copy the linklink copied!Chile

Economic growth will remain robust, at above 3%, in 2019-20. Supportive financing conditions, high copper prices, the planned tax and labour reforms and positive business sentiment will underpin investment. Low real interest rates and strong wage growth will support private consumption. Stronger growth will start to translate into higher employment growth. However, inequality is still high, driven by persistent low intergenerational mobility.

Monetary policy needs to remain accommodative and only start tightening in 2020 as slack dissipates further. The structural fiscal deficit will narrow moderately, according to the medium-term fiscal path set by the authorities, putting the debt-to-GDP ratio on a downward path. The approval and implementation of planned key structural reforms in the areas of taxes, pensions and labour and business regulations would lead to a more favourable growth outlook and more inclusiveness.

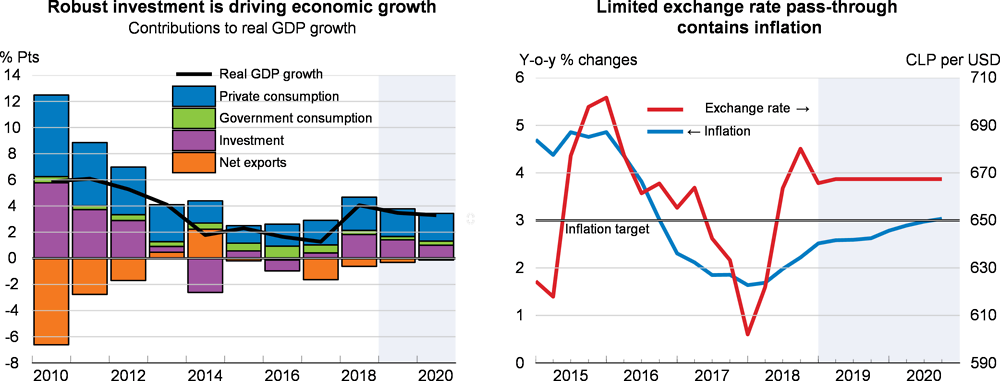

Growth has been boosted by investment

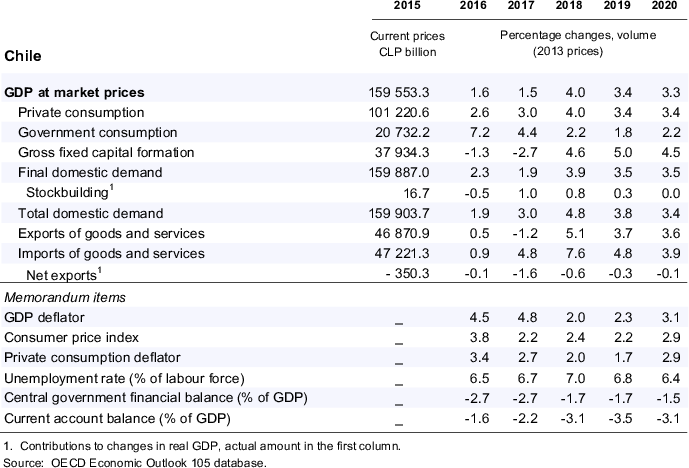

In 2018, the economy grew at its highest rate since 2013, led by investment and buoyant non-mining sectors. Household consumption accelerated amid subdued inflationary pressures and rising confidence. However, while administrative data points to healthy formal employment growth, the unemployment rate has not eased. Excess capacity in the labour market due to a large flow of migrants has contained wage growth. Economic activity slowed down in the first quarter of 2019, amid weather-related disruption to mining and weaker manufacturing output and lower export growth. Inflation remains close to the bottom of the central bank’s tolerance range, partly explained by a weaker exchange rate pass-through.

Source: OECD Economic Outlook 105 database.

Policy measures are needed for stronger and more inclusive growth

Because inflation has been weaker than expected, the central bank has appropriately halted the tightening that started at the end of 2018. Monetary policy is projected to remain accommodative and start tightening again at a slow and gradual pace as inflation approaches the 3% target and labour market slack shrinks and wages accelerate.

Fiscal policy is broadly appropriate with a gradual consolidation in line with the fiscal rule. Fiscal consolidation will take place by reducing spending growth and will be aided by recent improvements to the fiscal framework with the creation of an independent fiscal council. The planned tax reform will boost investment by simplifying the tax code, accelerating depreciation and speeding up VAT reimbursements. There is still room to increase revenues and make the tax mix more progressive and growth friendly, by raising revenues from environmental, property or personal income taxes while reducing corporate taxes.

Stronger and more inclusive growth will require ambitious reforms in other areas. A comprehensive agenda to bolster the business environment by streamlining regulations and licensing procedures will be key to lifting medium-term growth. Efficient public investment, particularly in education and training, innovation, and digital and transport infrastructure, should foster productivity and more inclusive growth. Boosting skills by enhancing lifelong learning and strengthening active labour market policies is needed to spread the benefits of digitalisation more widely. The pension reform currently under discussion in Congress is expected to raise pensions currently paid out through the publicly funded solidarity pillar, increase future pensions by raising mandatory contributions to privately managed individual accounts, while enhancing competition between pension fund administrators. Aligning the retirement age of men and women and linking it to life expectancy would further improve pension sustainability.

Growth is projected to remain robust

Growth is projected to remain robust on the back of solid macroeconomic fundamentals. Strong investment, aided by supportive financing conditions, high copper prices, the planned tax and labour reforms and positive business sentiment will drive growth and employment. A low and stable inflationary environment and stronger job creation will support private consumption. Government consumption and net exports will remain muted. However, a weaker external environment, driven by trade tensions, regional instabilities and a faster-than-anticipated normalisation of US monetary policy, remain important downside risks. Failure or delay to implement the planned tax reform, and the resulting uncertainty, would also lead to weaker growth. On the upside, full implementation of the ambitious structural reform agenda could raise investment more than anticipated. Faster growth in the region could also deliver higher growth.

Metadata, Legal and Rights

https://doi.org/10.1787/b2e897b0-en

© OECD 2019

The use of this work, whether digital or print, is governed by the Terms and Conditions to be found at http://www.oecd.org/termsandconditions.