copy the linklink copied!Chapter 3. The business environment for SMEs and entrepreneurship in Brazil

This chapter gives an overview of the main strengths and weaknesses of the business environment for small- and medium-sized enterprises (SMEs) and entrepreneurs in Brazil. Brazil’s participation in global trade is only half the OECD average, which limits opportunities for SME exports and SME participation in global supply chains. Product market regulations, including tax compliance, continue to be burdensome for many companies, including larger SMEs ineligible for one of the two existing preferential tax regimes (Simples Nacional and Micro Empreendedor Individual [MEI]). Credit market conditions are also tight for SMEs, as shown by a high interest-rate spread between SME loans and large-company loans. Nonetheless, the government has introduced some important reforms to remedy these problems. In the area of trade policy, local content requirements are being progressively lifted. MEI and Simples Nacional have simplified considerably the regulatory and tax environment for micro and small companies with gross annual revenues respectively below BRL 81 000 and BRL 4.8 million. And a series of policy reforms have reduced the degree of credit subsidy and banking concentration in the domestic credit market.

copy the linklink copied!Macroeconomic conditions

Brazil is recovering from one of the deepest recessions in its history

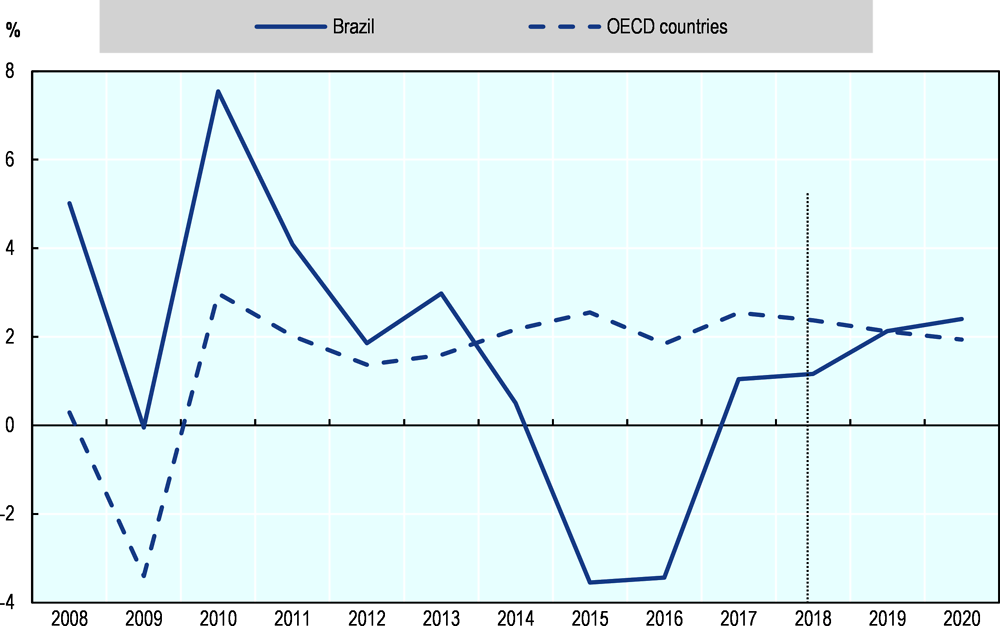

Brazil grew faster than the OECD area in the wake of the 2008 global financial crisis but experienced one of the worst recessions in its history in 2015-16. Since 2017, gross domestic product (GDP) growth has turned positive again, with growth rates expected to be in line with the OECD average in the coming years (Figure 3.1).

Source: OECD (2018a), OECD Economic Outlook, Volume 2018 Issue 2, https://dx.doi.org/10.1787/eco_outlook-v2018-2-en.

High government deficit is a reason for concern

In 2015, at the peak of the economic recession, Brazil’s government deficit reached a record high of more than 10% of GDP. Despite the end of the recession in 2017 and further economic recovery expected in 2019 and 2020, the government deficit is expected to stay above 6% of GDP in 2020, which is the outcome of structural issues such as high and growing spending on pensions and social programmes (World Bank, 2017). The pension reform has, indeed, become one of the main policy priorities of the new government that took office in early 2019.

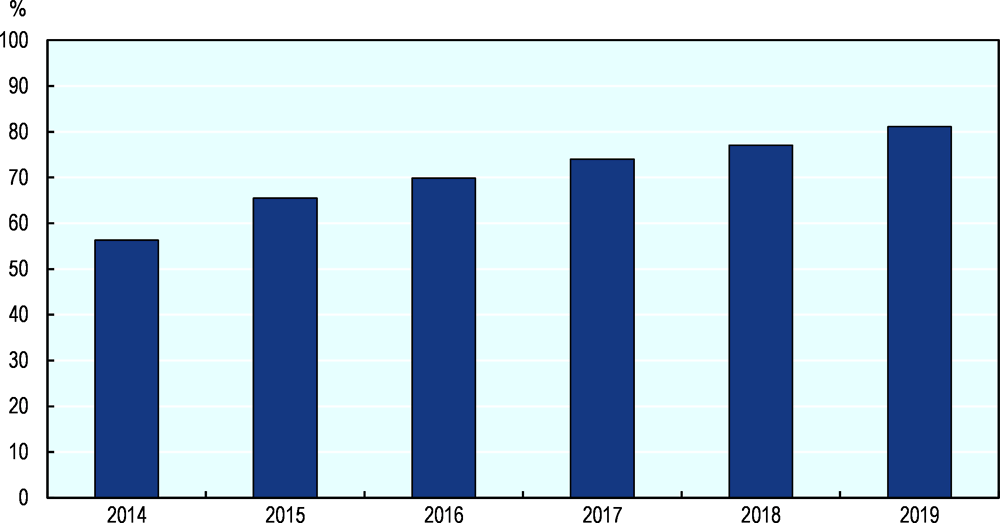

Government debt in relation to GDP rose from 56% in 2014 to 81% in 2019 (Figure 3.2). The government needs to put in place a major fiscal effort to level the budget, corresponding to 5% of GDP when only the primary balance (i.e. net of interest payments) is taken into account. Without major spending cuts, notably on pensions, public debt is expected to rise further, exceeding 100% of GDP in 2023 and 150% in 2030. The federal government also pays high interest rates on its sovereign debt; in 2018, when the debt was about 77% of GDP, interest-rate expenditures totalled 8% of GDP, well above the OECD average of 2.6% (World Bank, 2017).

Source: OECD Economic Outlook Database.

The federal government also needs to monitor public debt at the state level. This is illustrated by the case of the states of Rio de Janeiro, Rio Grande do Sul and Minas Gerais, which declared a state of financial calamity in 2016 after being unable to repay their debt amounting to 12% of GDP (World Bank, 2017).

copy the linklink copied!Education, skills and the labour market

Education and skills levels

Brazil’s educational attainments are lower than those of other countries with similar levels of spending on education

Brazil has made significant strides when it comes to education. In particular, participation in education for children between 5 and 14 has been made universal. Between 2007 and 2017, the proportion of the population aged 25-34 with an education level below upper secondary declined from 53% to 36%. As many as 17% of Brazilians in the same age group attained tertiary education in 2017, an increase of 7 percentage points from 2007 (OECD, 2018b). Enrolments in higher education also tripled between 2000 and 2015 (World Bank, 2017).

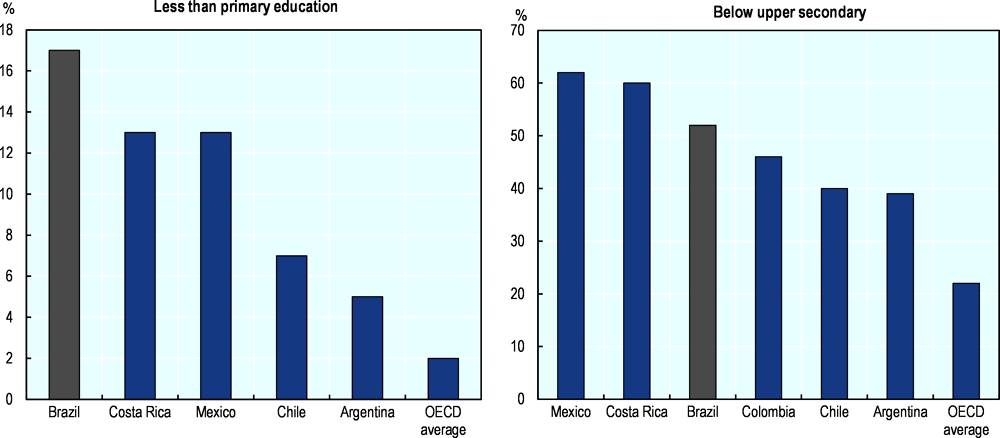

Nonetheless, many challenges remain. Just over half of the population aged 25-64 had not attained upper secondary education in 2017, more than double the OECD average (22%). While Brazil performs better than Costa Rica and Mexico, it does worse than Argentina, Chile and Colombia among other Latin American countries. Moreover, 17% within the same age group (25-64 years old) lacks primary education in Brazil, which is higher than any other Latin American country for which data are available (Figure 3.3). Enrolment rates in Brazil also fall sharply after the age of 14. In 2016, 69% of Brazilians aged 15-19 and 29% of those aged 20-24 were enrolled in some form of education, compared with OECD averages of 85% and 42% respectively (OECD, 2018b).

Source: OECD (2018b), Education at a Glance 2018: OECD Indicators, OECD Publishing, Paris, https://dx.doi.org/10.1787/eag-2018-en.

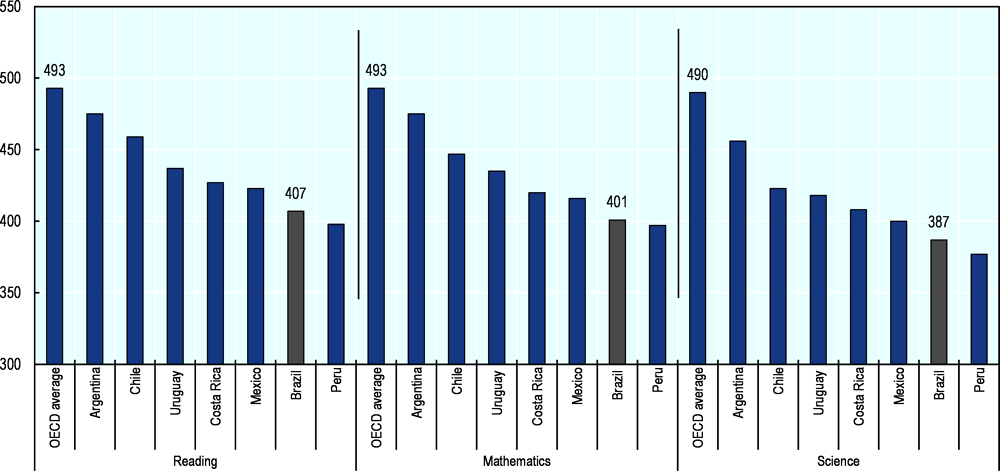

Brazil scores relatively poorly in the OECD Programme for International Student Assessment (PISA), which ranks the performance of 15-year-old students on standardised tests in literacy, mathematics and science. Brazil’s scores are below the OECD average in all three indicators and, with the exception of Peru for reading and mathematics, also below those in other Latin American countries covered by PISA (Figure 3.4).

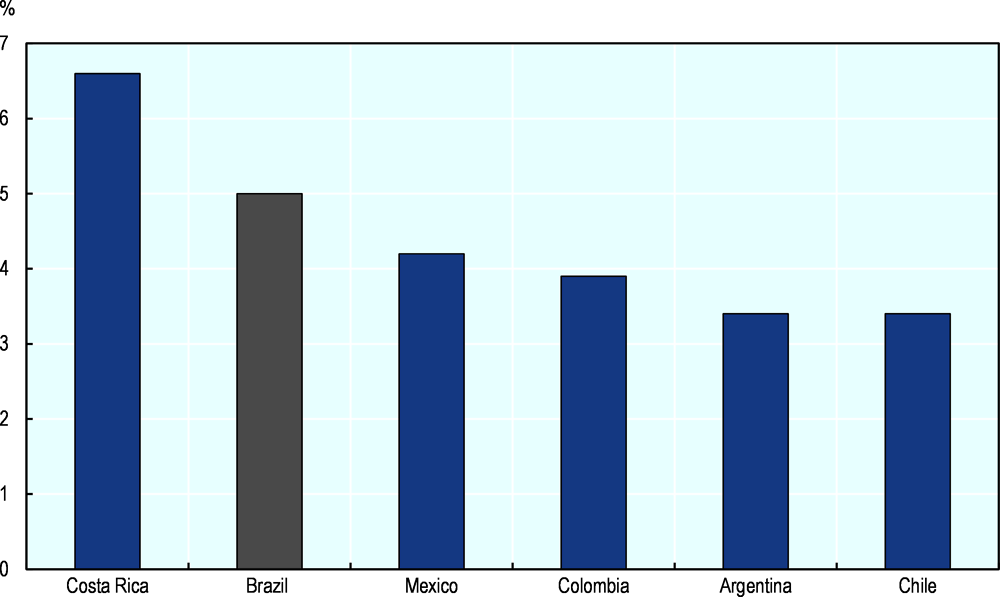

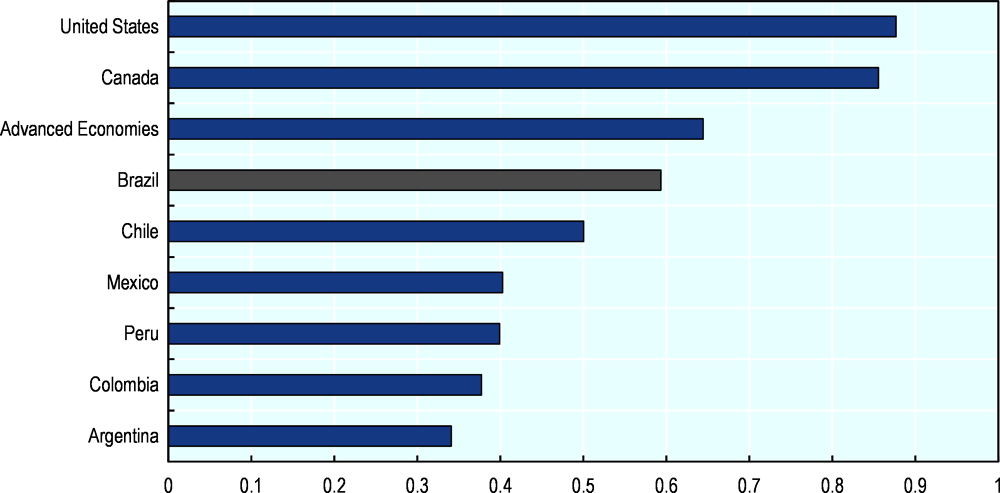

Nonetheless, Brazil’s spending on education corresponds to 5% GDP, which is higher than other Latin American countries such as Argentina, Chile, Colombia and Mexico, all of which have higher average PISA scores (Figure 3.5). Thus, there is room for improving the impact of education spending on education outcomes.

Note: The test scores for Argentina are from Buenos Aires only.

Source: OECD (2016), PISA 2015 Results (Volume I): Excellence and Equity in Education, https://dx.doi.org/10.1787/9789264266490-en.

Source: OECD (2018b), Education at a Glance 2018, OECD Publishing, Paris, https://dx.doi.org/10.1787/eag-2018-en.

Recent labour market trends and policies

Brazil’s skills shortages have eased in the aftermath of the recession

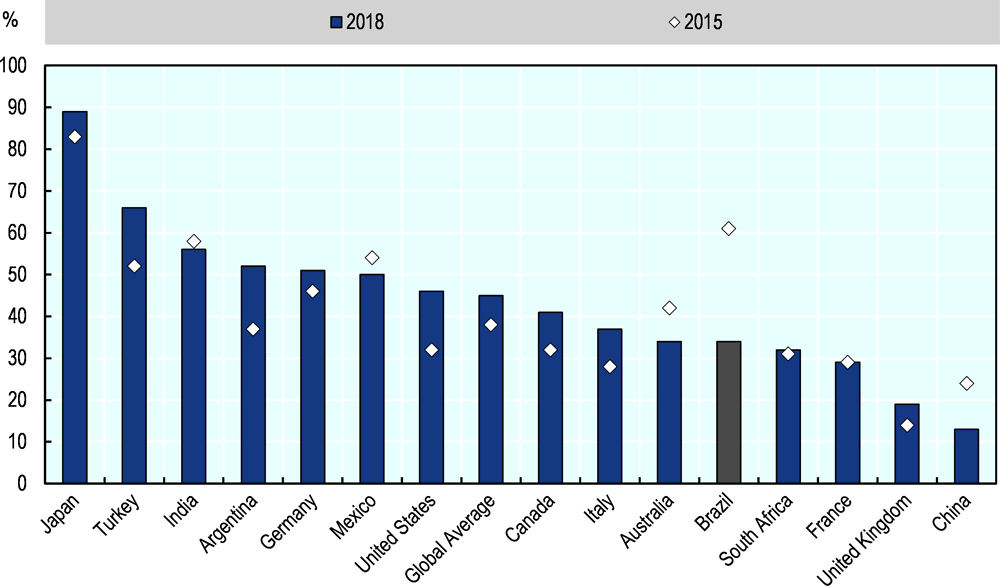

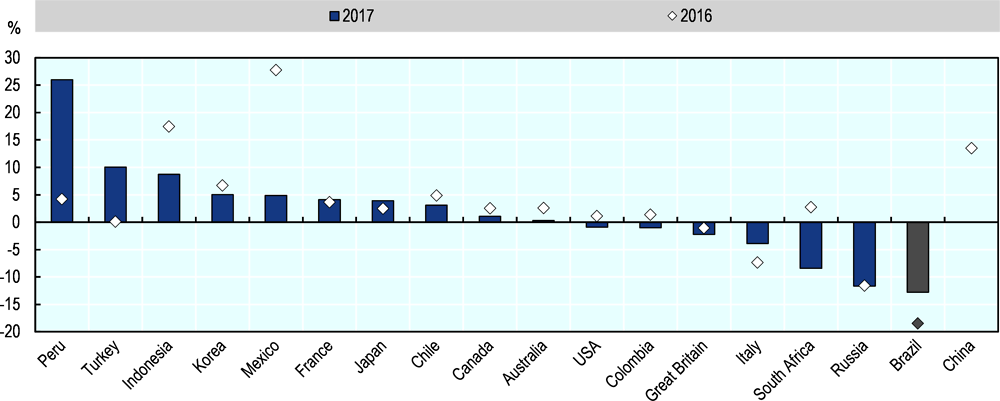

A large-scale survey by Manpower, a Human Resources multinational, show that before the 2015-16 recession, more companies in Brazil (61% of the total) than in other countries were likely to report recruitment problems; after the recession, however, this proportion fell significantly (34%) (Figure 3.6). To the extent that this drop is linked to the consequences of the recession – companies are not pressed to hire during economic doldrums – skills shortages may re-emerge as the economy recovers.

Source: Manpower Group 2018 Talent Shortage Survey.

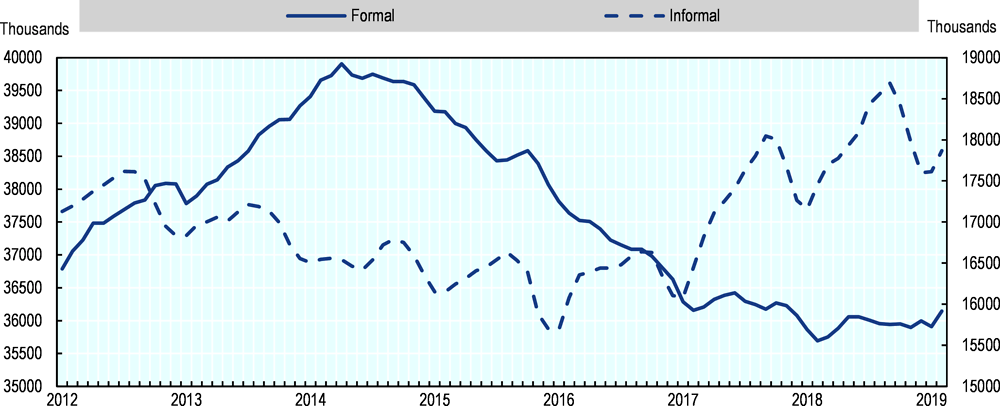

The recession has caused an increase in informal employment

Following the 2015-16 recession, the official unemployment rate reached 12% in 2017, only to decline marginally in 2018. Unemployment is forecast to decline further in 2019 and 2020, although it should remain above the pre-crisis levels. The rise in unemployment has come with an increase in informal employment: the share of workers in the informal labour market rose from 21.7% in April 2015 to 25.0% in April 2018 (Figure 3.7).

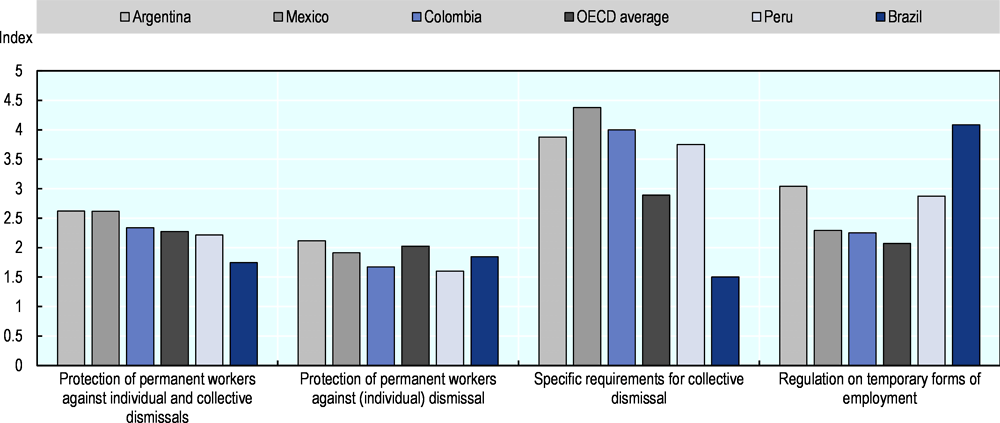

The government has recently introduced an important labour market reform

The OECD Employment Protection Legislation indicators show that Brazil has relatively few restrictions on the dismissal of permanent workers, while regulations on temporary contracts are stricter than the OECD average and in other Latin American countries (Figure 3.8).

Note: The left-hand scale refers to formal employment, the right-hand scale to informal employment.

Source: OECD (2018c), Getting Skills Right: Brazil, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264309838-en.

Note: Data from Brazil are from 2012, data from Mexico are from 2013. The second indicator is a subcomponent of the first, focussing only on individual dismissals that are typically regulated less strictly.

Source: OECD/IAB Employment Protection Database.

Brazil introduced major changes to its labour law in 2017 (Consolidação das Leis do Trabalho). One of the main aims of the reform has been to introduce more flexibility in the labour market. For example, the new law allows probation periods of up to 90 days, which have indeed become a common practice. The reform also allows the use of fixed-term contracts for a duration of up to two years in total and has introduced a regulatory framework for intermittent work and labour outsourcing. One of the main outcomes of the reform has been a sharp reduction in the number of labour lawsuits, from more than 2 million between January and September 2017 to less than 1.3 million over the same period in 2018.1 A survey conducted in 2017 by the National Industry Confederation (Confederação Nacional da Indústria, CNI) shows that business owners are sanguine about the effects of the labour reform, with increased flexibility in labour contracts considered to be one of its main benefits (CNI, 2017).

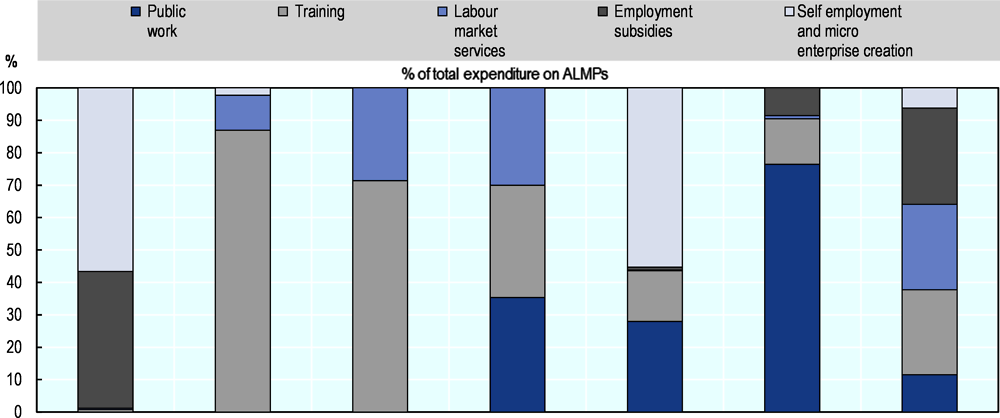

Brazil’s government spending on active labour market policies is mostly focused on self-employment support and employment subsidies

Brazil’s spending on active labour market policies (ALMP) amounts to 0.5% of GDP, which is in line with the OECD average. However, 56% of ALMP spending goes to self-employment support, while 42% goes to employment subsidies under the form of Abono Salarial2 and Salário Familia.3 By contrast, very little support is offered to train displaced workers or to actively assist them in seeking other employment opportunities. This contrasts with most common approaches in OECD and other Latin American countries (OECD, 2018d) (Figure 3.9), although it should be noted that organisations in Sistema S (see Chapters 4 and 5 for more details), which are not formally part of the government, play an important role in training provision in Brazil.

Source: OECD (2018d), OECD Economic Surveys: Brazil 2018, https://doi.org/10.1787/eco_surveys-bra-2018-en.

Overall, Brazil’s ALMP mix does not seem to be well-equipped to tackle unemployment and encourage the transition from informal to formal employment. Abono salarial could, therefore, be reformed to help employers recruit first-time job seekers and/or other disadvantaged workers (such as long-term unemployed and older workers) (World Bank, 2017). ALMP spending could also partially be moved from current dominant programme areas – i.e. self-employment promotion and employment subsidies – to training programmes and labour market intermediation.

Vocational education and training (VET) policies have recently been reformed to increase their effectiveness

Only 9% of Brazilian students in upper secondary education are enrolled in vocational education, compared with the OECD average of 44% (OECD, 2018b). Until recently the main federal policy to increase the number of VET students was PRONATEC (Programa Nacional de Acesso ao Ensino Técnico e Emprego), which between 2011 and 2017 reached about 8 million students through a budget of BRL 14.5 million (OECD, 2018c). Different evaluations, however, point to the modest impact of PRONATEC on the employability and wage of participants. In some cases, the impact has even been estimated to be negative, to the extent that participants in some states had fewer chances of joining the formal labour market than non-participants (Barbosa Filho et al., 2015).

One exception has been the small component of PRONATEC operated by former MDIC, which absorbed 2% of the total number of participants (about 160 000 people) and whose courses were set up at the explicit request of individual businesses through a website called Supertec. Empirical evidence shows that the impact of these demand-driven courses on the employment of participants has been more positive than in the case of other PRONATEC courses. In addition, participants in PRONATEC-MDIC often found employment in firms other than those that had requested the course, thus showing that the training offer had been able to identify local skills shortages (O’Connell et al., 2017).

It follows that one of the main problems associated with the mainstream PRONATEC courses has been precisely their lack of alignment with local skills needs. The programme did engage in some consultations with social partners and the private sector, but not in a structured and regular way. PRONATEC courses had to be selected from a predefined national catalogue, which is probably not the best way to keep up to date with local skills needs. As a result, some Brazilian states developed their own professional training courses outside of PRONATEC to better address local skills demands (OECD, 2018c).

The federal government is expected to launch in 2019 a new VET policy, Emprega Mais (Employ More). This new initiative will seek to address the lack of skilled workforce at the firm level, the mismatch between skills demand and skills supply at the local level and the link between vocational training and employability. Emprega Mais targets three main objectives: the re-insertion of the unemployed in the labour market; the upskilling of existing workers; and the inclusion of the youth in the labour market. It will be important for this new policy to learn from the experience of PRONATEC, notably about the importance of receiving inputs and feedback from the private sector for the design of a relevant training offer.

copy the linklink copied!International trade conditions

Brazil is not sufficiently integrated into global trade

Brazil is not sufficiently integrated into global trade, which is a major impediment to SME internationalisation. Trade flows, defined as the sum of exports and imports, were 29% of GDP in Brazil in 2018, much lower than the OECD, the World and the Latin America and the Caribbean (LAC) averages (respectively 57%, 56% and 47%). Other indicators corroborate Brazil’s limited integration into global markets. The foreign value-added content of gross exports, an indicator of backward trade linkages and integration in global value chains, was 10.2% in 2016. This is slightly above the South and Central America average (9.9%), but significantly below the OECD and G20 averages (respectively 19.3% and 18%) (OECD, 2018e).

Some of the reasons behind Brazil’s limited participation in global trade are relatively high tariff and non-tariff measures, poor infrastructure quality, the large size of the domestic market which reduces the needs for exporting, as well as low export culture and managerial skills of Brazilian small business owners. By way of example, the percentage of imports subject to at least one non-tariff measure is higher in Brazil than the world average: 89% for technical regulations and conformity assessment procedures, 66% for sanitary and phytosanitary measures, and 65% for quantity controls, which are all above the world average (Dutz, 2018).4 As to the quality of infrastructure, between 2013 and 2017, gross capital formation declined by a combined 28% in Brazil (OECD, 2018a). A study by the Inter-American Development Bank (IDB) also finds that lower transport costs, through an improvement in factory-to-port infrastructure, would have a significant impact on trade, particularly on those municipalities that export less because of lack of connections to main roads and railways (Mesquita Moreira, 2013).

The potential benefits of trade liberalisation are large

The potential benefits of trade liberalisation are large. An OECD study simulates the impact linked to: i) a reduction in import tariffs; ii) the lift of local content requirements; iii) a reduction in export taxes. The study estimates that these three policy changes together would increase total exports by around 30%, especially in manufacturing, and would create up to 1.5 million new jobs, especially among low-skilled people (Araújo and Flaig, 2016). Another simulation exercise from the World Bank gauges the economic impact of trade policy reform under three scenarios: i) a unilateral reduction of tariffs by 50% towards non-Mercosur countries and a streamlining of non-tariff measures among Mercosur countries;5 ii) a reciprocal preferential trade agreement between Mercosur and the EU; and iii) a preferential trade agreement between Mercosur and the Pacific Alliance group.6 The study finds large positive impacts on exports in all three scenarios – in the order of magnitude of 7%, 5% and 2% respectively – as well as an impact on GDP of around 2% if all these scenarios were to materialise (Reis et al., 2018).

The government has introduced trade liberalisation reforms

Brazil has recently introduced important reforms in the area of trade liberalisation. In mid-2019, the government published a list of national priority goals that include the reform and reduction of the Mercosur Common External Tariff, the reduction of national tariffs for capital and IT goods under the Mercosur agreement, the adoption of trade facilitation measures, and the negotiation of new free trade agreements.7 Particularly important is the recent free trade agreement signed by Mercosur and the EU in June 2019, which also includes a specific provision to help SMEs tap into global value chains, participate in government procurement and set international joint ventures. This agreement will play a very important role in enhancing openness to trade, but it will have to be ratified by national parliaments to come into effect. With respect to non-tariff measures, Brazil has taken steps to reduce the use of local content requirements and, as part of the Mercosur bloc, it has concluded regulatory coherence agreements with the EU, Mexico and Canada.

Chapter 6 of this report investigates more closely Brazil’s targeted programmes to support SME exports, including export training, export finance, trade facilitation and supplier development programmes.

copy the linklink copied!Public governance

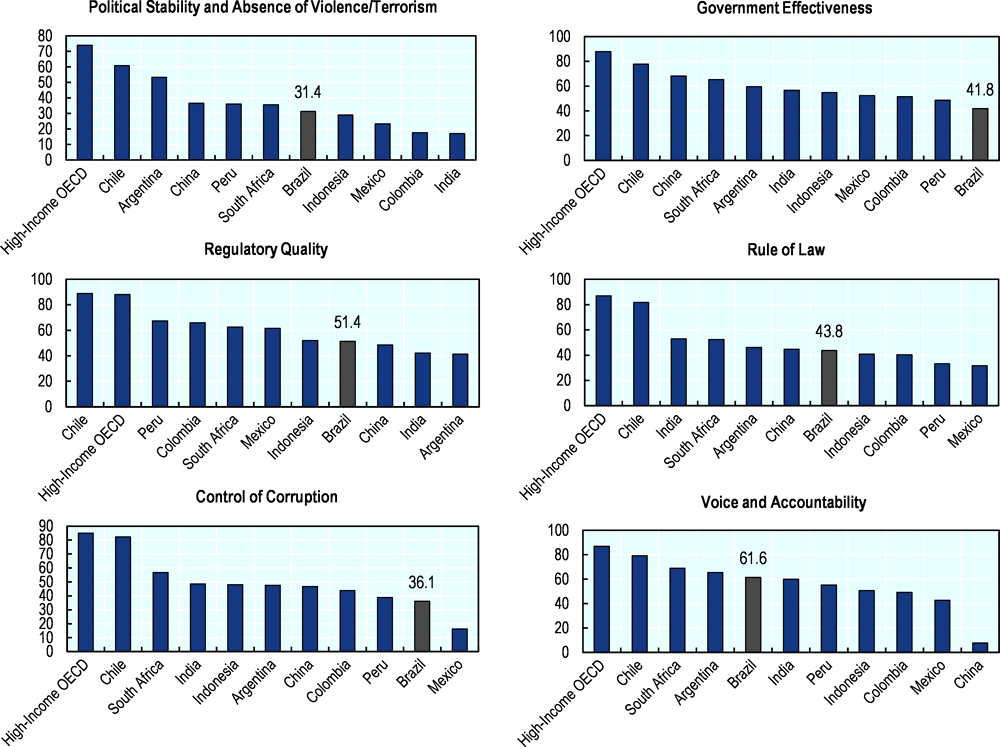

Government effectiveness and transparency is perceived as low in Brazil

The World Bank collects information on the quality of governance through the Worldwide Governance Indicators (WGI). The six indicators – political stability, government effectiveness, regulatory quality, rule of law, control of corruption and voice and accountability – show that Brazil performs poorly compared to other Latin American and emerging economies in the areas of government effectiveness and control of corruption, whereas Brazil’s performance is broadly in line with the other countries in the other indicators (Figure 3.10).

Low trust in the government is also confirmed by Latinobarómetro, a private non-profit organisation that runs a large survey in LAC countries on an annual basis. The 2017 edition showed that only 7% of Brazilians declare trusting their government, lower than any other participating country. In addition, 17% of Brazilians consider corruption to be the most pressing issue, only behind Colombia and Peru (Latinobarómetro, 2018).

While these figures need to be taken seriously, it should be noted that they also come at a time when large-scale corruption has been on the spotlight in Brazil for many years due to the investigation called Lava Jato (car wash), which has been underway since 2014 and has uncovered a vast network of bribes and money laundering involving high-profile politicians and businessmen.

Recent actions to improve public governance should be consolidated

Brazil has taken important actions to improve public governance in recent years, especially through the issuance of Presidential Decree No. 9.203/2017 which aims to establish appropriate internal control and risk management frameworks to tackle corruption. As part of the decree, the government is developing procedures to design, implement, monitor and evaluate integrity programmes, risk management and internal controls (OECD, 2018f).

The Brazilian government has also, by and large, embraced the opportunities that digitalisation can offer to provide services in a more inclusive, transparent and collaborative way. In 2016, the government adopted the Digital Governance Strategy 2016-19, which was updated in 2018. The strategy sets priorities such as “promoting the availability of open government data, boosting the use of digital technologies for transparency purposes, improving the delivery and use of public digital services, securing the take-up of digital identity (…) and increasing citizen participation through digital platforms” (OECD, 2018g).

Note: “High-income OECD” includes all OECD member countries except Mexico and Turkey. Stability and Absence of Violence/Terrorism measures perceptions of the likelihood of political instability and/or politically motivated violence, including terrorism. Government effectiveness reflects perceptions of the quality of public services, the quality of the civil service and the degree of its independence from political pressures. Regulatory quality reflects perceptions of the ability of the government to formulate and implement sound policies and regulations that permit and promote private sector development. Rule of law reflects perceptions about the quality of contract enforcement, property rights, the police and the courts, as well as the likelihood of crime and violence. Control of corruption reflects perceptions about the extent to which public power is exercised for private gain, including both petty and grand forms of corruption.

Source: The Worldwide Governance Indicators (WGI) – World Bank.

copy the linklink copied!The tax environment

The standard tax system

Brazil’s tax burden is high

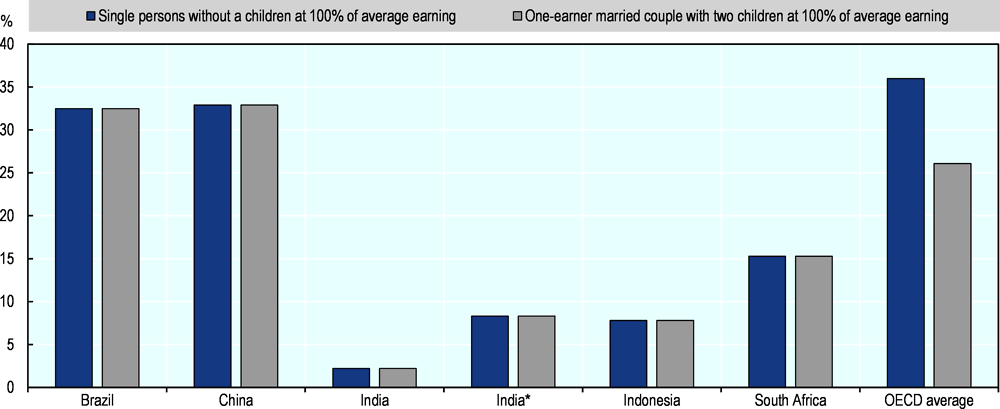

Tax revenues as a percentage of GDP amounted to 32.2% in Brazil in 2016, close to the OECD average of 34.2%, but well above the LAC average of 22.7%. A distinctive feature of the Brazilian tax system is that more than 30% of tax revenues are collected at the subnational level, which is the result of the federal nature of the Brazilian state (OECD/CIAT/IDB/ECLAC, 2018). Brazil raises most of its tax revenues from value-added taxes (VAT) and from corporate taxation. Brazil’s statutory corporate income tax (CIT) rate is indeed 34%, one of the highest CIT rates worldwide (World Bank, 2018a). On the other hand, few tax revenues originate from capital gains tax and from inheritance and property taxes. The former features different tax rates depending on the type and level of investment, making collection difficult. Tax collection on property is undermined by outdated valuation methods and property cadastres. A simplification of capital gains taxation and an overhaul of the cadastre system could help diversify Brazil’s sources of government fiscal revenues and thereby reduce the CIT rate (World Bank, 2018a). Finally, Brazil’s tax wedge on labour (defined as income tax plus employee and employer contributions minus cash benefits as a percentage of labour costs) is comparable to the OECD average and China (Figure 3.11).

Note: This indicator measures income tax plus employee and employer contributions less cash benefits as a proportion of labour costs, 2016. India: This rate applies when the employee works in a firm with more than 20 employees.

Source: OECD (2018h), Taxing Wages 2016-2017. Associated Paper: Selected Partner Economies (Brazil, China, India, Indonesia and South Africa), OECD Publishing, Paris. https://www.oecd.org/tax/tax-policy/taxing-wages-selected-partner-economies-biics-2018.pdf.

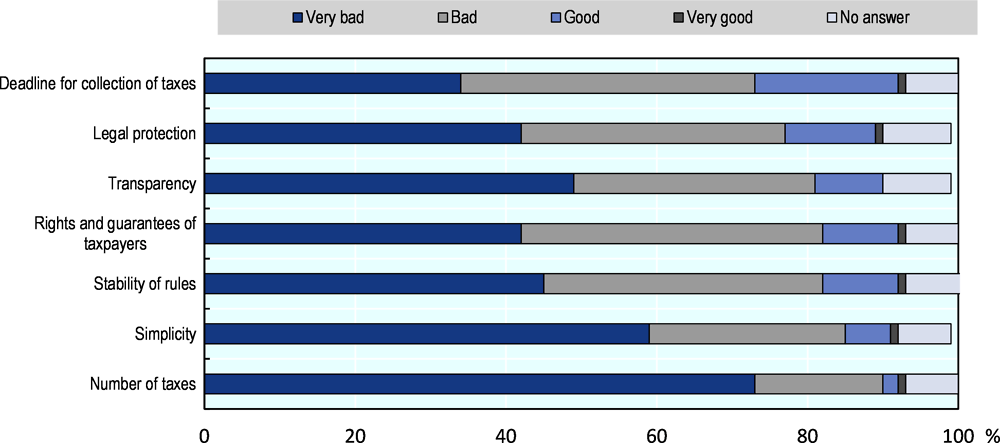

Brazil’s tax compliance costs are also high

A CNI survey highlights a general dissatisfaction of industrial firms with the national tax system. Respondents to the survey considered the sheer number of taxes the main problem, followed by compliance complexity and the predictability of tax rates and tax rules. Other areas for improvement included the rights and guarantees of taxpayers, the transparency of the tax system, and deadlines related to tax collection (Figure 3.12). Firms under the Simples Nacional regime (see below) expressed a less negative opinion about the tax system than those under the mainstream regime. Nonetheless, a majority of them were also dissatisfied, especially with respect to the number of taxes and tax complexity (CNI, 2015).

Note: The sum of the percentages may differ from 100% due to the rounding of percentages.

Source: CNI (2015), “Indústria reprova sistema tributário brasileiro”, Sondagem especial 63. http://arquivos.portaldaindustria.com.br/app/cni_estatistica_2/2015/08/28/189/SondEspecial_Tributacao_Agosto2015.pdf.

Payroll taxes, for example, are characterised by a host of levies such as FGTS (Fundo de Garantia do Tempo de Serviço), a compulsory savings instrument for Brazilian employees, and contributions to Sistema S, among others (Table 3.1) (Appy, 2015).

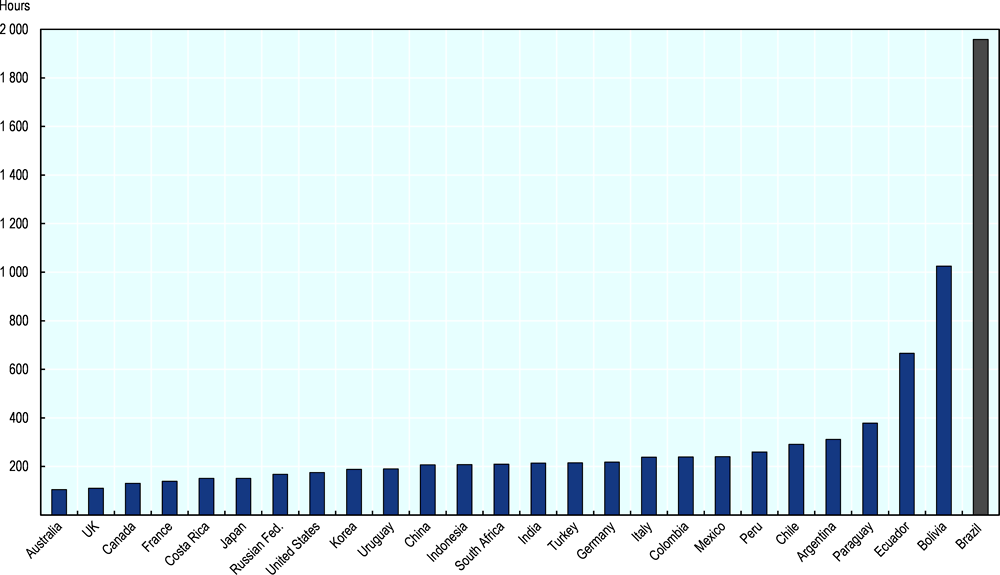

International statistics also confirm that Brazil’s tax system is particularly complex from a comparative perspective. Brazil ranks 184th out of 190 countries in the World Bank’s Doing Business ranking when it comes to paying taxes. It takes Brazilian firms almost 2 000 hours to prepare their taxes under the mainstream tax regime, considerably more than in other G20 and Latin American countries (Figure 3.13). A major complication is that tax authority is divided between the central government, the 26 states (plus the Federal District) and more than 5 000 municipalities (World Bank, 2017). This considerably adds to compliance costs, especially for enterprises active in several states (World Bank, 2018a).

Note: The number of hours is calculated on a benchmark manufacturing company.

Source: World Bank’s Doing Business Database.

The current indirect taxation would benefit from a comprehensive reform

The ICMS (Imposto Sobre Operações Relativas à Circulação de Mercadorias e Serviços de Transporte Interestadual e Intermunicipal e de Comunicação) is a tax on sales and services. It represents one of the main sources of revenues for Brazilian states (and the Federal District) and entails a major compliance cost for SMEs, which spend on average 1 116 hours a year to comply with the ICMS. This is more than for all other taxes combined and constitutes one of the main reasons why Brazil is an outlier when it comes to tax compliance costs (World Bank, 2018b).

ICMS is a complex tax that combines a tax on industrial production, a tax on sales, and a sort of customs tariff applied to interstate sales (Rezende, 2013). In addition, the tax base, the tax code and the tax rate vary, sometimes significantly, from state to state and from activity to activity.

In its current form, the ICMS has several market-distorting features:

-

Different levels of taxation apply at different stages of the production process, which may result in a misallocation of resources. As products and services resulting from a long production chain are taxes several times, the ICMS falls more heavily on complex manufacturing goods, thus favouring activities that typically take place in short chains such as the extraction of raw materials, the production of (basic) agricultural products or simple services activities such as those in retail trade.

-

Because of its “cascading nature”, the ICMS provides an incentive for firms to integrate in a vertical way, i.e. combining several stages of production normally operated by different firms, even in the absence of efficiency reasons to do so.

-

The ICMS also encourages tax competition across states. By offering reduced rates, higher tax credits or changes in tax collection and timing of refunds, states can attract more mobile economic activities, while concentrating taxation on more immobile activities.

-

Finally, the ICMS reduces the incentive for firms to establish branches or set up activities in different Brazilian states with different tax regimes. E-commerce activities, for example, face very considerable compliance costs under the ICMS regime.

These distortions are not present in traditional VAT systems in which products and services are charged irrespective of the length and geographical location of the value chain, but rather on the final price of the end product (Appy, 2015).

Apart from ICMS, Brazil has four other notable indirect taxes (three federal and one local which vary across cities):

-

IPI (Imposto sobre Produtos Industrializados), a federal VAT on industrial products.

-

ISS (Imposto sobre Serviços), a municipal services tax.

-

COFINS (Contribuição para o Financiamento da Seguridade Social), a federal VAT financing the social security system.

-

PIS (Programa de Integração Social), a federal VAT intended to finance the payment of unemployment insurance and allowances for low-income workers (e.g. Abono Salarial).

The combination of various indirect taxes raises compliance costs, which are proportionally higher for smaller businesses. The abovementioned CNI survey highlighted the harmonisation of ICMS and other indirect taxes as a key reform priority (CNI, 2015). In this regard, the federal government could take steps to streamline the different indirect forms of business taxation, reducing whenever possible variations across states. In particular, the distortionary impact of ICMS should be avoided by levying a tax on the end value added of products and services so as to eliminate its current cumulative nature.

The experience of India in simplifying its indirect taxation regime is of relevance to Brazil and could provide a possible model to follow (Box 3.1).

Description of the approach

The government of India introduced a major reform of its indirect tax system in July 2017 through the launch of the Goods and Services Tax (GST). The GST replaced a patchwork of indirect taxes at the federal and state levels, such as the excise duty and central sales tax on interstate sales transactions. The reform aimed to: reduce the cumulative taxation at various stages of the production process (tax cascading); harmonise indirect taxation across India; facilitate the creation of a common internal market; foster tax compliance and lower tax compliance costs.

The reform was conceived to be budget-neutral, although it was also expected to affect resource allocation between the central government and state governments and among different states. As a response to this, the federal government committed to compensating potential revenue losses incurred by states for five years since the implementation of the reform.

Administrative control was shared between the central government and the states. States assessed 90% of the businesses with an annual turnover of INR 15 million or less for scrutiny and audit, while the central government assessed the remaining 10%.

Factors for success

The reform has been successful: tax compliance costs have decreased and costs for firms operating in different Indian states have dropped significantly, based on estimates by PricewaterhouseCoopers, a consultancy. One of the major success factors has been that the government has proved receptive of feedback from the business community, including during the transition period.

Obstacles and responses

The reform required investments in IT infrastructure and (re)training of tax officers across the country. In addition, the government had to organise workshops and training sessions to inform the business community about the upcoming changes.

Despite marking a clear improvement compared to the previous situation, the current GST tax is still relatively complex with around 100 goods and services fully exempt, different rates (6%, 12%, 18%, 26% and 28%), threshold limits for small businesses, and special provisions for certain poorer states.

Finally, revenues from GST have fallen short of expectations, with the central government having to compensate state governments for this shortfall. Nonetheless, revenues are expected to increase in the future, as businesses will become more acquainted with the new regime and the collection process will become increasingly digitalised.

Relevance for Brazil

The experience from India illustrates the benefits of simplifying the indirect tax regime. Importantly, the decision to compensate state governments for potential revenue shortfalls generated political buy-in at the local level, something which would also be relevant in the context of Brazil.

For further information

OECD (2017), OECD Economic Surveys: India 2017, OECD Publishing, Paris, https://dx.doi.org/10.1787/eco_surveys-ind-2017-en; PricewaterhouseCoopers (2018), 365 Days of GST: A Historic Journey, .https://www.pwc.in/assets/pdfs/india-services/indirect-tax/365-days-of-the-gst-a-historic-journey/a-historic-journey.pdf (accessed on 9 February 2020).

Preferential tax and regulatory regimes for SMEs: Simples Nacional and MEI

Simples Nacional is the main federal SME policy8

Brazil operates two main preferential regimes for micro and small enterprises: Simples Nacional and the Micro Empreendedor Individual (MEI). The first had originally been introduced in 1996 with the name of Simples Federal, as originally it applied only at the federal.9 Subsequently, Lei Complementar 123/2006 extended this regime to all states and municipalities of the Federation, so the regime was rebranded Simples Nacional. The aim of Simples Nacional is to streamline the tax system and reduce the tax rate for micro and small firms as defined by the law – i.e. companies with annual gross revenues up to BRL 4.8 million. Under Simples Nacional firms pay eight taxes (six federal, one state-level and one municipal) through a single document and at a single rate that depends on annual revenues and type of economic activity. In addition, a few other fiscal obligations are reduced (ILO, 2014).

The scheme substantially reduces tax compliance costs for companies and thereby the need for small businesses to hire attorneys and accountants (Dutz, 2017). According to some estimates, companies opting for Simples Nacional have a tax burden of between 17%-20% of net profits, compared with between 28-39.5% for companies outside of this regime (Conceição et al., 2018).

Simples Nacional is fiscally expensive but its reform would require an overall reform of the corporate tax system

About 65% of Brazilian (formal) firms operate within Simples Nacional, making it the main federal policy for SMEs. In 2015, based on estimates from the Special Secretariat for Federal Revenues, Simples Nacional accounted for 25.6% of total fiscal spending, i.e. BRL 69.2 billion, more than any other tax spending item (RFB, 2018).10

Given Brazil’s complex tax and regulatory system, Simples Nacional plays an important role for the survival of micro and small enterprises. A survey by SEBRAE (Serviço Brasileiro de Apoio às Micro e Pequenas Empresas) highlights that, should Simples Nacional be abolished, 29% of companies under this regime would close, 20% would go informal and 18% would reduce their activity.11 Furthermore, preferential treatment for micro and small enterprises is enshrined in the federal Constitution, making it a constitutional right (see Chapter 4). Nonetheless, compared to other SME preferential tax regimes, Brazil’s Simples Nacional stands out because of its very high revenue threshold (Conceição et al., 2018): in other countries, the threshold is typically between USD 40 000 and USD 150 000, whereas in Brazil it stands at around USD 1.15 million (Table 3.2).12 Similarly to other firm-size legislations, Simples Nacional has also been reported to cause threshold effects by deterring business growth beyond the annual revenue threshold.13

Going forward, the Brazilian government could consider a three-pronged reform in which Simples Nacional is reformed together with the mainstream corporate tax system. First, the revenue threshold of Simples Nacional could be lowered to approach more closely the experience of other countries, such as Colombia or Mexico. This would have the merit of reducing the budgetary impact of the policy. Second, the mainstream corporate tax system should be simplified, possibly adopting some of the provisions of Simples Nacional and extending them to the whole enterprise population. This would reduce tax compliance costs and would eliminate disincentives to grow. Third, Brazil could gradually decrease its statutory corporate income tax rate from 34% to a level between 20% and 25%, in line with the average of OECD member states.

The Micro Empreendedor Individual (MEI) regime has encouraged the formalisation of micro-enterprises

Brazil introduced a second preferential tax regime for micro and small businesses in 2009, the Micro Empreendedor Individual (MEI), more closely targeted at the formalisation of self-employed people. The main advantages offered to those who opt for this regime are very low administrative costs related to business registration and tax payment, as well as pension coverage.

In terms of eligibility conditions, MEI entrepreneurs cannot exceed BRL 81 000 in annual gross revenues, cannot employ more than one person, cannot be a partner, administrator or owner of another business, and must operate in a sector covered by the regime (over 400 activities mostly in the area of personal services).

MEI features the following preferential conditions: i) social security contributions are set at 5% of the minimum salary; ii) a fixed monthly payment is paid to cover a state and municipal tax, i.e. ICMS and ISS; iii) if the business has an employee, the micro-entrepreneur pays 3% of his/her remuneration to the social security system, while 8% is deducted from the salary to converge into the Guarantee Fund of Work Time (Fundo de Garantia do Tempo de Serviço, FGTS); iv) businesses are exempt from income taxation and other federal taxes; v) taxes are paid electronically once a year. The whole MEI registration process is also conducted through an easy-to-use online portal.

An evaluation of MEI in the North-western state of Rondônia shows that 86% of its users were satisfied with the scheme and that this policy helped many micro-entrepreneurs to regularise their position. The scheme was also considered successful in tackling poverty: 39% of MEI entrepreneurs in Rondônia had not completed high school, suggesting that the scheme is reaching low-skilled people who often start a business out of necessity.14

SEBRAE has also considered MEI successful in alleviating poverty and encouraging formalisation, with nearly 9 million companies that have opted for this regime between 2009 and 2019. One of the main benefits is that formal registration has enabled micro-enterprises to access external finance, notably through the credit products of public development banks. Moreover, between 50 000 and 70 000 companies graduate every year from MEI into Simples Nacional (SEBRAE, 2016). MEI is also a relatively inexpensive policy, accounting for 0.52% of total federal tax spending in 2015 (BRL 1.4 billion) (RFB, 2018).

However, there are also some abuses associated with MEI through the so-called practice of pejotização, which occurs when employers contract workers who should legally be hired as employees as self-employed workers. In doing so, employers avoid paying social contributions (pension, health insurance, etc.) and other social obligations (e.g. the thirteenth annual salary). To provide some evidence to this thesis, IBGE data show that only 38.9% of the Brazilian workforce consists of employees, which sets Brazil as an outlier in the international context.15 Furthermore, a recent analysis by IPEA (Applied Economics Research Institute) shows that most people registered as individual micro-entrepreneurs are between the top 30% and 50% richest of the population, which is not fully consistent with the original objective of MEI to focus on low-income people on the edge of the formal sector (Costanzi, 2018).

Going forward, the practice of pejotização should be monitored and tackled to ensure that MEI does not lead to a simultaneous erosion of labour rights and tax revenues. However, in this process, the merits of MEI should not be overlooked, notably the fact that it has helped business formalisation and boosted the survival of micro-enterprises (see Chapter 2).

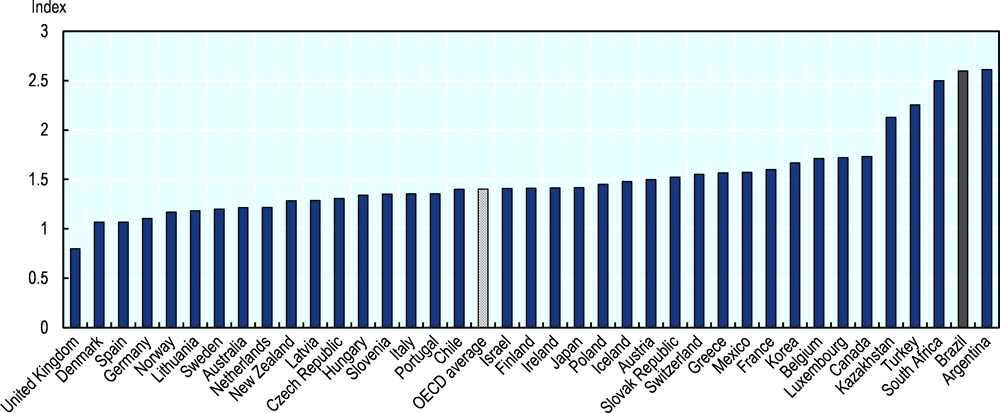

copy the linklink copied!Product market regulations

Product market regulations are restrictive, but there have been improvements

The 2018 edition of the OECD Product Market Regulation (PMR) database covers six main dimensions of the business environment: public ownership, government involvement in business operations, simplification and evaluation of regulations, administrative burden on start-ups, barriers in service and network sectors, and barriers to trade and investment. In the overall index, which summarises these six dimensions for a group of 38 countries (mostly OECD member states), Brazil ranks better than Argentina but worse than all other countries (Figure 3.14).

The six dimensions of the OECD PMR index are further subdivided into 18 lower-level indicators. Brazil scores quite negatively in the areas of public procurement (with a score of 3.75 compared with the OECD average of 1.34), impact assessment of regulation on competition (with a score of 4.50 compared with the OECD average of 1.09) and tariff barriers (with a score of 4.00 compared with the OECD average of 0.16).16 Brazil’s score is better or on par with the OECD average when it comes to price controls, command and control regulation, and government involvement in network structures (such as electricity generation, e-communication and transport).17

Note: The OECD PMR indicators were completely revamped in the last edition of 2018. As a result, the last edition is not comparable to previous vintages (2013, 2008 and 2003).

Source: OECD 2018 PMR database.

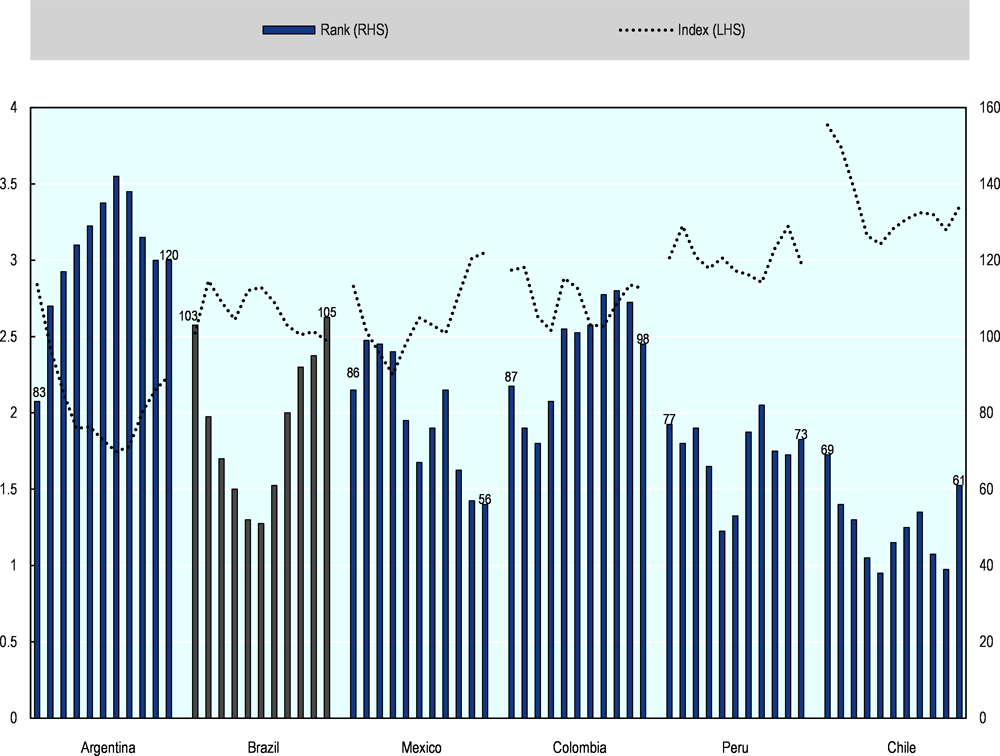

The World Bank Doing Business survey also measures the ease of doing business worldwide, covering some of the areas that are also in the OECD PMR database. In 2019, Brazil ranked 109th out of the 190 countries participating in this annual exercise (Table 3.3), an improvement by 16 positions from the previous year.

This improvement is the result of a number of important reforms in different policy areas. With respect to laws and regulations, for example, the government has introduced a regulatory guillotine to revoke obsolete laws that have no longer legal effect. More recently, through Provisional Measure 188/2019, the new government has also introduced a mandatory regulatory impact analysis (RIA) for federal regulations and acts that are expected to have an impact on businesses. A similar rule was set out in Law N. 13 848/2019 concerning the decision-making process of regulatory agencies. Such obligation is subject to future specific regulations, which shall provide for the content and methodology of the RIA, the minimum requirements to be examined, and the cases when the assessment is mandatory or can be waived.

Going forward, Brazil could focus on the following issues to further improve the regulatory environment. First, it could establish an independent body responsible for RIA to spread its use among government ministries and agencies. Mexico, for instance, established the National Commission for Regulatory Improvement (CONAMER) in 2000 to undertake a regular cost-benefit analysis of new laws and regulations. Similarly, there is no systematic use in Brazil of ex post evaluation to assess whether regulations have achieved their objectives or have had unintended consequences. In this respect, Colombia carries out reviews of the existing regulatory framework every three years through the Comisiones Reguladoras and could be taken as an example to follow (Querbach and Arndt, 2017).

Second, the federal government should continue its efforts to streamline regulations across states and municipalities. In this area, the national regulation harmonisation policy REDESIM (see Chapter 4 for more details) already helps harmonise state and municipal-level regulations affecting opening a business and safety and environmental standards at work. In the framework of REDESIM, the federal government could encourage the diffusion of regulatory good practices from leading to lagging states. By way of example, if Minas Gerais were a country, it would rank 30th in the World Bank Doing Business, compared with 149th in the case of São Paulo (World Bank, 2018b).

copy the linklink copied!Access to finance

Credit market conditions

Average credit market conditions are tight in Brazil

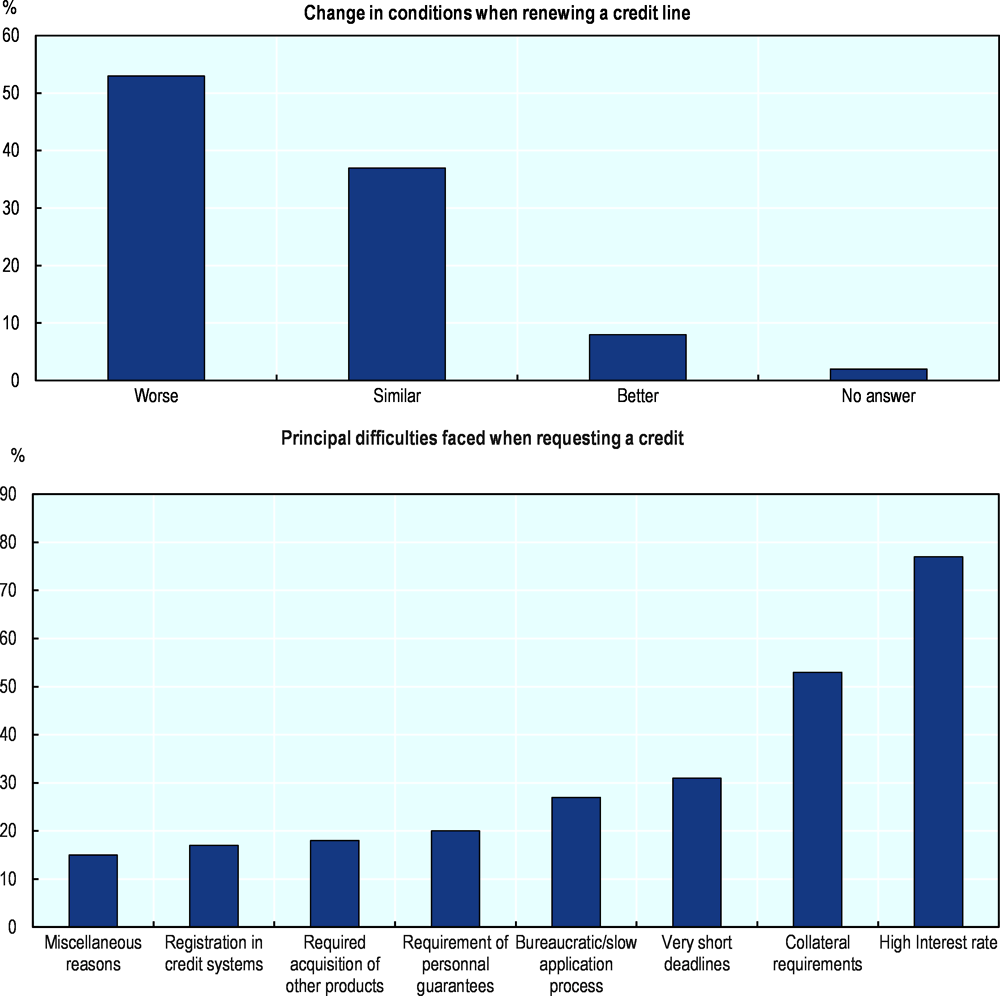

The 2015-16 Brazilian recession has had a deep impact on the credit market for SMEs: according to a 2016 survey by CNI, 53% of the interviewed companies faced worsened credit conditions after the recession, 35% were refused new credit lines, while 40% received only a fraction of the loan they had initially requested (CNI, 2016). High interest rates were considered the most pressing problem, followed by collateral requirements and short deadlines (Figure 3.15).

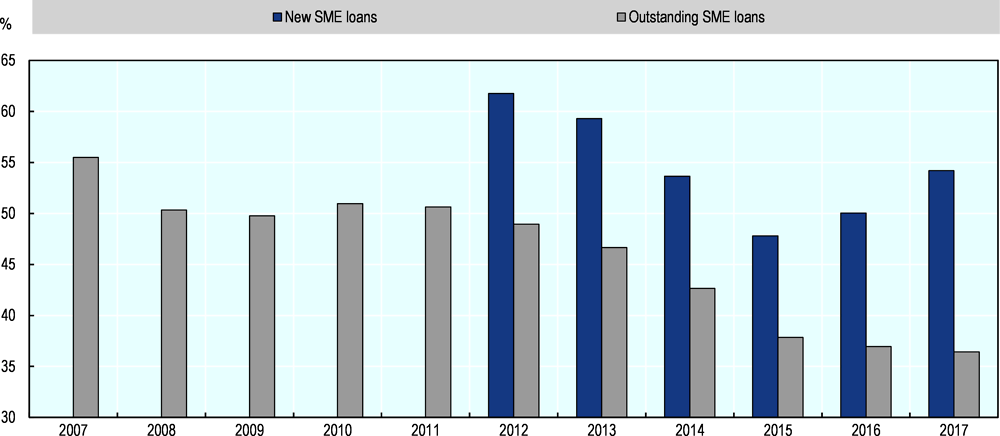

Between 2015 and 2017, the outstanding stock of SME loans declined by around one-third in Brazil (Figure 3.16). Thereafter, credit conditions have partly eased for large enterprises but not for SMEs (Banco Central do Brasil, 2018a), as shown by the fact that the spread between the loan interest rate applied to large companies and SMEs has not come back to the pre-recession levels (12% in 2014 vs. 16% in 2017).

While credit conditions have worsened after the recession, a tight credit market is rather a structural problem for Brazilian SMEs. Between 2007 and 2017, the share of SME loans in total business loans declined from 55% to 36% (Figure 3.17). In 2017, the average interest rate charged to SMEs was 25%, while the interest-rate spread between SMEs and large companies was 16%, both of which are high by international standards. These figures are influenced by a number of factors, such as the Central Bank’s policy interest rate (on average 10% in 2017), high credit default rates, a high share of earmarked credit, information asymmetries in the credit market, and high taxation of financial institutions.

Source: CNI (2016), “Piora das condições de financiamento na indústria”, Sondagem especial 67. https://bucket-gw-cni-static-cms-si.s3.amazonaws.com/media/filer_public/38/93/3893a1f9-6369-4185-8505-f6e17daeb3bf/sondespecial_financiamentoparacapitaldegiro_junho2016.pdf.

Note: All data are corrected for inflation. The definition of an SME varies from one country to another.

Source: OECD (2019), Financing SMEs and Entrepreneurs 2019: An OECD Scoreboard, OECD Publishing, Paris, https://doi.org/10.1787/fin_sme_ent-2019-en.

Source: Source: OECD (2019), Financing SMEs and Entrepreneurs 2019: An OECD Scoreboard, OECD Publishing, Paris, , https://doi.org/10.1787/fin_sme_ent-2019-en.

Survey data from SEBRAE confirm the low uptake of credit among Brazilian SMEs, notably among micro and small enterprises (MPEs) complying with Lei Complementar 123/2006. This survey points to a strong decline in the proportion of MPEs using bank finance over the period 2013-17, whereas informal sources of finance, such as loans from relatives and friends or from loan sharks remained constant or even increased during the same period. Overdrafts and business credit cards are the two most common sources of bank finance in Brazil, although they are generally expensive instruments (Table 3.4).

Increased transparency would ease credit market conditions

Lack of information on credit worthiness drives up interest rates. In this respect, a new federal law approved in April 2019 allows credit bureaus and the credit registry to collect positive credit information on individuals and legal entities without getting their explicit prior approval. As a consequence, the number of people and legal entities with available credit information is expected to increase from 6 million, when only negative information could be gathered, to 110 million (Banco Central do Brasil, 2019). This reform should make the credit market more transparent, for example by allowing people and firms with good credit histories to obtain loans at better conditions.

On the other hand, Brazil could improve its collateral registry for secured transactions. In particular, its registry framework for movable collaterals is fragmented, paper-based and expensive. Improving this registry would enable SMEs to collateralise assets such as equipment or inventory more easily, thus favouring access to finance (World Bank, 2018c). In this respect, a recent law (i.e. Law 13 775/2018) has regulated the electronic registry of commercial invoices (duplicata eletrônica), which is a step in the right direction.

Brazil has a high proportion of earmarked lending, but its relevance in the business credit market has declined

Brazil is also characterised by a high share of earmarked lending, i.e. lending which is allocated by law to specific sectors or purposes. The three main forms of earmarked lending in Brazil are rural credit, housing credit (mortgages) and BNDES credit. Historically, the share of earmarked credit in total credit increased between 2008 (32.5%) and 2016 (49.9%), only to slightly decrease to 45.9% in 2018. Much of the growth in earmarked lending, however, is the result of a rise in mortgage lending – from 17.2% of the total in 2008 to 42.7% in 2018 – whereas the share of earmarked lending allocated to firms dropped from 50.9% in 2009, at the peak of the global financial crisis, to 29.7% in 2018. Accordingly, the share of BNDES in total earmarked lending also progressively declined from above 50% of the total in the period 2008-11 to 33% in 2018 (BNDES, 2019).

A common criticism levelled at earmarked lending is that, by favouring lower interest rates in targeted sectors, it leads to higher interest rates in other sectors. A simulation of the Central Bank shows that re-addressing 10% of earmarked lending to other operations would reduce interest rates by 1.3% and increase credit volumes by 5.6% in the non-earmarked market (Banco Central do Brasil, 2018a).

BNDES is the main source of earmarked credit for SMEs. Since 2018, BNDES credit has been pegged to the Central Bank’s new long-term interest rate (i.e. Taxa de Longo Prazo, TLP), whose implicit subsidy component is being phased out (see Chapter 5). Because of its intermediary role, BNDES has also helped reduce banking concentration by enabling small financial institutions to apply for and use its SME credit lines. This is shown, for example, by the fact that the five largest national banks hold 70% of total credit, but only 40% of credit originating from BNDES.

Strengthening creditor’s rights in insolvency procedures would spur secured lending

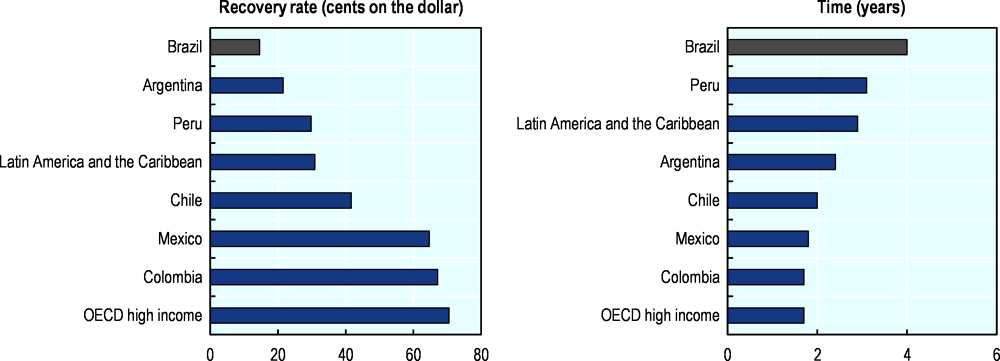

High interest rates are also linked to legal insecurity in the collection and recovery of pledged collaterals. Comparative data illustrates that the average recovery rate upon insolvency (i.e. the cents on the dollar that can be recovered by creditors upon insolvency) amounted to 14.6 in 2017 in Brazil, compared with the LAC (Latin America and the Caribbean) average of 30.9 and the average of high-income countries of 70.5. Moreover, the average insolvency procedure takes 4 years in Brazil, compared with 2.9 years in the LAC region and 1.7 years in high-income countries (Figure 3.18).

One of the key problems in insolvency procedures is that deadlines are poorly enforced. In addition, creditors have no right to put forward a re-organisation plan, and there is limited scope for intervention if the creditor’s concerns are not addressed (Cooper et al., 2017). This situation discourages banks from small business lending even in the presence of collateral assets.

Plans to reform bankruptcy procedures are under discussion. Priority should go to addressing the creditor-debtor imbalance of power, ensuring stricter enforcement of deadlines, and facilitating the development of consensual re-organisation plans. Procedures for extrajudicial recovery and out-of-court settlements, currently not very common, could also be encouraged.

Note: OECD high-income countries include all OECD countries, except Colombia, Mexico and Turkey.

Source: World Bank’s Doing Business Database.

Important reforms have been taken to strengthen competition in the credit market

Banking concentration – i.e. the share of total assets in the banking system held by the top five banks – has been on the rise in Brazil, from 57% in 2000 to 82% in 2016. While this is similar to countries with smaller populations such as France, Canada or Australia (all with a rate between 80% and 82%), it is higher than in countries with larger populations such as Mexico (70%), Japan (51%) or the United States (43%) (BIS, 2018).

The Central Bank has recently put in place a number of measures to increase competition in the Brazilian credit market. Since 2018, it has adapted financial sector regulations to the size of the financial institution and, accordingly, to its risk posed to the national financial system. This has reduced licensing requirements and entry costs for smaller financial institutions, notably peer-to-peer lending companies and direct lending platforms. A 2019 Presidential Decree has also made it easier for these fintech companies to receive foreign capital.

Competition in the credit market has also been strengthened by new regulations that allow credit co-operatives to expand their activity, which has already been on the rise in the last years (Banco Central do Brasil, 2018b). Resolution 4716/2019 allows credit co-operatives to receive savings deposits, while Resolution 4749/2019 allows credit co-operatives to issue banking notes. Both are expected to help credit co-operatives to diversify funding sources and operations and, thereby, place them in a better position to compete with traditional financial institutions. BNDES has also played an important role in the diffusion of credit co-operatives, notably by supporting their participation in its credit lines (Risson and Bulcão Flach, 2013).

Going forward, it will be important to continue supporting credit co-operatives, including by strengthening their professional risk management. There is evidence, for example, that the size of a credit co-operative and the quality of its management have a significant impact on its life expectancy (Carvalho et al., 2015). BNDES could play a role in this agenda, for example by offering training and capacity-building to credit co-operatives in line with the principle of public development banks offering not only finance but also technical assistance (see Chapter 5).

Box 3.2 summarises some of the main new measures that Brazil has adopted to reduce the cost of capital and to stimulate efficiency in financial intermediation and private investment, including reforms to foster competition in the credit market. As part of these reforms, the establishment of foreign bank branches and the provision of cross-border banking services could also be encouraged in the future, as it is currently subject to prior approval by Brazilian authorities, based on international agreements, reciprocity or national interest.18 In its efforts to reform the financial sector, Brazil could also draw inspiration from Mexico, which has recently introduced a wide-ranging financial sector reform (Box 3.3).

-

Electronic issuance and electronic registration of trade notes (Law 13476/2017).

-

Electronic registration and collateralisation of payment scheme receivables (Resolution 4734/2019 and Circular 3952/2019).

-

Centralisation of all registration and deposit of financial assets and securities, as well as custody services (Resolution 4593/2017).

-

Expansion of credit reporting and scoring to improve credit risk assessment (Supplementary Law 166/2019 – still to be regulated).

-

Extension of credit information system data availability, from 1 to 2 years (Communiqué 32053/2018).

-

E-money issuers authorised to pass the interest earned from sterilised funds at the Central Bank on to clients (Circular 3944/2019).

-

Capped interchange fee on debit payment scheme transactions (Circular 3887/2018).

-

Permission for credit co-operatives to receive savings deposits (Resolution 4716/2019) and to issue banking notes (Resolution 4749/2019).

-

Publicly available information on the rates charged by financial institutions on the website of the Central Bank.

-

Companies allowed to open and close demand deposit accounts online (Resolution 4697/2018).

-

Improved positive credit reporting, which allows the sharing of reliable and updated data (Complementary Law 166/2019).

-

Introduced treatment in bank prudential regulation proportional to the size and risk profile of the institution (Resolution 4553/2017).

In January 2014, the government of Mexico introduced a broad financial sector reform, hinged on three main pillars: more effective property rights protection for creditors; stronger legal authority to manage the resolution of banks; and promotion of competition among financial intermediaries. Under the third pillar, the Federal Competition Commission monitors the level of competition in the banking sector, including by sanctioning anti-competitive practices in the determination of commercial interest rates. For example, the sales of financial products conditional on the acquisition of others (i.e. bundled sales) are forbidden under the new regulation. Similarly, the transfer of bank accounts and bank loans from one institution to another has become less costly and time-consuming after the reform. Finally, the reform has reduced commission fees for financial institutions when they use each other’s infrastructures.

Sources: OECD (2015), OECD Economic Surveys: Mexico 2015, OECD Publishing, Paris, https://doi.org/10.1787/eco_surveys-mex-2015-en; BIS (2014), “BIS central bankers’ speeches Manuel Sánchez: Mexico’s banking system-opportunities from reform”, https://www.bis.org/review/r140305b.pdf; Itaú BBA (2015), Mexico’s Financial Reform: A Step in the Right Direction, https://www.itau.com.br/itaubba-en/economic-analysis/publications/macro-vision/mexicos-financial-reform-a-step-in-the-right-direction.

Financial inclusion is also being strengthened

The newly elected government has also undertaken new policies to strengthen financial inclusion. In April 2019, for example, it introduced the so-called Simple Credit Enterprise (Empresa Simples de Crédito, ESC). Through this new legal entity, individuals will be able to lend money legally to small businesses. ESCs will not have minimum capital requirements, but they will not be able to charge loan fees. Annual gross revenues in ESC should not exceed the BRL 4.8 million threshold. The government expects that the ESC reform will result into an injection of more than BRL 20 billion per year into additional small business lending.

In July 2019, the Central Bank also launched the BC# initiative to make strides on the democratisation of the national financial system. The BC# Agenda will guide the work of the Central Bank over the next few years and is based on four dimensions: i) inclusion; ii) competitiveness; iii) transparency; and iv) financial education. The first two pillars are the most relevant from the point of view of SMEs. The first refers to the national financial system reaching out more people, notably through microcredit, which is considered pivotal to strengthening access to credit and generating employment. Within the second pillar, the Central Bank is undertaking research on the potential of instant payment, open banking and block-chain technologies to increase competitiveness in the credit market.

Alternative sources of finance

Brazil has a well-developed venture capital (VC) industry

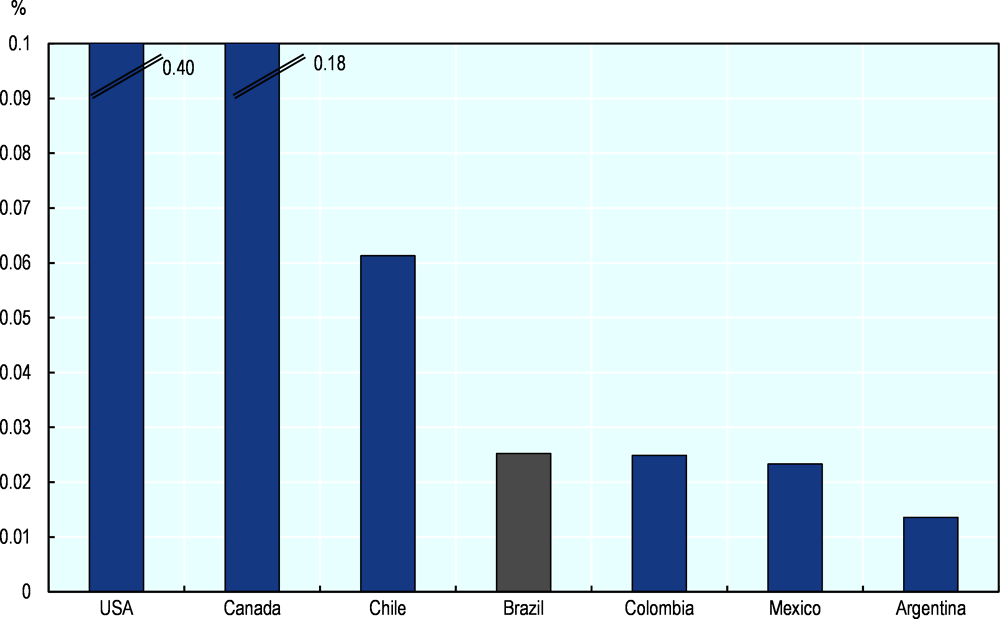

Brazil has the largest VC market in Latin America, with around 75% of all investments in the region in 2017. VC investments amounted to 0.06% of national GDP, a higher share than in other Latin American countries (Figure 3.19). Fintech and agri-tech were the sectors that attracted the most investments in 2017.

Note: Underlying data is expressed in current USD, current exchange rates.

Sources: OECD for Canada and the United States, the Latin American Private Equity & Venture Capital Association (LAVCA) for other countries.

The International Monetary Fund (IMF) Financial Development Index corroborates Brazil’s front-runner status in equity finance in Latin America. It shows that Brazil has more developed financial markets and financial institutions than other Latin American countries, with a performance that is just below the average of high-income economies (Figure 3.20). The Latin America Venture Capital Association (LAVCA) ranks countries based on 13 indicators assessing the business environment for VC investments. In 2017-18, Brazil ranked second, behind Chile, with its main strength being the laws on PE/VC fund formation and operation and the state of development of capital markets.

Although Brazil’s VC market is large and growing by regional standards, there is still unmet demand. Brazilian executives answering to a World Economic Forum (WEF) survey reported a decline in VC availability over the period 2007-17, suggesting that the supply of venture capital has not kept up with growing demand (Figure 3.21) (WEF, 2018).

Note: The Financial Development Index is a composite indicator of a Financial Institutions Index and a Financial Market Index. Financial institutions include banks, insurance companies, mutual funds and pension funds. Financial markets include stock and bond markets. Financial development is defined as a combination of depth (size and liquidity of markets), access (ability of individuals and companies to access financial services), and efficiency (ability of institutions to provide financial services at low cost and with sustainable revenues). This broad multi-dimensional approach to defining financial development follows the matrix of financial system characteristics developed by Čihák et al. (2012).

Source: Financial Development Index Database, International Monetary Fund.

Brazilian legislation is broadly supportive of equity finance and fintech

Brazil’s legislation is broadly supportive of equity finance. A 2016 reform initiated by the Brazilian Securities Commission (Comissão de Valores Mobiliários, CVM) has been a major policy development in this field. The new regulation has increased the number of assets available for equity investment (e.g. corporate debt bonds), divided funds in different categories (i.e. seed capital, emerging companies and multi-strategy) and reduced restrictions to invest abroad (e.g. totally lifted for multi-strategy funds). In addition, the reform has increased transparency in accounting practices through the adoption of the International Accounting Standards Board’s guidelines and has introduced the concept of “angel investor” in national legislation.

In the area of fintech, the Central Bank launched in 2018 a Laboratory of Financial and Technological Innovations. It gathers academics, entrepreneurs and banks with the goal of boosting financial inclusion through fintech platforms. Selected start-ups are asked to present projects in line with the Central Bank’s strategy to reduce the cost of credit and are supported by large technology companies such as Amazon Web Services or Microsoft.

In addition to a supportive legal framework, the Brazilian government invests in a number of VC funds dedicated to established SMEs and start-up, especially through BNDES and FINEP (the national innovation agency). These initiatives are more closely analysed in Chapters 5 and 7 of the report.

Note: Survey of executives answering the question: “in your country, how easy is it for start-up entrepreneurs with innovative but risky projects to obtain equity funding?” [1 = extremely difficult; 7 = extremely easy], each value is a 2-year weighted average. For instance, the last index value for 2017 is a 2016-17 weighted average value.

Source: WEF (2018), The Global Competitiveness Report 2018, http://www3.weforum.org/docs/GCR2018/05FullReport/TheGlobalCompetitivenessReport2018.pdf.

Online alternative finance is on the rise, but from a comparatively low base

Online alternative finance, including peer-to-peer lending and equity crowdfunding, represents another potential source of finance for Brazilian start-ups with a higher risk profile. Although volumes have been on the rise in recent years, activities remain subdued compared to neighbouring countries. Crowdfunding activities in Brazil reached 0.003% of GDP in 2017, behind Chile, Colombia and Mexico, the other Latin American countries for which comparable data are available (OECD, 2019).

The CVM has started regulating crowdfunding only very recently. CVM Instruction 588, enforced in July 2017, formally authorised equity crowdfunding for SMEs. Based on this instruction, companies with gross annual revenues below BRL 10 million can raise up to BRL 5 million each year. On the investor’s side, individuals can invest up to BRL 10 000 per year, in order to limit the risk of losses.19

copy the linklink copied!Conclusions and policy recommendations

This chapter has looked into the quality of the business environment for SMEs and entrepreneurship in Brazil. It has started by showing that, despite recent progress, the share of the population without primary education is higher in Brazil than in other Latin American countries. In addition, only 9% of Brazilian students in upper secondary education are enrolled in vocational education. PRONATEC, Brazil’s main vocational training policy until 2018, has failed to have a positive impact on the employment of participants, mostly because of the limited involvement of the private sector in deciding the content and scope of the training. Future VET policies, notably Emprega Mais, should build on the experience of PRONATEC, trying to design training courses more closely aligned with the skills needs of the private sector.

Trade flows, defined as the sum of exports and imports, amounted to 29% of GDP in 2018, much lower than the world average (56%). Empirical estimates suggest that the benefits of trade liberalisation would be large, including for SMEs that would have more opportunities to export and participate into global supply chains. Brazil’s trade policies are undertaken in the framework of the Mercosur trade bloc. Recent important reforms include a drop in the number of local content requirements, a reduction of national tariffs for capital and IT goods under the Mercosur agreement, and the free trade agreement signed between Mercosur and the EU in June 2019.

Brazil’s overall business regulatory burden has been eased over the last decade, which is also the result of the introduction of two main tax and regulatory regimes for micro and small businesses. MEI has been quite successful in helping the formalisation of own-account workers mostly working in the personal services sector. Simples Nacional is the main federal SME policy, covering more than 65% of the total enterprise population. There is scope for adjusting some aspects of Simples Nacional, for example lowering the revenue threshold which is high by international standards, but this should be done contextually with an overall simplification of Brazil’s standard corporate tax system.

The interaction between federal, state and municipal legislation is an additional element of complexity in the Brazilian regulatory environment. The current efforts to streamline and harmonise the regulatory framework across different levels of government, notably through the REDESIM initiative, should be strengthened. Ex ante regulatory impact analysis (RIA) and ex post policy evaluation should become more regular practices, building on a recent government measure that has made RIA compulsory for regulations and acts with an expected impact on businesses.

Credit market conditions are generally tight in Brazil, especially for SMEs. The Central Bank has introduced important reforms to reduce the cost of capital and increase competition in the credit market. Credit bureaus, for example, have been allowed to collect positive information on individuals and legal entities without the need for their prior approval. Competition has been encouraged in multiple ways, including by new regulations that govern the activities of fintech companies and that diversify funding sources for credit co-operatives.

Finally, VC investment in Brazil is high by international standards, although the supply of VC has not kept up with growing demand. Regulation is broadly supportive of equity investments and fintech. Online alternative finance, including peer-to-peer lending and equity crowdfunding, has been on the rise in recent years, but remain small compared to neighbouring countries.

-

Change the balance of spending in active labour market policies by reducing support for self-employment and increasing support for training and job search assistance programmes.

-

Improve support for vocational training through the new Emprega Mais programme, making sure that training courses benefit from inputs and feedbacks from the private sector.

-

Consider introducing a single national value-added tax following the example of India, while lobbying states to simplify and harmonise the state-level ICMS tax.

-

Consider an overall reform of corporate income taxation in which the standard system is significantly simplified (for example, adopting some of the Simples Nacional’s provisions), the statutory corporate income tax rate is reduced, and the income threshold of Simples Nacional is lowered.

-

Increase oversight of MEI to ensure that this policy is not used by employers to contract people who should be legally hired as employees as self-employed workers (i.e. the so-called practice of pejotização).

-

Expand the use of regulatory impact analysis (RIA) by establishing an independent body comparable to CONAMER in Mexico.

-

Encourage more competition in the credit market by simplifying entry procedures for foreign banks and by continuing to encourage the development of alternative domestic lenders (e.g. credit co-operatives and fintech organisations).

-

In line with the recent regulation of electronic trade notes and centralised registration of payment receivables, continue to improve, digitalise and centralise the registry for movable collateral assets with a view to strengthening secured business lending.

-

Reform insolvency procedures by streamlining the overall process (e.g. enforcing deadlines within the foreclosure procedure), encouraging out-of-court settlements and strengthening creditor rights (e.g. the right to have a say on re-organisation plans).

-

Continue to develop an appropriate regulatory framework for credit co-operatives.

References

Appy, B. (2015), Por que o Sistema Tributário Brasileiro Precisa ser Reformado, Centro de Cidadania Fiscal (CCiF), São Paulo, http://www.ccif.com.br/wp-content/uploads/2018/07/Appy_Tributa%C3%A7%C3%A3o_1610.pdf.

Araújo, S. and D. Flaig (2016), “Quantifying the Effects of Trade Liberalisation in Brazil: A Computable General Equilibrium Model (CGE) Simulation”, OECD Economics Department Working Papers, No. 1295, OECD Publishing, Paris. https://doi.org/10.1787/5jm0qwmff2kf-en.

Banco Central do Brasil (2019), Lei do Cadastro Positivo é sancionada, Brasília, https://www.bcb.gov.br/detalhenoticia/336/noticia.

Banco Central do Brasil (2018a), Relatório de Economia Bancária: 2017, Brasília, https://www.bcb.gov.br/content/publicacoes/relatorioeconomiabancaria/REB_2017.pdf.

Banco Central do Brasil (2018b), Panorama do Sistema Nacional de Crédito Cooperativo, Brasília, https://www.bcb.gov.br/estabilidadefinanceira/coopcredpanorama.

Barbosa Filho, F.H., R. Porto and D. Liberato (2015), Relatório Técnico – PRONATEC Bolsa Formação: Uma avaliação inicial sobre reinserção no mercado de trabalho formal, Ministério da Fazenda, Secretaria de Politica Econômica (SPE), Brasília, https://www.anpec.org.br/encontro/2015/submissao/files_I/i13-b96b730ed095ec6aec5c375de1e9d6dd.pdf.

BIS (2018), “Structural changes in banking after the crisis”, CGFS Papers N. 60, Bank for International Settlements, Basel, https://www.bis.org/publ/cgfs60.pdf.

BIS (2014), “BIS central bankers’ speeches Manuel Sánchez: Mexico’s banking system-opportunities from reform”, Bank for International Settlements, Basel, https://www.bis.org/review/r140305b.pdf.

BNDES (2019), “Uma breve análise do crédito direcionado”, unpublished document, Banco Nacional de Desenvolvimento Econômico e Social.

Carvalho, F., M. D. Montoya, S. Bialoskorski and A. Guimarães (2015), “Exit and failure of credit unions in Brazil: A risk analysis”, Revista Contabilidade & Finanças, Vol. 26/67, pp. 70-84, https://doi.org/10.1590/1808-057x201411390.

Cihak, M., A. Demirgüç-Kunt, E. Feyen and R. Levine (2012), Benchmarking Financial Systems Around the World, World Bank, Washington, DC, http://documents.worldbank.org/curated/en/868131468326381955/Benchmarking-financial-systems-around-the-world.

CNI (2017), “Indústria espera aumento do emprego com a Reforma Trabalhista”, Sondagem especial 70, https://bucket-gw-cni-static-cms-si.s3.amazonaws.com/media/filer_public/6f/88/6f88ae5e-2b15-4459-b9a5-3f84dc2ca030/sondespecial_reformatrabalhista_dezembro2017.pdf.

CNI (2016), “Piora das condições de financiamento na indústria”, Sondagem especial 67, https://bucket-gw-cni-static-cms-si.s3.amazonaws.com/media/filer_public/38/93/3893a1f9-6369-4185-8505-f6e17daeb3bf/sondespecial_financiamentoparacapitaldegiro_junho2016.pdf.

CNI (2015), “Indústria reprova sistema tributário brasileiro”, Sondagem especial 63, http://arquivos.portaldaindustria.com.br/app/cni_estatistica_2/2015/08/28/189/SondEspecial_Tributacao_Agosto2015.pdf.

Conceição, O., M. Saraiva, A. Fochezatto and M. França (2018), “Brazil’s Simplified Tax Regime and the longevity of Brazilian manufacturing companies: A survival analysis based on RAIS microdata”, EconomiA, Vol. 19/2, pp. 164-186, https://doi.org/10.1016/J.ECON.2017.10.003.

Costanzi R. (2018), Os Desequilíbrios Financeiros do Microempreendedor Individual (MEI), IPEA, http://www.ipea.gov.br/portal/images/stories/PDFs/conjuntura/180117_CC38_desequilibrio_financeiro_MEI.pdf

Cooper, R., F. Cestero and D. Soltman (2017), “Insolvency reform in Brazil: An opportunity too important to squander”, Emerging Markets Restructuring Journal, No. 4, https://www.clearygottlieb.com/~/media/organize-archive/cgsh/files/2017/publications/emrj-summer-2017-issue-4/insolvency-reform-in-brazil--an-opportunity-too-important-to-squander-updated-2.pdf.

Dutz, M. (2018), Jobs and Growth: Brazil’s Productivity Agenda, The World Bank, Washington, DC, https://doi.org/10.1596/978-1-4648-1320-7.

Dutz, M. (2017), Business Support Policies: Large Spending, Little Impact, World Bank, Washington, DC, http://documents.worldbank.org/curated/en/458011511799140856/pdf/121668-REVISED-Brazil-Public-Expenditure-Review-Business-Support-Policies.pdf.

ILO (2014), Notes on Policies for the Micro and Small Enterprises in Brazil, ILO Regional Office for Latin America and the Caribbean, https://www.ilo.org/wcmsp5/groups/public/---americas/---ro-lima/documents/publication/wcms_318209.pdf.

Itaú BBA (2015), Mexico’s Financial Reform: A Step in the Right Direction, https://www.itau.com.br/itaubba-en/economic-analysis/publications/macro-vision/mexicos-financial-reform-a-step-in-the-right-direction.

Latinobarómetro (2018), Informe Latinobarómetro 2018, Santiago de Chile, http://www.latinobarometro.org/latdocs/INFORME_2018_LATINOBAROMETRO.pdf.

Mesquita Moreira, M. (ed.), Too Far to Export: Domestic Transport Costs and Regional Export Disparities in Latin America and the Caribbean, Inter-American Development Bank, Washington, DC, https://publications.iadb.org/en/publication/17434/too-far-export-domestic-transport-costs-and-regional-export-disparities-latin.

O'Connell, S., L. Mation, J. Bevilaqua and M. Dutz (2017), “Can business input improve the effectiveness of worker training? Evidence from Brazil’s Pronatec-MDIC (English)”, Policy Research Working Paper, No. WPS 8155, World Bank Group, Washington, DC, http://documents.worldbank.org/curated/en/444871501522977352/Can-business-input-improve-the-effectiveness-of-worker-training-evidence-from-Brazils-Pronatec-MDIC.

OECD (2019), Financing SMEs and Entrepreneurs 2019: An OECD Scoreboard, OECD Publishing, Paris, https://doi.org/10.1787/fin_sme_ent-2019-en.

OECD (2018a), OECD Economic Outlook, Volume 2018 Issue 2, OECD Publishing, Paris, https://dx.doi.org/10.1787/eco_outlook-v2018-2-en.

OECD (2018b), Education at a Glance 2018: OECD Indicators, OECD Publishing, Paris, https://dx.doi.org/10.1787/eag-2018-en.

OECD (2018c), Getting Skills Right: Brazil, Getting Skills Right, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264309838-en.

OECD (2018d), OECD Economic Surveys: Brazil 2018, OECD Publishing, Paris, https://doi.org/10.1787/eco_surveys-bra-2018-en.

OECD (2018e), Trade in Value added: Brazil, OECD, Paris, http://www.oecd.org/industry/ind/TIVA-2018-Brazil.pdf.

OECD (2018f), “Building public trust through further reforms to safeguard responsiveness and integrity”, Brazil Policy Brief, OECD, Paris, https://www.oecd.org/policy-briefs/Brazil-Building-public-trust-en.pdf.

OECD (2018g), Digital Government Review of Brazil: Towards the Digital Transformation of the Public Sector, OECD Digital Government Studies, OECD Publishing, Paris, https://doi.org/10.1787/9789264307636-en.

OECD (2018h), Taxing Wages 2016-2017. Associated Paper: Selected Partner Economies (Brazil, China, India, Indonesia and South Africa), OECD, Paris, https://www.oecd.org/tax/tax-policy/taxing-wages-selected-partner-economies-biics-2018.pdf.

OECD (2017), OECD Economic Surveys: India 2017, OECD Publishing, Paris, https://dx.doi.org/10.1787/eco_surveys-ind-2017-en.

OECD (2016), PISA 2015 Results (Volume I): Excellence and Equity in Education, PISA, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264266490-en.

OECD (2015), OECD Economic Surveys: Mexico 2015, OECD Publishing, Paris, https://doi.org/10.1787/eco_surveys-mex-2015-en.

OECD/CIAT/IDB/ECLAC (2018), Revenue Statistics in Latin America and the Caribbean 2018, OECD Publishing, Paris, https://dx.doi.org/10.1787/rev_lat_car-2018-en-fr.

PricewaterhouseCoopers (2018), 365 Days of GST: A Historic Journey, .https://www.pwc.in/assets/pdfs/india-services/indirect-tax/365-days-of-the-gst-a-historic-journey/a-historic-journey.pdf (accessed on 9 February 2020).