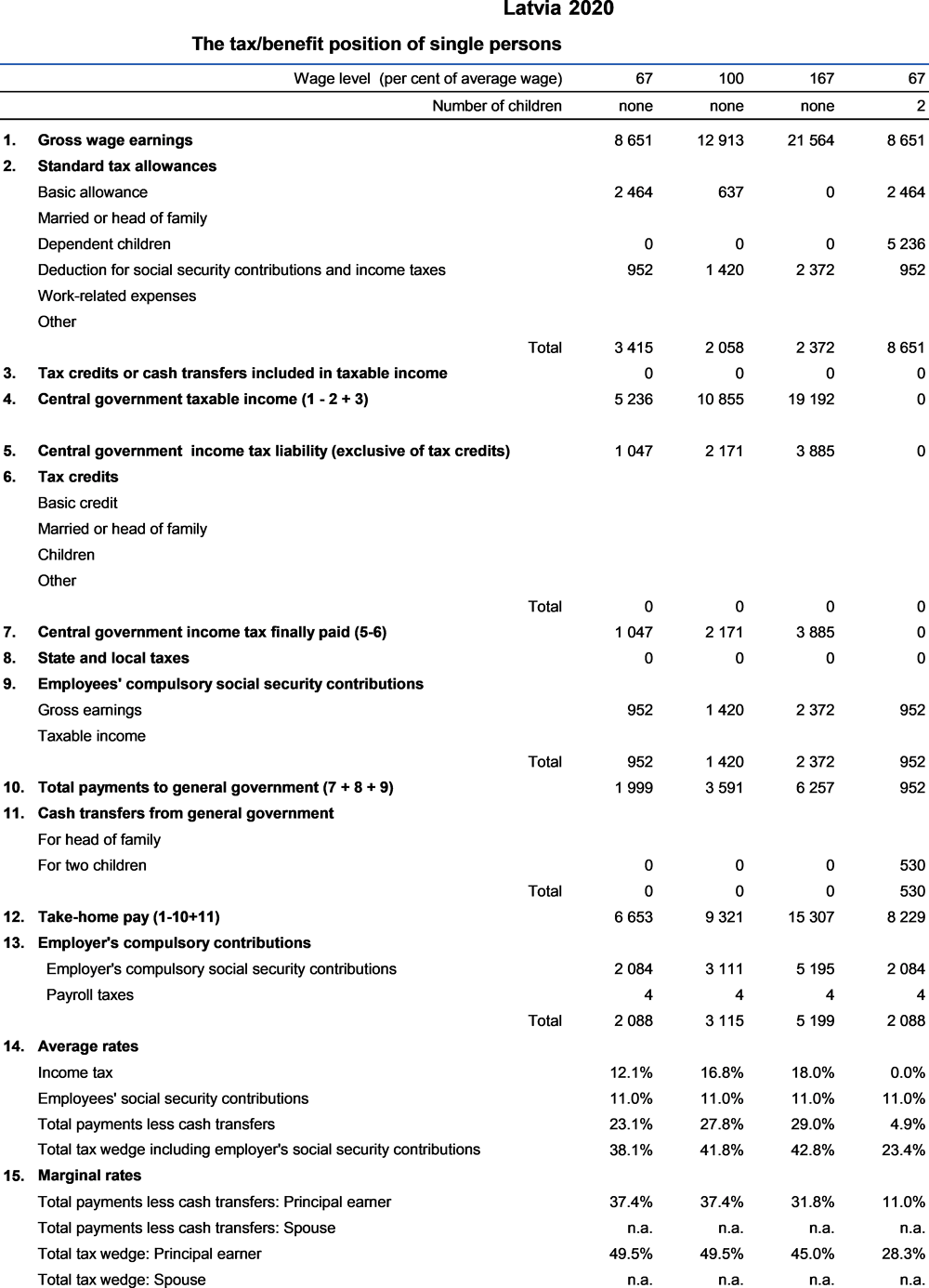

Latvia

This chapter includes data on the income taxes paid by workers, their social security contributions, the family benefits they receive in the form of cash transfers as well as the social security contributions. Results reported include the marginal and average tax burden for eight different family types.

Methodological information is available for personal income tax systems, compulsory social security contributions to schemes operated within the government sector, universal cash transfers as well as recent changes in the tax/benefit system. The methodology also includes the parameter values and tax equations underlying the data.

Since 2014, the Latvian currency is the Euro (EUR). In 2020, EUR 0.88 was equal to USD 1. That year, the average worker in Latvia earned EUR 12 913 annually (Secretariat estimate).

From 1th January 2018, Latvia has introduced an ambitious tax reform. One of the main goal of this reform is reach Latvian government as well as international expert’s expectations – to reduce the tax wedge, especially for low-wage earners.

1.1. Central government income tax

Since 2018, with labour tax reform for the first time the progressive income tax system is introduced, as well as the differential non-taxable minimum, the allowance for dependents and the non-taxable minimum for pensioners is increased, and the minimum monthly wage is raised.

1.1.2. The main tax allowances

1.1.2.1. Standard tax reliefs

Since 2016, the differentiated non-taxable minimum is introduced.

The differentiated non-taxable minimum varies depending on the person's income level: higher for lower wages, but less for higher wages. The differentiated non-taxable minimum gradually is raised.

In 2019 the differentiated non-taxable minimum varies from EUR 0 to 230 per month and in 2020 - from EUR 0 to 300 per month (see table below).

For example, in 2019, the maximum tax allowance amount is EUR 230 per month and it is applied to persons with the taxable income below EUR 440 per month. If taxable income is between EUR 440 per month and EUR 1 100 per month, the differentiated annual non-taxable minimum is calculated according to specific formula. The allowance gradually decreases until it reaches zero or not be applied. The same calculation was in 2018 and will be in 2020 with relevant year data. It is important to note that from 2018, the differentiated non-taxable minimum in full amount is applied already during the tax year. It is based on the State Revenue Service (SRS) forecast which takes account the taxpayer annual income of the previous year. In 2017 the non-taxable minimum was applied only in the minimum amount for all taxpayers (EUR 60) and only after the next tax year, when taxpayer submitted annual tax return, it applied on the basis of the data regarding person’s annual taxable income.

The allowance for dependents is also deductible from income before taxes.

The tax allowance for each dependant (which in most cases are children) gradually is raised - in 2018 to EUR 200 per month or EUR 2 400 per year, in 2019 to EUR 230 per month or EUR 2 760 per year and in 2020 to EUR 250 per month or EUR 3 000 per year. In 2017, it was EUR 175 per month or EUR 2 100 per year.

The taxpayer can apply allowance for a child below 18 years old and for a child below 24 years old if he or she continues studies of a general, professional, higher or special education. The allowance for child relates to taxpayer's child and in certain cases - sisters, brothers, grandchildren, as well as guardianship or dependent persons.

As of 2016, the rule of law narrowed, removing allowances for unemployed spouse, parents or grandparents, except if these persons are with disabilities.

From 2017, the tax allowance for dependents is expanded by non-working spouse, who is taking care of the minor child with a disability, if the non-working spouse does not receive taxable income or State pension.

In addition, as of July 1, 2018, the allowance is applicable for unemployed spouse who is taking care of:

three or more children below 18 years or below 24 years old (if he/she studies), of which at least one is below 7 years old;

five children below 18 years or below 24 years old (if he/she studies).

To support employment of youth during the summer (from June 1st to August 31st), parents can still receive tax allowance for dependents (children while they have working relationship):

Relief for Compulsory social security contributions: Employee’s state social security contributions are deductible from income before taxes.

1.1.2.2. The main exemptions:

income from rural tourism or agricultural production, as well as of mushrooming, berry-picking or the collection of wild medicinal plants and flowers or an uncultivated species of an individual - a park of walrus (Helix pomatia), if it does not exceed a turnover of EUR 3 000 per taxation year, including the sums of State aid for agriculture or of the European Union aid for agriculture and rural development, in amount of EUR 3 000 per taxation year;

insurance compensations, except such insurance compensations paid on the basis of a life, health and accident insurance contract entered into by the employer and a life-long pension insurance contract (with accrued funded pension assets in accordance with the Law on State Funded Pensions);

insurance compensations which have been disbursed upon the occurrence of an insurable event in relation to the life and health of the insured person due to an accident or illness, in accordance with the life insurance policy (including with accumulation of funds) regardless of who has entered into the insurance contract;

the supplementary pension capital, which has been formed from contributions of private individuals or their spouse or a person related to their relatives up to the third stage within the meaning of the Civil Law into private pension funds according to licensed pension plans and paid to participants in pension plans;

income from Latvian or other EU Member State or EEA State and local government bonds;

capital gains on immovable property, if the ownership of the payer has been for more than 60 months (5 years) and it has been the declared as place of residence of the person for at least 12 months (1 year);

capital gains on immovable property, if the ownership of the payer has been for more than 60 months (5 years) and the last 60 months (5 years) this immovable property has been the only real estate of the payer;

capital gains on immovable property which has occurred in relation to the division of property in the case of dissolution of marriage, if it has been the declared place of residence of both spouses at least 12 months until the day of entering into the alienation contract;

capital gains on immovable property, if this income is invested a new in a functionally similar immovable property within 12 months or before alienation of the immovable property or real property prior to expropriation;

income from the alienation of personal property (movable objects such as furniture, clothing and other movable objects belonging to an individual intended for personal use) except income from the sale of items (tangible or intangible) prepared for sale or purchased, the capital gains and other income from capital and scrap sales;

scholarships paid from the budget, association or foundation resources;

scholarships up to 280 euros per month paid by an entrepreneur in accordance with the procedure set out by the Cabinet of Ministers for the organization and implementation of work environment training shall be paid by the merchant, institution, association, foundation, natural person registered as a performer of economic activity, as well as individual enterprise, including farmer or fishermen's farm, and other economic operators;

grants paid to a student who attends a medical education program to promote the acquisition of an educational program and which is paid out from the institution of health care institution;

prizes of lotteries and gambling if the amount (total amount) of the prize (value thereof) does not exceed EUR 3 000 per taxation year;

material and monetary prizes (premiums) received at competitions and contests, the total value of which in the taxation year does not exceed EUR 143, and the prizes and premiums acquired at international contests the total value of which does not exceed EUR 1 423 a year, as well as the financial incentive paid out to the laureates of the prizes of the Baltic Assembly and prizes of the Cabinet;

revenues from gifts up to EUR 1 425 from natural person, other than a close relative;

revenues from gifts in full amount from natural persons, if the giver is connected to the payer by marriage or kinship to the third degree;

dividends, income equal to dividends or notional dividends if the enterprise income tax has been paid etc.

1.1.3. Tax schedule

From 2018, the personal income tax (PIT) system is progressive (in 2017 the PIT rate was a flat tax rate of 23%).

In 2020, the PIT rates are set:

23% - for income exceeding EUR 20 004 but not exceeding EUR 62 800 per year (in 2018 not exceeding EUR 55 000 per year);

31.4% - for income exceeding EUR 62 800 per year (in 2018 exceeding EUR 55 000 per year).

The tax rate 20% and 23% (depending on the level of income) is applicable monthly in the workplace where a payroll tax book is submitted. In the workplace where a payroll tax book is not submitted, only the rate 23% should be applied.

The rate 31.4% has calculated only in annual tax return. During the year, the tax is paid as Solidarity tax for employee revenue above EUR 62 800 per year. The Solidarity tax part of 10.5% is transformed into a Personal income tax rate of 31.4%. Compulsory social security contributions from incomes above EUR 62 800 per year is not be paid.

In 2018, the compulsory social insurance contribution rate is increased by one percentage point from 34.09% to 35.09% to ensure financing of the health sector (0.5% paid by the employee and 0.5% paid by the employer). In 2020, the same rate (35.09%) remains.

Social insurance contributions covers:

social insurance in respect of accidents at work and occupational diseases;

In 2020, the maximum object of mandatory social payments is 62 800 EUR per year.

2.1. Employees’ contributions

Employees pay 11% of their earnings in contributions. The taxable base is the total amount of the gross wage or salary including vacation payments, fringe benefits and remuneration of expenses related to work above a certain threshold. The assessment period is the calendar month.

2.2. Employers’ contributions

Social security contributions are also paid by employers at a rate of 24.09% on behalf of their employees. The taxable base and the assessment period are the same as for employees’ contributions.

The total contribution rates paid by employees and employers are applied:

2.3. Solidarity tax

From 2016 Solidarity tax was introduced.

From 2019 the Solidarity tax rate has been reduced from 35.09% (2018) to 25.50%. See more in the table below on the distribution of Solidarity tax rate from 2016 to 2020.

The difference between 2018 and 2019 is that:

in 2018 Solidarity tax rate is set at the same level as the current social security contributions rates (11% and 24.09%). Solidarity tax is applied during the tax year to the same rate as the social security contributions.

in 2019 and 2020 Solidarity tax is set at 25.5%, which is less than the current social security contributions rate of 35.09% (11% and 24.09%). Also in 2019 and 2020 Solidarity tax is applied during the tax year to the same rate as the social security contributions (35.09%). Therefore, the overpaid solidarity tax is refunded to employer at next year.

The tax is paid for the income exceeding the maximum amount of the social security contributions object. In 2019 and 2020 the ceiling is raised to EUR 62 800 per year (in 2018 was EUR 55 000 per year). The tax period is the calendar year.

The purpose of Solidarity tax is to eliminate existing regressivity in the labour tax system and to equalize the tax burden on labour between low-wage earners and the high wage earners. This problem appeared when the social contribution ceiling was re-introduced in 2014.

Solidarity tax applies to all socially insured individuals – employees, self-employed, if their income over a calendar year exceeded the maximum amount of mandatory contribution of the statutory social insurance. Employers are also subject to solidarity tax (in the same way, as they are liable for paying employer social insurance contributions).

2.3.1. Payroll tax

The Business risk fee is paid in the state basic budget, and then transferred to the Employee claim guarantee fund, which is administrated by the state agency “Insolvency administration”. The Insolvency administration is a public institution controlled by the Ministry of Justice.

If an enterprise is insolvent, the Insolvency Administration satisfies employee claims for their unpaid salaries, compensations for the paid annual leaves and compensations for dismissal in case of the end of the employment relationships.

The Business risk fee does not confer entitlement to any kind of social benefits.

The Business risk fee is a constant payment for a person EUR 0.36 per employee per month.

3.2. Transfers for dependent children

From 2015, support for families has been introduced through differentiated family state benefits:

From March 1, 2018 an additional allowance for families is paid:

For example, for family with six children additional allowance is EUR 216 per month (66 (for 3) +50+50+50).

The state pays family benefits to all children until they reach the age of 15. Children enrolled in basic or secondary schools or vocational education institutions operating on the basis of basic education have the right to receive family benefits until the age of 20.

In addition there are four other types of family benefits for which payment depends on either the age of the child(ren) and/ or the status of the person(s) looking after them: maternity and paternity benefit; childbirth benefit; parental benefit; child care benefit (additional benefit for child with disabilities). These are not included in the modelling.

The differential non-taxable minimum is increased - in 2018 ranges from EUR 0 to 200 per month, in 2019 - from EUR 0 to 230 per month and in 2020 - from EUR 0 to 300 per month. In 2017, non-taxable minimum ranged from EUR 60 to 115 per year.

The tax allowance for each dependant is raised - in 2018 to EUR 200 per month, in 2019 to EUR 230 per month and in 2020 to EUR 250 per month. In 2017, it was EUR 175 per month.

The non-taxable minimum for pensioners is increased - in 2018 to EUR 250 per month, in 2019 to EUR 270 per month and in 2020 to EUR 300 per month. In 2017, it was EUR 235 per month.

5.1. Average gross annual wage earnings

In Latvia the gross earnings figures cover wages and salaries paid to individuals in formal employment including payment for overtime. They also include additional bonuses and payments and other payments such as for the annual and supplementary vacations, public holidays, sick pay (sick-leave certificate A), payment for public holidays and other days not worked, social security compulsory contributions paid by the employees and personal income tax, as well as labour remuneration subsidies.

5.2. Employer contributions to private pension and health schemes

Some employer contributions are made to private health and pension schemes but there is no relevant information available on the amounts that are paid.

The equations for the Latvian system are mostly on an individual basis.

The functions which are used in the equations (Taper, MIN, Tax etc) are described in the technical note about tax equations. Variable names are defined in the table of parameters above, within the equations table, or are the standard variables “married” and “children”. A reference to a variable with the affix “_total” indicates the sum of the relevant variable values for the principal and spouse. And the affixes “_princ” and “_spouse” indicate the value for the principal and spouse, respectively. Equations for a single person are as shown for the principal, with “_spouse” values taken as 0.