2. Planning and public governance

This chapter examines governance for clean energy finance and investment governance and power planning in Indonesia. It provides an overview of Indonesia’s institutional framework for clean energy and electricity market structure, as well as identifies areas to improve coordination across institutions, at all levels of government, to ensure effective and consistent goals and policies. The chapter also highlights progress and opportunities to improve the country’s clean energy finance and investment-related targets, strategies and power planning mechanisms with a view to sending credible, ambitious and long-term signals to investors.

Indonesia has committed to ambitious clean energy and emission reduction targets, which will necessitate strong policy action in order to mobilise the substantial amount of finance and investment needed to realise these goals. Considering the number of policy areas and government institutions (including at the sub-national level) involved in that effort, good public governance as well as effective coordination mechanisms will be essential enabling factors. Equally, defining a long-term pathway to realise a clean energy transition, with clear targets and milestones, backed by strong political commitment as well as transparent monitoring and evaluation to track progress, will be critical to build market confidence and give investors early signals of future market development.

Strengthening of the National Energy Council’s co-ordination role is needed

The National Energy Council (DEN) is the main body responsible for cross-sector energy issues and is responsible for overseeing the implementation of national energy targets outlined in the RUEN (National Energy General Plan) across different line ministries. DEN also plays a vital role to guide and assist regional governments to establish regional energy general plans (RUED) and supports provinces interested in developing clean energy. In practice, few of DEN’s recommendations reach the implementation phase due to challenges in internal co-ordination and implementation, despite DEN’s prominent role under the President of Indonesia and being chaired by the Minister of Energy and Mineral Resources. In addition, from 2009 to 2020, regular coordination meetings to discuss and overcome energy issues were limited and not able to be conducted consistently. Over this period, only four of the required 22 plenary meetings were held while only 28 of the 72 minimum required member meetings took place. The operationalisation of DEN according to its original mandate as stated in the 2007 Energy Law and Presidential Regulation No. 26/2008 would strengthen its role and improve the implementation of its recommendations.

Strengthening co-ordination between government institutions is crucial to enhance and streamline the regulatory environment

Progress on clean energy development is currently hindered, in part, by the large number of ministries involved in energy policy, with sub-optimum coordination. This includes the Ministry of Energy and Mineral Resources, the Ministry of Industry, the Ministry of Public Works and Housing, the Ministry of Finance, the Ministry of Trade, the Ministry of Transport, the National Development Planning Agency, the Ministry of Research and Technology; and the Agency for Assessment and Application of Technology. Regional and local governments are also responsible for developing energy efficiency and renewable energy regulations, as are sub-national governments. Co-ordinating policy and improving clarity in the roles and responsibilities of these actors would help to create a more cohesive and conducive environment to accelerate clean energy development. The national government should work closely with regional governments to insure they have the skills and resources necessary to deliver the clean energy transition.

Economic dynamics impact energy and should be better reflected in energy planning and target setting

A high economic growth assumption in the 2011 Masterplan for Acceleration and Expansion of Indonesia's Economic Development (MP3EI) was used in the RUEN model for setting the 23% renewable energy target for 2025. The 35 GW expansion programme announced in 2015 for completion by 2019 also used this high assumption. Yet, economic growth has been substantially less than forecasted and energy demand growth even lower, as digitalisation, a shift towards less energy-intensive services and behaviour changes have all slowed down energy demand since 2015 (MEMR, 2020[1]). As a result, in 2018 the government revised the 35 GW programme’s target commercial operation date to 2024. It recently revised the target again to 2028 to reflect the global economic recession. These repeated changes highlight the need to better account for economic dynamics within Indonesia’s energy plans and target setting.

Aligning energy planning with One Map tools could improve clean energy investment

RUEN is referenced by the National Power Utility (PLN) in its annual electricity business plan (RUPTL), though RUPTL uses lower short-term economic growth assumptions, creating inconsistencies with lower PLN outlooks compared to RUEN targets. Both RUEN and RUPTL’s overestimation of energy demand also creates uncertainty on the timing for new capacity additions, which negatively impacts the return potential for projects and discourages investments. Renewable energy project locations stated in RUPTL, likewise do not align with project developers preferred sites to meet the potential market demand, limiting integration of potential renewable electricity without expansion of the transmission network. The government has developed the Indonesia One Map tool gathering spatial information from various ministries, including renewable energy potential and electricity infrastructure that can be layered with other elements such as demographic data, transportation and communication infrastructure, and forestry and mining areas. The One Map tool is an opportunity to align RUEN and RUPTL models to improve outlooks and information on renewable energy potential, making energy planning more consistent and robust to increase investor confidence.

Data transparency and accessibility is a key for enhancing financial project support

Clean energy projects have characteristics such as geographic location, energy resource type and intermittency of electricity production, which many financial institutions are unfamiliar with. This creates challenges to assess and manage risks associated with the projects. To overcome these challenges, financial institutions require transparent data that can be used to compare information provided by project developers in their feasibility studies and that ideally can be assessed by an independent verifier. The government is expected to provide some data currently held by various government institutions, such as topography data, rainfall levels, catchment area status and potential for renewable energy resources. In spite of OJK’s efforts to report financial institutions’ data needs, there is still a considerable lack of easily accessible data.

Energy efficiency and promotion of renewable energy can support green economic recovery

The 2020-24 Medium-term National Development Planning (RPJMN) adopted a low-carbon development initiative (LCDI), which will allow more sustainable activities to help achieve Indonesia’s climate change target. While the 2020-24 RPJMN referred to RUEN and has more stringent aspects that need to be applied by all ministries and government bodies, there is no clear indication of how investment can meet the LCDI objectives. With abundant renewable energy resources and significant energy savings potential across the economy, as well as the LCDI that can guide green recovery measures, there is great opportunity for Indonesia to invest in clean energy as a way to bolster economic recovery while reducing emissions. Further efforts are needed if this potential is to be realised, as Indonesia has only reached a 9.15% share of renewables in Total Primary Energy Supply (TPES) in 2019, which is far behind the 23% target set in the RUEN for 2025 (DEN, 2020[2]). Unlocking access to low-cost finance is also critical if the targets are to be met.

Clean energy development needs clear, long-term signals from the government that reflect opportunities for investors

Changes in clean energy planning and governance can negatively impact investor confidence and project development. In recent years, abrupt changes such as the 2018 revocation of the 2016 energy service company (ESCO) regulation have complicated clean energy finance and investment, especially given the often long-term nature of those projects. Impending measures such as the revision of Government Regulation on Energy Conservation and the New and Renewable Energy Law currently under preparation should help to create a more coherent framework for energy efficiency and renewable energy governance since it would allow the ESCO business model and feed-in-tariff (FiT) scheme to improve clean energy investment. Ensuring the intent of those measures is reflected across national energy planning and policy implementation will be critical to encouraging and enabling the market to seize clean energy opportunities by providing long-term signals to investors.

Strengthen DEN’s co-ordination role in order to ensure effective implementation of its policy recommendations can speed up Indonesia’s clean energy transition. Importantly, ensuring that DEN can be operationalised according to its original designation stated in the 2007 Energy Law and Presidential Regulation No. 26/2008 can improve the implementation of its recommendations and thereby help achieve the country’s clean energy targets.

Facilitate capacity building and technical assistance for local governments and universities to carry out energy transition programs as well as provide incentives for effective implementation of energy efficiency and renewable energy projects at the local and regional levels. Share good practices and success stories across different provincial and municipal governments, and where relevant provide support to help replicate success from one province or municipality to another.

Conduct a transparent and integrated assessment of the economic and behavioural assumptions behind energy outlooks used to set policy targets and energy plans. This includes ensuring there is appropriate planning capacity (e.g. within the Ministry of Energy and Mineral Resources, or MEMR) to address evolving needs and opportunities in a more complex and dynamic energy system, particularly as demand forecasting increasingly will need to account for the links between network changes and expansion, decentralised energy production and energy efficiency uptake.

Consider revising the RUEN to reflect changes in Indonesia’s economic situation and in the costs and performance of clean energy technologies. These adjustments then will be referred by the annual RUPTL revision process using the One Map tool to improve the outlook for clean energy development, market demand, and electricity or other infrastructure.

Consult with stakeholders, including from the financial sector, to help build consensus and investor confidence in the clean energy targets, increasing the attractiveness of those projects and facilitating access to finance.

Prioritise the development of a transparent and accessible database that links clean energy data with financial aspects of clean energy projects to minimise perceived risk. Encourage independent entities to provide project data and support overall enhancement of clean energy project feasibility studies, which will contribute to more viable business and financial plans.

Identify priority clean energy technologies and communicate as part of the energy planning process. This will help signal investment opportunities and identify required support mechanism to help achieve Indonesia’s affordability, economic development, and environmental sustainability goals. Setting priorities for clean energy technology development can also be used as a benchmark to track progress over time and make necessary adjustments to energy planning and governance to ensure the long-term success of those targets.

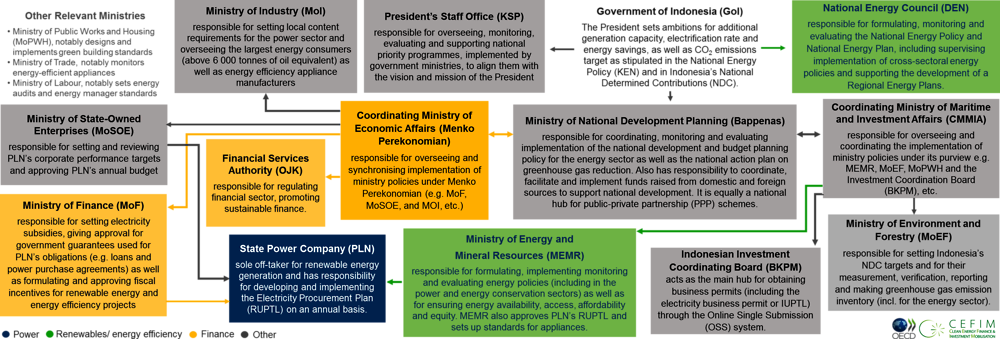

Clean energy policy, finance and investment governance is split across multiple institutions

Indonesia’s institutional framework for clean energy policy, finance and investment is fragmented across numerous institutions see Figure 2.1). The Ministry of Energy and Mineral Resources (MEMR) is the main institution responsible for developing and implementing Indonesia’s energy policy, including renewable energy and energy conservation, and the monitoring of energy use through the online energy management reporting system. The clean energy sector falls under the purview of the Directorate-General (DG) of New and Renewable Energy and Energy Conservation (NREEC). MEMR is also responsible for regulating the power sector through the DG of Electricity. Additionally, MEMR has a number of agencies exerting key responsibilities over, for example, clean energy Research and Development (R&D) and innovation (the Agency for R&D); the mapping of geological resources, volcanology and disaster mitigation (the Geological Agency); and the continuous development of MEMR’s staff and human resources in the field of energy (through the HR Development Agency) (see Chapter 7 for more details on R&D and training and capacity building).

In addition to MEMR, the Ministry of Finance (MoF) and Financial Services Authority (Otoritas Jasa Keuangan, OJK) also hold important responsibilities over clean energy finance and investment. The MoF approves tax and price incentives as well as guarantees that may be provided to support power projects (see Chapter 5 for a detailed discussion on Indonesia’s clean energy incentive schemes). MoF’s Directorate of Government Support Management and Infrastructure Financing is responsible for reviewing and approving guarantee requests. MoF also recommends the maximum level of electricity subsidies to PLN in the national budget and reviews loan arrangements entered into by PLN (including eventual government guarantees of PLN’s loans) (PwC, 2017[3]). As the financial market supervisor and regulator, OJK has played a key role in mainstreaming sustainable finance in the country through a number of policies and measures, including in the field of clean energy (see Chapter 6).

At the heart of overall investment promotion, facilitation and regulation is the Indonesian Investment Coordinating Board (Badan Koordinasi Penanaman Modal, or BKPM), which has played an instrumental role in establishing a business-friendly environment in the country in recent decades, co-ordinating across the entities that influence investment policies or their implementation (OECD, 2020[4]) . In recent years, its focus has been to simplify licensing, facilitate investment projects and improve conditions to attract investments (see Chapter 5). This is a challenging task, however, given the number of ministries and public agencies – including the Coordinating Ministry for Maritime and Investment Affairs (CMMIA), the Coordinating Ministry for Economic Affairs (CMEA), and the President’s Staff Office – involved in clean energy investment promotion and facilitation, not excluding the provincial, district and municipal governments that also play a role.

Source: OECD, 2020.

Other government institutions also hold important responsibilities over matters related to clean energy finance and investment (see Table 2.1), including:

The Co-ordinating Ministry of Maritime and Investment Affairs (CMMIA) co-ordinates line ministries responsible for energy, transport, environment, and investment issues and provides policy implementation support.

The Co-ordinating Ministry of Economic Affairs (CMEA) co-ordinates line ministries responsible for finance, industry, state-owned enterprises, research and technology, and spatial planning issues and provides policy implementation support.

The National Energy Council (Dewan Energi Nasional, DEN) is a co-ordination body responsible for co-ordinating energy-related cross-sectoral matters and monitoring progress towards clean energy targets. It brings together ministries indirectly involved in the energy sector, namely MEMR, MoF, the Ministry of Environment and Forestry (MoEF), the Ministry of National Development Planning (Bappenas), the Ministry of Transport (MoT), and the Ministry of Industry (MoI). DEN is chaired by the President and Vice President. The Minister of MEMR serves as Executive Chairperson.

The President’s Staff Office is an ad-hoc institution responsible for monitoring the implementation of all the President’s priority programmes by line ministries; such as (in clean energy) increasing the capacity of installed renewable energy in the national energy mix; the implementation of minimum energy performance standards (MEPS); and the mandatory labelling of electrical appliances.

The Ministry of National Development Planning or Bappenas (Badan Perencanaan Pembangunan Nasional) establishes the national medium- and long-term development plans, manages international development funding sources as well as monitors progress towards targets set out in Indonesia’s National Determined Contribution (NDC) under the Paris Agreement. Bappenas is also responsible for facilitating cooperation on infrastructure projects between the government and private investors.

Line ministries and institution:

The Ministry of Finance (MoF) is responsible for setting the electricity subsidy, gives the approval for government guarantees for PLN’s obligations in loans and power purchase agreements (PPAs) as well as formulating and approving the fiscal incentives for renewable energy and energy efficiency projects

The Ministry of Industry (MoI) sets local content requirements (LCRs) for a range of renewable technologies.

The Ministry of Public Works and Housing (MoPWH) is responsible for establishing green building codes and setting green building standards.

The Ministry of Trade (MoTrd) monitors the trade of energy efficient appliances.

The Ministry of State-owned Enterprise (MoSOE) oversees the business and management performance of the national state-owned power utility (PT PLN or simply PLN).

The Ministry of Environment and Forestry (MoEF) is responsible for governing environmental issues related to the energy sector.

The Indonesian Investment Coordinating Board (BKPM) is Indonesia’s investment promotion agency, notably responsible for granting business permits to clean energy projects (see Chapters 4 and 5).

The Financial Services Authority (OJK) is responsible for formulating the financial industry regulation and the sustainable finance policy as well as monitoring and evaluating its implementation.

Lack of an effective co-ordination body is a challenge

According to the 2007 Energy Law, DEN has the strongest position to oversee the implementation of the national energy policy (Kebijakan Energi Nasional, or KEN) which is the guideline for the country to achieve some of the energy targets including to reach 23% of renewable energy share by 2025 in the TPES. DEN is the sole co-ordination platform for cross-sectoral energy issues and is led by the President with daily activities chaired by the Minister of Energy and Mineral Resources. The government is represented by eight ministries (AUP-Anggota Unsur Pemerintah) (see Table 2.1) and eight members representing other stakeholders (AUPK-Anggota Unsur Pemangku Kepentingan) are chosen by parliament.

DEN addresses energy issues through its plenary meetings which are supposed to be conducted at least twice a year and led by the President, as well as member meetings led by the Minister of Energy and Mineral Resources every two months. These meetings are expected to establish policy recommendations that need to be implemented by the ministries and stakeholders that are then subsequently monitored and evaluated by DEN. While, ministries need to report to DEN on the progress of implementing the policy recommendations, they also need to report to other existing co-ordination bodies i.e. CMMIA, CMEA, Bappenas, and the President’s Staff Office.

The multiplicity of these co-ordination bodies has had unintended consequences, however, sometimes resulting in implementation of overlapping policy measures. For example, the CMMIA, the President’s Staff Office, and Bappenas have all included the rural electrification programme (consisting of the development of renewable power plants in remote areas and small islands) in their broader policy programmes, but all have done so with different levels of detail as well as inconsistencies in the type of technology and size of project to be developed under the programme. Setting up a single online reporting mechanism could thus help address this issue, through enhancing co-ordination across programmes and facilitating the monitoring of their implementation.

Overall, the lack of an effective co-ordination body for clean-energy-related issues has made the co-ordination process a challenge. Despite its co-ordination role, DEN has been perceived to be ineffective and lacked the authority to ensure acceptance and application of its recommendations by other line ministries. For example, DEN has faced significant challenges in getting different line ministries to agree on Indonesia’s electric vehicle programme on a range of issues under its co-ordination, e.g. on local content requirements, incentives, safety, and environment aspects1, before it was ultimately approved by the President in 2019. Acting on this issue, parliament recently recommended the government amend current regulations to strengthen DEN’s role and functions, although it remains to be seen how this will be followed through2.

Setting a long-term strategy to achieve a clean energy transition is important to send the right market signals and help drive up investment. To be credible, clean energy targets should be ambitious but also realistic, well-budgeted, and time-bound. Ambitious objectives should be accompanied with quantified intermediate milestones that can help investors get a sense of how (fast) clean energy markets are expected to develop (OECD, 2015[5]).

Indonesia’s policy-planning mechanism for clean energy finance and investment is complex and articulated over different time horizons. MEMR is the main body responsible for defining Indonesia’s clean energy strategy while Bappenas is responsible for mainstreaming that strategy into the country’s overarching medium- and long-term development plan – that sets the course for the country’s development in all policy areas – as well as climate strategy. Ensuring that these different policies and plans are consistent, coherent, well-articulated, with clear, time-bound and measurable objectives is important in order to scale up clean energy investment that can meet the low-carbon development and climate change targets.

Clean energy plays an important role in Indonesia’s climate strategy

Indonesia defined long-term carbon emission reduction objectives as part of its Nationally Determined Contribution (NDC) under the 2015 Paris Agreement to address climate change and contribute to the global mitigation effort. Under its NDC, Indonesia committed to lowering carbon emissions by 29% (or around 834 million tons CO2 equivalent) and up to 38% (or about 1 081 million tons CO2 equivalent) with international assistance by 2030 compared to the 2010 baseline. Additionally, the target shows that Indonesia relies heavily on the forestry sector to reduce emissions by 60%; whereas the energy sector also plays a pivotal role in national carbon reduction efforts, accounting for around 38% of targeted emission reduction under its unconditional NDC (see Table 2.2). However, the impact of the current COVID pandemic could affect the trajectory and achievement of emissions; hence, this should be reflected in NDC targets.

Emission reduction in the energy sector will be achieved through the implementation of various programmes as defined in the 2012 National Action Plan for Greenhouse Gas Reduction (RAN-GRK) and the 2019 Roadmap of NDC Implementation on Mitigation Action, such as the development of renewable and energy efficiency projects. Interestingly, although the energy sector is the second major contributor to reduce emissions after the forestry sector, the government estimates that around USD 236 billion will be absorbed by the energy and transport sectors or around 95% of total USD 247 billion investment needed to achieve the country’s NDC by 20303. This requires further evaluation from the government to recalculate the investment needs as the cost of clean energy technology has significantly declined over the last decade.

Indonesia’s clean energy goals are laudable but could prove challenging to achieve

In the energy sector, the 2007 Energy Law is the primary reference for Indonesia’s long-term energy policy and targets. The law notably mandated the issuance of Indonesia’s National Energy Policy (Kebijakan Energi Nasional, KEN) in 2014 to provide an overarching policy framework for the energy sector. KEN devises a high-level strategy for Indonesia to achieve energy security and energy independence based on energy management principles such as accessibility, affordability, and sustainability. To reach those objectives, KEN defines a range of high-level targets to be achieved over the 2025 and 2050 horizons (see Table 2.3), including a 23% renewable energy share in Total Primary Energy Supply (TPES) by 2025 as well as a 1% annual reduction in energy intensity until 2025. While KEN is embedded in Government Regulation No. 79/2014, it is not legally binding.

To complement the commitment to establish more efficient energy use, Government Regulation No. 70/2009, which notably governs how the country should implement energy conservation activities to reduce energy consumption by, for example, setting the standard and labelling programme. It also establishes the obligation for large energy consumers (above 6 000 TOE per year) to report their energy consumption and energy management actions. To promote its implementation, the government provides incentives and assistance to stakeholders. In reality, the implementation of these regulations face obstacles including the electricity oversupply which discourages energy efficiency activities as the government prioritises programs to increase electricity consumption.

Alongside the commitment to achieve KEN objectives, the government enacted the National Energy General Plan (Rencana Umum Energi Nasional or RUEN) in 2017, which defines more detailed, annual targets, as well as programmes to be implemented by line ministries. RUEN notably breaks down KEN’s 2025 installed power capacity target into annual technology sub-targets for each province, based on estimates of their renewable resource potential (see Chapter 1 for more details on Indonesia’s renewable potential). It also sets out a number of programmes and measures to achieve targets, including: renewable energy resource management, incentive and price scheme design, capacity building, and research and development, as well as areas for international cooperation. However, it is not clear how these programmes align with Indonesia’s NDC and RAN-GRK. Additionally, RUEN does not provide estimates of investment needs to realise targets, let alone a strategy to mobilise domestic and foreign sources of finance and investment. In this regard, the Institute for Essential Services Reform (IESR) and Institute for Energy Economics (IIEE) (2019)4 estimated that USD 72.3 billion (or 44.2 billion excluding large hydropower i.e. above 10 MW) will be needed to reach RUEN’s renewable energy targets by 2025, far below what has been realised to date (see Chapter 1) (IESR, 2019[6]).

RUEN’s targets could be ambitious, as it is based on optimistic underlying assumptions. There are a number of assumptions used in the RUEN model to estimate future energy demand, of which two are of particular importance: economic growth projections ranging from 4.8% in 2015 to 8.0% in 2025 – derived from the 2011 Masterplan for Acceleration and Expansion of Indonesia's Economic Development (MP3EI)5 document – and population growth projections ranging from 1.3% in 2015 to 0.8% in 2025. However, economic growth assumptions underlying RUEN’s targets turned out to be greatly over-estimated; for instance, the MP3EI projected an annual GDP growth average of 6.54% over 2015-19, while actual economic growth only averaged 5.03% over that period based on Indonesia’s Statistical Agency (BPS, 2020)6, mechanically inflating targets (including installed power capacity for both renewables and fossil fuels by 2025)7.

Local governments need to play a greater role in implementing clean energy targets

While the 2007 Energy Law obligates local governments (province and regency) to establish Regional Energy General Plans (RUEDs) referring to RUEN, close to half of the country’s local governments have yet to do so. As of 2021, for instance, 19 provinces (out of 34 in total) have enacted a RUED while the plans of the remaining provinces are still being developed8.

There is also a mismatch between RUEN’s provincial-level targets and provinces’ actual level of ambition. For example, the Papua province, which abounds with renewable sources (albeit with a low population) is yet to prepare a RUED while South Kalimantan continues to prioritise coal projects in its RUEDs, despite this being inconsistent with RUEN plans. Equally, many provinces’ RUED targets differ from those stated in RUEN; for example, South Sumatera’s RUED plans for the construction of 50 MW of solar PV projects by 2025, while RUEN plans for 296 MW over the same period (based on the province’s potential and demand projections). Notwithstanding these challenges, some provinces have been particularly ambitious under their RUEDs, with the Bali province being a case in point, as it is committed to 100% renewable electricity by 2050.

Most of the difficulties faced by local governments in developing robust RUEDs, are attributable to a lack of capacity as well as limited understanding about clean energy. Many local governments, for example, lack the financial and human resources to undertake the modelling and research work needed to develop RUEDs. Local governments also lack the authority to set a sufficiently attractive renewable power price as set out at the national level. Adding to the challenges, there is a very long bureaucratic process to obtain local parliaments’ final approval of RUEDs.

Indonesia’s new mid-term plan could help revive support for clean energy

The Ministry of National Development Planning (Bappenas) is responsible for establishing the Medium-term National Development Plan (Rencana Pembangunan Jangka Menengah Nasional or RPJMN), which sets the course for Indonesia’s development over a five-year horizon (tallying with presidential mandates) through a range of multi-sectorial objectives and targets. The RPJMN is designed through a series of bottom-up and top-down consultations, and allocates state budget to different line ministries and agencies. These institutions and local governments then use the RPJMN as a reference to develop and implement their own plans and policies, e.g. the annual Government Work Plan (or Rencana Kerja Pemerintah) and Medium-Term Regional Development Plan.

The recently adopted 2020-24 RPJMN has made the low-carbon development initiative (LCDI) and the green economy the cornerstone of its development strategy. This is a welcome step for clean energy given the plan recognises the importance of renewable and energy efficiency for Indonesia’s economic development and reiterates the government’s commitment to achieve RUEN and NDC targets. The RPJMN represents a great opportunity to demonstrate that clean energy and the green economy can help support Indonesia’s economic growth, particularly as it recovers from the impact of the COVID-19 crisis.

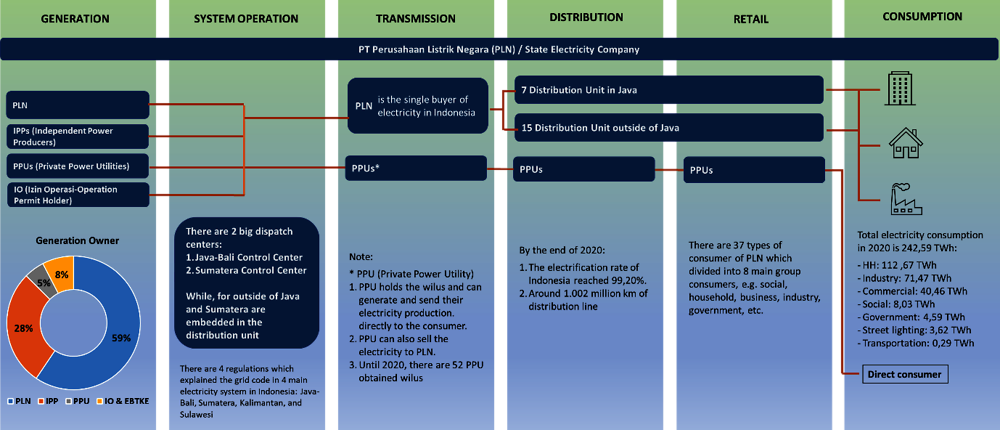

Electricity Law No. 30/2009 is the main legal basis for Indonesia’s electricity market. The law notably allocates roles and responsibilities to different government institutions and other market players as well as defines the electricity permitting, tariff-setting and planning processes (see next section for more details on electricity planning). The law also states that Indonesia’s State Electricity Company (PLN) shall maintain a dominant position in all segments of the power market, making it a de facto (vertically-integrated) monopoly (see Figure 2.2).

Source: OECD, 2020

There have been attempts to unbundle PLN and liberalise Indonesia’s power market through the enactment of Electricity Law No. 20/2002. However, the law was later rescinded by the Constitutional Court of Indonesia on grounds that it was contrary to the constitution, which states that electricity provision should remain the responsibility of the state. Consequently, the government issued a number of government decrees (and close to 40 implementing regulations summarised in Table 2.4) to guarantee fair-competition and well-functioning of the market, although implementation has proved challenging in practice (see Chapter 4). Despite PLN’s dominant role in power generation (owning two-thirds of generation assets), the government has been encouraging increased participation by Independent Power Producers (IPPs) and electricity business area (Wilayah Usaha Ketenagalistrikan) permit holders in the market over the last five years, in a bid to re-allocate PLN’s limited resources to generation and transmission infrastructure. As a result, the share of IPPs in total power generation rose from 21% of total installed capacity in 2015 to 26% in 2019 (MEMR, 2020[7]).

In addition, to ensure that the implementation and management of the electricity market is carried out in a more transparent and fair manner, there are some suggestions of establishing an independent renewable energy regulatory body which is also expected to accelerate the utilisation of clean energy. The Indonesia Renewable Energy Society (Masyarakat Energi Terbarukan Indonesia, or METI) proposed this idea to parliament, which is currently drafting the New and Renewable Energy Law9. In a recent study, meanwhile, the Asian Development Bank (ADB) emphasised that such a regulatory body could be formed through the stipulation of government regulation or presidential regulation in a similar manner to the establishment of the SKK Migas (the Upstream Oil and Gas Special Regulatory Taskforce) or the BPTJ (the Indonesia Road Toll Regulatory Agency)10. If Indonesia intends to consider and assess this suggestion, there are some lessons that can be learnt from other countries, such as SEDA (Sustainable Energy Development Authority) in Malaysia, ERC (Energy Regulatory Commission) in the Philippines, EMRA (Electricity Market Regulatory Authority) in Turkey or ANRE (the National Electricity Regulatory Authority) in Morocco.

Unlike in the generation segment, PLN has been the sole developer of the country’s transmission and distribution infrastructure. Although regulation allows private developers to build transmission and distribution lines, there are some requirements, such as obtaining an electricity business area permit, establishing a feasibility study, providing adequate funding and obtaining power wheeling approval from the Energy Minister, which the process and the practice have been a deterrent for developers to invest in the electricity downstream business. Until the end of 2019, 52 private power utilities (PPUs) have obtained the electricity business area permit, allowing it to provide electricity directly to its customers.

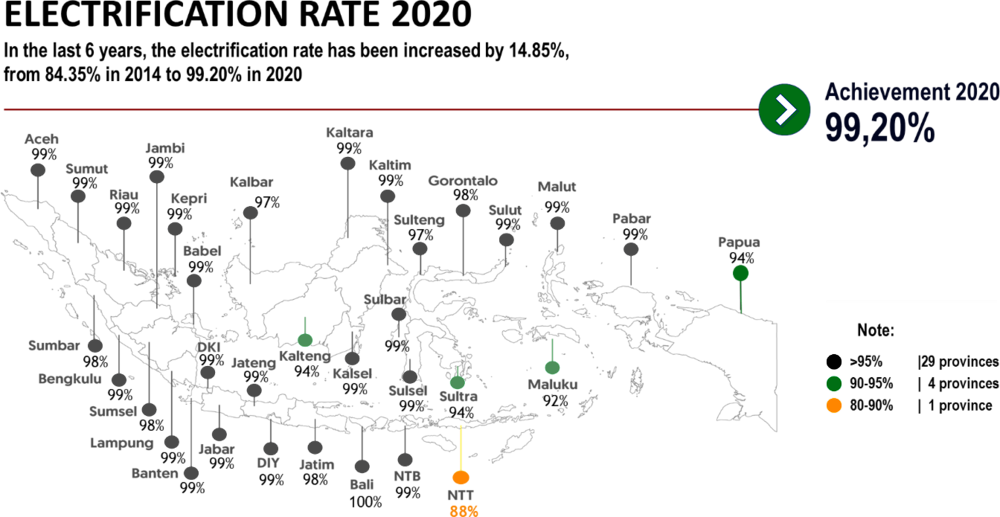

In line with the generation plan, PLN submitted its commitment to the government to build a transmission and distribution line which is stated in the Electricity Business Plan (RUPTL). This is very important since it can help PLN to reach more of the market thus lowering its oversupply capacity in some areas of the country. Hence, the government asked PLN to invest more in transmission and distribution lines11. Despite some delays in its development, by December 2020, PLN had built around 61 960 circuit kilometres (ckm) of transmission lines spread across 28 electricity systems, as well as two big dispatch centres, i.e. the Java-Bali Dispatch Centre and the Sumatera Dispatch Centre (other dispatch centres being embedded in each PLN distribution units). Concerning distribution lines, PLN has built around 1 005 080 ckm, which helped increase the country’s electrification rate to 99.20% (see Figure 2.3; see Chapter 1).

Source: MEMR, 2021

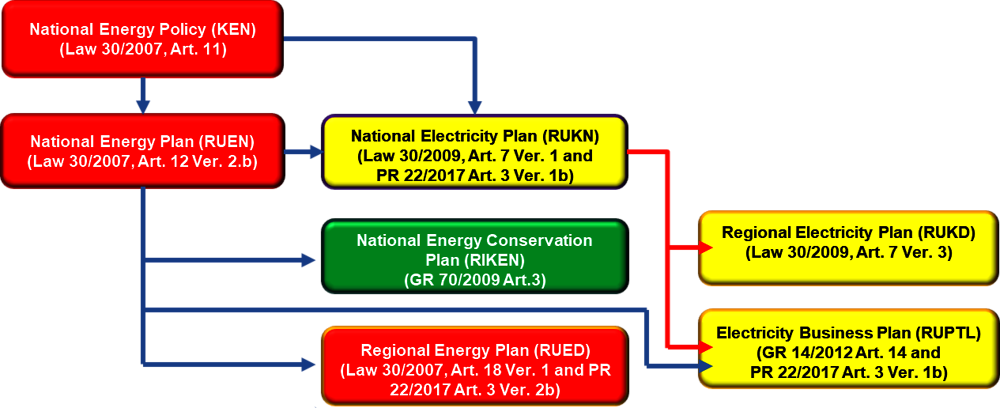

Electricity planning is set out in a number of planning documents (see Figure 2.4):

The National Electricity General Plan (Rencana Umum Ketenagalistrikan Nasional, or RUKN) constitutes the backbone of Indonesia’s electricity planning. Referring to KEN, the plan notably makes forecasts for power supply and demand as well as plans investment and utilisation of renewable energy resources over a 20-year horizon. MEMR’s DG of Electricity is tasked to develop and update RUKN on a regular basis with the current RUKN covering the years 2019-2038.

The Regional Electricity General Plan (Rencana Umum Ketenagalistrikan Daerah or RUKD) is prepared by local governments in reference to the RUKN to guide how the electricity infrastructure will be developed based on regional conditions. Although it is mandated by Electricity Law, until the end of 2020, no provinces had established RUKD using 2019 RUKN. However, there were some provinces which established RUKD using 2008 RUKN, i.e. East Kalimantan, Central Java, and West Nusa Tenggara.

The Electricity Business Plan (Rencana Umum Penyediaan Tenaga Listrik or RUPTL) is a ten-year electricity development plan developed by PLN on a regular basis, in reference to RUKN, KEN and RUEN. The RUPTL is a very important document for all investors in the Indonesian power sector as it contains detailed and up-to-date demand forecasts, future expansion plans, electricity production forecasts, and fuel requirements, etc. It also allocates project development to PLN and IPPs, as well as defines the procurement route for IPPs to build power plants. All projects should be listed in the RUPTL prior to procurement.

Source: 2007 Energy Law, 2009 Electricity Law

In addition to these plans, in 2015 President Joko Widodo launched the 35 GW programme to accelerate the achievement of the 100% electrification ratio and RUEN’s targets. Some of the capacity of the 35 GW programme is to continue the FTP-2 project that was not implemented after 2015 due to the changes of demand projections. Furthermore, the 35 GW programme is to be integrated into the RUPTL. However, the plan is confronting similar challenges as faced by previous Fast Track Programmes (FTPs) causing some delays in project delivery (see Box 2.2).

To address the electricity shortage and lowering fuels import that caused a heavy subsidy on fossil fuels in the state budget, in 2006, Indonesia launched the 1st Fast Track Programme (FTP-1) targeted to build around 10 000 MW of coal-fired power plants by 2010. Referring to Presidential Regulation No. 71/2006, of the 40 different locations of coal-fired power plants, 10 of them are located in Java (with a total capacity of 7 430 MW) and 30 locations outside Java (total capacity 2 121 MW).

In 2009, the government revised the regulation and changed some objectives, e.g. the completion date from 2010 to 2014, the location from 40 to 37, and the total capacity from 9 551 MW to 9 935 MW. However, until March 2011, only 9.5% of the 9 935 MW installation target had been reached. Later, the government’s evaluation found that some obstacles were hindering the project completion, such as land clearance, the developer’s financial capability, and mismatched power plant technical specifications1. Furthermore, these factors forced the government to amend the FTP-1 regulations several times to revise the project list, with the last changes stipulated by Presidential Regulation No. 193/2014 that postponed the completion of FTP-1 until 2016.

Despite the low achievement of the FTP-1 target, in 2010, Indonesia confidently launched the 2nd FTP (FTP-2), which highlighted a major contribution of renewable energy power plants from hydro 1 753 MW and geothermal 4 925 MW or 66% of total 10 047 MW target generation capacity, while the rest consisted of coal-fired power plants 3 025 MW and gas power plants 344 MW2. To ensure the delivery of the FTP-2, the government introduced a MEMR regulation, but these regulations have been revised several times, with the last regulation enacted in 2014 to add more coal-fired power plants, making the total target reached 17 428 MW that needs to be built by 2019. As of December 2020, only 2 170 MW of FTP-2 projects were commercially operated.

Those electricity development programmes show an acute problem in providing a land area for the project. Although Presidential Regulation No. 71/2006 – as well as other regulations afterwards – stated that land procurement should be cleared within a maximum of 120 days, in reality, this is not happening. Hence, Indonesia needs to ensure that there will be a thorough solution to overcome the land clearance issue. The experience of the State Asset Management Agency (Lembaga Manajemen Aset Negara or LMAN) to provide land for the toll-road project (see Chapter 4) will be a good reference should the government decide to accelerate the clean energy project.

← 1. https://www.esdm.go.id/id/media-center/arsip-berita/direktorat-jenderal-ketenagalistrikan-review-program-10000-mw-tahap-i.

← 2. https://inilah.com/news/1957390/program-listrik-10-ribu-mw-pakai-energi-terbarukan.

Differences across energy and power plans affect the clean energy investment climate

The three main energy and electricity planning documents (RUEN, RUKN, and RUPTL) use different models and assumptions to determine installed generation capacity needs leading to significant discrepancies across these documents (see Table 2.6). Slower economic and energy demand growth have also caused delays in the build-out of planned generation capacity under the RUPTL, which could further widen the gap between planned and installed capacity. These numerous inconsistencies, in turn, create confusion among investors and ultimately affect the clean energy investment climate. More co-ordination across government institutions is needed to align plans, targets and underlying projection assumptions.

A more transparent and sound RUPTL is needed to boost investment

As mentioned above, PLN is responsible for submitting their plan which includes the involvement of IPPs to get the approval from the government before they start to build power plants. However, there have been concerns over the transparency and fairness of the allocation process since it uses a bottom up process based on the input from PLN regional offices that sometimes neglect the input from potential project developers backed with a proper pre-feasibility study as a requirement to be considered in the preparation of RUPTL.

According to Electricity Law No. 30/2009 and Presidential Regulation No. 4/2016 – later revised by Presidential Regulation No. 14/2017 – PLN shall be given priority to develop power infrastructure under the following conditions:

Equally, PLN shall work with, or allow private companies (IPPs and PPUs / IO (Izin Operasi-Operation Permit Holders) to develop electricity infrastructure under the following conditions:

Despite these requirements, in practice, PLN can arbitrarily allocate the development of projects, with some projects being categorised as “unallocated” – meaning they can be undertaken either by PLN or IPPs. However, there have been inconsistencies in terms of projects being planned across RUPTLs (e.g. with projects being modified, if not erased, from one RUPTL version to another).

One Map Policy and Indonesia One Data could support a more coherent electricity planning

To address institutional co-ordination issues over spatial planning, the government established the One Map Policy through President Regulation No. 9/2016. The One Map Policy consists of a single online repository called the Geoportal One Map – which launched in 2018 – to archive and centralise various infrastructure and other sectorial spatial plans (established and managed by different line ministries) and hence, help solve Indonesia’s long-lasting issues of overlapping spatial plans and land rights (see (OECD, 2019[8]) for more details on Indonesia’s spatial planning issues). To complement the One Map Policy, the government enacted President Regulation No. 39/2019 on Indonesia One Data that requested data holders (ministries and other government institutions) to provide dynamic data based on the format and definition guided by this regulation.

This repository will allow multiple users to overlay existing infrastructure and sectoral plans. In the energy sector, the Geoportal One Map (also called Energi dan Sumber Daya Mineral / ESDM One Map) will notably include data on renewable resource potential mining areas, transmission lines, and power plant locations. In addition, MEMR is still preparing to publish the ESDM One Data which will consist of dynamic data including daily electricity production, electricity and energy price, energy export and import value, etc. Thus, the ESDM One Map and One Data provides a great opportunity for Indonesia to further integrate energy models by better linking them and verifying adequacy with actual renewable resource potential, transmission infrastructure as well as energy demand.

It would be an important step for Indonesia if the PLN electricity system planning could be integrated with the ESDM One Map and ESDM One Data to make it more transparent and reliable, which could lead to better investment decisions by stakeholders. Currently, electricity planning lacks a linkage between the potential energy resources and the market demand towards the generation, transmission and distribution lines development plan. One example of this is the Mahakam (East Kalimantan) electricity system whereby the available supply of around 200 MW could not be delivered to the new market demand since the development of transmission and distribution lines are left behind. Other examples can also be seen in the Papua region where big hydro potential around 1 000 MW exists, but there is no demand nor any plans to build transmission and distribution lines.

With the available datasets on the ESDM One Map and ESDM One Data, the government and PLN could use it to monitor and evaluate the implementation of electricity planning and progress of the project. This has occurred for example when the government and PLN assessed the price proposals from geothermal project developers. Some of the price components include availability of supporting infrastructure close to the project location, and resource potential in areas that lack supporting infrastructure or where low potential resources could lead to higher price requirements for the developer. The government and PLN evaluated this claim using the infrastructure availability data resource potential available on the ESDM One Map and ESDM One. This allowed for the agreed geothermal price to fairly reflect the real conditions of the project.

Referring to the situation mentioned above, Indonesia could usefully draw from Australia’s experience in developing the Australia Renewable Energy Mapping Infrastructure (AREMI) (see Box 2.3). Similar to the One Map, the AREMI centralises a comprehensive set of clean energy-related data and plans, such as real-time power plant performance, market demand potential, network infrastructure gap and renewable resource potential. Through integrating multiple energy data, the AREMI map greatly helped investors to identify clean energy investment opportunities and thereby helped avoid risks of stranded assets.

During the first decade of the 2000s, effective energy efficiency and renewable energy programs reduced the overall demand for centralised fossil fuel generated energy. Major investments had been made into the electricity grid based on projected ongoing growth in energy demand and in particular to enable supply at times of peak demand in rural areas. In 2014, the Australian Renewable Energy Agency (ARENA) funded a project to build an online national renewable energy mapping platform to inform investors and other stakeholders about potential Renewable Energy (RE) resources, existing electricity infrastructures and real-time electricity system performance, as well as spatial map and demographic demand information on other infrastructures.

The objective of this project – the Australian Renewable Energy Mapping Infrastructure (AREMI) – was to establish a one stop shop for renewable energy mapping data which furthermore could support the investment decision on what kind of electricity infrastructure needed to be built in a specific area, e.g. either a power plant with certain capacity and type of technology or transmission/distribution lines with certain lengths and capacity. While this map could assist the government to promote and monitor the electricity projects in various regions, it was also expected to reduce the time and costs of project preparation, and to support the analytical work by stakeholders.

In the beginning, the Australian Government appointed National Information and Communication Technology Australia (NICTA) to develop the system with support from Geoscience Australia, the Bureau of Meteorology, and the Commonwealth Scientific and Industrial Research Organisation (CSIRO). In mid-2016, Data61, under CSIRO, took over the project and continued to expand the AREMI maps that until recently had collected around 1 100 datasets consisting of electricity and renewable infrastructure, environmental data, topography, and population from various data custodians.

A further report from Data61, stated that according to the evaluation conducted by the Centre for International Economics (CIE), AREMI was attributed to generate a benefit of around AUD 11.7 million of a total AUD 47.5 million net benefit made by investors. The CIE also found the utilisation of AREMI created a benefit-cost ratio of more than 5:1 which means for every dollar spent, AUD 5 in new economic value is generated for the Australian economy in terms of time saved, improved decision making, and higher valued activities1.

← 1. AREMI decommissioning letter

Clean energy technology development and demand behaviour will reshape Indonesia’s energy landscape

Fast-changing renewable technology development and cost-decline globally will greatly influence renewable generation planning in Indonesia. Worldwide, the cost of renewable technologies has plummeted over the last decade, for example, the cost of solar photovoltaics (PV) dropped by 82% between 2010 and 2019 eventually leading to a substantial increase in the share of renewables in electricity generation (IRENA, 2020). Yet, Indonesia’s electricity sector continues to rely heavily on coal (63%) with renewables only playing a minor role (11.5%) (see Chapter 1 for more details on Indonesia’s power system fuels). Some coal-fired power plants have been in operation for over 30 years, which recently led the government to plan for the gradual replacement of around 1.6 GW of coal-fired power plants with solar PV (Jakarta Post, 2020)12.

Like other countries, Indonesia is experiencing a changing behaviour in energy consumption driven by digitalisation. It is supported by a large share of millennials and generation Z (age 8-39 years), around 53.81% of the total population of 270.2 million people (BPS, 2021)13, while the rate of Internet penetration in the country is 73% as reported in Digital 2021 Indonesia by We Are Social and Hootsuite14. Millennials are more familiar with Internet-based economic activities (digitalisation) and they also prefer to use more efficient energy technology, such as ride-sharing services (i.e. GoJek and Grab), and live near cities. In addition, the IEA Digitalisation and Energy report (2017) stated how digitalisation is reshaping the energy sector and this furthermore should encourage Indonesia to remodel its energy supply and demand projection.

References

[10] Bridle, R. et al. (2018), Missing the 23 Per Cent Target: Roadblocks to the development of renewable energy in Indonesia GSI REPORT, http://www.iisd.org/gsi (accessed on 15 January 2019).

[13] DEN (2020), Buku Bauran Energi Nasional, Dewan Energi Nasional, https://den.go.id/index.php/publikasi/index/BauranEnergi.

[2] DEN (2020), Buku Bauran Energi Nasional 2020 (National Energy Mix Book 2019), Dewan Energi Nasional, Jakarta, https://den.go.id/index.php/publikasi/index/BauranEnergi (accessed on 19 April 2021).

[6] IESR (2019), Kebutuhan Investasi Energi di Indonesia (English translation: Energy investment needs in Indonesia), http://iesr.or.id/pustaka/kebutuhan-investasi-energi-indonesia/ (accessed on 3 April 2020).

[12] Kennedy, S. (2020), Research: land use challenges for Indonesia’s transition to renewable energy, The Conversation, https://theconversation.com/research-land-use-challenges-for-indonesias-transition-to-renewable-energy-131767 (accessed on 6 November 2020).

[1] MEMR (2020), Handbook of Energy & Economy Statistics of Indonesia 2019, Ministry of Energy and Mineral Resources, Jakarta.

[7] MEMR (2020), Statistik Ketenagalistrikan 2019 (Electricity Statistics 2019), Ministry of Energy and Mineral Resources, Jakarta, https://gatrik.esdm.go.id/assets/uploads/download_index/files/c4053-statistik-2019-highres.pdf (accessed on 19 April 2021).

[4] OECD (2020), OECD Investment Policy Reviews: Indonesia 2020, OECD Investment Policy Reviews, OECD Publishing, Paris, https://dx.doi.org/10.1787/b56512da-en.

[8] OECD (2019), OECD Green Growth Policy Review of Indonesia 2019, OECD Environmental Performance Reviews, OECD Publishing, Paris, https://dx.doi.org/10.1787/1eee39bc-en.

[11] OECD (2015), Overcoming Barriers to International Investment in Clean Energy, Green Finance and Investment, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264227064-en.

[5] OECD (2015), Policy Guidance for Investment in Clean Energy Infrastructure: Expanding Access to Clean Energy for Green Growth and Development, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264212664-en.

[9] PWC (2019), As many as 21 PPAs for new and renewable energy power plants planned to be signed this year, https://www.pwc.com/id/en/media-centre/infrastructure-news/april-2019/planned-to-be-signed-this-year.html (accessed on 9 November 2020).

[3] PwC (2017), Power in Indonesia - Investment and Taxation Guide, http://www.pwc.com/id (accessed on 11 January 2019).

Notes

← 1. https://www.thejakartapost.com/news/2019/07/29/division-among-ministers-may-delay-issuance-of-ev-regulation.html.

← 2. http://www.dpr.go.id/berita/detail/id/25269/t/Peran+DEN+Belum+Optimal.

← 3. Dian Lestari, Head of Center for Climate Finance and Multilateral Policy, “Green Finance Facility to Support Clean Energy Projects in Indonesia”, Online FGD Developing a Green Finance Facility, October 2020.

← 4. https://iesr.or.id/en/pustaka/kebutuhan-investasi-energi-indonesia.

← 5. MP3EI is a development planning document stipulated by Presidential Regulation Number 32 of 2011 in the early presidency of Susilo Bambang Yudhoyono. It contained various government development programmes in six economics corridors—big islands based, e.g., Java, Sumatera, Kalimantan, Sulawesi, Papua-Maluku, and Bali-Nusa Tenggara—to accelerate the development across the country to achieve a developed country status by 2025 through some indicators, e.g., income per capita, economic growth, and GDP value. Source: https://www.bappenas.go.id/id/berita-dan-siaran-pers/kegiatan-utama/master-plan-percepatan-dan-perluasan-pembangunan-ekonomi-indonesia-mp3ei-2011-2025/.

← 6. .https://www.bps.go.id/indicator/11/104/1/-ser, i-2010-laju-pertumbuhan-pdb-seri-2010.html.

← 7. President Regulation No. 22/2017 about National General Energy Policy (RUEN).

← 8. https://den.go.id/index.php/publikasi/index/pembinaanrued.

← 9. https://www.cnbcindonesia.com/news/20200917152103-4-187563/ruu-ebt-ada-usul-badan-pengelola-energi-terbarukan-dibentuk.

← 10. https://www.adb.org/sites/default/files/publication/668226/better-regulation-future-indonesia-electricity-sector.pdf.

← 11. https://www.reuters.com/article/indonesia-electricity-idAFL4N2AY2AO.

← 12. https://www.thejakartapost.com/news/2020/11/30/ministry-mulls-retiring-giant-suralaya-coal-plant-replacing-it-with-solar-farm.html.

← 13. https://www.bps.go.id/website/materi_ind/materiBrsInd-20210121151046.pdf

← 14. https://datareportal.com/reports/digital-2021-indonesia