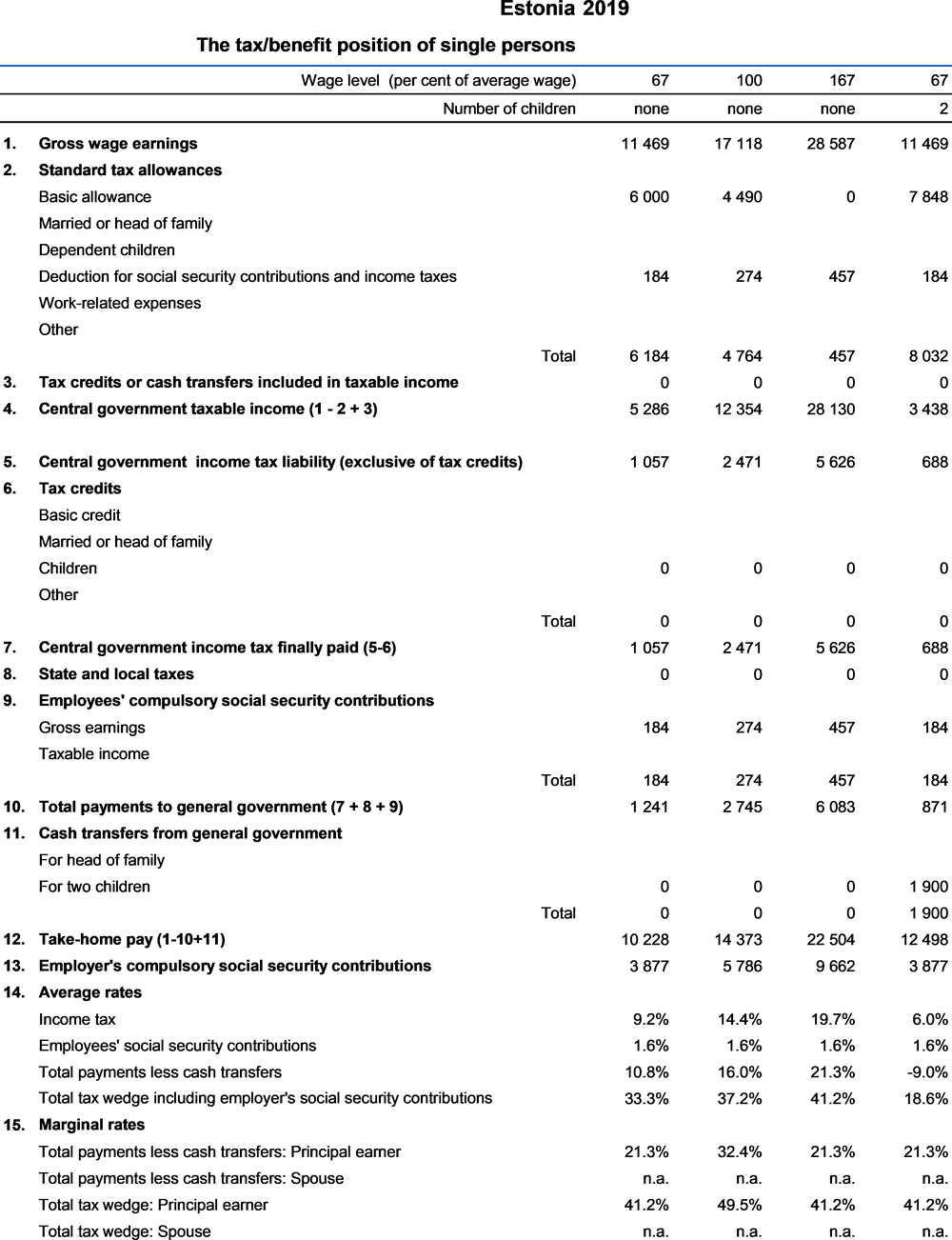

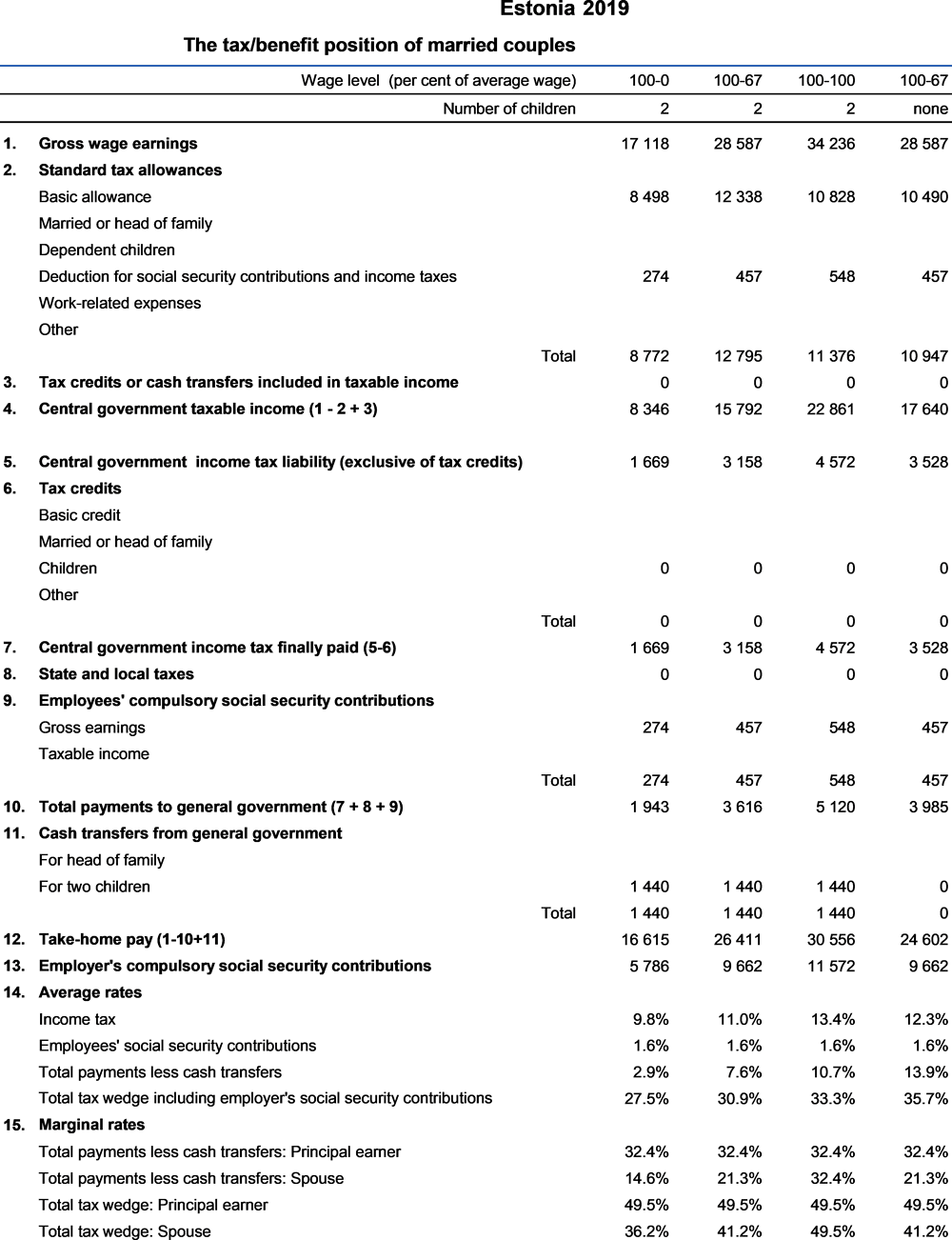

copy the linklink copied!Estonia

This chapter includes data on the income taxes paid by workers, their social security contributions, the family benefits they receive in the form of cash transfers as well as the social security contributions and payroll taxes paid by their employers. Results reported include the marginal and average tax burden for eight different family types.

Methodological information is available for personal income tax systems, compulsory social security contributions to schemes operated within the government sector, universal cash transfers as well as recent changes in the tax/benefit system. The methodology also includes the parameter values and tax equations underlying the data.

The Estonian currency is the Euro (EUR). In 2019, EUR 0.89 was equal to USD 1. In 2019, the average worker in Estonia earned EUR 17 118 (Secretariat estimate).

copy the linklink copied!1. Personal income tax system

1.1. Central government income tax

1.1.2. Tax allowances

1.1.2.1. Standard tax reliefs

-

A general (basic) allowance of EUR 6000 is deductible from individual income in 2019. It starts declining from income of 14 400 and reaches EUR 0 at EUR 25 200. From 1 January 2017, the supplementary basic allowance for the spouse came into force. The spouse’s yearly income must be below EUR 2 160 and the family`s total yearly income must be below EUR 50 400.

-

A child allowance of EUR 1 848 is also deductible from income for each of the second and any subsequent children up to and including the age of 16.

-

Relief for social security contributions: Employee’s compulsory contributions for unemployment insurance are deductible for income tax purposes.

-

Tax credits: was abolished from 2017.

1.1.2.2. Non – standard tax reliefs applicable to income from employment

-

II pillar pension contributions: In 2019, these represent voluntary payments to private funds for all employees and are paid at a rate of 2% of earnings.

-

Housing loan interest, educational costs, gifts and donations are deductible from taxable income within upper limits of EUR 1 200 and 50% of taxable income per year. Housing loan interest deductions upper limit is 300€ within that 1 200€ from 2017.

-

Voluntary pension contributions (III pillar): Contributions paid by a resident to the provider of a pension plan based in Estonia or in another EU Member State according to a pension plan that is approved and entered into a special register in accordance with the pension legislation are deductible from taxable income. In 2019 such deductions are subject to an annual limit of a sum equal to 15% and maximum of EUR 6 000 of the employee’s, public servant`s or members of legal person management or control body income in a calendar year.

copy the linklink copied!2. Compulsory social security insurance system

The compulsory social security insurance system consists of three schemes as follows:

-

pension insurance;

-

health insurance;

-

unemployment insurance.

2.1. Employees’ contributions

Employees pay 1.6% of their earnings in contributions for unemployment insurance. The taxable base is the total amount of the gross wage or salary including vacation payments, fringe benefits and remuneration of expenses related to work above a certain threshold. The assessment period is the calendar month.

2.2. Employers’ contributions

Social security insurance contributions are also paid by employers on behalf of their employees. The taxable base and the assessment period are the same as for employees’ contributions. The employers’ contribution rates are applied in two parts:

-

Unemployment insurance – 0.8% of employee earnings.

-

Pension and health insurance – as follows for monthly earnings above EUR 500.

In addition there is a lump sum payment for each employee of EUR 165.00 per month (split between pensions and health insurance on a 20:13 basis).

copy the linklink copied!4. Universal cash transfers

4.2. Transfers for dependent children

Estonia’s family benefits are designed to provide partial coverage of the costs families incur in caring for, raising and educating their children.

The state pays family benefits to all children until they reach the age of 16. Children enrolled in basic or secondary schools or vocational education institutions operating on the basis of basic education have the right to receive family benefits until the age of 19. Applications for the allowance are made on an annual basis and the payments are not taxable. The values of these benefits in 2019 are shown in the table below. The single parent child allowance is paid for each child. From 1 July .2017 the parents allowance for families with three to six children was introduced, EUR 300 per month. Parents allowance for families with seven or more children was increased from EUR 168.74 per month to EUR 400 per month from1 July 2017.

In addition there are nine other types of family benefits for which payment depends on either the age of the child(ren) and/ or the status of the person(s) looking of them: maternity benefit; childbirth allowance; parental benefit; child care allowance; conscript’s child allowance; child’s school allowance, child allowance for a child under guardianship or foster care; start in independent life allowance; adoption allowance (single payment). These are not included in the modelling.

In addition to existing benefits, from July 1, 2013 the need-based child benefits were introduced. Need-based family benefit income threshold is based on Statistical Office relative poverty threshold published by the 1st of March in a year before current budget year. In 2017 the need based threshold is EUR 394 in a month for the first household member. For every other at least 14-years old member the threshold is EUR 197 and for the younger members EUR 118.2 in a month. Need-based family benefit is in 2017 EUR 45 in a month for single child family and EUR 90 for families with two or more children. These need-based benefits were abolished from 2018.

copy the linklink copied!5. Main changes in tax/benefit system since 2005

-

The personal income tax rate was steadily reduced from 24% in 2005 to 21% in 2008. In 2015 it was reduced to 20%.

-

The child tax allowance applied for the third and subsequent children for 2005 and the second and subsequent children in 2006 and 2007. It applied to all children in 2008 and then returned to the 2007 position in 2009.

-

The employee unemployment contribution rate was reduced from 1% to 0.6% in 2006 and then raised in 2 stages to 2.8% at the end of 2009. The corresponding rates for employers were a reduction from 0.5 % to 0.3% in 2006 increasing to 1.4%. In 2013 the employee unemployment contribution rate was reduced from 2.8% to 2.0% and the corresponding rate for employers from 1.4% to 1.0%. In 2015 the employee unemployment contribution rate was reduced from 2.0% to 1.6% and the corresponding rate for employers from 1.0% to 0.8%.

-

In addition to existing benefits, from July 1, 2013 the need-based child benefits were introduced. Further details in section 4.2 on cash transfers. These were abolished from 2018.

-

From 2016, a non-payable tax credit for low-income earners (“madalapalgaliste tagasimakse”) was introduced. Further details in section 1.1.2. on tax allowances. It was abolished from 2017.

-

From 2017 the possibility to use spouse`s basic tax-free allowance was reformed. From January 1st 2017, the supplementary basic allowance for the spouse came into force. The spouse’s yearly income must be below EUR 2 160 and the family`s total yearly income must be below EUR 50 400.

copy the linklink copied!6. Memorandum items

6.1. Average gross annual wage earnings calculation

In Estonia the gross earnings figures cover wages and salaries paid to individuals in formal employment including payment for overtime. They also include bonus payments and other payments such as pay for annual leave, paid leave up to seven days, public holidays, absences due to sickness for up to 30 days, job training, and slowdown through no fault of the person in formal employment.

The average gross wage earnings figures of all adult workers covering industry sectors B–N by NACE Rev.2 are estimated with average wage growth rate forecast of Estonian Ministry of Finance.

6.2. Employer contributions to private pension and health schemes

Some employer contributions are made to private health and pension schemes but there is no relevant information available on the amounts that are paid.

2019 Tax equations

The equations for the Estonian system are mostly on an individual basis.

The functions which are used in the equations (Taper, MIN, Tax etc) are described in the technical note about tax equations. Variable names are defined in the table of parameters above, within the equations table, or are the standard variables “married” and “children”. A reference to a variable with the affix “_total” indicates the sum of the relevant variable values for the principal and spouse. And the affixes “_princ” and “_spouse” indicate the value for the principal and spouse, respectively. Equations for a single person are as shown for the principal, with “_spouse” values taken as 0.

Metadata, Legal and Rights

https://doi.org/10.1787/047072cd-en

© OECD 2020

The use of this work, whether digital or print, is governed by the Terms and Conditions to be found at http://www.oecd.org/termsandconditions.