copy the linklink copied!Slovak Republic

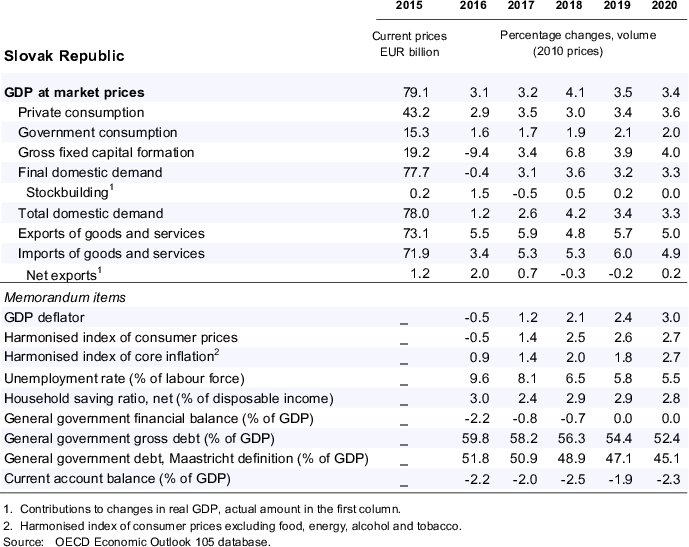

Growth is projected to remain strong over the next two years, driven mainly by domestic demand. Low unemployment and rising wages will support household consumption. Investment growth will remain solid, underpinned by favorable financial conditions and by the disbursement of EU structural funds. External demand is weakening, but the launch of a new production line in the automotive sector will support gains in export market shares. Consumer price inflation will remain above 2% as the labour market tightens further.

The government should reach budget balance by 2019 as planned, given the absence of spare capacity and medium-term challenges posed by population ageing. However, if downside risks were to materialise, fiscal policy should stand ready to mitigate the downturn. The government also needs to enhance public-sector efficiency. In particular, education reform and measures to enhance Roma integration are important to make growth more inclusive.

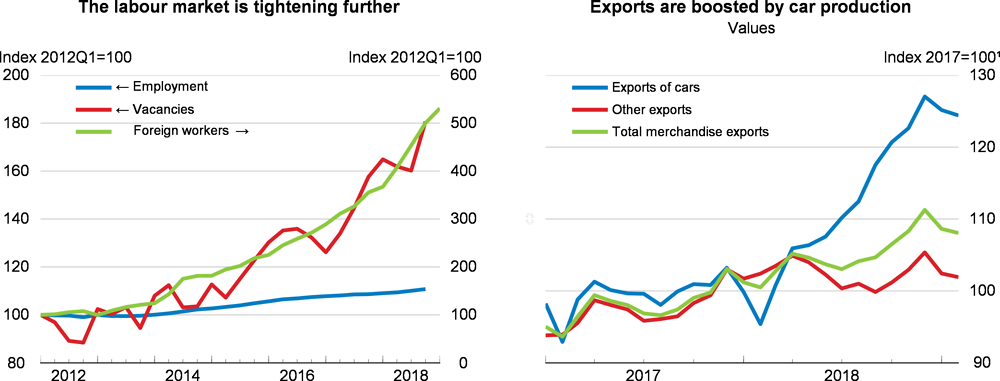

Growth is moderating but still robust

Economic growth slowed at the end of 2018 due to a weaker external environment, but domestic demand remains strong. Investment activity has increased, fuelled by a faster absorption of EU funds, favourable financial conditions and continuous investment in car manufacturing. Household consumption continues to expand on the back of a buoyant labour market. Employment growth has slowed somewhat, reflecting persistent labour shortages. New production capacity in the automotive sector has boosted exports despite a weaker external environment. Imports have been growing faster than exports, reflecting import-intensive investment and strong household consumption. Inflation moderated at the end of 2018, mainly as a result of a decline in food price inflation, but it remains above 2%.

1. Six-month moving average.

Source: OECD Economic Outlook 105 database; Eurostat; Central Office of Labour, Social Affairs and Family; and Statistical office of the Slovak Republic.

Fiscal policy should remain prudent

The government’s fiscal policy objective is to reach a balanced budget by 2019, but the risk of slippage has increased. The government should maintain its objective, given robust economic growth and the medium-term challenges posed by rapid population ageing. The Slovak Republic has one of the fastest ageing populations in the OECD, which will significantly increase ageing-related spending in the future. The recent change to the constitution, which prevents increasing the pension age above the age of 64, will add to these fiscal pressures. A prudent fiscal stance would also make more room for manoeuvre in the event of shocks, as Slovakia’s open economy is very much exposed to international trade tensions and volatility. If downside risks materialised and growth slowed significantly, fiscal policy should stand ready to limit the downturn.

Priority spending should be financed by a combination of expenditure switching and improved efficiency. The government should also persist in its efforts to improve tax collection. Structural reforms are needed particularly in the area of education and more needs to be done to improve the well-being of Roma, who suffer from significant social exclusion. Early-childhood education and better-trained teachers are necessary parts of such reforms.

Growth is projected to remain robust

Growth will remain robust, but slow somewhat as the effects of new production capacity in the car industry will fade. Export growth is expected to decelerate in 2020. Private consumption will continue to grow strongly thanks to strong employment and wage growth, supported by the substantial increase in public sector wages in 2019 and 2020. Investment activity will benefit from the rising absorption of EU funds and from the increase in defence expenditure. Narrowing spare capacity will gradually push consumer price inflation towards 3%. The main risk is on the external side, as the Slovak economy is particularly exposed to any disruption in trade, given its inclusion in global value chains and significant reliance on the automotive sector. On the upside, supportive financial conditions and rising wages could strengthen private domestic demand even more than projected.

Metadata, Legal and Rights

https://doi.org/10.1787/b2e897b0-en

© OECD 2019

The use of this work, whether digital or print, is governed by the Terms and Conditions to be found at http://www.oecd.org/termsandconditions.