2. Overview of the Vietnamese state-owned sector

State-owned enterprises play an essential role in the economic development of Viet Nam. They account for a large share of the economy and dominate in key business areas and receive preferential treatment from the government. This chapter provides an overview of Viet Nam’s SOE sector and its evolving presence in the national economy. Lastly it discusses the government’s recent efforts to improve the Vietnamese business environment by facilitating the SOE equitisation progress.

State-owned enterprises still account for a large share of the economy in Viet Nam. They dominate most of business areas in the economy and also have a close relationship with the government. Thanks to the government’s efforts to reduce the sector through equitisation and restructuring, the number of SOEs and its share in overall employment has significantly decreased over the years. However, SOEs still have a significant impact on the economy through their preferential position regarding access to credit and land. OECD mission team is informed that SOEs are treated “favourably” in all aspects by the government. Sectoral ministries and local governments give their affiliated SOEs privileges such as access to capital, natural resources, land, and human resources.

Although there are no explicit provisions in the Vietnamese law that indicate SOEs are entitled to preferential lending rates, in practice, a state enterprise that has higher operational costs than its private competitors can benefit from lower borrowing costs resulting from government guarantees extended by state-owned banks which hold more than 40% of assets of all credit institutions as of end-2020 (Public-Private Infrastructure Advisory Facility, 2016[1]; OECD, 2022[2]; World Bank Group, 2019[3]).

The new 2020 Law on Enterprises has broadened the definition of SOEs categorising SOEs into two groups based on the percentage of state ownership. As prescribed in Article 88 of the new Law on Enterprises, SOEs are i) enterprises with 100% charter capital held by the State and (ii) enterprises with more than 50% (but less than 100%) charter capital or voting shares held by the State. The previous 2014 Law on Enterprises had defined SOEs as enterprises with the form of a one-member limited liability company with the state as the sole owner. According to the new definition, there are 2 109 SOEs held by central government in the country,1 providing 1.1 million jobs as of 2019 (GSO, 2021[4]). Additionally, there are around 1 100 SOEs at the subnational level according to the General Statistics Office of Viet Nam. Enterprises with less than 50% state ownership are categorised and treated as private enterprises under the Vietnamese law. For instance, both Vinamilk and FPT are partially owned by the state but less than controlling shares level. As such, they are treated the same as private enterprises.

Both the absolute number of SOEs and its share in all enterprises significantly decreased over the past decade from 3 281 (1.18%) in 2010 to 2 109 (0.31%) in 2019 as a result of the government’s initiative on equitisation and divestment of SOEs. In the same period, its share in turnover in all enterprises reduced from 27.2% to 13.6%; pre-tax profit from 32.3% to 23.2% – implying that the government is divesting profitable SOEs and maintaining ownership for less profitable SOEs – consequently resulting in a decline in the contribution to the state budget from 45.4% to 26.9% (GSO, 2021[4]; ADBI, 2020[5]) (see Figure 2.1, Figure 2.2).

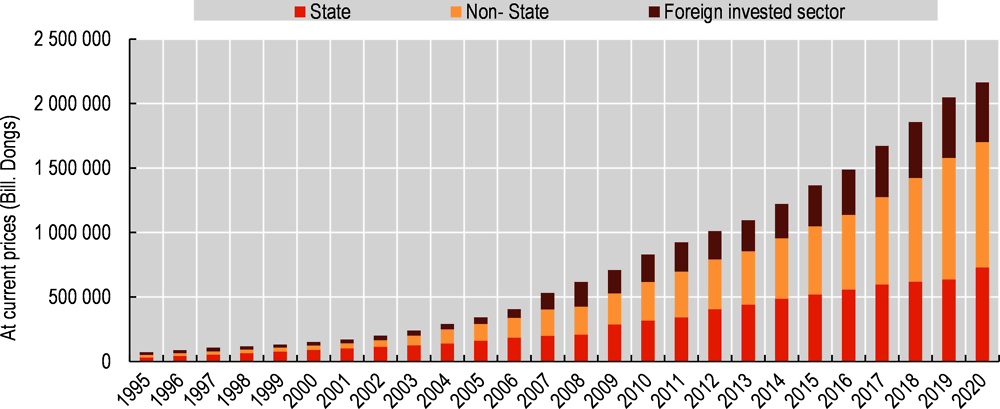

Regardless of such downward trend in several indicators, the state-owned sector is still a significant contributor to the national economy compared to domestic private enterprises and foreign direct investment (FDI) enterprises. State-owned enterprises constitute 22.8% of the country’s capital, accounting for around 30% of the country’s GDP (ADBI, 2020[5]; OECD, 2020[6]; GSO, 2021[4]). During the 2016-19 period, the state-owned enterprise sector still attracted considerable capital for production and business accounting for around a quarter of the total amount of capital attracted by all enterprises in the same period (GSO, 2021[4]).

Source: GSO (2021[4]), Statistical Yearbook of Viet Nam, https://www.gso.gov.vn/en/data-and-statistics/2022/08/statistical-yearbook-of-2021/.

Source: GSO (2021[4]), Statistical Yearbook of Viet Nam, https://www.gso.gov.vn/en/data-and-statistics/2022/08/statistical-yearbook-of-2021/.

State-owned enterprises are dominant across the economy and the most economically important ones are found in essential sectors. Like in many other countries large-scale SOEs are prevalent in the public utilities and network industries (e.g. telecommunication, energy, water and transportation). The economic importance of SOEs remains significant by international standards, with entire sectors still dominated by a few of these companies, such as in energy (electricity (87%) and petroleum products (84% of gasoline retail sale) and telecommunications (90% of mobile phone subscribers), thwarting potential economy-wide productivity gains (OECD, 2022[2]). Electricity of Vietnam (EVN) and PetroVietnam (PVN), the two largest corporations in the energy industry by total assets are fully state-owned. Only three companies – Electricity Vietnam (EVN), Petro Vietnam (PVN) and Viettel Telecom represent up to half of the state-owned sector’s total revenues.

Since the start of the equitisation process in 2010, the state’s presence in the manufacturing industries has reduced especially in the electronics and food processing sector – though it bears mentioning that the state still has widespread ownership (of 446 companies) in the manufacturing industries particularly with regard to textile and garment sector. The country also retains strong state ownership in sectors such as agriculture (in “primary sectors” in Table 2.2); finance; real estate and construction; and wholesale and retail trade (OECD, 2020[6]).

Other than fully state-owned VietnamBank for Social Policies and Vietnam Development Bank, the state owns more than 50% of shares in the largest domestic commercial banks such as Vietinbank, BIDV, Agribank and Vietcombank (Vuong and et al., 2019[7]).Vietnamese commercial banks deserve some credits for their financial stability, with the average capital adequacy ratio (CAR) of commercial banks from 2010 to 2015 being 14.79% which is above the requirement of the CzR regulated in the BASEL II (8%) (Nguyen, 2020[8]). Both return on equity (ROE) and return on assets (ROA) indicate relatively good performance in recent years (Korea Trade Promotion Corporation (KOTRA), 2020[9]). However, presence of FOLs and non-performing loans make banking sector less attractive for equitisation, in particular for some banks where bad assets could be hiding in the loan book.

2.2.1. Listed SOEs

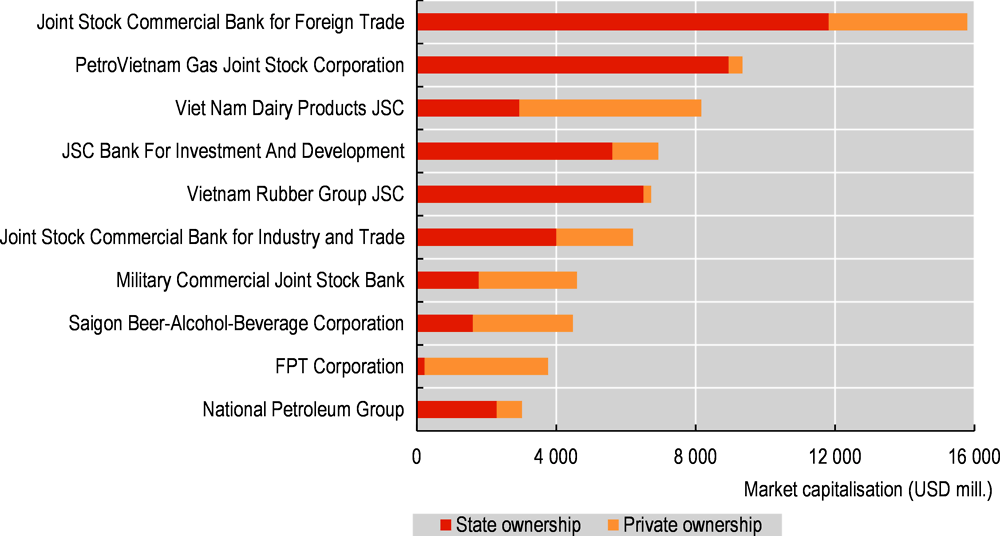

Among the listed companies in Viet Nam are 35 SOEs with majority state ownership. An additional 25 companies have the state as a significant minority shareholder (with a stake exceeding 10% of the voting shares) (see Annex C). As shown in the table below, among the ten largest SOEs with state ownership share, four are found in the financial sector and two belong to the PetroVietnam hydrocarbons group. The largest listed company with a majority shareholding is Joint Stock Commercial Bank for Foreign Trade of Viet Nam (market capitalisation of USD 15.8 bn.). The largest listed company with a minority state shareholding is Viet Nam Dairy Products (market capitalisation of USD 8.2 bn.) in which the state has 37.9% of the shares (see Figure 2.3). Partial privatisations through stock market listings have not brought much change in public sector ownership control in stock markets. In Viet Nam, the public sector still holds 28% of the capital of the largest listed companies as of end-2018 (see Figure 2.4).

According to an OECD study, most countries engaging in listing SOEs expect the companies to enjoy better access to financing going forward and to maintain higher standards of transparency and disclosure in consequence of the stock market listing and maintenance rules (OECD, 2016[10]). In Viet Nam, while listed SOEs have consistently performed better than other types of SOEs, their performance is less impressive than private listed companies. In an attempt to fix this problem, the Ministry of Finance has recently announced five-year roadmap on application of IFRS to all enterprises including SOEs.

Note: Data on market capitalisation and state ownership share of the listed companies is extracted from VietStock, https://finance.vietstock.vn/ on 7 October 2021.

Note: USD 1 = VND 22 837 on 7 October 2021.

Source: Author’s elaboration based on VietStock, https://finance.vietstock.vn/, submissions from the Ministry of Finance and SCIC on size and sectoral distribution of listed companies with state ownership of no less than 10%. Integrated information from the submissions is available in Annex B and Annex C.

Note: The table shows market capitalisation weighted average ownership for the public sector. Calculations are based on ownership data for the 100 largest listed companies in each market.

Source: OECD (2019), Equity Market Review of Asia 2019, OECD Capital Market Series, Paris, http://www.oecd.org/daf/ca/oecd-equity-market-review-asia.htm,

2.2.2. SOE as an investor

The state-owned sector has consistently been an important contributor to investment over the past two decades. Its share in total investment by corporate sector with different types of ownership is similar to that of domestic private companies and almost two times larger than that of foreign-invested sector (Figure 2.5). Such large presence of the state-owned sector in investment landscape and rather limited investor base can be explained by restrictions on foreign participation in the SOE equitisation process and prohibition in the past on majority foreign ownership of public companies. The OECD mission team was informed that foreign investors are often discouraged from buying stakes in SOEs as they are offered only minority stakes when doing so. Reluctance among investors have been often linked to the continued mix of commercial and non-commercial objectives in equitised firms, as well as the government’s insistence on holding more than 50% post equitisation. Government often retains significant direct or indirect shareholdings or strategic veto rights in listed companies.

The government has tried to address this issue by improving regulations on foreign ownership limits (FOLs) in recent years. New Security Law which came into effect in 2019 aims to remove FOLs in most industries except for specific sectors important to national security. This allows for public companies to take steps to increase the foreign ownership to 50% or above, or to remove foreign ownership restrictions when given approval by the State Securities Commission. However, a timeline for the implementation is not clear.

2.2.3. SOEs as vehicles of national development: A historical perspective

State-owned enterprises in Viet Nam are traditionally expected by the government to play a double role of implementing national development strategies and serving its central government. Legal texts, government strategies and policy guidelines are often developed with a view to achieving development strategy goals, which means that they are directed at the incumbent SOEs.

Reforms of ownership and governance have as their main objectives raising the effectiveness, cost efficiency and accountability in respect of their public policy objectives. Financial performance, while not neglected, traditionally came across as a secondary consideration mostly linked to the fact that the government wants to avoid fiscal loss. This has led to providing government guarantees on debt issued by SOEs, distorting level playing field.

At the meeting of the 12th Party Central Committee in May 2017, Vietnamese Government officially recognised for the first time the need to restructure and enhance efficiency of SOEs and the importance of promoting private sector2 by passing resolutions to tackle these issues. The resolutions have been translated into Socio-Economic Development Strategy for 2021-30 endorsed by the 13 National Party Congress in 2021 (Foster and Tien, 2021[11]). While the State officially recognised that the private sector is the foundation for economic growth and no longer the State in its official declaration at the Five Year Party Congress that met in late January, in certain markets, differences in access remain a problem. Notably, a preference for SOEs among state-owned financial institutions is often asserted. State-owned banks hold more than 40% of assets of all credit institutions as of end-2020 and development of non-bank financial sector and diversification of financial channels will help achieve more efficient resource allocation and better market access for private businesses. Avoiding bailing out lagging SOEs with state aid is important to facilitate market access for new entrants (World Bank Group, 2019[3]; OECD, 2022[2]) .

There have been recent improvements in the Vietnamese business environment – mostly driven by better and clearer laws and regulations implemented by government. The latest measures aiming to improve a business-friendly regulatory framework and ensure a level playing field between SOEs and private firms including foreign ones include the new Public Private Partnership (PPP), the amended Labour Code and the amended Competition Law. In the same vein, the government set a target to increase the share of private sector activities to 50% of its GDP by 2020, up from 43% in 2017 through equitisation of SOEs, encouraging the entry of innovative domestic SMEs and exit of insolvent SOEs. Vietnamese laws and regulations do not prescribe regulatory discrimination between companies based on ownership. However, this principle is often not adhered to in practice. This issue is covered more extensively in the Chapter 3 on “SOEs in the Marketplace” of the Part II of this report.

Most economically significant SOEs are located within business groups. In the earlier phases of the reform process a number of individual SOEs were merged into larger and more financially strong state general corporations (SGCs). With Viet Nam’s accession to the WTO many SGS were clustered into giant and highly diversified state economic groups (SEGs). The SEGs were at the time of formation considered as representatives of the “commanding heights” in the economy, likened by many researchers to the Korean Chaebols and Japanese Keiretsu. However, unintended consequence of their creation is that they have distorted competition landscape as directed lending within the large state-controlled Groups has been often practiced.

Ministry of Planning and Investment has recently set out a plan on development of large-scale SOEs focusing on developing the seven major state-owned companies with the combined total assessed value of over VND 20 trillion as industry leading companies to support the overall growth of their respective sectors. The government has emphasised that the plan is to allow for bigger autonomy for these SOEs in their decision making, removing certain regulations related to investment projects in order to reduce the state intervention in their internal affairs. However, it remains to be seen whether these state-owned companies will have a better access to government finance and guarantees compared to other SOEs or private companies.

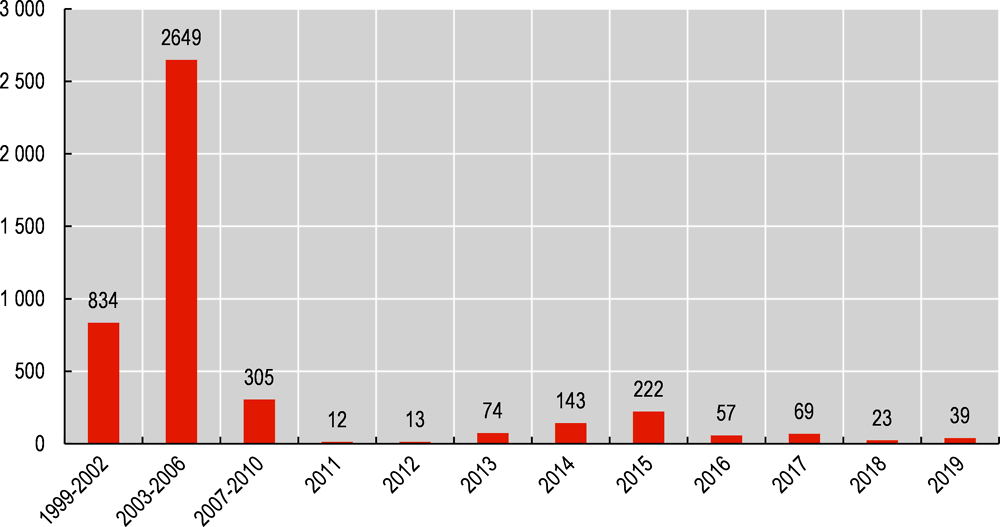

Since “Doi Moi” market-oriented economic reforms was launched in 1986, the restructuring of state-owned enterprises (SOEs) has been one of the top priorities of the economic reform process in the country. The equitisation of SOEs went ahead at fast pace in the 1990s and early 2000s but has slackened over the past decade. The total number of equitised SOEs was 2 649 during 2003-06 period. However, the number went down to 305 during 2007-10 period.

Equitisation means the conversion of a wholly owned company into a company that is owned by multiple shareholders. Enterprise Development Agency of the Ministry of Planning and Investment has been assigned to draft a decision by the Prime Minister on the classification of SOES – wholly owned, over 50%-owned, over 65% and under 50%. Depending on the state ownership extent, plans for sale of shares to external parties vary. When the state doesn’t have to earn controlling shares at a particular SOE, then external investors can purchase as much as they wish to control the company.

As a measure to accelerate the equitisation process of SOEs, in 2016, the Prime Minister approved a project on the restructuring of state-owned economic groups and corporations for the period of 2016-20. In 2017, the government successfully sold 54% of Saigon Beer Company (Sabeco) to Thai Beverage. From 2016 to June in 2020, Viet Nam had 175 equitised enterprises reaching a total enterprise value of VND 443.5 trillion, of which the state capital scale accounts for VND 207.1 trillion (GSO, 2021[4]).

A number of SOEs did not meet 2020 deadlines specified in Decision No. 26/2019/QD-TTg of Prime Minister and deadlines were reset for 2021. In 2021, only three SOEs were equitised amid the prolonged COVID-19 pandemic, and none were on the list approved by the Prime Minister. Viet Nam aims at completing the restructuring process of SOEs by 2025, through which around USD 11 billion in proceeds is expected to be raised.

Source: (ADBI, 2020[5]) (OECD, 2020[6]), Viet Nam Chamber of Commerce and Industry (VCCI).

Divestment and equitisation process in recent years has been widely criticised as being too slow and constantly behind schedule. Major challenges in undertaking equitisations include too tight deadlines, unclear directions from government notably related to land ownership rights, land valuation and evaluation of book value of SOEs. Reluctance among investors have been often linked to the continued mix of commercial and non-commercial objectives in equitised firms, as well as the government’s insistence on holding more than 50% post equitisation. A number of equitised SOEs still have important share of state ownership and have failed to attract foreign investors. Government often retains significant direct or indirect shareholdings or strategic veto rights in listed companies (OECD, 2016[10]; 2019[12])

The delay in equitisation is not only related to the approval process of real estate rearrangement and handling, but also due to complex state ownership arrangements consisting of a number of ownership representative agencies (Commission on Management on State Capital at Enterprises, Ministries, agencies, People’s Committees of Provinces) which do not have a clear guidance for SOEs in their respective portfolio to review and develop a business project in accordance with the direction of the Prime Minister. Multiple layers of bureaucracy have made it difficult and time-consuming for SOEs and related investors in participating in equitisation process. Plus, the COVID-19 pandemic in the past two years has diluted the Govenrmnet’s priority over equitisation of SOEs.

Further reform is foreseen mostly through equitisation of more companies and in the foreseeable future SOEs will maintain their dominant position only in sectors directly related to defence or national security. In an ideal scenario, all others will be open to foreign participation and/or competition. The government’s Socioeconomic Development Strategy (2011-20) recognises the importance of SOE reform, prioritizing faster rates of equitisation and privatisation. The government also plans to enact a new equitisation plan until 2025 period in the first half of 2022.

According to the government, SOEs after equitisation perform better and operate more efficiently as the use and management of state capital was improved. The mission team was informed that this has been reflected in the growth rates, production and business activities, the average income of employees and the total payment to the State budget. Some of the examples include Vinamilk (Viet Nam Dairy Products JSC), FPT (Information-telecommunication-technology group FPT Corporation) or REE (The Refrigeration Electrical Engineering Corporation) which maintain a high capitalisation value after equitisation according to stakeholders.

References

[5] ADBI (2020), State-Owned Enterprise Reform in Viet Nam: Progress and Challenges, https://www.adb.org/publications/state-owned-enterprise-reform-viet-nam-progress-challenges.

[11] Foster and Tien (2021), Corporate Acquisitions and Mergers in Vietnam, Wolters Kluwer.

[4] GSO (2021), Statistical Yearbook of Viet Nam, https://www.gso.gov.vn/en/data-and-statistics/2022/08/statistical-yearbook-of-2021/.

[9] Korea Trade Promotion Corporation (KOTRA) (2020), Banking industry performance in Viet Nam, https://dream.kotra.or.kr/kotranews/cms/news/actionKotraBoardDetail.do?SITE_NO=3&MENU_ID=180&CONTENTS_NO=1&bbsGbn=243&bbsSn=243&pNttSn=183292.

[8] Nguyen, P. (2020), Optimal capital adequacy ratio: An investigation of Vietnamese commercial banks using two-stage DEA, https://www.tandfonline.com/doi/full/10.1080/23311975.2020.1870796#:~:text=In%20general%2C%20the%20average%20CAR,the%20BASEL%20II%E2%80%948%25.

[2] OECD (2022), OECD Economic Survey of Viet Nam: Economic Assessment, OECD Publishing, Paris, https://doi.org/10.1787/8f2a6ecb-en.

[6] OECD (2020), Multi-dimensional Review of Viet Nam - Towards an Integrated, Transparent and Sustainable Economy, https://www.oecd-ilibrary.org/development/multi-dimensional-review-of-viet-nam_367b585c-en.

[12] OECD (2019), Corporate Governance Frameworks in Cambodia, Lao PDR, Myanmar and Viet Nam, https://www.oecd.org/daf/ca/Corporate-Governance-Frameworks-Cambodia-Lao-PDR-Myanmar-Viet-Nam.pdf.

[10] OECD (2016), Broadening the Ownership of State-Owned Enterprises: A Comparison of Governance Practices, OECD Publishing, Paris, https://doi.org/10.1787/9789264244603-en.

[1] Public-Private Infrastructure Advisory Facility (2016), Improving Private Sector Participation in Vietnam.” Impact Assessment, October.

[7] Vuong, Q. and et al. (2019), The Vietnamese Economy at the Crossroads, Southeast Asia and the ASEAN Economic Community, https://www.academia.edu/44314404/The_Vietnamese_Economy_at_the_Crossroads.

[3] World Bank Group (2019), Finance in Transition: Unlocking Capital Markets for Vietnam’s Future Development, https://documents1.worldbank.org/curated/en/971881576078190397/pdf/Finance-in-Transition-Unlocking-Capital-Markets-for-Vietnam-s-Future-Development.pdf.

Notes

← 1. There are also a large number of provincial and municipal SOEs which are managed at a sub-national level by their respective local governments. The SOE Guidelines would be applicable to these companies if their owners decided to implement them, but sub-national level SOEs are not in the scope of this review. The report is only focused on the SOE sector at the national level.

← 2. Private sector in Viet Nam mostly consists of small and medium-sized enterprises (SMEs), whereas SOEs tend to be large and operate in shielded sectors. A general concern of business community in Viet Nam is a relative scarcity of the funding available to SMEs, which is also spotted in many OECD countries.