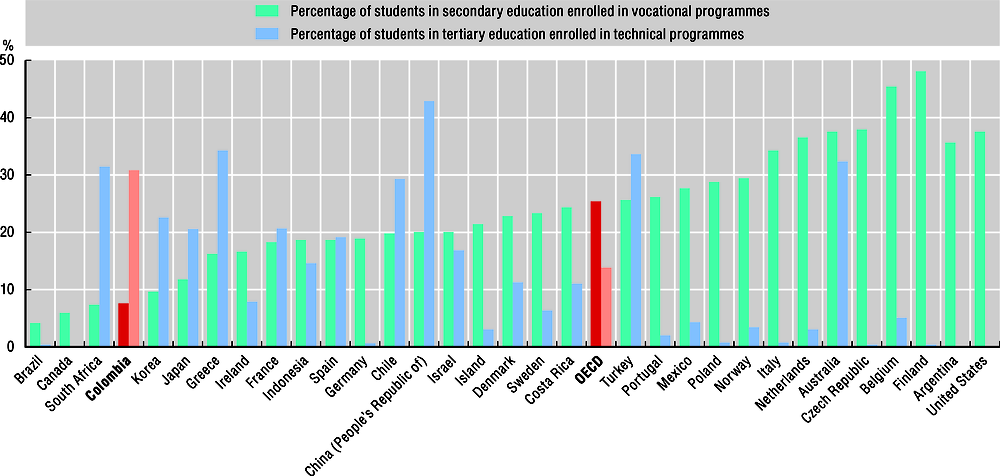

About 30% of Colombian companies identify difficulties in finding skilled workers as the main obstacle to productivity growth (WEF, 2015). The most pressing skill shortage concerns technical workers, but the share of students enrolled in professional and technical degrees in Colombia is low, even in comparison to other EMEs (Figure 1.5). Skills shortages also contribute to poor managerial quality, which can hinder the adoption of innovative new technologies in firms (Andrews, Nicoletti and Timiliotis, 2018).

Notes: Technical/vocational enrolment in secondary education (ISCED 2 and 3) includes teacher training. Enrolment in technical tertiary education is the enrolment at ISCED Level 5B programmes.

Source: UNESCO (2019), UNESCO Institute for Statistics Database, http://data.uis.unesco.org (accessed on 4 June 2019).

Increased public support will be required to the regions that are lagging behind in order to raise the quality of primary education. A national curriculum framework for school education should also be established, which would help set high and equal expectations for all children and provide guidance to teachers on what students should be learning at each stage. This should be complemented with the development of professional standards, improved teacher training and professional development (OECD, 2016b).

copy the linklink copied! Promoting digital innovation

To use digital technologies effectively, firms need to invest not only in digital skills, but also in knowledge-based capital, including data, organisational change and complementary skills that enable high-performance work practices (OECD, 2017b). The improvements in the educational system, therefore, should be complemented with better innovation policies to generate knowledge-based capital.

Colombia’s innovation system is still modest and lacks a strong business core. Research and development (R&D) expenditure is low at 0.2% of GDP, compared to 2.4% in the OECD (OECD, 2015b). Only 30% of total R&D is performed by the business sector, compared with 70% on average for OECD countries. Colombian firms engage little in innovation and only a small portion of firms introduce new products (Figure 1.6).

Note: Data for Colombia refer to 2014-15 (services) and 2013-14 (manufacturing).

Source: OECD (2019d), OECD Innovation Statistics and Indicators (database), http://oe.cd/inno-stats (accessed on 4 June 2019).

Framework conditions for innovation have improved significantly in Colombia in recent years, but there is scope for improvement. Efforts aimed at increasing the efficiency and effectiveness of innovation require improvements in knowledge diffusion channels. It is therefore essential to strengthen collaboration between businesses, education and research institutions, which is weak in Colombia.

The government has several strategies to promote innovation and R&D, including ICT-related innovation. However, there seems to be a large number of programmes with limited resources and, in some cases, overlapping objectives (see Chapter 5).

copy the linklink copied! Setting a regulatory framework conducive to digitalisation

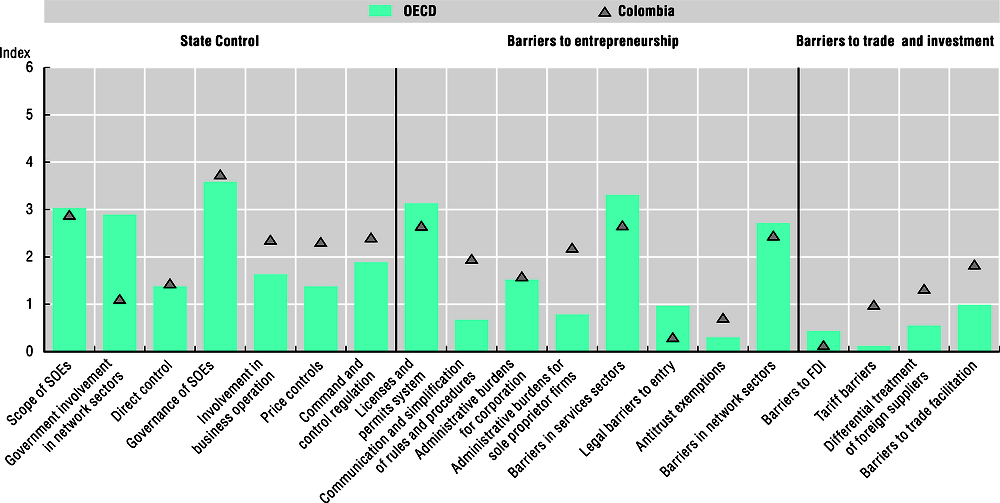

Colombia has significantly improved its regulatory environment over the last decade by simplifying the process to start a business, pay taxes and resolve insolvency, as well as by reducing entry costs and barriers to entrepreneurs. Colombia now ranks around the OECD average in about half of the dimensions of product market regulation. However, product market restrictiveness remains above the OECD average in some important areas, such as the state’s involvement in business operations, regulatory procedures in some sectors and competition in some network sectors (Figure 1.7).

Simulations suggest that aligning product market regulation with OECD best practices could boost GDP by 0.25% to 0.50% annually over five years (OECD, 2016a).

Note: SOE = state-owned enterprise; FDI = direct foreign investment. The OECD Product Restrictiveness Index scales from 0 to 6, from least to most stringent.; FDI: foreign direct investments. More information is available at: www.oecd.org/economy/reform/indicators-of-product-market-regulation/.

Source: OECD (2018c), OECD Product Market Regulation Statistics (database), https://doi.org/10.1787/pmr-data-en.

The costs of doing business in Colombia are exacerbated by the difficulties in enforcing contracts through the judicial system (World Bank, 2018; DNP, 2018). Enforcing a standard debt contract takes much more time than in OECD countries and other EMEs; and the experience of other LAC countries shows that the cost of lengthy procedures is particularly high for young firms (Arnold and Flach, forthcoming).

Getting regulation right in the telecom industry is essential for the development of broadband services, access to the Internet and uptake of advanced digital technologies. Colombia has taken steps to strengthen the independence of the communication regulator (the Commission for Communications Regulation [Comisión de Regulación de Comunicaciones, CRC]) following the main recommendations of the OECD Review of Telecommunication Policy and Regulation (OECD, 2014). The trend towards convergence of the telecommunication, broadcasting and content industries observed in many OECD countries calls for the prompt development of a converged regulatory framework in Colombia. The recently approved bill on the modernisation of the ICT sector aims to address these issues (see Chapter 2).

copy the linklink copied! Policies for digital transformation in Colombia

Over the last decade, digitalisation policies in Colombia have been organised around three components. The first one is the ICT Law issued in 2009, which established the Information Technologies and Communications Fund (Fondo para las Tecnologías de Información y las Comunicaciones) “to finance plans, programs and projects to primarily facilitate universal access and universal service” (Law 1341 of 2009).

The second component consists of three PNDs issued in 2010-14, 2014-18 and 2018-22. The PND is the formal and legal instrument that establishes the objectives of government, setting programmes, investments and goals for a four-year period.

The third component are the ICT strategic sectoral plans set by the Ministry of Information and Communication Technologies (Ministerio de Tecnologías de la Información y Comunicaciones [MinTIC]): Live Digital (Vive Digital) (2010-14); its follow-up Live Digital for the People (Vive Digital para la Gente) (2014-18); and the newly launched The Digital Future is for All (El Futuro Digital es de Todos) (2018-22).

The PND 2018-2022 puts forward a Pact for the Digital Transformation of Colombia (Pacto por la Transformación Digital de Colombia) (DNP, 2018) with four main objectives:

-

promote the digital transformation of society and close the digital divide among individuals, businesses and territories

-

foster productivity in the government and in businesses through advanced digital technologies, e.g. big data, AI and the Internet of Things

-

foster investment and skills development for Industry 4.0

-

promote entrepreneurship, particularly for technology-based start-ups and in creative industries.

To achieve these objectives, the PND sets two major goals with several targets to be achieved by 2022 (Table 1.1).

The ICT strategic sectoral plan El Futuro Digital es de Todos articulates the PND around five axes (MinTIC, 2019):

-

Effective use of ICTs by citizens. Citizens will trust, use and benefit from ICTs.

-

Modernisation of the ICT sector. The legal and regulatory framework of the ICT sector will be updated to transform it into a modern, dynamic sector and an engine of inclusive growth.

-

ICT-driven economy. The Colombian economy will be driven by a creative, innovative, entrepreneurial and export-oriented ICT sector that will become a regional leader.

-

High-quality connectivity for all. Colombia will be connected to high-speed, with high-quality services at a fair price, thus closing the digital divide.

-

Digitalisation of the public administration procedures and services. Colombia will achieve digitalisation of all public administration processes at the national level and of 50% at the regional level, thus becoming a regional leader in digital government.

copy the linklink copied! Going Digital: An integrated policy approach in the digital age

The OECD has developed an Integrated Policy Framework to support a whole-of-government approach to coherent policy making in the digital age. The framework recognises technologies, data and business models as the driving forces underlying digital transformation, and builds on a cross-cutting analysis of the transformation across many different policy areas (OECD, 2019e). The framework itself includes seven integrated building blocks (Figure 1.8).

Source: OECD (2019a), Going Digital: Shaping Policies, Improving Lives, https://doi.org/10.1787/9789264312012-en.

These integrated building blocks do not represent discrete policy domains; rather, each of them brings together multiple policy areas (see more details on each building block below). They also do not stand in isolation, but are related to one another. This configuration underscores that leveraging the benefits and addressing the challenges of digital transformation requires identifying policy areas that are jointly affected and that need to be co-ordinated. It also underscores that all building blocks are needed to make digital transformation work for growth and well-being.

Access

Reliable communications infrastructures and services underpin the use of all digital technologies, and facilitate interactions between connected people, organisations and machines. Similarly, the data that flow through networks are also emerging as a source of value in the digital era, but their productive use is predicated on their availability.

As reliable communications infrastructures and services are essential to digital transformation, the first integrated building block concerns access to data, communications infrastructures and services (e.g. fibre optic backhaul, towers, spectrum, international cables), encompassing efficient, reliable and widely accessible broadband communication networks and services and key complementary enablers, (e.g. a co-ordinated system of international domain names, increasing uptake of IPv6 Internet addresses, Internet exchange points), data, software, and hardware. These act as the technical foundations for an open, interconnected and distributed Internet that enables both the global free flow of information and, more generally, digital transformation. Multiple policy domains need to be considered to ensure access, including: communications infrastructures and services, competition, investment, and regional development.

Use

Access to digital networks provides the technical foundation for the digital transformation of the economy and society, but does not necessarily ensure widespread diffusion of digital tools and their effective usage, which are needed for individuals, governments and firms to reap the benefits of digital transformation through increased participation, innovation, productivity and well-being. Diffusion and effective use crucially depend on investments in ICTs, complemented by investments in knowledge-based capital, including data and organisational change; on a favourable business environment (e.g. one that fosters business dynamism); on the availability and allocation of skills; and on trust. Therefore, multiple policy domains need to be considered under use: digital government, investment, business dynamism and SMEs, education and skills, and digital security and privacy.

Innovation

Innovation – another integrated building block – pushes out the frontier of what is possible, driving job creation, productivity growth, and sustainable growth and development. Digital innovation, in particular, has driven radical changes in the ways people interact, create, produce and consume. Digital innovation not only gives rise to new and novel products and services, it also creates opportunities for new business models and markets, and can drive efficiencies in the public sector and beyond. In addition, digital technologies and data drive innovation in a wide range of sectors, including education, health, finance, insurance, transport, energy, agriculture and fisheries, as well as the ICT sector itself. Multiple policy domains need to be considered to foster innovation, including entrepreneurship and SMEs; science and technology; competition; digital government; and sectoral policies such as energy, finance, education, transport, health and education, among others.

Jobs

Digital transformation has already begun to change the nature and structure of organisations and markets, raising important questions about which jobs might disappear and where new ones will come from, what they will look like and which skills will be required. At the same time, issues around who might be the most affected and what can be done to foster new job creation and to align skills development with the changing skills requirement of jobs have emerged. Technological advances and the introduction of new business models have given rise to the “platform economy” and have led to the emergence of new forms of work such as “crowd work”, “gig work” and other forms of on-demand labour. Making sure that digital transformation leads to more and better jobs will depend on the kind of policies that accompany it, including in the areas of labour markets, education and skills, and social protection; since the impacts may be concentrated in some industries and regions, sectoral and regional policies will be important, too.

Society

Digital transformation affects society and culture in complex and interrelated ways, as digital technologies change the ways in which individuals, firms and governments interact among and with one another. For digital transformation to work for growth and well-being, it is essential that public policies support a positive and inclusive digital society. To do so, multiple policy domains need to be considered: social policies (e.g. housing and welfare), education and skills, tax and benefit policies, environment, health, and digital government. Digital transformation changes the distribution of benefits, raising the question of where life is getting better, and for whom, making social policies an important part of the policy toolbox. In particular, social policies can help address a range of digital divides.

Trust

Trust is fundamental to the digital transformation; without it, individuals, firms and governments won’t fully use digital technologies, and an important source of potential growth and social progress will be left unexploited. Countries may benefit from greater cross-border co-operation if they develop comprehensive and coherent national strategies for digital security and privacy to address issues such as the protection of personal data, the resilience of essential services (e.g. water, energy, finance, public health and safety), the creation of incentives (e.g. cyber insurance, public procurement), support to SMEs and related skills development, in consultation with all relevant stakeholders. At the same time, it is important to continue promoting effective protection to consumers engaged in e-commerce and other online activities, as this will help the digital economy flourish as well as be inclusive.

Market openness

Digital technologies are transforming the environment in which firms compete, trade and invest. Market openness policies related to trade, investment, financial markets, competition and taxation play an important role in ensuring that favourable conditions exist for the digital transformation to flourish. Digital transformation also affects market openness policy domains, raising opportunities and posing challenges. Governments could benefit from periodically reviewing market openness policies and, where appropriate, update them to ensure that they are well suited to making digital transformation work for growth and well-being.

copy the linklink copied! Going Digital in Colombia

This Review examines opportunities and challenges raised by digitalisation in Colombia in the areas highlighted above. It also looks at the policies in place and makes recommendations to improve them, based on the Going Digital Integrated Policy Framework. The Review focuses on selected components of the framework according to priorities expressed by the Colombian government.

Chapter 2 examines trends and structural features of the telecommunication market and discusses the institutional framework for sectoral regulation to enhance access and use of communication services.

Chapter 3 reviews recent trends in the use of digital technologies by individuals, businesses and the government in Colombia; analyses the skills required to use these technologies effectively; and provides policy recommendations.

Chapter 4 analyses recent changes in the economic structure of Colombia and examines how digital policies are interacting with several areas, including industrial and trade policies.

Chapter 5 examines opportunities and challenges raised by digitalisation in two key areas – innovation and skills – and analyses key policies in these areas and provides recommendations.

Chapter 6 reconsiders the policies analysed in the other chapters in relation to their coherence among policy domains and across levels of government and makes recommendations for Colombia’s Digital Strategy.

References

Andrews, D., G. Nicoletti and C. Timiliotis (2018), “Digital technology diffusion: A matter of capabilities, incentives or both?”, OECD Economics Department Working Papers, No.1476, OECD Publishing, Paris, https://doi.org/10.1787/7c542c16-en.

Arnold, J. and L. Flach (forthcoming), “Structural policies and the productivity of firms in Brazil”, OECD Economics Department Working Papers, OECD Publishing, Paris.

Brown, J.D. et al. (2016), “Productivity convergence at the firm level: New evidence from the Americas”, in: Thompson Araujo, J. et al. (eds.), Understanding the Income and Efficiency Gap in Latin America and the Caribbean, The World Bank, Washington, DC, https://doi.org/10.1596/978-1-4648-0450-2_ch5.

Central Bank of Colombia (2014), “Una visión general de la política comercial colombiana entre 1950 y 2012”, Borradores de Economiá, No. 817, Central Bank of Colombia, Bogotá, www.banrep.gov.co/sites/default/files/publicaciones/archivos/be_817.pdf.

CONPES (2019a), “Política Nacional de Laboratorios: Prioridades para mejorar el cumplimiento de estándares de calidad”, Documento CONPES, No. 3957, National Council for Social and Economic Policy, Bogotá, https://colaboracion.dnp.gov.co/CDT/Conpes/Económicos/3957.pdf.

CONPES (2019b), “Política de Formalización Empresarial”, Documento CONPES, No. 3956, National Council for Social and Economic Policy, Bogotá, https://colaboracion.dnp.gov.co/CDT/Conpes/Económicos/3956.pdf.

Cory, N. (2017), “Cross-border data flows: Where are the barriers, and what do they cost?”, Information Technology & Innovation Foundation, www2.itif.org/2017-cross-border-data-flows.pdf?_ga=2.219653402.2080636828.1533311065-794592145.1533311065.

Criscuolo, C., J. Timmis and N. Johnstone (2015), “The relationship between GVCs and productivity”, background paper for the Global Forum on Productivity, OECD, Paris, www.oecd.org/global-forum-productivity/events/Relashionship_btween_GVCs_and_productivity_6_09_2016.pdf.

DANE (2019), “Principales agregados macroeconómicos, base 2015”, Cuentas Nacionales Anuales (database), https://www.dane.gov.co/index.php/estadisticas-por-tema/cuentas-nacionales/cuentas-nacionales-anuales (accessed on 15 April 2019).

DANE (2018), “International trade: Exports”, National Administrative Department of Statistics, www.dane.gov.co/index.php/en/statistics-by-topic-1/foreign-trade/international-trade-exports (accessed on 12 August 2018).

DANE (2017), “Indicadores básicos de tenencia y uso de tecnologías de la información y comunicación – TIC en microestablecimientos”, National Administrative Department of Statistics, https://www.dane.gov.co/index.php/en/statistics-by-topic-1/technology-and-innovation/information-and-communication-technology-ict/basic-ict-indicators-in-enterprises (accessed on 12 August 2018).

DNP (2018), Plan Nacional de Desarrollo 2018-2022 “Pacto por Colombia, Pacto por la Equidad”, National Planning Department.

Dougherty, S. and O. Escobar (2013), “The determinants of informality in Mexico’s states”, OECD Economics Department Working Papers, No. 1043, OECD Publishing, Paris, https://doi.org/10.1787/5k483jrvnjq2-en.

IDB and Finnovista (2017), “Fintech: Innovations you may not know were from Latin America and the Caribbean”, Inter-American Development Bank, https://doi.org/10.18235/0000703#sthash.KPMCQIZ3.dpuf.

Jütting, J. and J. de Laiglesia (2009), Is Informal Normal?: Towards More and Better Jobs in Developing Countries, Development Centre Studies, OECD Publishing, Paris, https://doi.org/10.1787/9789264059245-en.

Karpowicz, I. (2014), “Financial inclusion, growth and inequality: A model application to Colombia”, IMF Working Papers, No. 14/166, International Monetary Fund, Washington, DC, https://www.imf.org/external/pubs/ft/wp/2014/wp14166.pdf.

Kowalski, P. et al. (2015), “Participation of developing countries in global value chains: Implications for trade and trade-related policies”, OECD Trade Policy Papers, No. 179, OECD Publishing, Paris, https://doi.org/10.1787/5js33lfw0xxn-en.

Loayza, N. V., L. Serven and N. Sugawara (2009), “Informality in Latin America and the Caribbean”, Policy Research Working Paper Series, No. 4888, The World Bank, https://ideas.repec.org/p/wbk/wbrwps/4888.html.

MGI (2019), Latin America’s Missing Middle: Rebooting Inclusive Growth, McKinsey Global Institute.

MinTIC (2019), “Plan Estratégico Sectorial 2019-2022”, draft, Ministry of Information and Communication Technologies, Bogotá, 20 January.

MinTIC (2015), “Vive Digital 2014-2018”, English version, https://www.slideshare.net/Ministerio_TIC/vive-digital-2014-2018-english-version (accessed on 22 May 2019).

MinTIC (2014), “Vive Digital Colombia”, https://www.mintic.gov.co/portal/604/articles-5193_recurso_2.pdf (accessed on 22 May 2019).

OECD (2019a), Going Digital: Shaping Policies, Improving Lives, OECD Publishing, Paris, https://doi.org/10.1787/9789264312012-en.

OECD (2019b), Latin American Economic Outlook 2019: Development in Transition, OECD Publishing, Paris, https://doi.org/10.1787/g2g9ff18-en.

OECD (2019c), OECD Economic Surveys: Colombia 2019, OECD Publishing, Paris, https://doi.org/10.1787/25222961.

OECD (2019d), OECD Innovation Statistics and Indicators (database), http://oe.cd/inno-stats (accessed on 4 June 2019).

OECD (2019e), “Vectors of digital transformation”, OECD Digital Economy Papers, No. 273, OECD Publishing, Paris, https://dx.doi.org/10.1787/5ade2bba-en.

OECD (2019f), “Trade in value added”, OECD-WTO: Statistics on Trade in Value Added (database), https://doi.org/10.1787/data-00648-en (accessed on 23 May 2019).

OECD (2018a), “Detailed National Accounts, SNA 2008 (or SNA 1993): Value added and its components by activity – ISIC Rev. 4”, OECD National Accounts Statistics (database), https://doi.org/10.1787/data-00721-en (accessed on 4 June 2019).

OECD (2018b), Digital Government Review of Colombia: Towards a Citizen-Driven Public Sector, OECD Digital Government Studies, OECD Publishing, Paris, https://doi.org/10.1787/9789264291867-en.

OECD (2018c), OECD Product Market Regulation Statistics (database), https://doi.org/10.1787/pmr-data-en.

OECD (2018d), Tax Challenges Arising from Digitalisation – Interim Report 2018: Inclusive Framework on BEPS, OECD/G20 Base Erosion and Profit Shifting Project, OECD Publishing, Paris, https://doi.org/10.1787/9789264293083-en.

OECD (2017a), Education at a Glance 2017: OECD Indicators, OECD Publishing, Paris, https://doi.org/10.1787/eag-2017-en.

OECD (2017b), OECD Digital Economy Outlook 2017, OECD Publishing, Paris, https://doi.org/10.1787/9789264276284-en.

OECD (2017c), OECD Economic Surveys: Colombia 2017, OECD Publishing, Paris, https://doi.org/10.1787/eco_surveys-col-2017-en.

OECD (2016a), Chile: Policy Priorities for Stronger and More Equitable Growth, Better Policies, OECD Publishing, Paris, https://doi.org/10.1787/9789264251182-en.

OECD (2016b), Education in Colombia, Reviews of National Policies for Education, OECD Publishing, Paris, https://doi.org/10.1787/9789264250604-en.

OECD (2016c), Making the Most of Public Investment in Colombia: Working Effectively across Levels of Government, OECD Multi-level Governance Studies, OECD Publishing, Paris, https://doi.org/10.1787/9789264265288-en.

OECD (2015a), OECD Economic Surveys: Colombia 2015, OECD Publishing, Paris, https://doi.org/10.1787/eco_surveys-col-2015-en.

OECD (2015b), OECD Science, Technology and Industry Scoreboard 2015: Innovation for Growth and Society, OECD Publishing, Paris, https://doi.org/10.1787/sti_scoreboard-2015-en.

OECD (2015c), Universal Basic Skills: What Countries Stand to Gain, OECD Publishing, Paris, https://doi.org/10.1787/9789264234833-en.

OECD (2014), OECD Review of Telecommunication Policy and Regulation in Colombia, OECD Publishing, Paris, https://doi.org/10.1787/9789264208131-en.

Park, C.-Y. and R.V. Mercado, Jr. (2015), “Financial inclusion, poverty and income inequality in developing Asia”, ADB Economics Working Paper Series, No. 426, Asian Development Bank, Manila, http://hdl.handle.net/11540/2272.

UNCTAD (2015), “International trade in ICT services and ICT-enabled services: Proposed indicators from the Partnership on Measuring ICT for Development”, UNCTAD Technical Notes on ICT for Development, No. 3, United Nations Conference on Trade and Development, http://unctad.org/en/PublicationsLibrary/tn_unctad_ict4d03_en.pdf.

UNESCO (2019), UNESCO Institute for Statistics Database, http://data.uis.unesco.org (accessed on 4 June 2019).

WEF (2015), The Human Capital Report 2015, Employment, Skills and Human Capital Global Challenge Insight Report, World Economic Forum in collaboration with Mercer.

World Bank (2019), Doing Business (database), www.doingbusiness.org/data (accessed on 4 June 2019).

World Bank (2017), Global Findex Database 2017, https://globalfindex.worldbank.org/#data_sec_focus (accessed on 4 June 2019).

Metadata, Legal and Rights

https://doi.org/10.1787/781185b1-en

© OECD 2019

The use of this work, whether digital or print, is governed by the Terms and Conditions to be found at http://www.oecd.org/termsandconditions.