3. Ports sector

This chapter provides an economic, institutional, and legal overview of the ports sector in Brazil. The water transport sector has a fundamental role in Brazil’s foreign trade and in its economic development: it is responsible for the flow of more than 98% of Brazilian exports and more than 92% of imports in terms of volume. Three main bodies are responsible for the creation of policies and guidelines for the port sector, while specific state-owned enterprises are responsible for exercising the functions of port authorities in public ports, and the Agência Nacional de Transportes Aquaviários as an independent regulatory agency is in charge of implementing the Ministry’s policies for ports and waterways.

3.1.1. Economic overview

Ports can be defined as places “having facilities for merchant ships to moor and to load or discharge goods or passengers to or from seagoing vessels” (OECD, 2002[1]). Whether maritime, inland or river, ports play an important function in the economic development of countries and regions by facilitating large-scale domestic and international trade in goods. Port infrastructure supports customers such as freight shippers, ferry operators and private boats (OECD, 2011[2]).

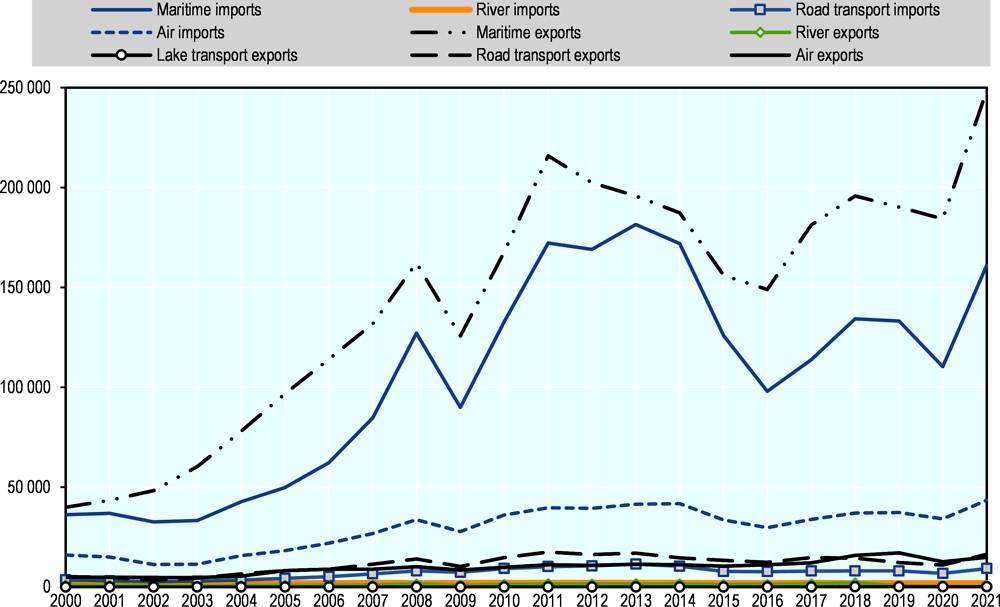

Although it may not represent a large portion of GDP (0.16%),1 the water transport sector has a fundamental role in Brazil’s foreign trade and in its economic development.2 It is responsible for the flow of more than 98% of Brazilian exports and more than 92% of imports in terms of volume. In 2021, exports and imports by maritime transport amounted to more than 851 billion net kilogrammes and USD 409 billion freight on board (FOB), an increase of 169% and 438%, respectively compared to 2000 data (Figure 3.1 and Figure 3.2).

Source: (Ministério do Comércio Exterior, 2022[3]).

Source: (Ministério do Comércio Exterior, 2022[3]).

In comparison to other regions and countries, Brazil plays an important role in world trade. In 2020, it accounted for 776 million tonnes or 7.3% of the global volume of loaded goods in maritime trade (Table 3.1). This volume saw 6.36% growth between 2014 and 2020, above the average of developing countries in the Americas and in Africa, but below those in Asia.

Prior to the COVID-19 pandemic in 2020, container shipments in seaports had continually grown between 2001 and 2020 around the world (except in 2009, after the 2008 crisis) both in terms of gross tonnage and the number of 20-foot equivalent units (TEUs). In 2020, nearly 750 million TEUs were loaded and unloaded in countries for which data were available, with Brazilian ports accounting for around 1.3% of total TEUs handled around the world in 2020.

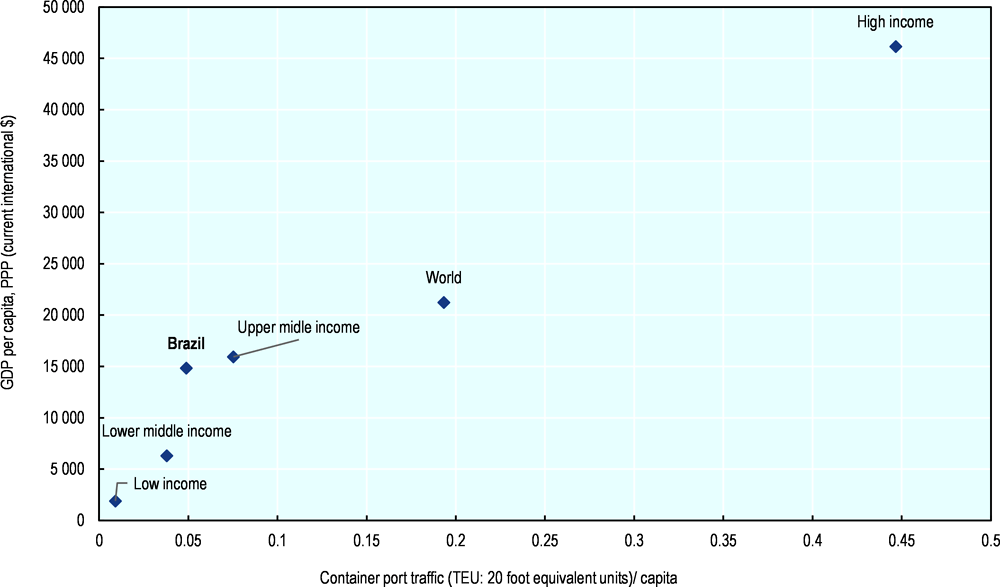

Containerised trade is positively related to GDP growth. The number of TEUs transported has a positive effect on trade flow between countries, which in turn has a positive impact on real GDP growth (CEPAL, 2020[6]) (Michail and Batzilis, 2021[7]). Figure 3.3 shows this positive correlation between countries with higher container port throughput and those with the highest GDP per capita.

Source: (UNCTAD, 2022[4]) and OECD calculation.

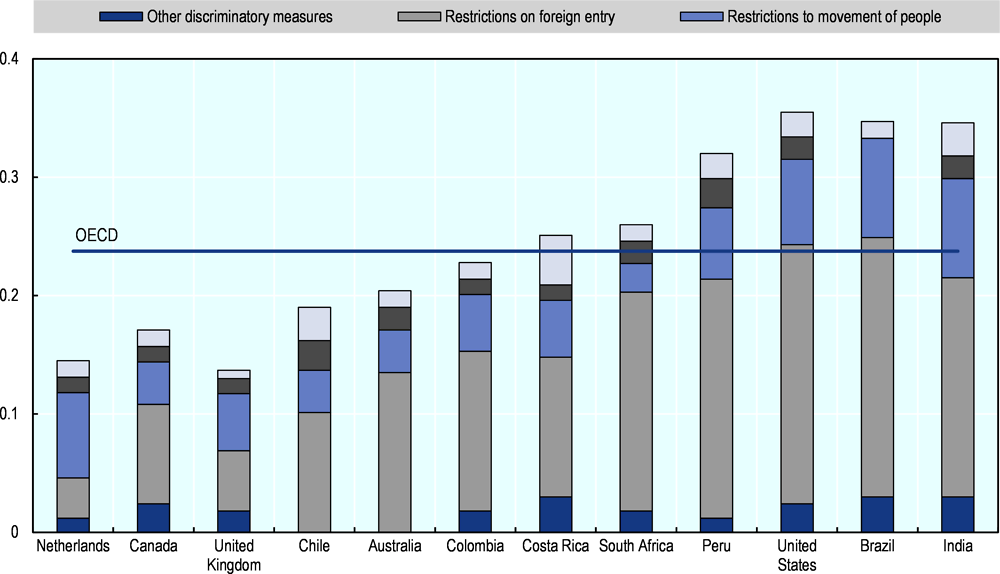

Regarding the regulatory environment, the maritime transport service sector in Brazil appears to be less open to trade and investment than the OECD average or other comparable economies, such as Chile, Colombia, and Costa Rica. This is shown by the OECD Services Trade Restrictiveness Index (STRI), which provides information on regulations affecting trade in services in different sectors.3 The STRI scores Brazil above other countries (Figure 3.4). In this respect, restrictions on foreign entry play an important weight on the composed result.4

Source: (OECD, 2022[8]).

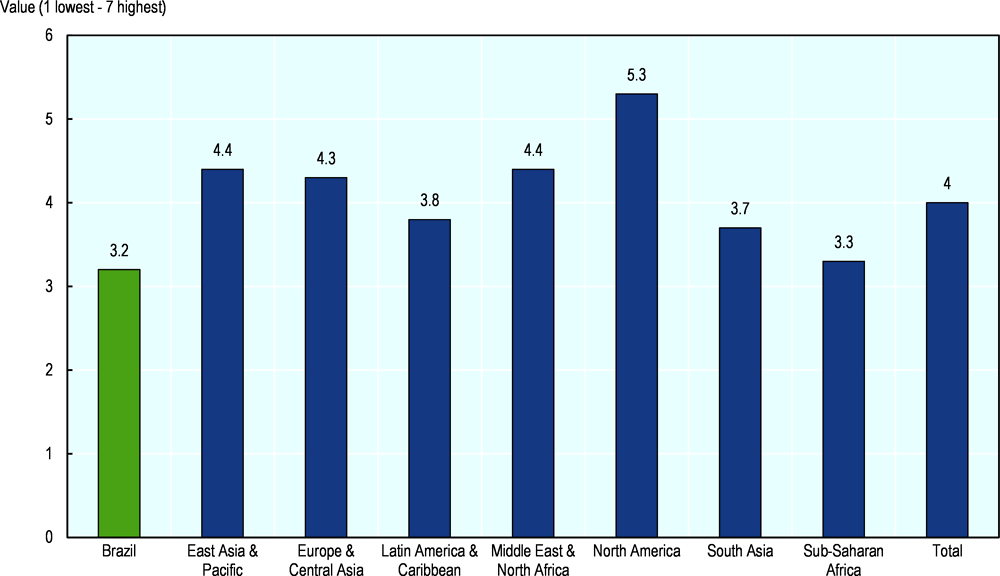

Brazil’s performance indicators for maritime transport are low. The World Economic Forum’s Global Competitiveness Index (GCI)5 ranks the efficiency of Brazilian seaport services at 104 out of 138 analysed countries, with a score of 3.2 on a scale of 1 (worst) to 7 (best). This is below both the average of all other regions in the world and below the world average of 4.0 (Figure 3.5). This inefficiency can also be seen in the GCI’s ranking of countries by income level (Figure 3.6). Brazil scores below average of other countries in its income group (upper-middle income), which was 4 in 2019.

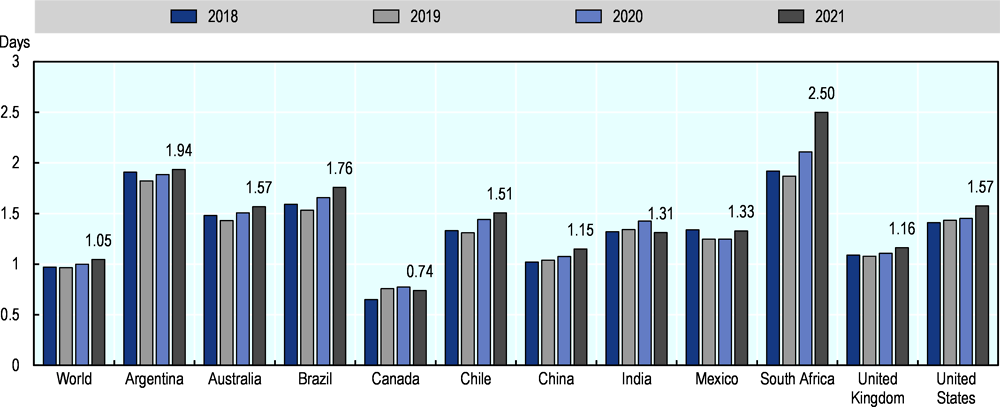

An alternative proxy measure of efficiency is time spent in ports; shorter times signal possible stronger port efficiency and trade competitiveness (UNCTAD, 2022[4]). Ships spent on average 1.76 days in Brazilian ports in 2021; this compared with a global average of 1.05 days; 0.74 days in Canada; 1.15 in China; and 1.16 in UK ports (Figure 3.7). Among the main reference countries, only South Africa (1.94 days) and Argentina (2.5 days) performed worse.

Source: (UNCTAD, 2022[4]).

Growth of the sector

In the early 1990s, Brazil undertook a reform process for the ports sector, aiming to promote competition by fostering entry and investment. The extinction of Portobrás, a state-owned company that had centralised ports’ administrative activities since 1975, and the enactment of Law No. 8.630/1993 enabled the private sector to invest in, lease and operate national maritime ports (AZEREDO, 2004[10]) (SILVA and FILHO, 2013[11]) (CADE, 2017[12]). In 2001, the creation of the National Agency of Waterway Transport (ANTAQ) enhanced legal certainty and fostered investor confidence. Continuing this process, in 2013, Brazil established a new regulatory framework (Law No. 12 815/2013) for the ports sector aiming to further enhance competitiveness and increase private-sector involvement in the supply of port infrastructure.

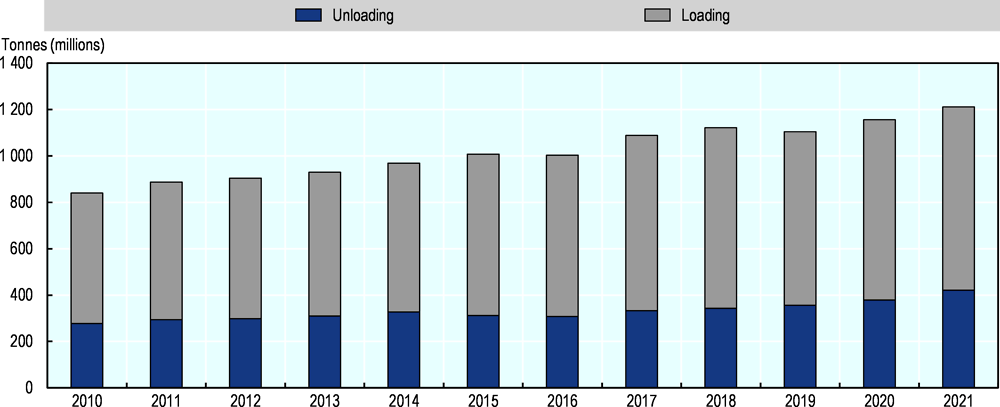

This new regulatory framework was a response to a lack of sectoral investment and growth. Since these reforms, the volume of cargo handled in Brazilian ports has increased and reached more than 1 200 million tonnes, an increase of 45% compared to 2010 levels (Figure 3.8).

Source: (ANTAQ, 2022[5]).

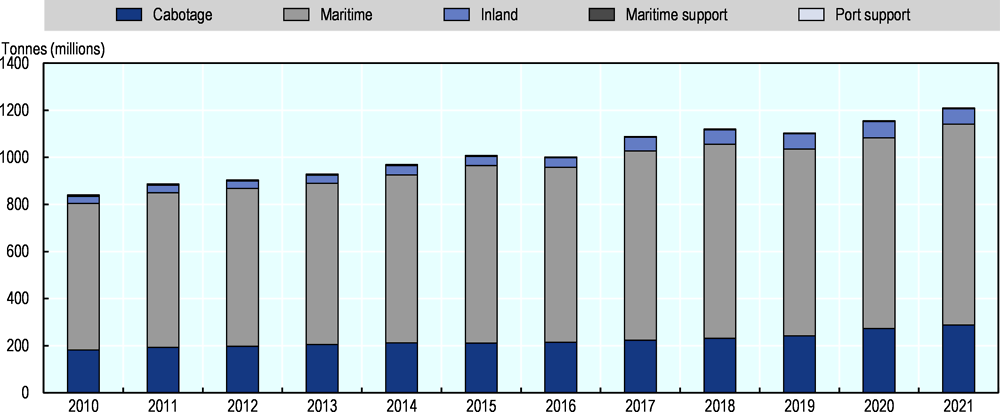

Maritime cargo is the main contributor to the overall amounts handled in Brazilian ports. In 2021, 71% of cargo handled in Brazilian ports was transported by maritime vessels, followed by domestically transported cargo (cabotage), which accounted for 24% of the total (Figure 3.9).

Source: (ANTAQ, 2022[5])

Market structure

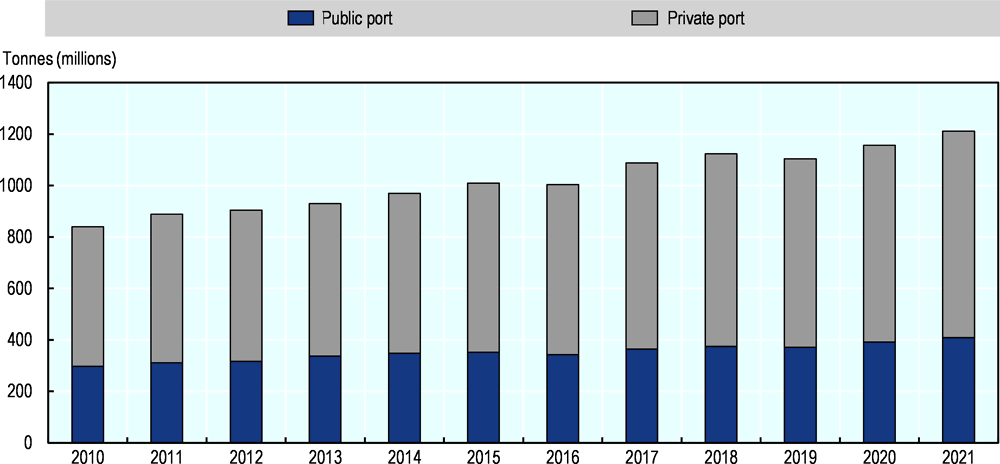

The regulatory framework enacted in the 1990s resulted in an increase in the number of authorisations for the construction of private-use terminals. In 2021, Brazil had 170 private-use terminals (TUPs) in operation subject to a fully privatised model and 125 terminals in public ports under a landlord model (ANTAQ, 2022[5]).6 Private ports were responsible for 66% of the cargo handled in Brazilian ports in 2021, against 34% for public ports (Figure 3.10).

Source: (ANTAQ, 2022[5]).

Among the ten main ports in Brazil (measured in gross tonnage handled), five are public ports and five private terminals (Figure 3.11). The leading private port is the Ponta da Madeira maritime terminal, located in the northeast of the country, which specialises in handling ore and has experienced rapid growth since 2014. The Port of Santos, southwest of São Paulo, has the largest container throughput in the country, accounting for around 30% of all containers handled in Brazil in 2021.

Source: (ANTAQ, 2022[5]).

The port sector is becoming increasingly vertically integrated From 1996 to 2016, 24 of the 81 merger cases related to port services analysed by CADE involved vertical integration. The most common cases of vertical integration in port industry are the ones related to production and export of bulk of plant origin (agricultural commodities) and the storage and movement services of these products in port terminals. It is common, in these markets, that large exporters of commodities hold equity interests, or even full control, in port terminals for production flow, which may be for captive use by shareholders or may be offered to some extent to store goods of other independent exporters (CADE, 2017[12]).

Vertical integration in Brazil has different roots that vary depending on the type of cargo. Before 2013, the regulation of private terminals established that the latter needed to prioritise their own cargo and were not allowed to handle only third-party cargo. Such regulatory evolution is one of the reasons why a considerable number of private terminals are still today part of vertically integrated companies in Brazil. For example, Vale integrates and manages most of the logistics chain for exporting minerals in Brazilian territory, including extraction, rail transport, movement in port terminals in maritime transport in own ships. In the vegetable bulk segment, which accounts for 264 million tonnes or 20% of the cargo handled in Brazilian ports in 2021 ((ANTAQ, 2022[5]) the logic of vertical integration also plays an important role. Companies like Bunge, ADM and Cargill have their own terminals in different regions of the country. In addition, they invest in other structures in the supply chain such as warehousing and intermodal transhipment (Bunge) and, river transport (ADM) (CADE, 2017[12]). As to liquid bulk terminals, vertical integration is also widespread, with companies producing commodities acting in the port operation and in other segments of the production chain (Coutinho, 2014[13]).

In line with this worldwide trend, in the Brazilian containerised cargo market, vertical integrations occurred between large domestic and foreign cargo shipping companies. For instance, TIL (in which MSC has a 60% stake) operates the Portonave private terminal, in Navegantes – SC, located in Itajaí Port Complex, region where the public terminal is also leased to APM Terminals. Maersk and MSC are partners in the port of Santos but compete directly in the containerised cargo market in Santa Catarina. Also, in the State of Santa Catarina, the private terminal of Itapoá has Aliança Navegação e Logística (belonging to the shipping group Hamburg Sud, now part of Maersk) among its shareholders (Jucá, 2021[14]). Other container terminals (partly) operated by shipping lines are in Rio de Janeiro (TIL), Pecém (Maersk) and Natal (CMA CGM).

The tendency of vertical integration is a world phenomenon which is also related to the increase of the use of mega-vessels. Given the amount of cargo transported, port operations may have the potential to create bottlenecks, eroding service reliability and limiting the efficiency in the use of this type of vessels. Aware of such relevance and aiming to boost operational performance and reduce physical bottlenecks (e.g. undersized infra- and superstructures, nautical accessibility), shipping companies have started to acquire container terminal facilities around the world. By acquiring terminals, carriers have also the opportunity to have more control of the manpower costs and invest in correlated business (OECD, 2017[15]) From 2002 to 2016, the share of carrier-controlled terminal operators has increased from 18% to around 38% globally (ITF, 2018[16]). This share is around 14% in Latin America.

While, as mentioned, vertical integration gives carriers the possibility to better co-ordinate their shipping activities as part of a whole logistics chain, it can lead to discriminatory treatment – as the carrier can, as terminal, towage or logistics operator, provide worse services to competing carriers, especially in concentrated markets. For example, carriers often use their terminals as leverage to cut rates in independent terminals and play out ports against each other (ITF, 2018[16]).

When looking at CADE’s decisional practice, from 1998 to 2018, 8 of 13 mergers cases related to container terminals involved some form of vertical integration. The main concern is the possibility of foreclosing upstream or downstream markets and induce rivals’ cost increases. If the port terminal of a group started to offer less efficient services for ships belonging to rival groups, this could lead to subsequent delays and cost increases for transporters. However, the possibility of such conduct was ruled out due to the reasons raised in the cases such as the existence of container terminals in nearby ports. The existence of idle capacity at container terminals would allow absorption of demand deviations in the event of a terminal closure to rival companies; it would not be economically viable for port terminals to operate only with cargo from the company of its economic group, as these would not have enough volume; in ports where corporate control is shared, market foreclosure of some shipowners would not be of in the interest of the other partners which do not operate maritime transport; in cases of Vessel Sharing Agreement, the choice of ports of passage is made jointly by the parties, so there would be no certainty that all participants in the agreement would agree to use integrated terminals owned by one of the participating companies. (CADE, 2018[17])There is an investigation on going (08700.003945/2020-50) about an allegation of practices of direct and indirect discrimination arising from the vertical relationship between ship owners and terminals, evidenced by dominant position at the port of Santos.

Generally, vertical integration is subject to merger control rules. In general, the acquisition of controlling stakes in other parts of the transport chain should thus be notified to the competent national competition authority, which will evaluate whether there are any possible antitrust concerns with the transaction (OECD, 2021[18]) In Brazil, the Law 12.529/2011 establishes an ex ante control of concentrations and imposes a duty to notify to CADE acts of economic concentration.

Concerning to the legislation, OECD countries have different strategies to deal with the vertical integration’s risks. Some countries define explicit port hierarchies that help focus public infrastructure investments and prevent shipping companies or large shippers from playing off ports against each other. (OECD, 2021[18])In Brazil, there is no legislation specifically restricting vertical integration between port terminals and carriers. Brazilian regulation seems to analyse vertical integration concerns on a case-by – case basis, rather than imposing general restrictions.

The Law 10233/2001 (which created ANTAQ) allows the transfer of ownership of concession or permission granted, preserving its object and contractual conditions if it is authorised by ANTAQ. The Brazilian legal system includes regulators of sectorial activities (regulatory agencies) and a horizontal competition defence system that is responsible for “prevention and repression of infringements against the economic order” (Article 1 of Law No. 12 529/11).

ANTAQ tried to introduce some form of regulation of vertical integration in 2014, when it sent to public consultation the Resolution 3 708 (which has never come into force). Article 18 established that the public notice may restrict or prevent the participation of companies’ members of economic groups that already operate in the organised port area; in the area of influence of the organised port; or in other economic activities that represent forms of vertical integration. In addition, to prevent the risks of vertical integration, the lease of terminals in public ports was subject to safeguards to avoid creating intra- and inter-port links, giving a regulatory role to ANTAQ, the Federal Court of Accounts and SEAE.

Recent trends

Private port terminals have been the main investment driver in the Brazilian port sector in recent years, particularly after 2013 and the enactment of the Ports Law (see Box 3.1). According to data from the Association of Private Port Terminals (ATP), founded in 2013 to represent the interests of the private port sector, the investment portfolio of private ports since the law has totalled BRL 45.83 billion, of which BRL 43.6 billion (95.9%) were investments in private-use terminals (TUPs); BRL 1.5 billion (3.35%) were in cargo transhipment stations (ETC); and BRL 333.8 million (0.73%) were in port tourism facilities (IPTur).7

3.1.2. Institutional overview

The institutions responsible for issuing or enforcing rules, instructions and guidelines in the ports sector play a significant role in the functioning of the market and can ultimately affect competition.

This section provides an overview of institutions responsible for issuing and implementing regulations and overseeing the ports sector in Brazil.

Three main bodies are responsible for the creation of policies and guidelines for the port sector.

Ministry of Infrastructure (Ministério da Infraestrutura), responsible for issuing guidelines and policies for the development and promotion of the port sector and maritime, fluvial and lacustrine port installations. The ministry is also responsible for the execution and evaluation of programmes, measures and projects that support the superstructure8 and infrastructure development of ports and maritime, fluvial and lacustrine port installations.

National Commission of Port Authorities (CONAPORTOS), responsible for co-ordinating and evaluating the efficiency of measures related to activities performed by public bodies and entities in ports and port facilities. Restructured by Decree No. 10.703/2021, it is composed of several public bodies9 and chaired by the Ministry of Infrastructure.

National Secretariat of Ports and Waterway Transports (SNPTA), responsible for establishing guidelines for awarding grants and for tax proposals in the waterway transport sector; proposing priorities in the investment programme to aid the creation and implementation of the Ministry of Infrastructure’s strategic planning regarding waterway and port transport; and elaborating grant plans and proposals for the infrastructure and service exploitation in the port sector and maritime, fluvial and lacustrine port installations.

Six state-owned port enterprises (Companhia Docas), linked with the Ministry of Infrastructure, are responsible for exercising the functions of port authorities in public ports, and the management and supervision of port facilities and public infrastructure within ports. The six Companhia Docas are: Companhia Docas do Pará; Companhia Docas do Ceará; Companhia Docas do Rio Grande do Norte; Companhia das Docas do Estado da Bahia; Companhia Docas do Rio de Janeiro; and Companhia Docas do Estado de São Paulo. Companhia Docas do Espírito Santo was recently privatised (see Section 3.1.3).

Based on a review of the regulation and the procedures of a significant number of institutions in the federal government, there has been an effort since 2011 to integrate the procedures of the governmental bodies into a project called Porto Sem Papel (port without paper). It consists of a digital database that centralises the information and documentation necessary to speed up the passage of goods through Brazilian ports. This single window allows companies to submit information (such as declarations, electronic consents for vessel stay, and certificates of origin and invoices) simultaneously to all relevant entities: the port authorities; National Health Surveillance Agency (ANVISA); the Federal Police (Polícia Federal); Ministry of Agriculture; the system for agriculture and international livestock surveillance (Vigiagro); the Brazilian Navy’s Maritime Authority; and the Brazilian Federal Revenue Service’s Customs Authority (Receita Federal). By 2021, the system had been implemented in 34 Brazilian ports (Ministério da Infraestrutura, 2021[20]). In the Port of Santos, the system resulted in a reduction of waiting times and congestion, which before its introduction was costing BRL 115 million a year (OECD, 2016[21]). The expansion of the project could lead to the integration of further governmental bodies, which will continue to reduce the administrative burden.

The National Agency of Waterway Transportation (ANTAQ), an independent regulatory agency of the federal government, is in charge of implementing Ministry of Infrastructure policy on ports and waterways in accordance with the principles and guidelines established by legislation (see Box 3.2). It is also responsible for inspecting, regulating and controlling the provision of services of waterway transport, and the operation of port and waterway infrastructure. In addition, ANTAQ examines the activities performed by the administration of public ports (referred to as “organised ports” in Brazilian legislation), port operators, leaseholders, and authorised port installations. The majority of sectoral regulations are issued by ANTAQ.

Regulatory agencies often find themselves under pressure from sectoral stakeholders and interest groups, which can subject them to different forms of control. Independence is crucial to ensure that the regulator can efficiently exercise its mandate to promote widespread access to services at competitive prices in its specific market (OECD, 2016[21]).

As defined by Law No. 10.233/2001 and Law No. 13.848/2019, ANTAQ has formal administrative independence in the decision-making process from the Ministry of Infrastructure. This independence is achieved thanks to different factors in line with international best practices. First, directors in charge of the agency have a fixed mandate, which prevents them from being influenced by political pressures and allows them to fulfil the objectives set by the legislation that created the regulatory agency. The designation of directors follows a centralised process, in which they are proposed and appointed by the president after Senate approval.

Second, ANTAQ has a multi-member decision making body. In general, boards are considered more reliable for decision making with collegiate decisions ensuring a greater level of independence and integrity than decisions taken by individuals, which are potentially subject to greater pressure from government and regulated industries (OECD, 2016[21]) One of ANTAQ’s major differences from other regulatory agencies in Brazil is that its collegiate board consists of a director general and two directors; all other regulatory agencies are composed of a director general and four directors. Stakeholders say that the reduction, occurred before the creation of the agency, during the legislative discussions, from five to three directors, which took place due to budgetary restrictions, could facilitate “regulatory capture” of ANTAQ by regulated industries. The organisational structure also includes an attorney, an ombudsman and an inspector general, whose duty is to supervise the agency’s functioning and its administrative and disciplinary proceedings. To solve this issue, in June 2022 the Provisional Measure 1120/2022 was proposed to introduce the possibility to have more directors in the collegiate board. The proposal is currently being discussed before the Brazilian Congress.

Third, in line with international best practices, ANTAQ leaders must go through a “cooling off” period before accepting jobs in either the government or regulated sector after their term of office. Having no restrictions on pre- or post-employment of agency staff increases the risk of “revolving doors” and conflicts of interest with industry (OECD, 2016[21]).

In selecting a regulator’s leadership, international best practice suggests transparency in the nomination and appointment process. According to the OECD Regulatory Policy Outlook 2021, 47% of regulators in OECD countries are now appointed by an independent panel (OECD, 2021[22]).

Promoting a culture of independence in regulatory agencies throughout the different phases of the regulatory cycle generates competition between regulatory agencies and thus economic efficiency. One important landmark, contained in Law No. 13.848/2019 (Law of the Regulatory Agencies), was the legal establishment of the model interaction between regulatory agencies and the bodies of competition defence. The law established ANTAQ as incumbent monitor of market practices of agents in the regulated sectors, in order to assist competition bodies in complying with relevant legislation. CADE is responsible for applying competition legislation in regulated sectors, for analysing mergers, and instituting and instructing administrative proceedings to investigate infringements. The regulatory agency may also help with technical opinions.

Figure 3.13 summarises the hierarchy and relation between regulatory bodies in the ports sector.

3.1.3. Overview of the legislation

The OECD has identified 77 pieces of legislation related to the ports sector. It should be noted that the sector is heavily regulated and that the services provided in publicly operated ports are more regulated than the services in private ports (TUPs). Since the provisions regulating public ports are more restrictive than those for private ports and in light of the purpose of this project, which aims to identify unnecessary regulatory restraints on market activities and develop alternative measures that still achieve government policy objectives, the OECD has found more restrictions concerning public ports (53 provisions) than private ports (16 provisions).

Law No. 12.815/2013 (Ports Law) provides the legal framework for the port sector in Brazil. It regulates the direct or indirect operation by the federal executive branch of ports and port facilities, and the activities of port operators. It covers the majority of the relevant issues for ports, such as the definition of terms, leasing and authorisation instruments, and issues related to 1) the administration of the public ports; 2) port operation; and 3) port workers.

The Ports Law establishes two different regimes: one for public ports, another for private ports (TUPs). Law No. 12.815/2013 provided for private terminals to operate outside public ports for the first time.10 More specifically, terminals within public ports operate under a public-lease regime, while terminals in private ports are subject to a different regulatory regime and authorisation process. This regulatory asymmetry gives rise to competition concerns when TUPs operating in a private and less regulated regime compete against more regulated terminals located within public ports (see Box 3.7).

Public ports operate under a landlord model that was first established by Law No. 8.630/1993. This model, which is still in use today, sees the federal executive branch provide port infrastructure, highway and waterway access and grant usage rights. Federal port companies – or Companhias Docas – are the port authorities within public ports. As noted in Section 3.1.2, these 100% state-owned companies are responsible for managing public ports, including those in Rio de Janeiro, Santos, Salvador, and Belém. In some cases, public ports are managed by federal states or municipal governments, which establish their own management entities – such as companies or government divisions – as is the case for the ports of Rio Grande, Itaqui, Suape, Paranaguá, among others.

The 2013 law’s main objective was to attract private investments by enabling the private-sector operation of port activities. It provided that private ports be subject to a fully privatised model that includes all investment in superstructure, infrastructure and equipment. Port operation and administration are also provided by the private stakeholder.

While the Ports Law allowed for public-port concessions in 2013, the first concession in Brazil was not granted until 2022, with others concessions scheduled (Box 3.3).

Following the publication of the Federal Development Strategy in October 2020, Brazil is planning to privatise the Companhias Docas, the state-owned enterprises (SOEs) active in the ports sector. These mixed-capital companies were created to operate in port management and until 1990 were linked to Portobrás. From 1990 to 2007, they were controlled by the Ministry of Transport, before moving under the aegis of the Secretary of Ports of the Presidency of the Republic from 2007 to 2016. They are currently tied to the Ministry of Infrastructure (CADE, 2017[12]).

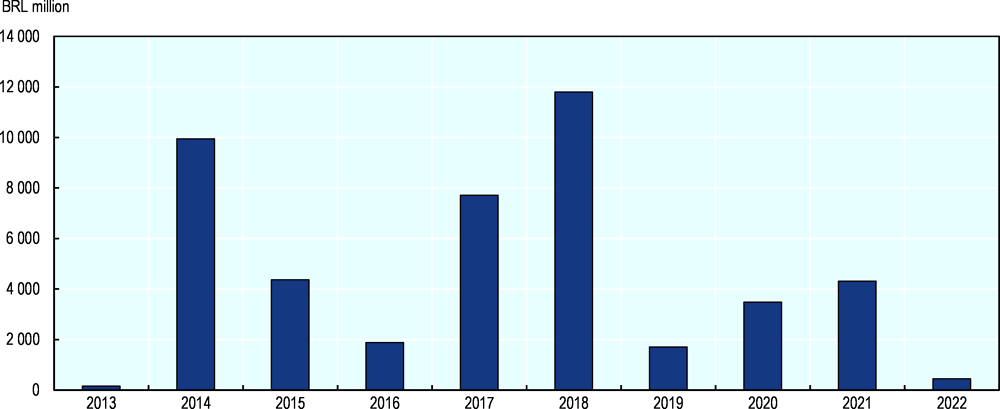

In 2020, the Companhias Docas only invested BRL 35.8 million, the lowest amount in the last decade. This was, for example, less than 10% of total investment in 2014 of more than BRL 492.8 million (Table 3.3). This decrease in investments can be explained by the lack of resources, since these companies have accumulated significant losses in recent years, a trend that was reversed in 2019 and 2020, with the professionalisation of their management, a preparatory step towards their privatisation.1

The first privatisation of a Companhia Docas took place in March 2022 with a 35-year concession of the Companhia Docas do Espírito Santo (Codesa), the owner of the port complex of Vitória, south-east Brazil.2 The second concession will be the Port of Santos, the largest port in Latin America, with a total throughput of more than 107 million tonnes (BNDES, 2021[26]), which is scheduled for the second semester of 2022. The draft of the public notice, among other documents, was discussed at a public hearing and consultation in March 2022. A public hearing for a third concession, for the Port of Itajaí, took place in April 2022. São Sebastião Port will also be conceded, and the public consultation and public hearing took place in February 2022. The next scheduled concessions are for the Ports of Salvador, Aratu-Candeias and Ilhéus, including the privatisation of Codeba, an SOE and port authority in north-east Brazil. The Brazilian Development Bank (BNDES) is conducting studies to this end and public hearings were scheduled for the second semester of 2022 (BNDES, 2022[27]).

← 1. The six SOEs responsible for managing public ports made losses of BRL 1.042 billion in 2018. In 2019, they had a BRL 911 million surplus and in 2020 the surplus was BRL 162.3 million, as they had to assume extraordinary expenses, such as the agreement to remedy the Portus pension fund’s actuarial deficit and voluntary redundancy programmes.

← 2. Codesa is responsible for managing the ports of Vitória and Barra do Riacho. According to preliminary studies conducted by BNDES, the four ports managed by Codesa have a diversified cargo profile (liquid fuels, dry bulk, pig iron, fertilisers, and containers), handle about 7 million tonnes of gross weight annually, and had BRL 155 million in total revenues in 2019.

The Ports Law has been gradually updated over the years, and relevant changes that aim to reinforce freedom of pricing in port operations have been implemented since 2020 (Box 3.4).

Aiming to attract more competition and dynamism to the sector, the Federal Government has made several changes to the Brazilian Ports Law (Law No. 12.815/2013) and decree (Decree No. 8.033/2013). The amendments were provided for in Law No. 14.047/2020 and Decree No. 10.672/2021.

The new law introduced important changes that aimed to bring greater efficiency and dynamism to the management of public ports. The changes brought by the 2020 law reinforced the logic of freedom of pricing in port operations and sought to limit practices harmful to competition (PPI, 2020[28]).

In order to simplify the leasing contracts of the port facilities, some contract clauses (e.g. on reversal of public assets) are no longer considered as essential (PPI, 2020[28]).

The new amendments also provided the regulator ANTAQ with more tools to encourage the use of idle areas in ports and allow interested parties to test the feasibility of operating there for a maximum period of 48 months. If more than one company is interested and it is not possible to grant them all the temporary use of such areas, the port administration can promote a simplified selection process to choose the project that best meets the public and port interests. After the expiration of the contract, if the cargo activity is considered viable in the formerly idle area, the government will hold a standard tender for the lease. The change lifted one barrier to competition, which had been a limited number of suppliers (PPI, 2020[28]).

Other amendments include the possibility of not running a competitive tender when it is proven that only one stakeholder is interested in exploring an area after a public call issued by the Port Authority. Finally, there was a point of legal uncertainty that the new law sought to solve by making explicit that the contracts signed between the concessionaire of the public port (exercising the role of port administration) and third parties are subject to the regulations for private ports (PPI, 2020[28]).

To reinforce the changes, in April 2021, Decree No. 10.672/2021 incorporated the regulatory simplification measures provided by Law No. 14.047/2020 and amended Decree No. 8.033/2013 that regulates the Ports Law. The simplification measures seek to facilitate investments and business activities in Brazilian ports (APEX, 2021[29]).

Source: (PPI, 2020[28]) and (APEX, 2021[29]).

Decree No. 8.033/2013 is important as it specifies the provisions of the Ports Law, detailing the operation of port facilities within the public-port area – such as how to design the public notice, leasing and concessions contracts and contracts of temporary use – and lays down provisions on authorisations and port workers.

The main instruments for planning in the sector are the Zoning and Development Plan (PDZ) for each port complex, the National Plan of Port Logistics (PNLP), the General National Leasing Plan (PGO), and the master plans for each port complex,

Other relevant legislation includes Law No. 10.233/2001, which created the National Agency of Waterway Transportation (ANTAQ), the independent regulatory agency responsible for inspecting, regulating and controlling the provision of services of waterway transports, and the operation of port and waterway infrastructures. In addition, ANTAQ examines activities performed by the administration of public ports, port operators, leaseholders, and authorised port installations. It also issues the majority of resolutions regulating the sector.

New legislation, Law No. 14.301/2022, introduced in January 2022, aims to lift regulatory restrictions on cabotage. Among its objectives are encouraging competition and competitiveness in the provision of cabotage transport services (SNPTA, 2021[30]) (see Box 3.5).

Maritime cabotage is sea shipping operating exclusively between ports in the same country. Historically, foreign vessels had restricted access to cabotage routes, which was often justified for security reasons; more recently, restrictions have been more related to maintaining national fleets and for employment reasons. Concerns about relaxing these regimes are often related to how opening cabotage to foreign operators may reduce operating costs, change employment practices, and weaken labour and safety standards for seafarers (UNCTAD, 2017[31]).

In 2022, the introduction of Law No. 14.301/2022 reformed the cabotage sector’s regulatory framework. It introduced new provisions alongside those of Law No. 9.432/1997, which reserved certain markets for the Brazilian maritime industry. The new regime aims to modernise the sector, mainly by lifting barriers to foreign entrants (PPI, 2019[32]). Research and international case experience suggest that the relaxation of cabotage regimes will improve competition and reduce prices in Brazil (Ipea, 2020[33]).

The main change provided for by the new regime concerns permits to simplify the expansion of cabotage and the entrance of new companies. Pursuant to the new provisions, Brazilian navigation companies (EBN), legal entities created according to Brazilian laws, with headquarters in the country, and no restriction on the nationality of the capital, will be allowed to charter vessels rather than owning them (SNPTA, 2021[30]).

Another amendment concerns the nationality of the crew. The old legislation established that on Brazilian-flagged vessels, the commander, the chief engineer and two-thirds of the crew had to be Brazilian nationals; the new regime relaxed this restriction and established that the commander, cabotage master, chief engineer, and chief engineer must Brazilian.

The expected results from the reform are an increase of 40% of the supply of cabotage vessels and 30% in annual cabotage growth (SNPTA, 2021[30]). However, to the best of the OECD’s knowledge, in the absence of implementing measures, the new regime is not yet applicable.

Sources: (UNCTAD, 2017[31]), (PPI, 2019[32]), (Ipea, 2020[33]), (SNPTA, 2021[30])

3.2.1. Background

While port management models vary across countries, there are four main models depending on the role that the public and private sectors play (Table 3.4).

The landlord model, in which the port’s land remains public but its infrastructure is leased long term to a private operating company, is the most common model in OECD countries, particularly for large and medium-sized ports (OECD, 2018[35]).

In Brazil, ports have recourse to two models: the landlord model for public ports – with a specific legal framework – and a model applying to fully privatised ports (TUPs), with its own legal framework. In 2021, there were 127 terminals in 25 public ports (out of a total of 35 public ports) subject to the landlord model and 170 TUPs in operation under the fully privatised model (ANTAQ, 2022[5]).

In general, despite reforms in recent decades that have opened port services to private participation, international experience shows that it remains more common for the ownership of port authorities to be in public hands. (Notteboom, Pallis and Rodrigue, 2022[36])

Australia has a two-model system similar to Brazil ports. It has a majority of public ports, and only a few private ports that can only deal with one type of cargo (ore). (Chen, Pateman and Sakalayen, 2016[37]).

New Zealand has a different model with full private ownership in which one or more private parties own both the port infrastructure and the land. (Notteboom, Pallis and Rodrigue, 2022[36])

The Mexican model combines elements of the landlord and the private port. Mexican ports are managed by private companies through an entity (Administración Portuária Integral), which is a concessionaire of the Ministry of Communications and Transport (SCT). Alongside the existence of public regulation and supervision, concession agreements also encompass the operation of ports, which is therefore carried out by private players. The institutional port framework is not rigid and different port management models coexist. (Netherlands Enterprise Agency, 2019[38]) In fact, in the two main Mexican ports, the Port of Veracruz, on the Gulf of Mexico, and the Port of Manzanillo, on the Pacific coast, private companies offer all services.

The landlord model is the most common in Europe. For example, the Port of Piraeus in Greece was a tool port until 2002, when it moved to a public landlord model, with the construction of a private terminal with its own physical and operational area within the port. (Britto et al., 2015[39]) The main exception is the United Kingdom, where the model is unique, characterised by significant private participation. There are three main models of port ownership in the UK: (i) private ownership (the government has no ownership interest in this kind of model, it ranges from ports owned by international groups to ports owned by private companies); (ii) trust ports (these are independent bodies which cannot be owned by other companies or shareholders, they are financially and strategically independent statutory corporations); and (iii) local authority owned ports (also operating on a competitive and commercial basis) (Maritime UK, 2022[40]).

Box 3.7 below provides an overview of the regulatory asymmetry that has resulted from Law No. 12.815/2013 and the main differences between leased terminals in public ports and private terminals (TUPs).

Regulatory asymmetry is one of the reasons why investors prefer to have a private terminal instead of competing in a tender to become lessees in public ports (Tribunal de Contas da União, 2020[7]).

Since the enactment of Law No. 12.815/2013, in light of their location within public ports, leased terminals in public ports have been subject to more regulations than privately run terminals (TUPs), which have greater freedom and more flexibility. This asymmetry was motivated by the objective of attracting more private investment, which was the main goal of the law.

Nevertheless, the legislator needs to balance the fulfilment of public-policy objectives – stimulating competition in ports – with the need to avoid harming the provision of public-port services, an objective established by the constitution. This balance is extremely important since competition is not a goal in and of itself and should not jeopardise the achievement of constitutional objectives. These asymmetrical regulations may distort competition between private and public ports and possibly even lead to anticompetitive outcomes in a market with high barriers to entry and a strong tendency towards vertical integration (Fernandes, 2016[14]).

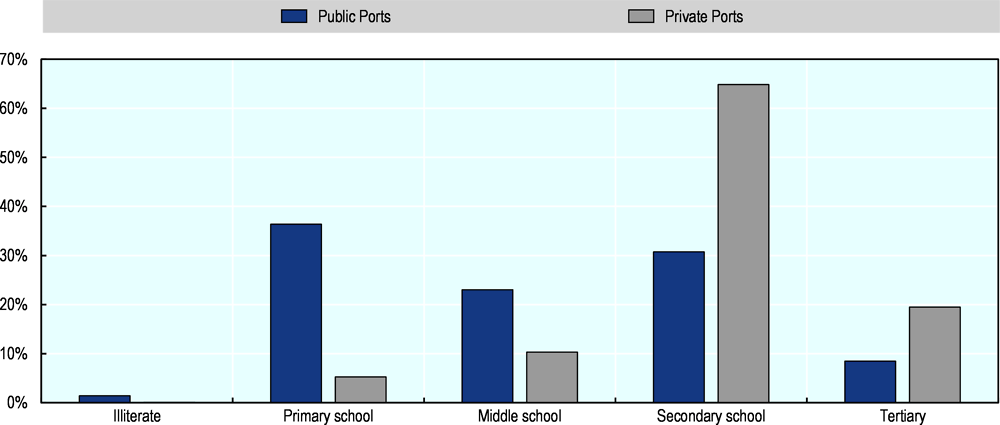

As summarised in Box 3.7, private terminals have a number of advantages over public ports. For instance, the cargo profile is defined by the port investors and may be changed after a communication to ANTAQ, whereas in public ports it is defined in the public notice and changing it requires an authorisation from ANTAQ. In addition, in private ports, workers are freely hired, and tariffs are freely negotiated while in public ports, port workers need to be hired through OGMO (see 3.3.2) and tariffs are set by ANTAQ. In order to guarantee a level playing field between public and private ports and increase competition in the ports sector the restrictions imposed by the legislation on public ports should be removed. This report used the OECD Competition Assessment Toolkit to identify the main legislative restrictions on public ports.11 They are the:

3.2.2. Duration of the process for reviewing tariffs in public ports

Description of the obstacle and policy makers’ objective

In Brazil, private ports can freely set their own tariffs. By contrast, ANTAQ sets the tariffs in public ports for each type of services provided by the port authority, such as those to vessels, port operators or owners of goods. Tariffs are fixed based on the specific characteristics of each public port and cover total costs and a profit margin for investors (Mello and Monteiro, 2020[42]). Tariffs are subject to annual readjustments, based on the Broad Consumer Price Index (IPCA), taking account the percentage variation of price indices incurred in the previous calculation period and any expected productivity gains. Private lessees within public ports are subject to tariff regulation under their respective concession and lease agreements.

Once ANTAQ has set the tariffs, it may also subsequently review them.12

Tariff reviews are common in ports worldwide. A 2015 survey of 67 ports from five continents showed that 60% revised their tariffs annually; 18% had no specific timeline for revisions; and 10% rarely revised their port tariffs (Bandara and Nguyen, 2016[43]).

Fixing tariffs by type of service is common practice in ports around the world. (ESCAP, 2003[44])

In Vietnam, the government provides a price framework, and a port operator can choose to raise or reduce tariffs within this maximum-minimum range (OECD, 2021[45]).

In Mexico, according to the Ports Law, the Secretariat of Infrastructure Communications and Transportation is the competent body to establish the basis for tariff regulation if in a port there is only one terminal dedicated to a specific cargo or one service supplier. For this purpose, the Secretariat may request an opinion from the Competition Commission on this issue (Congreso de los Estados Unidos Mexicanos, 1993[46]).

In Thailand, Singapore, Brunei Darussalam, and South Africa, tariffs are set by a national body, such as the national port authority (Port Regulator of South Africa, 2022[47]). In Malaysia and Cambodia, local port authorities in each port set their own tariff (OECD, 2021[45]).

In Germany, shipowners can enter into civil-law agreements with a port operator and define different tariffs for its use of the port; for instance, it can negotiate discounts if its vessels regularly visit a port. In the Port of Gothenburg, Sweden, individual port authorities establish tariffs and the national government can intervene through regulations of general application (OECD, 2021[48]).

In Portugal, tariffs for port services provided directly by port authorities are regulated by Decree-Law No. 273/2000, which establishes tariff-setting formulas, exemptions and discounts. Each port authority then publishes annually its own tariffs within the rules of that law. If the services are provided by private operators, tariffs are determined in the respective concession and licensing contracts (OECD, 2018[34]).

Although tariff regulation may restrict a port authority’s ability to set tariffs, it may be justified in traditional monopoly sectors where a counterweight is needed to the lack of competing alternatives. The regulation introduced by ANTAQ may prevent port authorities from abusing any market power they hold through their monopoly on the provision of the services in the specific port.

Private ports handle 66% of the total cargo handled in Brazilian ports, although the majority of containerised cargo is handled in public ports as shown in Section 3.1 Market Structure. However, the relevant market is defined by CADE by type of cargo in each port complex and CADE notes that certain ports face significant competition, while others are not subject to any competitive pressure. Due to this fact regulations applying to public ports may be burdensome (e.g. prior price notification as opposed to price regulation) in the event specific public ports are subject to sufficient competitive pressure from TUPs located outside the public port.

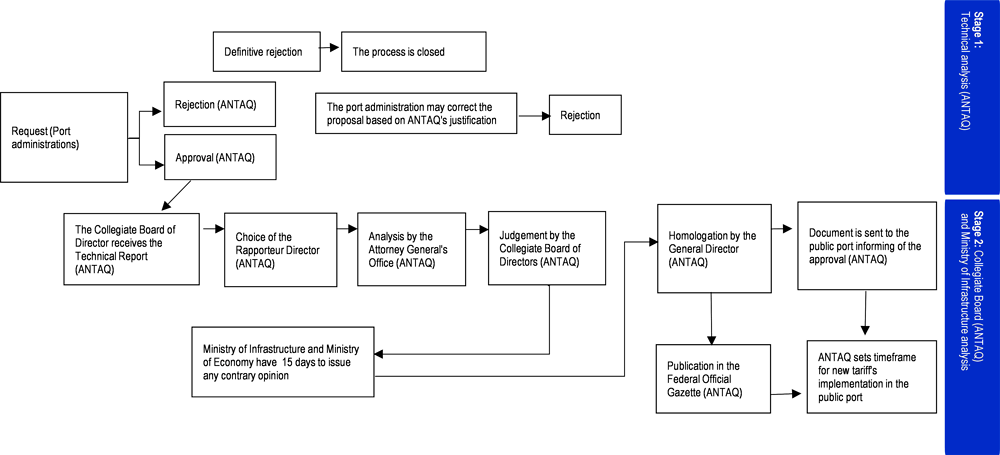

In addition, the process of reviewing tariffs in public ports is complex,13 as it is long and involves ANTAQ, SNPTA, and the Ministry of Economy (Figure 3.14). ANTAQ launches the tariff-review process by giving prior notice to the granting authority at least 15 working days in advance. It analyses proposals received from port administrations for approval and may request additional information and clarifications; it then informs the granting authority and the port administrations about the tariff adjustments.

Source: (ANTAQ, 2021[49])

Port administrations must provide ANTAQ with a justification of their review proposals, showing that the cost increases cannot be absorbed by increases in productivity or operational efficiency and need to be passed on to users of the facilities or service recipients.

Harm to competition

Since the tariff must be approved by ANTAQ and it takes a long time (Table 3.6) for the approval, the proposed tariff may become outdated and based on past costs. A tariff based on past costs may generate a decrease in the quality of the service since the cost cannot be covered. In addition, such lower quality service may lead the user to choose another port (Tribunal de Contas da União, 2020[41]).

Service quality, efficiency and tariffs are key drivers of competition between private and public ports (Tribunal de Contas da União, 2020[41]). Since TUPs outside public ports compete with lessees within public ports, but only the latter are subject to the long and complex tariff-review process described above, public ports may suffer from a competitive disadvantage compared to private ports. This creates another asymmetry which harms competition.

The risk of competitive disadvantage is even more serious since the enactment of Law No. 12815/2013. Following the repeal of the prohibition for private terminals to deal with third-party cargo (see 3.1, Market structure), public port authorities must face indeed competition from private ports (more specifically, from TUPs located outside public ports area) (Mello and Monteiro, 2020[42]). The asymmetrical regulation described in Box 3.7 may translate into an advantage for private ports. For example, given the length of the review process, a tariff based on outdated costs may lead to a decrease in service quality as costs can no longer be covered (Tribunal de Contas da União, 2020[41]). Reduced service quality in turn may then divert users to a competing port.

By contrast, private ports have the flexibility and agility to revise their tariffs quickly whenever needed. As a result, tariffs based on actual costs allow ports to keep their users and attract new ones since port tariff is an important factor in the choice of a port (Bandara and Nguyen, 2016[43]) (De Souza and Pitombo, 2021[50]).

With a need for a more agile process in public ports, the OECD recommends that Brazilian authorities consider reviewing the regime so as to simplify and speed up the revision process for port tariffs. A faster review process may in turn avoid the risk of reduced quality, while removing a competitive disadvantage for public ports when compared to private terminals.

Brazilian authorities may also consider imposing even less stringent regulation (such as prior price notification currently applicable also to TUPs) whenever specific public ports face sufficient competitive pressure.

3.2.3. Instruments to grant private port zones and facilities

Regulatory framework

Three solutions were put in place by Law No. 12 815/2013 for private participation in ports:

In the concession model for public ports the concessionaire acts as both port administrator and port authority, while under the leasing model, the lessee acts only as port operator of zones within public ports.14

The first concession in the country was awarded in March 2022 (Box 3.9).

The first concession awarded in Brazil was part of the privatisation of the Companhia Docas do Espírito Santo (Codesa), the authority of the port complex in Vitória, southeast Brazil (BNDES, 2021[24])

The chosen model is a combination of concession and privatisation. All Codesa’s shares held by the federal government were sold and it will become a private-sector company. The privatisation process was conducted by the sale of all shares held by the federal government following the signature of a concession contract between the executive branch and the company for the operation of the Ports of Vitória and Barra do Riacho for 35 years (Governo do Brasil, 2022[51]).

BNDES conducted preliminary studies and recommended an adaptation of the classic landlord system with a hybrid public-private management system for port terminals awarded through concessions to the private sector. The port authority would be private, but the public administration would still be responsible for strategic planning and assuring national interests (BNDES, 2021[24])

The concession of the Port of Santos, the largest in Latin America, is expected for the second semester of 2022. The draft of the Public Notice for Port of Santos Concession establishes limitations to participation in the bidding, namely that at least 60% of the concessionaire’s capital must be held by economic groups with no conflict of interest related to operations in the Port of Santos; this restriction to ownership extends to the entirety of any economic group (ANTAQ, 2022[52]). The study conducted by BNDES highlights that this limitation aims to maintain a concessionaire’s independence in relation to public ports’ main infrastructure contractors. This keeps the premise of the private landlord model, in which the public-port concessionaire does not intervene directly in port operations since the winning bidder – the future port authority – will not be a company with interest related to operations in the port (ANTAQ, 2022[52]) (BNDES, 2021[26]).

If competition in the market seems impossible or inefficient, the possible solution to deliver advantages to the consumers and address the market failure of a natural monopoly may be competition for the market (OECD, 2019[53]). In such situations, the selection process of operators is vital to preserving the benefits of competition. Leasing is useful in cases where competition in the market may not be viable, for instance, where there are space constraints or safety, security or public-interest concerns as in public ports (OECD, 2021[45]).

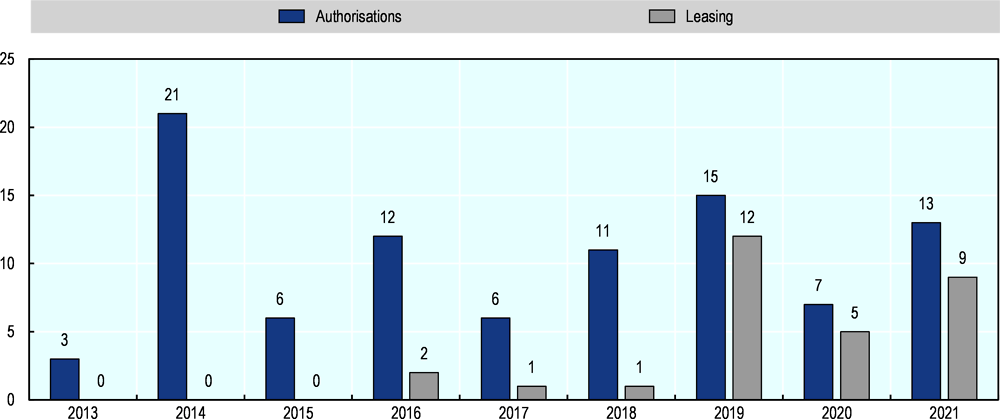

In Brazil, as in the majority of Latin American countries – Chile, Mexico, Costa Rica, Ecuador, Guatemala, Honduras, and Jamaica – leasing is granted after public tenders (Suárez-Alemán, A., 2020[54]). In Brazil, from 2013 to 2021, 30 leasing contracts of cargo terminals in public ports were signed – with the highest number being 12 in 2019.

Source: (ANTAQ, 2022[5]) and (ANTAQ, 2022[6]).

In the leasing, only the management of contracts and assets are delegated to the private concern for a period of up to 35 years, extendable once for a maximum total of 70 years. It is also awarded through a public tender. At the end of the contract, all contracts and assets return to the Federal Executive Branch.

The authorisation requirement is justified by the importance of port services for the economy and because of the use of the national waters. The state can exercise regulation and inspection in activities closely linked to the public interest. Due to their importance to the public interest and their spill over effects for the economy, these types of activities – such as port activities – need regulations that grant the public administration the control of the way these services are offered to guarantee that their provision in the best possible way (Moreira Neto and de Freitas, 2015[55]).

Leasing

Leasing is the instrument established by Law No. 12.815/2013 for the operation and indirect management of public port areas and facilities. The use of leasing aims to allow for the expansion and development of ports while in theory removing the financial and risk burden from governments, encouraging efficiency and reducing monopoly shortcomings (World Bank, 2007[56]). Promoting a competitive bidding process to select the most efficient company is important because leasing grants exclusive rights to operate a specific asset within the public port. In this situation the lessee acts as a monopolist for that the specific area or terminal (OECD, 2014[57]).

Unclear access and participation criteria for bidding can prevent the identification of the most efficient company to hold the leasing contract, while more efficient companies may be excluded from the market, with consequences on service quality (OECD, 2021[18]).

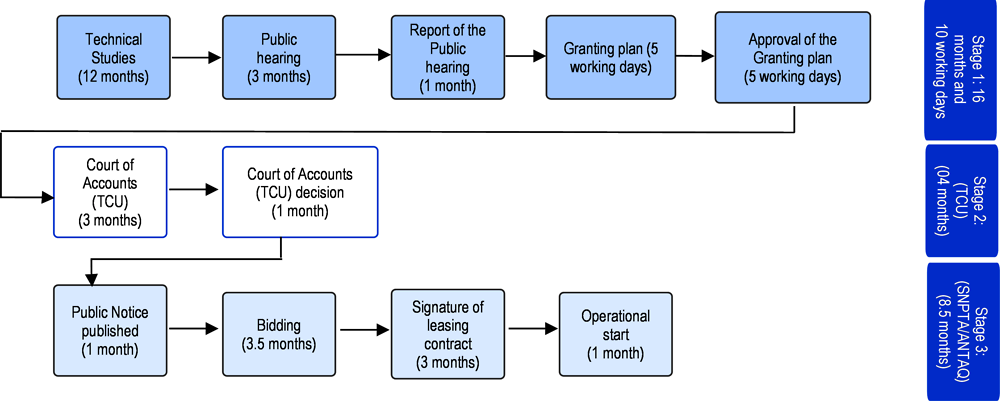

The process for leasing organised port areas and terminals follows the planning guidelines contained in the National Plan for Port Logistics (PNLP), the Master Plan, and each port’s Development and Zoning Plan (PDZ). These documents contain detailed information on the handling and storage capacity at public ports and an analysis of whether such capacity meets current and projected future demand for all load profiles. Figure 3.16 provides an overview of the main steps in a leasing procedure, a process that takes 28 months on average.

Source: OECD, based on (Tribunal de Contas da União, 2020[41])

The leasing process may itself be creating barriers and limiting investment, with some requirements raising barriers to competition and not promoting efficiency and quality in port services.

Any requirements of potential port operators must provide legal certainty and ensure competitiveness, in line with broader port policies. To this purpose, there must be no disproportionate entry barriers or exorbitant clauses in the business relationship between the parties (public body and private lessee). The OECD found four areas that posed barriers to competition:

Centralisation of the bidding process

Description of the obstacle and policy makers’ objective

Before Law No. 12.815/2013, port authorities controlled the leasing of terminals. In order to ensure stronger control over leasing in public ports, Law No. 12.815/2013 established the Federal Executive Branch, specifically the Port Secretariat of the Ministry of Infrastructure, as the granting body for leasing of terminals in public ports. The objective of this provision was to centralise decision-making in the Port Secretariat, partly to ensure an integrated view of sectoral public policy and to develop sectoral expertise. Since the reform, however, the process for assigning leasing contracts in public ports – from technical studies to start of operations – now takes an average of 28 months (Tribunal de Contas da União, 2020[41]).

The main instrument applied to Brazilian public ports is the traditional leasing process described above. However, in order to mitigate the lengthiness of this process, which could result in idleness in public ports, new instruments have been recently introduced. These include the simplified leasing process (established in the art 6 Decree No. 8033/2013) and temporary use contracts (art. 5-D Law 12.815/2013).

The simplified leasing instrument facilitates and speeds up investments in small areas or areas with little economic relevance or that are not on the federal government’s list of priority terminals to be included in the Investment Partnerships Program – PPI. This modality can be applied to contracts of up to 10 years, and the studies are based on unit values for exploration of areas in organised ports (ANTAQ, 2021[58]). The “simplified” process is expected to take six months. Until July 2022, this procedure was applied to two bidding procedures.15 In July 2022, there were 10 applications for a simplified bidding process being analysed by ANTAQ.

The temporary use contracts, introduced by the “mini-reform in Brazilian Ports Law” (Box 3.4), allow interested parties to test the feasibility of moving cargoes without a consolidated market through a contract with a maximum term of 48 months (PPI, 2020[28]). If no formal tender procedure is launched and if more than one company is interested and it is not possible to grant the areas to only one of them, the port administration can promote a simplified selection process to choose the project that best meets the public and port interests. In this way, the area to handle a cargo (which would have no investors) becomes more attractive and this mitigates risks of possible idleness. Until July 2022, 22 temporary use contracts were signed, two of them after the enactment of the Law No. 14047/2020, which added the temporary use contract to the Law No. 12 815/2013.

In 2018, in order to mitigate the effects of this centralisation, the Ministry of Infrastructure published Ordinance No. 574/2018. As an exception to the leasing procedure described in Figure 3.16, this delegated to specific port authorities not only the bidding procedure for port leases, but also the execution, management and inspection of such contracts. According to the ordinance, a delegation of decision-making power is not automatic and must be formalised by a specific agreement signed between the Ministry of Infrastructure and the entity responsible for the administration of the respective port, with the involvement of ANTAQ. To take advantage of the opportunities created by the ordinance, regain their autonomy and begin awarding leases for their areas and terminals, the administration of each Brazilian public port must meet the requirements of the Ministry of Infrastructure and the ministry must agree to the request and sign a formal agreement. The main requirements include a schedule foreseeing the main actions planned for the next three years, the establishment of the port authority in accordance with the Law of SOE’s (Law 13.303/2016), updated master and zoning plans with ISPS-Code certification and a minimum score in the port authorities management index ( Índice de Gestão das Autoridades Portuárias – IGAP). The requirement of this score shows that, to have the delegation, the port authority must have an adequate level of management.

So far, only two port authorities had these functions delegated and the first leases signed by port authorities in accordance with the new ordinance only took place in March 2022 (Ministério da Infraestrutura, 2022[59]).

Harm to competition

The centralisation of decision-making power and the number of participating bodies prolong and slow the bidding process. During the lengthy leasing procedure, a terminal can often lie idle, and any potential lessee may lose opportunities. This situation may also prevent companies from even entering the bidding process.

In addition, the centralisation of planning, decision-making and running of bidding processes for all public ports creates administrative bottlenecks. Despite their expertise, responsible teams within centralised entities may simply not have enough time to conduct all the processes simultaneously. They also have less knowledge of the day-to-day operations or specificities of each port than local administrators.

This situation results in a bidding process for port leasing that is incompatible with the agility needed to optimise the use of public space. This may result in lost opportunities for the port and potential lessees, and a loss of revenue for port authorities due to low occupancy rates; this may in turn lead to financial unsustainability and an inability to invest. In addition, this might result in financial damage to the state due to the underutilisation of infrastructure and a port’s public assets, as well as the need for monetary support to the port authorities. Overall, a loss of efficiency in the system will ultimately result in higher costs of cargo handling and so in the wider Brazilian economy (Tribunal de Contas da União, 2020[41])

Despite the decentralisation attempt, as said, only two port authorities had the delegation, which has left in place barriers arising from the length and inefficiency of the centralised leasing procedure.

Brazilian authorities should consider introducing more flexibility in the rules of Ordinance No. 574/2018 to give more autonomy to port authorities when choosing lessees, whether through tenders or simplified processes for non-complex contracts, while remaining subject to federal legislation on public procurement and port-leasing contracts.

Internationally, many port authorities have the autonomy to issue calls for port operators and then to conduct the selection process.

In the United Kingdom, the Port of London Authority conducts the selection of port operators itself following the PLA Investment Plan., a document in which the Port Authority presents its strategy, vision, investment categories and their characteristics, the criteria by which they are evaluated and claims to be open to receiving proposals from potential partners.

In Australia, the Port Authority of New South Wales, which is owned by the state Government of New South Wales, publishes online instructions on the presentation of a project and the necessary documents. After the submissions, the port authority decides if it approves or not the project.

In the Port of Rotterdam (which belongs 70% to the city of Rotterdam and 30% to the central government), commercial partners are selected through a process defined by the managers, who decide the most convenient procedure to use from a variety of possible methods, including individual invitation and a public call.

The authority of the Port of Antwerp-Bruges, an SOE, has three different processes to select its partners: public bidding; non-public selection; and upon a company’s initiative. The projects are selected considering criteria such as a company’s financial health, the amount of the proposed investment, project quality, and number of potential jobs generated. There is no public transparency on the reasons for awarding a contract.

At Port Houston, which belongs to the state of Texas, the selection process is dependent on the duration of a contract. For those of less than 50 years, no tender is required, and the authority can choose freely. For contracts of more than 50 years, a tender process is needed, although the process is fast and 90% of tenders are concluded in four to eight months. The port also has contracts called “month-to-month leases” that are the equivalent of monthly rental agreements. This type of contract was created for urgent or transit cargo or for areas where no previous leasing contract existed. The objective of this instrument is to respond quickly to the changes in the market and not to lose business opportunities.

Source: (Tribunal de Contas da União, 2020[41])

Duration of leasing contracts

Description of the obstacle and policy makers’ objective

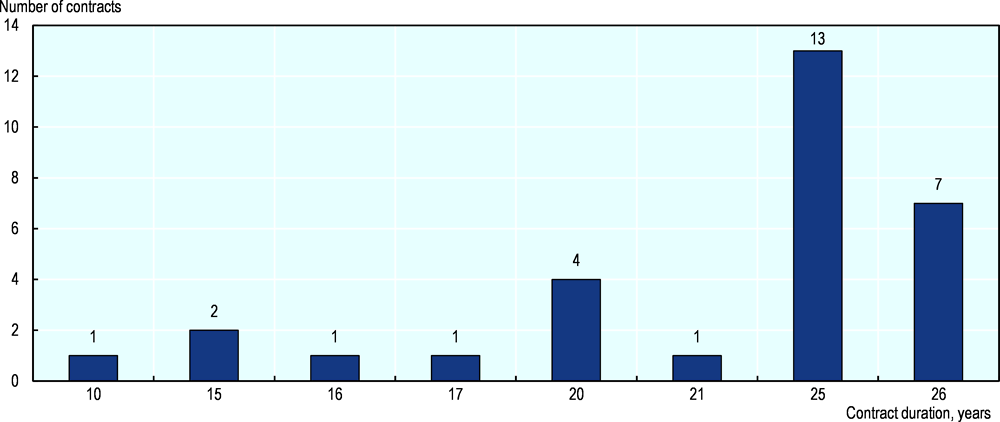

In Brazil, Law No. 12815/2013 establishes that the initial maximum length of a leasing contract for public ports is 35 years, extendable once for a maximum term of 70 years, depending on the performance of the lessee. The OECD has analysed 30 leasing contracts, signed after 2013, and more than half were granted for 25 years, as this was the maximum initial term set in the legislation before 2017 (Figure 3.17).

Note: The data used was obtained from (ANTAQ, 2022[60]) and the duration considered refers to the period from the signing of the contract until the end of its validity (the public data available at the website) and not the duration between the date of transfer of the area and the end of its validity.

Source: (ANTAQ, 2022[60])

Harm to competition

A long-lease contract allows a lessee to engage in long-term investment. Indeed, “longer concessions are sometimes preferred as this ensures that the capital investment made by the concessionaire has a stable long-term period of revenue returns to ensure its financing” (World Bank, 2018[61]). On the other hand, long-term contracts prevent new tenders, while shorter contracts generate more frequent competitive tenders that “can facilitate entry and ensure that any benefits of increased competition are reflected more promptly” (World Bank, 2018[61]).

Contract lengths and possible extensions vary from country to country. In Latin America, 57% of contracts are between 15 and 25 years, while the minimum length is 10 years (Manzanillo in the Dominican Republic). Medium-length contracts are between 24 and 26 years in more than half of the countries, but in Colombia, Ecuador, Jamaica, and Peru they are between 29 and 30 years. In 11 of 20 of the contracts analysed the contracts do not allow an extension; 8 of 20 do; and in 2 (Balboa and Cristóbal in Panama), the extension is automatic if the lessee fulfils its obligations (Suárez-Alemán, A., 2020[54]).

Analysis by the ITF/OECD of a dataset of more than 730 contracts shows that leases on container terminals have an average duration of 32.5 years. In Portugal, port authorities set the duration of the contracts for towing services at no more than 10 years and concessions of cargo-handling services at no more than 30 years. Lengths may vary inside the same port and across ports. (OECD, 2018[34])Around 90% of contracts for European terminals over 100 hectares are awarded for durations of 30 to 65 years. (Notteboom, 2008[62])

Sources: (Suárez-Alemán, A., 2020[54]) (OECD, 2018[34]) (Notteboom, 2008[62]).

Empirical evidence suggests that, even though the duration of the leasing in Brazil is 25 years and in line with the average contract length in Latin America (Box 3.11), certain leasing contracts have been awarded for a longer time than the period needed to recover the capital invested (Figure 3.18). Data available for 30 terminal-leasing contracts reveals a weak correlation between the duration of a terminal award and the volume of accumulated investment by the private sector, given factors other than duration that can affect investment choices.

Source: (ANTAQ, 2022[60]).

The European Directive No. 2014/23/EU on the Award of Concession Contracts establishes that, in contracts lasting more than five years, the level of the investment should be linked to the maximum duration of the contract. EU legislation establishes that the duration of a concession should be limited to avoid market foreclosure and restriction of competition. However, long durations may be justified if it is indispensable for the recoupment of investment (European Parliament, 2014[63]).

The European regulation provides that when estimating contract length any initial and later investments necessary to operate the concession, including expenditure on infrastructure, copyrights, patents, equipment, logistics, hiring, training of personnel and initial expenses should be taken into account (European Parliament, 2014[63])

Brazilian authorities should review the regulations to establish clear criteria that ensure that the duration of a contract takes into account the level of investment. The duration of a lease should be determined on a case-by-case basis and expressly tied to the minimum number of years required to repay the capital invested in each case.

More specifically, the period of validity of leasing contracts should be established to allow amortisation of and a return on the investment for the lessee. At the same time, it is recommended that the leasing contract include the appropriate mechanisms to allow for early termination in the event of any changes of market circumstances and conditions not provided for in the initial contract (OECD, 2018[34]).

Absence of flexibility in leasing contracts

Description of the obstacle and policy makers’ objective

The OECD has found two main obstacles related to the limited flexibility of public authorities when considering changes to the use and improvement of spaces in public ports. These concern the change in the type of cargo and the authorisation for new investments.

Change in cargo type

In Brazil, Ministry of Infrastructure Ordinance No. 530/2019 regulates changes in cargo profile for public ports. The regulation establishes that any change in the type of cargo that an operator can handle and store in the terminal is based upon on information it must produce. The provisions require the involvement of the port authority and ANTAQ, as well as an examination of possible rebalancing of the contract in case of force majeure or of fortuitous circumstances.16

The lessee must apply to the granting authority with a justification of the claim, accompanied by an investment plan that contains the following information:

1. information and data regarding the current capacity and performance of the leasing

2. revised capacity and performance estimates for the port leasing if the proposed contractual amendment were to be approved

3. information about services that the lessee intends to add or exclude from the contract

4. information on possible competition impacts in the port’s region of influence that would result from the intended contractual change (Ministério da Infraestrutura, 2020[64])The lessee may also include any other information that it considers relevant to its claim.

In public ports, a change in cargo type handled will be approved if it is compatible and coherent with the public policies defined for the port sector and the public port’s overall planning (Ministério da Infraestrutura, 2020[64]).

Unlike public ports, private ports do not face such a burdensome process. The cargo profile of a private port can be changed by an operator simply informing ANTAQ.

Authorisation for new investments

Receiving authorisation for new investments in public ports, using the ordinary process,17can be a lengthy process. During a 2019 consultation by the Federal Court of Accounts, SNPTA stated that it had had 16 requests from port operators for approval of new investments waiting for analysis, the oldest dating back to 2016 (Tribunal de Contas da União, 2020[41]). Authorisation for new investments is in the Decree No. 8.033/2013 and in Article 8 of Ministry of Infrastructure Ordinance No. 530/2019. The article of the Ordinance establishes that whenever there is justified public interest, the relevant authority may approve the realisation of investments not originally foreseen in port-leasing contracts, after analysis by ANTAQ.

The lessee must present ANTAQ an executive project document accompanied by a note of technical responsibility at least six months before the start of the work. In the case of works implemented in stages, the lessee may present partial executive projects for each stage, at least six months prior to the start of any work.

Implementation of an investment plan can only begin after a favourable opinion from ANTAQ that confirms the plan’s compatibility with and approved study of technical, economic and environmental feasibility (EVTEA), any addendum (including contractual conditions signed by the lessee and the granting authority), and the market values of new investments. If the executive project document presented to ANTAQ is incompatible with the approved EVTEA, the lessee may make the necessary adjustments. If ANTAQ believes that the estimated value of the investment is lower than foreseen in the project document, then it can follow Ministry of Infrastructure guidelines to present alternative scenarios that ensure the contract’s continued economic-financial balance. The lessee must execute the work according to the approved executive project document. Any changes in the executive project previously approved by ANTAQ require a new analysis and a statement confirming its compatibility with the approved EVTEA, the amendment, and market values. If considered compatible with these conditions, the pre-existing amendment remains in place. (Ministério da Infraestrutura, 2020[64])

According to stakeholders, the Ordinance No. 530/2019 has improved the situation thanks to its provision of an agreement of investment risk. This instrument is used in specific circumstances that authorise immediate and urgent investments not provided for in the initial contract of lease and prior to ANTAQ analysis.18 When signing an agreement of investment risk before an authorisation is granted, the port operator assumes the risk that: 1) the investment plan will be later rejected, if the granting authority finds it incompatible with public policy; 2) the investment plan will need to be revised later to gain approval; 3) ANTAQ will reject the submitted EVTEA study of technical, economic and environmental feasibility; 4) in any other risks may be discriminated in that agreement.

Private ports are not required to go through a burdensome process to undertake new investments. Instead of requiring an authorisation, they simply need to inform ANTAQ of any new investment (Ministério da Infraestrutura, 2020[64]).

Harm to competition

Port terminals require constant investment and, given the dynamism of international trade and the frequent technological innovations, prospective port operators cannot foresee in the bidding phase all potential needs that may arise throughout the contract duration to keep the business efficient and competitive. This is the reason why legal instruments concerning port leases require flexibility in order to allow timely contractual adaptations to competitive commercial and technological changes, and so allow fast way to investments to those ends.

In Brazil, as has been noted, port lease contracts for public ports do not grant the necessary flexibility to allow lessees to adapt to the dynamism of market. It is complicated to amend leasing contracts even if it would benefit the public interest and the lessee. This is also because the principle of abidance obliges the administration and the bidders to comply with the criteria and rules established in the notice for tender. Delays in amendment approval generate costs to companies that can lose contracts and opportunities and cannot adapt their business to the reality and modernity of the port sector. This absence of flexibility generates difficulties for the management of contracts and reduces their efficiency.

These difficulties in implementing new investments put public ports at a competitive disadvantage compared to private ports, which have more autonomy.

In Rotterdam, a terminal operator needs authorisation from the port authority to change the type of cargo that it is entitled to handle. Stakeholders report that the process is rapid. Likewise, at Port Houston, the authority authorises cargo profile modifications as long as they are judged in the interest of the port.

For new investments, if a lessee in Rotterdam invests more than initially agreed, the term of the lease may be extended, but not necessarily changed, as efficiency and raised cargo-handling capacity are prioritised to increase revenues. In Houston, any claim for new investment, such as extending the term or reducing the value of the lease, is made by the terminal operator and results in detailed monitoring of the budget and project execution.

Source: (Tribunal de Contas da União, 2020[41]).

The OECD recommends that Brazilian authorities review the regulations and put in place more efficient and speedy processes for contractual changes.

Brazilian authorities should also consider the creation of more instruments such as the agreement of investment risk, which make it easier for the operator to change the contract at its own risk with the possibility of a later rebalancing of the contract in cases of public and private interest.

3.2.4. Authorisations to build and operate port facilities

Regulatory framework

In Brazil, it is possible to build private port facilities outside the area of a public port, provided that an authorisation is obtained from federal authorities. The Federal Constitution of 1988, in its art. 21, item XII, item “f”, establishes the competence of the Federal Executive Branch to exploit, directly (through the public administration) or indirectly (via operators which act upon delegation of obligations and rights, through the instruments of authorisation, concession or permission) sea, river and lake ports. Law No. 12.815/2013 establishes that the indirect exploitation of port facilities located outside the public port area will take place upon authorisation. The instrument for the authorisation is called “adhesion contract”.

Figure 3.19 below provides an overview of the authorisation process.

Source: OECD, based on (Tribunal de Contas da União, 2020[41])

The OECD found that the main barriers to authorisation were related to performance guarantees, bid bonds, and technical requirements to participate in the public selection (which will be analysed in Chapter 4). In addition, the process of obtaining an authorisation excludes foreign companies and imposes administrative burdens and other costly requirements.

Duration of the process to obtain the declaration of adequacy

Description of the obstacle and policy makers’ objective