2. Science and technology enabling economic growth and ecosystems preservation

After reviewing selected ocean-related scientific and technological advances, Chapter 2 shifts to four individual in-depth case studies that serve to illustrate how some innovations in the ocean domain may potentially both enable economic development and support ecosystem improvement and preservation. The case studies include floating offshore wind power, ballast water management, innovation in the marine aquaculture sector, and possible conversion of decommissioned oil and gas rigs and renewables into artificial reefs.

2.1. Recent developments in science and technology

While the concept of sustainable or green growth is gaining ground in the ocean-user community, there is nonetheless continuing debate about the cost of trade-offs between economic development and environmental integrity involved in its implementation. This chapter offers insights into specific innovations and combinations of innovations, which can attain both objectives simultaneously: promote the economic development of ocean-based industries while fostering marine ecosystem sustainability.

With that context in mind, this OECD chapter has a threefold purpose:

-

Provide a brief update on ocean-related scientific and technological advances;

-

Contribute to the growing body of evidence indicating that the development of the ocean economy and sustainability of marine ecosystems can go hand in hand with one another;

-

And offer further insights into how science and technology innovation can contribute to improving that balance between economic development and environmental concerns.

After reviewing selected ocean-related scientific and technological advances, Chapter 2 shifts to four individual in-depth case studies that serve to illustrate how some innovations in the ocean domain may both enable economic development and support ecosystem preservation and improvement. The case studies include floating offshore wind power, conversion of decommissioned oil and gas rigs and renewables into artificial reefs, ballast water management, and innovation in the marine aquaculture sector. These case studies shed light on a trend in the ocean domain that is already emerging in many other areas of the economy, namely, the increasingly complex, rapidly changing, multifaceted nature of the challenges that science and technology are called on to address.

2.1.1. Ocean-sustainability challenges that science needs to address

Science is crucial to achieving global sustainability and adequate stewardship of our ocean, since it provides the wherewithal to deepen our understanding and monitor the ocean’s resources, its health, as well as predict changes in its status.

Recent years have seen the publication of numerous reports by national and international organisations setting out, from their standpoint, the main challenges and priorities that ocean science need to address. There are a good number of shared themes, for example: climate change and its impacts on the ocean (sea-level change, acidification, etc.), the deterioration of ocean and coastal ecosystems as a consequence of human activity, marine biodiversity loss, plastic pollution, declining fish stocks, ocean-related disasters, geohazards, and ocean governance, to name but a few.

However, there are also some divergences among the organisations in terms of national and regional priorities. For example, the impact on coastal communities and the issue of the Arctic are of key importance to the Canadian ocean scientific community’s report (Council of Canadian Academies, 2013[1]); the future of marine food webs figures prominently in the US National Research Council Decadal Survey of Ocean Sciences (National Research Council, 2015[2]); the European Marine Board identifies the need for a functional and dynamic definition of marine ecosystem health (European Marine Board, 2013[3]); and the uneven global distribution of benefits from the use of the ocean and its resources represent an important source of concern for the United Nations First Global Integrated Marine Assessment (United Nations, 2017[4]). A significant achievement of the UN Sustainable Development Goals for the ocean (SDG 14) was to capture for the first time and compress the essence of many diverse challenges facing the ocean science community (Box 2.1).

14.1 By 2025, prevent and significantly reduce marine pollution of all kinds, in particular from land-based activities, including marine debris and nutrient pollution.

14.2 By 2020, sustainably manage and protect marine and coastal ecosystems to avoid significant adverse impacts, including by strengthening their resilience, and take action for their restoration in order to achieve healthy and productive oceans.

14.3 Minimize and address the impacts of ocean acidification, including through enhanced scientific cooperation at all levels.

14.4 By 2020, effectively regulate harvesting and end overfishing, illegal, unreported and unregulated fishing and destructive fishing practices and implement science-based management plans, in order to restore fish stocks in the shortest time feasible, at least to levels that can produce maximum sustainable yield as determined by their biological characteristics.

14.5 By 2020, conserve at least 10% of coastal and marine areas, consistent with national and international law and based on the best available scientific information.

14.7 By 2030, increase the economic benefits to small island developing States and least developed countries from the sustainable use of marine resources, including through sustainable management of fisheries, aquaculture and tourism.

14.A Increase scientific knowledge, develop research capacity and transfer marine technology, taking into account the Intergovernmental Oceanographic Commission Criteria and Guidelines on the Transfer of Marine Technology, in order to improve ocean health and to enhance the contribution of marine biodiversity to the development of developing countries, in particular small island developing States and least developed countries.

Source: United Nations (2016[5]), Global Indicator Framework for the Sustainable Development Goals and Targets of the 2030 Agenda for Sustainable Development, United Nations Statistical Commission, 49th session, A/RES/71/313, New York, March.

One crucial element that all reports agree on is that the ocean is a very complex ecological and biogeochemical system that is under serious threat (e.g. pollution from human activity, overfishing in most parts of the world, destruction of marine ecosystems affecting the subsistence of local coastal populations) but which is still not well understood. How much pressure can the ocean take? How will an increasingly unhealthy ocean impact the planet’s biodiversity, the weather, the climate and our societies?

Two important interdisciplinary capabilities are still needed to get a better understanding of the ocean:

-

The capacity to study and integrate many diverse ecosystem dynamics and various biogeochemical cycles across different scales -- including temporal scales (in the order of days or centuries) and spatial scales (from a few kilometres to very large basins);

-

The capability to observe throughout the water column, all the way to the sea floor, the pressures and ecological-biogeochemical responses in the ocean interior (e.g. nutrients, oxygen, components of the plankton and indicators of their physiological status) to describe how very small processes could contribute to critically important and much wider variability.

This much needed multifaceted understanding of the ocean requires many scientific disciplines, from biology to physical sciences, to build up and analyse years of data from across broad expanses of the ocean, to collect new data, and deploy new technologies. International cooperation will be key, bearing in mind that organisational setups and ocean science capacities also vary greatly from country to country (IOC, 2017[6]). In addition to the different ocean science communities, other scientific disciplines are also joining in fundamental research that may ultimately benefit the ocean. For example, dedicated research and development into new sustainable petrochemical production routes (from production to use and disposal of products) may contribute to efforts to curb and stop the leakage of plastic pollution and other harmful chemical products into the ocean (IEA, 2018[7]). This primarily land-based pollution finds its way to the ocean via domestic and commercial wastewater (e.g. cleaning and sanitary products), agricultural run-off, and seepage from disposal sites. Much progress needs to be made to tackle the root of this chemical pollution, both in terms of the R&D required to find potential alternatives that would be less damaging to the environment, and in terms of changing current production and consumption practices (e.g. building on the circular economy concept) (OECD, 2018[8]).

Two milestones for the global ocean science community are forthcoming. For the first time, the Intergovernmental Panel on Climate Change (IPCC) will be producing a Special Report on the Ocean and Cryosphere in a Changing Climate in the second half of 2019 (IPCC, 2018[9]). Over 100 scientists from more than 30 countries are currently assessing the latest scientific knowledge about the physical science basis and impacts of climate change on ocean, coastal, polar and mountain ecosystems, and the human communities that depend on them. And 2021 will see the launch of the United Nations Decade of Ocean Science for Sustainable Development (2021-2030), with the objective that very diverse scientific communities and users of the ocean work together to develop further the knowledge base on the ocean (IOC, 2018[10]).

2.1.2. Selected trends in ocean science and technology

The OECD report on the ocean economy in 2030, written in 2015, already described many of the key advances under way in science and technology to help address the bulk of the challenges outlined above (OECD, 2016[11]).

In the course of the next couple of decades, a string of enabling technologies promises to stimulate improvements in efficiency, productivity and cost structures in many ocean activities, from scientific research and ecosystem analysis to shipping, energy, fisheries and tourism. These technologies include imaging and physical sensors, satellite technologies, advanced materials, information and communication technology (ICT), big data analytics, autonomous systems, biotechnology, nanotechnology and subsea engineering (Table 2.1). In addition to incremental innovations, there is the prospect of different technologies emerging and converging to bring about quite fundamental shifts in knowledge acquisition and marine industry practices.

A cursory glance at the more recent literature suggests that, in the short period that has elapsed since the writing of the Ocean Economy in 2030 report, there has been an acceleration of research interest in the potential for applications of some of those technologies in gaining a better understanding of marine ecosystems, their workings, and the requirements for their better management (Box 2.2).

Remote sensing using high-frequency radar and high-resolution satellites, with applications in:

-

Monitoring and modelling of oil spills from ships and offshore platforms, and of chemical contaminants (Singha and Ressel, 2016[12]; Li et al., 2016[13]; White et al., 2016[14]; Tornero and Hanke, 2016[15]; Strong and Elliott, 2017[16]; Spaulding, 2017[17]; Nevalainen, Helle and Vanhatalo, 2017[18]; Mussells, Dawson and Howell, 2017[19]; Azevedo et al., 2017[20]);

-

Measurement ocean surface currents using AIS (Guichoux, 2018[21]) and mapping global fishing activity (Kroodsma et al., 2018[22]);

-

Biochemical modelling of plankton biomass (Gomez et al., 2017[23])

-

Management of coastal zones and wetlands ( (Kim et al., 2017[24]; Wu, Zhou and Tian, 2017[25]).

Genetics, eDNA and other genetic toolkits applied in

-

Monitoring and assessment of (invasive) species in ecosystems (e.g. (Darling et al., 2017[26]));

-

Monitoring seabed mining disturbances (Boschen et al., 2016[27]);

-

Detecting bacteria in ballast water (Pereira et al., 2016[28]).

Acoustics, imagery and artificial intelligence advances in:

-

Monitoring (migratory) fish movements (Martignac et al., 2015[29]; Geoffroy et al., 2016[30]; Shafait et al., 2016[31]);

-

Monitoring marine habitats and ecosystem characteristics (Wall, Jech and McLean, 2016[32]; Cutter, Stierhoff and Demer, n.d.[33]; Trenkel, Handegard and Weber, 2016[34]); and recognition of marine species ( (Siddiqui et al., 2018[35]; Chardard, 2017[36]);

Autonomous systems. Progress in Unmanned Autonomous Vehicles (UAVs), gliders and Autonomous Underwater Vehicle (AUVs), including improved sensors, and high-resolution tools for 4D oceanic measurements:

-

Use of gliders in marine surveys (Colefax, Butcher and Kelaher, 2018[37]);

-

Use for research purposes in otherwise inaccessible and remote locations, including in the polar regions, and as key components of the Global Ocean Observing System (GOOS) (Forshaw, 2018[38]);

-

Monitoring and inspection in oil spill response (Dooly et al., 2016[39]; Gates, 2018[40]).

Enabling technologies appear set to contribute in important ways to the sustainable development of the ocean economy, not least by vastly improving data quality, data volumes, connectivity and communication from the depths of the sea, through the water column, and up to the surface for further transmission. While the examples are far from exhaustive, they do serve to illustrate the richness of current innovations in the ocean economy that are addressing either the one or the other objective. Two are particularly highlighted below:

-

Blockchain and big data analytics applications, for example, are starting to be deployed in port facilities and maritime supply chains. Shipping companies, logistics businesses, port operators and other maritime transport stakeholders are looking to more integrated services across the entire supply chain as a means of generating cost savings and greater efficiencies, as well as improvements in quality of service. The prospects for achieving those benefits by getting the various relevant operations (administration, logistics, shipping, terminal and port) to work together more smoothly have been boosted by the advent of digital platform technologies. For example, within the administrative segment of shipping operations, transport operators are currently exploring the potential for using distributed ledger technology (DLT), most notably blockchain. This technology does away with the need for an intermediary in transactions between stakeholders, while potentially offering a rapid and secure authentication method for freight transport. New players are emerging in the form of shipping tech start-ups with the capacity to leverage higher data volumes. They include digital freight forwarders, rate analytics services, collaboration or exchange platforms, tracking platforms and service fulfilment networks (International Transport Forum, 2018[41]).

-

The emergence of autonomous ships is also an important disruptive element for some industries, as are autonomous underwater vehicles (AUVs). AUVs and gliders with improved sensor platforms have progressed from niche status to an established part of operations in various marine sectors. In the oil and gas sector, however, the technology still has to mature to a stage at which oil and gas operators consider it a vital component of operations (Wilby, 2016[42]). This technology is deployed in monitoring and inspection for leakages in underwater carbon capture facilities, as well as in the inspection of deep-sea pipelines (Forshaw, 2018[38]). There are future opportunities for deployment in offshore decommissioning (Westwood Global Energy Group, 2018[43]) and possibilities for use in offshore wind (Westwood Global Energy Group, 2018[44]).

Other selected innovations primarily supporting the development of the sustainable commercial use of the seas and ocean are presented in Box 2.3.

Artificial intelligence applications in acoustics and imagery:

-

Development of machine learning to interpret subsurface images from seismic studies using computer vision technology and automate the analysis of technical documents with natural language processing technology (Zborowski, 2018[45])

-

Fisheries - Single beam and multi-beam echo sounder systems, real-time 3D visualisation software, sonars and catch monitoring systems (Kongsberg, 2017[46]), video imagery and recognition of fish species assisted by artificial intelligence (AI) (Siddiqui et al., 2018[35]);

-

AI in renewable ocean energy used for e.g. sea wave height prediction, sea-level variation prediction, wave hindcasting (Jha et al., 2017[47]).

Remote sensing using high-frequency radar and high-resolution satellites with applications in:

-

Decision making on suitability of aquaculture sites (Fernandez-Ordonez, Soria-Ruiz and Medina-Ramirez, 2015[48])

-

Offshore wind farms (Zecchetto, Zecchetto and Stefano, 2018[49]), (Kubryakov et al., 2018[50]).

-

Algal bloom forecasting for aquaculture insurance purposes (Miller, 2018[51]).

Modelling progress in applications in:

-

Development of methodologies and numerical modelling of wave and tidal energy and their environmental impacts (Side et al., 2017[52]; Venugopal, Nemalidinne and Vögler, 2017[53]; Heath et al., 2017[54]; Gallego et al., 2017[55]);

-

Wind resource assessments (Zheng et al., 2016[56]) (Kulkarni, Deo and Ghosh, 2018[57])

-

Impact of wind and waves on ocean facilities, e.g. siting of aquaculture facilities (Lader et al., 2017[58])

2.1.3. Introducing the four case studies

Beyond recent advances in science and technologies, the focus of this chapter is on innovations and combinations of innovations which embody the very the notion of green growth in the ocean by successfully fostering economic development and ocean sustainability simultaneously. To do this, it presents four in-depth innovation case studies: floating offshore wind; ballast water management; marine aquaculture; and rig- and renewables-to-reefs.

The four case studies are very different. They differ in scale and in the degree of maturity of the respective activity. Floating wind power is still in its infancy, with only one commercial-scale facility in operation in the world. Ballast water treatment technologies have so far been installed in only a small number of ships, but expansion could be rapid. Oil and gas rig conversion into artificial reefs is current in some parts of the world, but not in others, and no renewables-to-rigs programmes exist anywhere. Marine aquaculture, by contrast, is well established in many parts of the world, is undergoing rapid expansion, and is being transformed at great speed by a whole host of innovations. For this reason, the marine aquaculture case study is addressed in more detail and at greater length, in order to illustrate the sector-wide dimension of the innovation process.

Moreover, innovation in the four activities is driven by different forces and different challenges. Innovation in floating wind power is largely science and technology driven; rigs-to-reefs conversions are driven both by industry’s need to reduce decommissioning costs and conservationists’ desire to create or restore ocean ecosystems; innovation in ballast water treatment is propelled essentially by regulation; and innovation in the marine aquaculture sector is motivated by multiple factors: the challenge of feeding a growing world population, the incentive to develop business opportunities, and the need to reduce pressures on coastal environments. As different as the drivers may be, progress in all the cases is science-led or at least science-based.

Each case study endeavours to address a number of key issues: the background and global context; the economic and environmental issues at stake; the research and technological innovations in prospect; and the contribution that the innovations could make to enabling economic development within the sector (e.g. through cost-savings, new business generation, emergence of new industries) and environmental sustainability to go hand in hand.

2.2. Case Study 1: Innovation in floating offshore wind energy

2.2.1. The economic and environmental issues at stake

Until recently, floating offshore wind technology was largely confined to research and development, but the coming decades could see it emerge on a commercial scale. For that to happen, however, a wide range of technological, economic, regulatory and environmental challenges will need to be addressed.

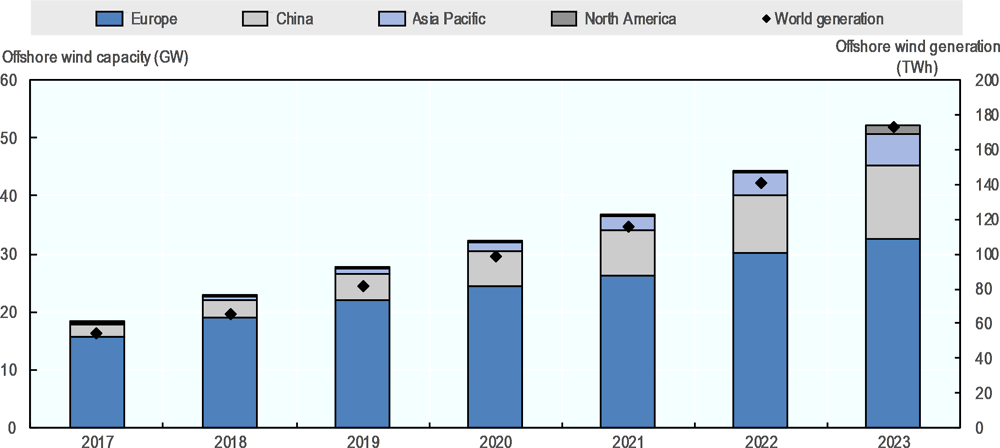

The offshore wind industry has grown at an extraordinary rate over the last 20 years or so, from almost nothing to a total capacity of 18 GW in 2017. The way has been led mainly by Europe and China. Growth prospects are strong. Between 2017 and 2023, total global capacity is expected to almost triple to 52.1 GW (IEA, 2018[59]).

The potential economic benefits of such a rapid expansion are considerable. The OECD’s 2016 report on the Ocean Economy in 2030 suggests that, on a business-as-usual basis, the global gross value added generated by offshore wind power could increase eight-fold and employment more than twelve-fold between 2010 and 2030. As a consequence, its share of the global ocean economy could grow from less than 1% in 2010 to 8% in 2030 (OECD, 2016[11]).

Wind power also offers considerable benefits to the environment through its contribution to reducing global CO2 emissions. By way of illustration, estimates of carbon emissions from offshore wind generation conducted in 2015 place life-cycle emissions in the range of 7 to 23 g of CO2 equivalent per kilowatt (gCO2e/kWh). This compares with around 500 g for gas-fired conventional generation and about 1 000 g for coal-fired conventional generation (Thomson and Harrison, 2015[60]). A similar result was arrived at in a more recent study by Kadiyala et al. (2017[61]) which estimated the mean life-cycle emissions of the offshore wind installations surveyed at 12.9 gCO2e/kWh (with an environmental payback period of just 0.39 years).

Source: Adapted from IEA (2018[59]), Renewables 2018: Analysis and Forecasts to 2023, https://dx.doi.org/10.1787/re_mar-2018-en.

Moreover, the potential contribution to reducing CO2 output stands to benefit indirectly the world’s ocean ecosystems by helping to slow the increase in acidification, de-oxygenation and the rise of sea temperature and sea levels. Hence, further rapid expansion of offshore wind power suggests further gains for the environment in terms of CO2 reductions.

To date almost all offshore wind turbines are of the fixed-bottom type, installed in shallow water (up to around 50-60 meters) in proximity of the coast. Fixed-base wind turbines are arguably today successfully delivering low energy costs, improved energy security and low environmental impact, and much of the future growth in total offshore wind generation will continue to stem from this type of platform. However, over time, fewer near-coast shallow-water sites will become available due to growing competition for space from other ocean users, as well as to the lack of physically suitable locations. The latter applies in particular to countries like Japan and parts of North America and Latin America whose coastal zones are situated in deep water. Floating offshore wind platforms offer a way out of this dilemma. They could be installed in positions benefitting from more space, less potential interference with other ocean activities, and stronger more regular winds. In principle, the potential is very large indeed (Table 2.1).

Despite being able to draw quite heavily on the experience that the offshore oil and gas industry has with floating structures, seabed fixtures and related technologies, floating wind farms have taken some time to emerge as a commercial-scale installation. Indeed, to date, there is only one single large-scale offshore wind platform operating in the world: The 30 MW Hywind is situated off the Scottish coast and has been operating successfully – even surpassing expectations – since 2017 (Hill, 2018[63]). Nevertheless, at the time of writing, not one floating offshore technology has proved itself to the extent that it could be purchased off the shelf (Dvorak, 2018[64]).

However, many more projects are approaching fruition or are currently under development. The Scottish government has approved the 50 MW Kincardine Floating Offshore Wind Farm. The Council of Ministers in Portugal has given the go-ahead to the development of the 25 MW WindFloat Atlantic (WFA) project in Viana do Castelo, 20 km off the coast of Northern Portugal. France has approved a total of four pilot floating wind projects: a 24 MW pilot floating wind farm in the Gruissan area; a 24 MW floating wind farm planned by Eolfi and CGN for the Groix area; a 24 MW floating wind farm in the Faraman area; and another 24 MW project off Leucate. Work is also underway on the 2 MW Floatgen floating wind project in the Port of Saint-Nazaire. Japan installed the Fukushima Hamakaze floating wind turbine in 2016, and has initiated several further floating wind projects, such as the demonstration one off Kitakyushu. In the United States, the 12 MW New England Aqua Ventus I floating offshore wind demonstration project is under way in the Gulf of Maine. More developments are in the pipeline for projects off the coasts of Scotland, Wales and Ireland (offshoreWIND.biz, 2017[65]).

Consequently, expectations are running high that the market will develop rapidly in the coming decade, growing from almost nothing in 2017 to around 1 300 MW in 2030 and providing a total installed capacity of over 5 GW by 2030 (GWEC Global Wind Energy Council, 2017[66]). The basis for such optimism would appear to be, inter alia, recent progress in research, development and innovation.

2.2.2. Developments in research and technology

At the moment there are three designs of substructures under development: spar-buoy, spar-submersible, and tension leg platform (TLP); see IRENA (2016[67]), for more detail. A fourth foundation design – barge – is also well advanced, though less so than the others.

The high expectations of vigorous market expansion in the coming years are built on estimates of the potential for floating solutions and on the progress that has been made in bringing floating wind turbines up to an advanced level of technological readiness. According to Wind Europe (2017[68]), the spar design is already at technology readiness level (TLR) 9, and the others are expected to reach that score within the next five years: Expectations are further fuelled by advances that are being made in such areas as the siting of turbines, construction materials and methods, new designs, and monitoring and inspection, as the following examples illustrate.

Improved siting of turbines

Remote sensing is playing an increasingly important role as a decision support tool in choosing the most suitable locations for wind energy offshore. The key advantage of satellites over conventional surface observations is that satellite data can cover a wider spatial range, allowing for more comprehensive assessment of potential offshore wind energy resources. Zheng et al. (2016[56]) note, however, that there are a limited number of satellites and orbits, so that the data gathered may be inadequate in terms of time synchronisation and spatial resolution, as they may not be able to cover large surface areas at the same point in time during observation. Moreover, they cannot capture variations in the wind field at different altitudes. Satellite data can however be enhanced by applying numerical simulation methods to the energy resource evaluations. As a consequence of technological progress in modelling, recent years have seen more and more reanalysis data successfully deployed in this field. James et al. (2018[69]), for example, report on a successful modelling exercise using a three-year dataset of wind forecasts above ground level over offshore regions of the United States to support and improve energy resource assessments and wind forecasts for New England and other coastal regions of the United States.

Looking to the longer term, Zheng et al. (2016[56]) point to the need for improvements in a range of related fields, including: short-, medium- and long-term forecasting of wind energy; and early warning of natural disasters that pose a risk to wind farms. Over the even-longer term there is the issue of climate change and the uneven distribution around the globe of potential changes in the wind induced by global warming. Wind farms in some areas are likely to be impacted more severely than those in other regions. Here too more research is called for (Kulkarni, Deo and Ghosh, 2018[70]).

Improved construction materials and methods

As turbines have become ever larger over the years, so too have their rotor blades. They have increased in length quite considerably in recent years, from about 30 m in the 1990s to more than 100 m today. The blades themselves are composed mainly of fibreglass reinforced resins with add-ins of balsa wood and carbon fibre. The carbon fibre enhances the stability of larger turbines, thereby providing higher capacity. Thus, in future the share of carbon fibre is expected to rise, despite the fact that it is more expensive than other materials (McKenna, Ostman v.d. Leye and Fichtner, 2016[71]). Advances are also expected in meeting the challenge of the higher loads associated with larger rotors. Tests are under way on active load-control techniques such as trailing edge flaps and smart structures, intelligent pitch control systems, smart sensors to monitor blade load, and microtabs to modify the loads on the turbine structure. Other innovative concepts include smart blades that adapt to conditions and reduce or replace the requirement for active control (McKenna, Ostman v.d. Leye and Fichtner, 2016[71]).

The harsh conditions of the ocean climate place particular demands on the structure and workings of floating offshore wind energy platforms. Turbine blades are now manufactured from composite materials, in which further advances can be expected in the coming years. They need to remain in service for around 25 years, but are very vulnerable to rust and require regular inspection and treatment. Hence, preventive coatings for turbine blades are under development which aim to reduce substantially inspection and maintenance costs1 (Fraunhofer, 2016[72]).

Research is also under way to develop criteria to support decisions on the selection of materials for the foundations of floating wind farms. In the case of tension leg platforms, for example, various materials and methods are available but these tend to have different characteristics when it comes to lifecycle costs, CO2 emissions, etc. Kausche et al. (2018[73]) calculate that pre-fabricated steel or pre-stressed concrete have clear advantages over welded steel solutions, a research outcome that could apply equally to spar-buoy and semi-submersible type foundations, on which however to date no data have been published.

New designs

It is estimated that around 20 players are currently working to move new foundation designs from the concept stage to commercialisation (Renewable Energy Agency, 2016[67]). Numerous innovations are in the pipeline. The Spanish company Saitec, for example, is developing a cost-effective floating wind farm solution SATH (Swinging Around Twin Hull) fitted with two twin concrete hulls that are fastened to a single mooring point, allowing the platform to swing around. The economic advantages arise from the single mooring point system, which shortens installation times and facilitates returning to port for major work, as well as from the fact that the platform and turbine equipment are assembled on shore at the harbour, thereby minimising operations at sea (offshoreWIND.biz, 2017[65]).

Swedish specialist Hexicon is building platforms with floating foundations equipped with twin turbines for greater cost efficiency, and the platforms being designed by Swedish manufacturer TwinSwirl reduce manufacturing and maintenance costs by installing the parts requiring maintenance inside the easily accessible generator housing above water level (SeaTwirl, 2018[74]). On matters of grid connection, where one of the key problems is power transmission from a platform subject to significant movement, Japanese researchers have developed and demonstrated a dynamic cable system capable of stabilising power transmission (Taninoki Ryota et al., 2017[75]).

Looking to the longer-term horizon, designs are expected to progress from the single-rotor model deployed today to multi-turbine arrays on a single structure, generating as much as 20 MW of power from numerous 500 kW turbines and cutting both installation and maintenance costs. And as of 2040, the sector is expected to be making inroads into solving the weight-related problems posed by ever larger turbines on tower-structure designs. Vertical axis turbines, currently still in their infancy, offer considerable potential in this respect (Carbon Trust and Offshore Renewable Energy Catapult, 2017[76]).

It is noticeable however, that for many of these innovations, the timeframe is long and it is unclear how quickly they will find their way into commercial scale use.

Monitoring, inspection, maintenance and repair

Remote monitoring of conventional fixed-bottom wind energy facilities is already widespread, remote maintenance and repair operations on the other hand are still in their infancy. But as floating offshore wind becomes mainstream, platforms will increasingly be located in deeper waters and harsher conditions at ever greater distance from the coastline. As a consequence, installation, operation, maintenance, and repair will become more difficult, more dangerous and more expensive. Solutions will need to be sought in automated, remotely operated technologies. This should open up further opportunities for AUVs, ROVs, subsea robotics, and so on. Indeed, the United Kingdom’s Catapult (2017[76]) predicts that, a few decades from now, the deployment of drones and AI-driven monitoring systems for offshore wind farms – fixed and floating – is set to become commonplace, as is the use of remotely controlled and even autonomous underwater repairs and maintenance. Again, however, many of the above are unlikely to find their way into commercial scale application for many years yet.

2.2.3. Challenges facing floating wind technology

The high expectations with respect to the near and medium term development of floating wind technology need to be put in perspective, since there are many economic, technological, institutional and environmental challenges ahead.

While much can be learned from fixed-base offshore wind farms, floating wind technology is far from being a simple extension of that technology innovation system. The supply chain is different from that used for fixed-base turbines in shallow, near-shore waters; the technologies are different, as are the cost structures; the impact on the marine environment is different; and other ocean users may be affected in other ways (Bento and Fontes, 2017[77]). The difference in cost structure is particularly striking with respect to capital expenditure. While the foundations make up only 20% of total capex for conventional fixed-base offshore turbines (the main cost components are related to the turbines themselves), they account for around two-thirds of total capex in the case of tension-leg (TLP) floating wind platforms (Kausche et al., 2018[73]).

Costs figure among the most important potential barriers to rapid development of floating offshore wind farms. Higher average distance to shore correlates with higher wind speeds and higher capacity factors, but entails lengthier export connection cables to grid. Water depth usually increases with distance to shore, but is associated with higher installation and foundation costs, in particular mooring costs (Myhr et al., 2014[78]). Compensating cost savings may be expected from more integrated supply chains, economies of scale, upscaling of turbines, and major repairs conducted onshore, but most such savings will take time to come through. The longer term also holds further challenges. For example, grid integration costs are likely to increase as levels of penetration by variable power generation sources rise. The Levelised Cost of Energy (LCOE) for existing offshore wind farms in Europe in 2015 ranged from 7.3 €ct/kWh to 14.2 €ct/kWh, higher than the LCOE of onshore wind energy or conventional generation technologies (Höfling, 2016[79]). The LCOE of floating wind turbines, in turn, will very probably be higher than for both onshore and fixed-bottom offshore installations: according to the IEA, about 6% higher than the 2014 baseline in the IEA medium-term scenario (Wiser et al., 2016[80]). The results of the IEA’s survey of over 150 world experts in offshore wind power suggest that trend reductions in the LCOE of floating wind energy solutions could converge with those of fixed wind power platforms, but not until around 2030.

According to the findings of the IEA survey of experts, the most significant enabler for driving down the levelised cost of energy is – in addition to learning from experience – research and development. Significant technical innovations will be required to improve the competitivity of floating wind farms, but so will innovations in site identification, serial production, supply chain integration and management, and logistics during construction and operation.

2.2.4. Impacts on the environment and marine ecosystems

As noted earlier, the net contribution of floating wind energy to the reduction of CO2 emissions is significant compared to fossil-fuel based energy sources. There are nonetheless non-negligible drawbacks for the marine environment. These include the impact on (migrating) birdlife, the effects on fish and marine mammals, as well as those on the seabed and benthic habitats.

Most of the available research on ecosystem impacts draws on Northern European experience with fixed-base offshore turbines. Offshore structures can under certain circumstances enhance the marine environment due to increased biological productivity (of fish, molluscs and other forms of marine life). However, the construction phase would appear to be particularly invasive, with construction noise and disturbance of the seabed having effects on benthic habitats and many species of marine life, and once complete may in addition disrupt habitat connectivity both in and beyond the immediate area. Once in operation, the turbines can be a source of acoustic disturbance for a range of marine animals. There are also risks to bird life: potential flight displacement, risk of collision, and fragmentation of habitat by creating a barrier between birds’ nesting grounds and their feeding grounds. Some progress is being made in developing the technological and scientific tools to address some of these problems. In the case of risks to avian species, for example, techniques ranging from radar monitoring, Thermal Animal Detection Systems (TADS) and acoustic detection, to video surveillance and computational collision models are currently being deployed in the study of bird flight and behaviour in the proximity of offshore wind farms.

The view is emerging that, at least as concerns the construction/installation phase, floating wind turbines would be less intrusive during dredging and seabed preparation operations than fixed-bottom turbines (Carbon Trust and Offshore Renewable Energy Catapult, 2017[76]). Nonetheless, numerous issues remain. For example, for floating platforms, cable routes still need to be prepared and cables laid, activities that are associated with considerable disturbance of sediments. Also, the mooring systems for floating turbines need a large mooring spread. For a typical (catenary) mooring system, the spread diameter increases by 14 m with every 1 m increase in water depth. For a wind farm installed at a water depth of 150 m, for example, this would translate into a mooring system that required a 2 km diameter area of seabed for every turbine in the farm. Not only does that significantly raise the cost of mooring system materials, it also increases the lease area and expands the seabed environmental impact (Hurley, 2018[81]).

Also, the ornithological impact would depend greatly inter alia on how close to shore the floating facility is deployed. In relation to interaction of the floating foundation with fish and marine mammals, little research appears to be available, not least due to the fact that as of today few floating platforms exist.

The construction and operation of floating facilities should benefit from the experience of installing and running fixed-base wind turbines with ecosystem impact assessment. But even here, there are still large knowledge gaps. Lack of baseline data is a considerable impediment to the evaluation of impacts. Indeed, baseline research is needed on a whole range of natural phenomena including on marine species’ population structures and status, and their distribution and abundance over many annual cycles. And much remains to be done to improve the knowledge base on long-term ecosystem impacts as well as on the cumulative effect of multiple impacts. Similarly, information about the effects on the whole ecosystem (as opposed to those on single species or specific ecosystem components) is generally quite limited, although there are signs of progress; see for example Pezy, Raoux and Dauvin (2018[82]).

2.2.5. Concluding observations

With innovation evolving apace and levelised costs of energy projected to follow a downward trajectory similar to those of fixed-base wind platforms, a promising future is discernible for the floating wind energy sector. The growth potential is considerable, and from a broader ocean industry point of view, one would expect economic spill over benefits to flow to other maritime sectors such as ports, shipyards (construction and repair), marine equipment, and shipping. But given the many challenges this new sector faces, it seems unlikely that floating wind energy will be making a perceptible impact at commercial level in the near or medium term. Hence, also the indirect and direct benefits to the marine environment through displacement of fossil fuels will take time to have any effect. Science and technology are at the leading edge of developments to address the engineering and cost-reduction challenges, just as they will be required to play a key role in closing knowledge gaps and resolving many of the uncertainties still surrounding the environmental impacts of floating wind platforms.

2.3. Case Study 2: Marine invasive alien species and ballast water treatment

Marine invasive alien species have been spreading across the globe for centuries, often wreaking considerable damage on native ocean and coastal ecosystems. Ships have been the principal cause, and as globalisation in recent decades has gone hand in hand with rapid growth in maritime transport, so too has the dispersion of invasive alien species grown across the world’s oceans. Innovation in ballast water treatment may contribute to control this growing issue better.

2.3.1. The economic and environmental issues at stake

The marine invasive alien species’ problem is extraordinarily diverse and truly global in geographical scale, as the International Maritime Organisation’s (IMO) list of the world’s most troublesome invasive species indicates. In many instances, the impact on the environment has been devastating, depleting zooplankton stocks, competing with, displacing and sometimes wiping out local native marine life, disrupting food webs, obstructing coastal structures, and even posing a threat to public health. The environmental impacts are often associated with substantial economic costs, ranging from losses to fisheries and aquaculture, foregone revenues from tourism, deterioration of port facilities, and so on. The overall costs are thought to run into the USD tens of billions annually (King, 2016[83]).

Some examples of aquatic bio-invasions causing major impact are listed in the table below, but there are hundreds of other serious invasions, which have been recorded around the world (Table 2.3).

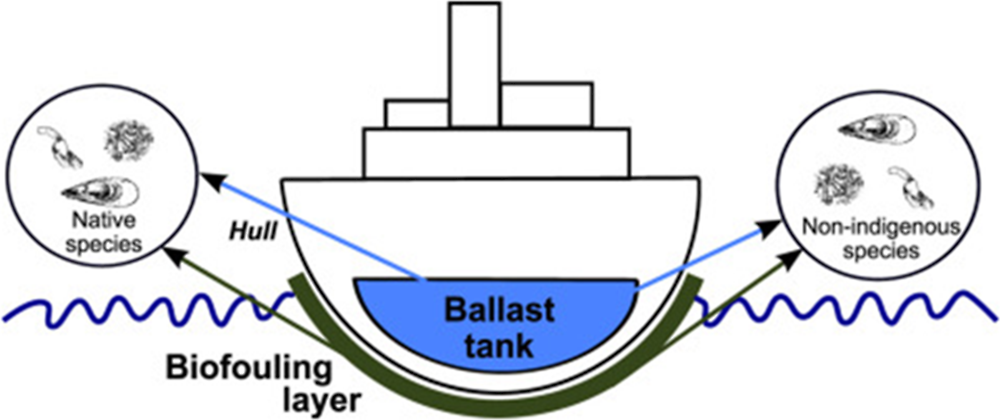

The two main vectors by which marine invasive species are redistributed globally are biofouling (largely on ships’ hulls) and ballast water (Figure 2.2).

Source: Fernandes et al. (2016[85]) Costs and benefits to European shipping of ballast-water and hull-fouling treatment: Impacts of native and non-indigenous species, https://doi.org/10.1016/J.MARPOL.2015.11.015.

This case study focuses on the latter, namely the water that is used to maintain ships’ stability and integrity under different operational situations. As the size of merchant vessels increased and maritime traffic expanded over the last seventy years or so, the volume of untreated ballast water being transferred unintentionally from one location to another has grown enormously. It is thought that today tens of billions of tons of ballast water are carried between the world’s seas every year (Davidson et al., 2016[86]), spreading thousands of marine organisms – larvae, plankton, bacteria, microbes, small invertebrates, etc.- into the local marine ecosystem when discharged. This ballast-related redistribution of invasive species is widely recognised as a major environmental and economic problem, challenging, complex and currently still unresolved (Batista et al., 2017[87]). As a result, the need to treat ballast-water has become a priority initiative at global level, encompassing national efforts to strengthen regulation as well as multilateral efforts to design and implement an international convention.

2.3.2. Current state of regulation

International ballast water management regulation has been long in the making. Indeed, the International Maritime Organization (IMO) has been tackling it since the 1980s, when Member States of the organisation began alerting its Marine Environment Protection Committee (MEPC) to their concerns. The year 1991 saw the adoption of Guidelines to address the issue, followed by work to build the IMO Ballast Water Management Convention, adopted in 2004. The Convention was eventually ratified by the IMO in September 2016. Although scheduled to come into force on September 8, 2017, implementation has been delayed until 2019 (see Box 2.4). All ships to which the Convention applies should be equipped with a Ballast Water Management System (BWMS) no later than 8 September 2024.

The Ballast Water Management (BWM) Convention requires all ships in international trade to manage their ballast water and sediments, according to a ship-specific ballast water management plan. All ships must carry a ballast water record book and an International Ballast Water Management Certificate. Ship-based diffusion of organisms (including invasive species) may vary by vessel type. Moreover, there are significant knowledge gaps also with respect to the natural spreading of organisms.

“All ships engaged in international trade are required to manage their ballast water so as to avoid the introduction of alien species into coastal areas, including exchanging their ballast water or treating it using an approved ballast water management system.

Initially, there will be two different standards, corresponding to these two options.

The D-1 standard requires ships to exchange their ballast water in open seas, away from coastal waters. Ideally, this means at least 200 nautical miles from land and in water at least 200 metres deep. By doing this, fewer organisms will survive and so ships will be less likely to introduce potentially harmful species when they release the ballast water.

D-2 is a performance standard which specifies the maximum amount of viable organisms allowed to be discharged, including specified indicator microbes harmful to human health.

New ships must meet the D-2 standard from today while existing ships must initially meet the D-1 standard. An implementation timetable for the D-2 standard has been agreed, based on the date of the ship's International Oil Pollution Prevention Certificate (IOPPC) renewal survey, which must be undertaken at least every five years.

Eventually, all ships will have to conform to the D-2 standard. For most ships, this involves installing special equipment.”

Source: IMO (2017[88]) Global treaty to halt invasive aquatic species enters into force. http://www.imo.org/en/MediaCentre/PressBriefings/Pages/21-BWM-EIF.aspx

Full success of the Convention depends on a number of issues, the most important being the following:

-

It will only apply to ships from flag states having ratified the Convention, and to ships entering their jurisdictions. At present the treaty has been ratified by more than 60 countries representing more than 70% of world merchant shipping tonnage. Given that this includes the dominant shipping nations as well as a host of other countries, it would be practically impossible to sail internationally without complying with the Convention. This effectively puts a brake on the exchange of invasive species, as vessels from nations not complying with the Convention are restricted to their own territorial waters.

-

In view of the widespread lack of awareness about the environmental and economic consequences of ballast water, major efforts will be required to integrate and train ship crews and port staffs.

Further international negotiation and collaboration in the years ahead will be critical factors in consolidating, implementing and expanding the Convention.

2.3.3. Current state and future development of ballast water treatment technologies

The Ballast Water Management (BWM) Convention standard applies to water upon discharge. However, ship owners are fully aware of the biological growth in ballast tanks, and so many already have or will in future have procedures for ballast water treatment in place for both water uptake and discharge.

The design and operation of BWM systems face multiple challenges. They have to be usable for many different types of vessel, prove effective in destroying a wide range of organisms, and be able to operate efficiently and safely under all kinds of ballast water conditions such as varying ranges of salinity and temperatures. Consequently, research has given rise to hundreds of different BWM applications that use a variety of underlying technological principles. These currently range inter alia from ultra violet, oxidation and de-oxygenation, to electrolysis, ultrasound and heat, as well as chemical biocides. (Latarche, 2017[89]). However, among the many vessels already equipped with BWM systems that are approved for use by the IMO and United States Coast Guard (USCG) , the vast majority utilise two main technologies for disinfection purposes – electro-chlorination or ultraviolet irradiation – often in combination with filtration (Batista et al., 2017[87]).

Both technologies have been subject to criticism. For example, common and abundant seawater phytoplankton have frequently been found to be resistant to UV treatment; especially smaller organisms and microbes often survive; and so the question of population re-growth in the ballast tank persists (Davidson et al., 2017[90]; Batista et al., 2017[87]; Wollenhaupt, 2017[91]). Electro-chlorination, in turn, has been found to demonstrate lower disinfection efficiency in upper reaches of estuaries and freshwater surroundings because of their lower salinity (Batista et al., 2017[87]). Moreover, environmental concerns have been raised about problems related to pollution from some chemical treatments being applied to ballast water (Davidson et al., 2017[90]).

In the absence of more effective treatments today, what is in the innovation pipeline for tomorrow?

One solution may lie in the development of green, environmentally friendly treatments that can handle the double challenge of making significant inroads into the spread of invasive species at reasonable cost while at the same time reducing impacts on the marine environment. An example is pasteurisation technology that does without UV, filters and chemicals. The Danish Bawat BMS (2018[92]), for example, is aiming for USCG-type approval in the course of 2019.

Meanwhile, currently available technologies are undergoing continual improvement through evolutionary (rather than revolutionary) advances, and through innovations that aim to mitigate the shortcomings of existing techniques. To date, over 65 ballast treatment systems have been given type approval by the IMO. And in terms of mitigation (e.g. sampling), research is apparently generating numerous applications that allow testing for some organisms whose continuing presence post-treatment would involve severe penalties from the regulators. While such applications do not detect all organisms or bacteria identified by IMO or USCG regulations, they can provide indications of whether the treatment system is working effectively and allow the vessel operators to undertake further action. Increasingly, these are small, relatively inexpensive hand-held devices that detect the presence of viable algal organisms, microbial activity etc. in the ballast water. (Latarche, 2017[89]). In addition, advanced lab-on-chip detectors have been tested recently which can measure various characteristics of certain microorganisms in ballast water, for example number, size, shape and volume (Maw et al., 2018[93]), and detection of bacteria in ballast water by new-generation DNA techniques has also been successfully tested (Brinkmeyer, 2016[94]).

2.3.4. Estimating economic costs and benefits

In complying with the requirements of the Convention, there are clearly large potential gains for the environment. For the shipping industry however there are costs involved, in the form either of installing BWMS in the newly built vessels or in retrofitting existing vessels. The flipside of the coin is that the shipbuilding and maritime equipment sectors stand to benefit from the extra revenue this involves. But how large is the additional revenue likely to be?

Several attempts have been undertaken in recent years to estimate the size of the potential additional BWMS market. All of them necessarily entail building multiple scenarios because the many different types of ship of different size require different ballast water volumes and different equipment. In their work on the costs and benefits of biofouling and ballast water in the European market, Fernandes et al. (2016[95]) rely upon three categories of ballast water volume (< 1 500 m3, 1 500 to 5 000 m3, > 5 000 m3), five categories of vessels and four categories of tonnage. Splitting each of the three categories of ballast water volume into two categories of vessels accounts for 93% of the world fleet that uses ballast water. Creating categories in this way reduces the complexity of assessing the potential costs of measures across a range of vessels. For example, all ships with ballast waters volume of less than 1 500 m3 are passenger and fishing vessels of less than 10 000 tonnes.

Estimates of the number of ships in the global merchant fleet likely to install/retrofit ballast water treatment systems vary considerably depending on the model used, assumptions made, and possibly the juncture in the shipping/shipbuilding cycle at which the estimates were made. (King D.M. et al., 2012[96]) ventured a rough estimate of 68 000 vessels installing on-board BWTS between the time of writing and 2020, assuming full compliance of the Convention. Linder (2017[97]) suggests between 30 000 and 40 000 vessels could be candidates for retrofitting. Clarksons Research (2017[98]) projects potential retrofit demand at around 25 400 ships, plus 1 000 to 2 000 ships per year in newbuild demand. And the OECD (2017[99]) indicated around 27 000 to 37 000 existing vessels might be expected to retrofit BWMS between September 2017 and September 2024.

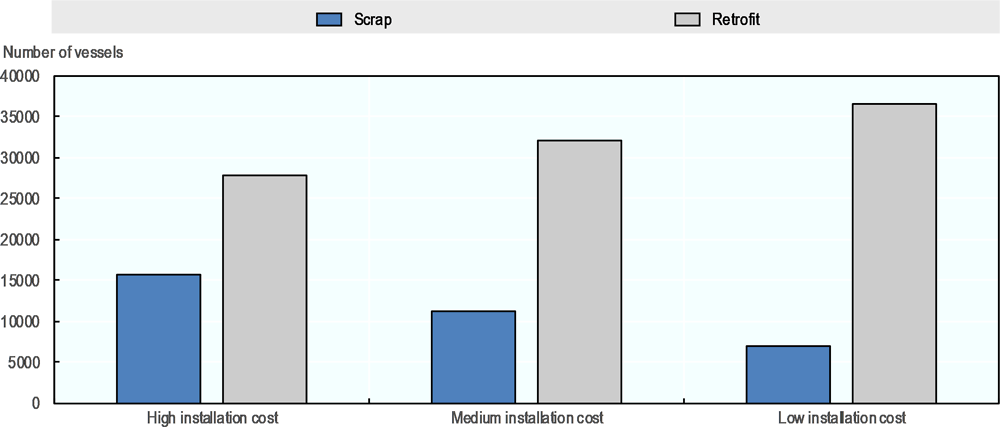

Estimates also vary when it comes to the average cost of retrofitting BWMS. Linder (2017[97]) estimates capital expenditure at USD 80 000-1 500 000, installation cost at USD 100 000-1 000 000, running cost at USD 0.01-0.02 per ton of ballast water, and sampling at USD 75 000-125 000 per vessel. Recent work of the OECD Secretariat (Figure 2.3) assess the impact of the Convention on additional demolition volume and retrofitting activity on the basis of three scenarios (OECD, 2017[99]). These are a high level scenario with installation costs reaching USD 3 million per ship; a medium level scenario with costs of USD 1.5 million per ship; and a low level scenario of costs of USD 0.5 million per ship.

Source: OECD (2017[100]) Analysis of Selected Measures Promoting the Construction and Operation of Greener Ships, http://www.oecd.org/sti/shipbuilding.

A highly simplified calculation, taking 25 400 existing vessels at an average retrofit cost of USD 2 million, would suggest a potential global BWMS market in the order of USD 50 billion. [The figure is in line with estimates of USD 45 billion by Linder (2017[97]), and at the low end of estimates of USD 50-74 billion by King et al. (2012[96]), albeit for the period 2011-2016). What is clear, however, is that the Convention could have a significant impact on the ship repairing industries, generating business opportunities which – under the proviso of further analysis – “may occupy around 20% to 50% of retrofitting capacity in the coming 7 years” (OECD, 2017[99]).

How likely is it that the huge additional potential of the global BWMS market will materialise in the coming years?

Economic theory at least suggests that uptake could well be slower than expected. As noted earlier, concerns have been raised by the shipping industry about the effectiveness of many ballast water treatment systems and their ability to meet consistently IMO and USGC discharge standards. Furthermore, King (2016[83]) indicates that IMO guidelines for certifying and testing are considered by many observers as vague and open to interpretation, and that USGC is thought to be tending towards lowering BWMS testing standards in order to facilitate market access for USCG-certified BWMS. King (2016[83]) goes on to apply two well-established theoretical approaches to analyse the situation in the budding BWMS market. The first, based on work by the economists Akerlof, Spence and Stiglitz, indicates that “quality uncertainty” may prevent markets from developing or at least may result in poorer quality goods or processes, especially in regulation-driven markets. In the BWMS market, lack of strict quality criteria from the outset is likely to see bad quality replace good quality, thereby undermining a potentially successful regulatory regime. The second theoretical approach, namely “game theory”, draws on work by the economists Harsanyi, Nash and Selten, to explore inter alia how regulated industries react to such quality uncertainty by deploying strategies aimed at avoiding or delaying compliance, or reducing the costs of compliance. This would suggest that further action by governments and regulators will be required if an effective and viable regulatory regime is to emerge.

However, a counter-argument can be made to the effect that lowering the USCG standard may in fact prove beneficial, to the extent that it could result in one single common international ballast water standard. After all, the fact that the USCG standard is stricter than the UN IMO standard is thought to have caused uncertainties in the maritime industry – both among developers of ballast water treatment technologies and among ship owners – in respect of which standard to apply and which technology to purchase.

Finally, it should be noted that it may prove difficult to meet the requirements of the Ballast Water Management Convention within the proposed time range given both the limited conversion capacity and the corresponding costs for ship owners.

2.3.5. Concluding observations

Successful implementation of the BWMC, underpinned both by further improvement of conventional treatment technologies and by innovation in greener technologies (such as pasteurisation), holds out the prospect of substantial benefits to marine life and to biodiversity more generally in ocean ecosystems. Economic benefits should arise on multiple fronts: cost savings in the maintenance of coastal and port facilities, enhancement of native fishery stocks, reduction of harmful impacts on marine aquaculture, increased tourist revenues, to name but a few. Even the shipping sector, that undoubtedly shoulders the lion’s share of the costs associated with installation and retrofitting of ballast water treatment systems, ultimately also stands to gain as the knock-on effects expected from compulsory BWT feed through to lower levels of bio-fouling and consequently to fuel savings and lower emissions; see for example Fernandes, (2016[85]). However, it may prove difficult to meet the requirements of the BWMC within the proposed time range given the limited conversion capacity and the corresponding costs for ship owners. There is room for public policy both to encourage innovation in ballast water treatment and to ensure that a viable, effective regulatory system be implemented and sustained.

2.4. Case Study 3: Innovation in marine aquaculture

Marine aquaculture is a striking example of a sector in which scientific and technological innovations are combining in ways that can contribute significantly to both economic and marine-ecosystem sustainability.

2.4.1. The economic and environmental issues at stake

The importance of aquaculture has been growing rapidly in recent decades as an expanding world population, rising incomes and changing food consumption patterns have all combined to push up global demand for fish food. Moreover, with growth in capture fisheries having plateaued, future growth in seafood production is expected to come largely from aquaculture, further underlining its key role in global food security.

Marine aquaculture production – finfish, crustaceans, molluscs and aquatic plants – currently stands at about 59 million tonnes, equivalent to just over one-half of global aquaculture production (FAO, 2018[101]). It produces some 6.6 million tonnes of finfish, almost 5 million tonnes of crustaceans, and almost 17 million tonnes of molluscs (FAO, 2018[101]). The vast bulk of farmed aquatic plants consist of macro-algae or seaweed. At 30 million tonnes, they make up more than half of total marine aquaculture by weight, but in terms of value – USD 11.7 billion – their share is quite small (FAO, 2018[101]). Global production of seaweed has been growing quickly, more than doubling over the period 2005-16, but remains dominated by China and Indonesia, which account for over 85% of the total (FAO, 2018[101]).

Future growth of aquaculture production volumes appears to be set on a slowing trajectory compared to the last few decades. The latest OECD-FAO Agricultural Outlook (OECD/FAO, 2018[102]) for example sees growth slowing to 2.1% p.a. in the period 2018-27 compared to the 5.1% of the previous decade. Important contributing factors are the increasingly scarce raw materials for fish feed, limited availability of appropriate sites at current levels of technology, concern about the environmental footprint of aquaculture, and increasingly crowded coastal waters raising the risk of disputes among other ocean users (shipping, fishing, oil and gas etc.). In addition to these, the licensing environment (Innes, Martini and Leroy, 2017[103]) and national policy have a significant role to play. The development of “investment ready” aquaculture zones for example in places such as Australia show how national policy can encourage production. Conversely, China’s 13th five-year plan (2016-20) is expected to slow growth in domestic production. Objectives there have shifted away from the past emphasis on increasing production and moved towards a more sustainable and market-oriented sector, where the focus is on improving quality and optimising industry structure. This will affect global aquaculture production due to the importance of China’s output at world level (OECD/FAO, 2018[102]).

Higher rates of growth in the coming decades are conceivable, but this would necessitate marked progress at several levels. Improvements in policy, licensing approaches and marine spatial planning could make important contributions. In addition, however, steps would need to include a reduction of the environmental impact of fish farms in coastal regions (e.g. destruction and/or pollution of coastal and aquatic ecosystems, introduction of exotic species into ecosystems, transmission of disease and parasites to wild populations), improved disease management, significantly higher proportions of non-fish feed for carnivorous species, and more rapid advances in the engineering and technologies required to establish offshore aquaculture operations (OECD, 2016[11]). In other words, future fish farming methods will need to be technically more sophisticated and more intelligent, requiring a “shift from experience-driven to knowledge-driven approaches” (Føre et al., 2018[104]). That in turn highlights the need also for scientific and technological innovation on multiple fronts.

2.4.2. Innovations in the pipeline

Innovation in aquaculture has in the past been largely technology driven. With some notable, albeit relatively recent exceptions, it has operated much through technology transfer, i.e. through mono-disciplinary research producing new technologies that emerge from the research system, get diffused by intermediaries such as advisory services, and adopted by users at farm level. Technology transfer is still regarded as the predominant approach to innovation in aquaculture, and is indeed considered the dominant culture in developing countries in South and Southeast Asia and Africa (Joffre et al., 2017[105]). While it has undoubtedly given rise to continuous innovation and remarkable increases in productivity, its practices have been subject to increasing criticism for what is considered to be inadequate consideration of ecological and social sustainability, and for creating growing challenges for ensuing generations of innovation processes. Systemic approaches on the other hand (e.g. systems innovation, socio-ecological approaches) which take a contextual, more holistic perspective on innovation, have become somewhat more widespread in recent years in developed countries. These tend to be multi-dimensional approaches, integrating technical, biophysical, environmental, economic and institutional dimensions into account (Joffre et al., 2017[105]).

In light of the above-described challenges and changes facing aquaculture development in the years ahead, especially for larger-scale intensive fish farming in developed countries, systemic approaches to innovation are moving increasingly into focus. Growing complexity of operation will call for novel solutions. In salmon farming, for example, direct observation as a means to garner key information on the state of populations and optimise their growth and welfare may become unviable for facilities housing millions of individual fish. And if, as expected, farms begin to move offshore2 into more exposed locations, access for personnel will become more problematic and remote automated operation more necessary (Føre et al., 2018[104]).

What kind of innovations are in the pipeline, which would contribute to addressing many of the challenges outlined above? What follows is an overview of advances unfolding in the various phases of aquaculture planning, implementation and operation, namely: aquaculture site selection, breeding, feeding, waste control, health monitoring and treatment, and engineering solutions.

Aquaculture site selection and area-wide assessment

Earth observation, with its exceptional spatial coverage, is considered to have substantial potential to support aquaculture management across a wide range of objectives, including aquaculture site selection, mapping of fish farm locations and surrounding area, as well as environmental monitoring (e.g. water quality) and the identification and tracking of toxic algal blooms (Kim et al., 2017[24]). While earth observation has been in use for some years in aquaculture research, recent advances in sensing can be expected to strengthen its contribution to improved aquaculture management in the years to come. Recent years have seen improvements in remote sensing with very high spatial resolution on board satellites programmed to revisit at shorter intervals, thereby expanding the capacity for tracking and monitoring sites. More such satellites are scheduled.

High data costs can of course limit access to advanced remotely sensed data, especially for developing countries, but here too the situation is evolving. Ever more high-resolution data from optical and radar satellites are becoming downloadable free of charge. The United States Geological Survey’s decision in 2008 to provide free access to its Landsat data archives proved ground-breaking in this respect. And more is on the horizon with the free and open data policy that applies to the Copernicus programme of the European Space Agency from its high resolution Sentinel-1A/B radar satellites and the optical Sentinel-2A/B sensors (Ottinger, Clauss and Kuenzer, 2016[106]).

Identifying appropriate sites for marine aquaculture is key to successful operation. On a smaller spatial scale than earth observation, a number of other useful tools exist for the purpose of site selection. These include for example GIS-based mapping, and modelling. GIS-based mapping affords access to marine and coastal datasets providing information for fish farm operators on availability of potential sites, as well on key factors such as environmental interactions and the presence of other, possibly competing ocean users. Recent progress has made it possible to combine GIS-based mapping with advanced modelling that provides further essential information such as predictions on oceanography, currents, animal growth, productivity and ecological environmental effects. The result is considerable enhancement of the outcome of the site-selection process by simultaneously augmenting farm productivity and reducing adverse impacts on the marine environment (Bricker et al., 2016[107]; Lader et al., 2017[58]).

Algal blooms figure among the greatest existential hazards to aquaculture. Around 300 different types of algal bloom have been identified, of which about one-quarter are toxic. When toxic algal blooms occur in shallow waters, they may pose a direct threat and can lead to severe reductions or complete loss of entire harvests. As non-toxic phenomena, they may also pose an indirect threat insofar as they can cause oxygen depletion (Ottinger, Clauss and Kuenzer, 2016[106]). In recent years, harmful algal blooms (HABs) of numerous varieties have occurred in a geographically wide range of waters: in North America (from New York to the Gulf of Mexico and the Pacific coasts of Canada and northwest United States), Scandinavia, Scotland, the Canary and Madeira Islands, and the Spanish and French Mediterranean, to name but a few. Harmful algal blooms are a natural occurrence in many areas and do not necessarily result from anthropogenic activity, and vary considerably over time, space and toxicity. Moreover, with growing climate change pressures, it is considered conceivable that harmful algal blooms may increase in frequency and severity (Wells et al., 2015[108]).

The economic cost of algal blooms is considerable. For example, in 2016 a series of HAB events caused severe damage to aquaculture in Chile. Salmon farmers lost some 39 million fish, equivalent to a harvest weight of 100 000 metric tons and a value of some USD 800 million (Anderson and Rense, 2016[109]). Shetland lost about half a million fish to one single harmful bloom in 2013. And until recently, the annual losses alone to the mussel industry in France, Ireland, Portugal, Spain and the United Kingdom totalled over EUR 30 million (Copernicus, 2016[110]). Looking to the future, harmful algal bloom events seem set to increase (Wells et al., 2015[108]).3 That, combined with expanding marine aquaculture capacity around the world, suggests the possibility of mounting economic costs in years to come unless science and technology begin to make substantial progress in developing an effective forecasting toolbox for early action (e.g. moving fish cages or reducing stocking density, or early or delayed harvest of shellfish).

The way forward consists in combining multiple approaches – earth observation (EO), in situ remote sensing, geographic information systems, new analytical tools for toxins, and mathematical modelling including algorithms. Although few in number, such systems that combine observation, modelling, etc. to predict harmful algal blooms do exist. In the United States, for example, the National Oceanic and Atmospheric Administration (NOAA) operates a forecasting system (HAB-OFS) for Florida and Texas that is based on a mixture of satellite imagery, field observations and mathematical models. A limitation is that it only identifies mono-specific high biomass blooms that can be detected from space with the help of ocean colour algorithms (Davidson et al., 2016[86]).

An additional example of such an integrated approach is the “ASIMUTH” project (Applied Simulations and Integrated Modelling for the Understanding of Toxic and Harmful Algal Blooms) set up as a response to the demand for short-term forecasts of harmful algal blooms events along the western European seaboard using earth observation (EO) data (Davidson et al., 2016[86]). Remote sensing satellite data and monitoring images track chlorophyll and water temperature. The system downscales the products of the Copernicus Marine Environment Service (CMEMS) and brings them together with biological data and input from harmful algal bloom experts to distribute warning bulletins to aquaculture producers via the internet or mobile devices. This permits the operators of fish and shellfish farms to make contingency plans (e.g. earlier harvest) to reduce the impact of the algal bloom event.

The benefits are twofold. Economic benefits are derived from accurate forecasting, and from timely action by farm operators. (Savings for mussel farmers in five major European aquaculture producing countries are estimated at over USD 2.5 million per annum (Copernicus, 2016[110]). Public health benefits are derived in the form of lower contamination rates of produce and lower impacts on human health.

Breeding

Selective breeding in aquaculture is generally aimed at raising profit rates through increasing harvest weight, improving disease resistance or shortening the time to harvest. Over recent years, breeding programmes at company level have shown that they can be highly profitable. In the case of sea bass or sea bream, for example, revenues typically surpass investment costs after five years and gross margins continue to increase thereafter. Selective breeding programmes for Atlantic salmon in Europe are estimated to raise production by 0.9% per year and additional profits by a total of almost EUR 31 million per annum. For sea bass, sea bream and turbot combined, extra annual production through selective breeding is estimated at 1 700 tonnes, and extra annual profits at EUR 2.7 million. Profits are expected to double in the coming years as more businesses launch selective breeding for sea bass and sea bream.

However, profitability alone may not remain the guiding principle in future, as concerns about the environmental impacts of marine aquaculture are growing. For example, excess feed and nutrient excretion contribute significantly to local eutrophication. Using European sea-cage farmed sea bass as an illustration, Besson et al. (2017[111]) show that the expected increase in sea bass production of almost 14% between 2014 and 2017 is likely to raise the rate of eutrophication by almost the same percentage, if nothing is undertaken to mitigate this. In addition, according to Komen (2017[112]), climate change can be expected to lead to rising and more extreme water temperatures, which in turn would exacerbate the problem.

In general, profitability and the potential environmental risks and impacts of marine aquaculture will vary considerably across regions and are influenced by a whole host of factors ranging from the number and density of cages and the species being farmed, to the specific ecology and environmental conditions of the farm location.

But there is clearly a place for selective breeding in future efforts to achieve a greater balance between business development and environmental sustainability. Increasing fish’s feed conversion ratios could considerably reduce the impact of excess nutrients on the environment while lowering feed costs and raising profitability. The economic and environmental sustainability of aquaculture already features among fish breeders’ key objectives (Besson et al., 2017[111]). But tomorrow’s breeding programmes will also need to consider the challenge of strengthening an animal’s resilience to changes in climate and environment, furnishing yet more incentives to re-orient breeding programmes towards environmental values.