3. Cultural and creative jobs and skills: who, what, where, and why it matters

Cultural and creative employment accounts for up to 1 in 20 jobs in some countries, and up to 1 in 10 in some regions and cities. Cultural and creative professionals can be found in almost all sectors, helping to drive innovation across the economy. While COVID-19 put a dent in longer-term growth in cultural and creative employment, its importance is likely to continue to grow in the future. However, to unleash the full potential of the sector, addressing issues such as high rates of precariousness, persistent skills gaps, diversity and inclusion, and the digital transition will be essential.

Cultural and creative employment accounts for up to 1 in 20 jobs in some OECD and European Union (EU) countries. It is particularly important in cities and capital regions, where it can account for up to 1 in 10 jobs.

Cultural and creative professionals help to drive innovation across the wider economy. Forty percent of cultural and creative employment can be found outside of cultural and creative sectors, e.g. industrial designers working in the automotive industry. Likewise, creative skills more generally, even outside of those held by creative professionals, help to drive innovation.

In recent years, growth in cultural and creative employment has outpaced growth in overall employment in most countries (13.4% growth compared to 9.1% on average between 2011 and 2019 across OECD and EU countries), but COVID-19 made a dent. The lingering effects of the pandemic could put longer-term strains on the sector and cultural and creative professionals, who frequently transition to non-cultural and creative careers during times of economic crisis. While public support measures helped to cushion some of this blow, they were not always well-adapted to the specificities of this sector, e.g. for workers who combine standard and freelance work.

Cultural and creative jobs are, on average, also more precarious than jobs in other sectors when looking at issues such as contract stability, fluctuations in income, and access to social protection. For example, across OECD countries, 29% of cultural and creative employees are self-employed, just over twice the average rate for all workers.

Women are better represented in cultural and creative jobs than employment overall, but significant disparities exist related to seniority, pay and market access. Likewise, more can be done to increase the representation of other disadvantaged groups and to make the sector more diverse.

Cultural and creative workers tend to be more highly educated and highly skilled than the average worker. However, there are persistent skills gaps in the sector. Improving entrepreneurship skills in particular is a key priority given the high rate of self-employment in the sector.

A lower share of cultural and creative jobs are at risk of automation than jobs overall, but these jobs will be transformed by digitalisation in other ways. Cultural sectors have long been at the vanguard of digitalisation, developing new models for production and consumption that are then mainstreamed across other sectors. Going forward, addressing disparities in access to digital tools, infrastructure and skills can help to ensure the full potential of digitalisation in the sector is realised.

Policymakers, the private sector and philanthropy all have a role to play in maximising the contributions cultural and creative employment can make to drive growth, innovation and inclusion. Key actions include:

Addressing gaps in social protection coverage, and leveraging other tools to improve job quality in the sector, such as developing sector skills strategies that consider both supply and demand factors, as well as the structure of public contracts and grants.

Closing skills gaps, particularly related to entrepreneurial skills and for specific sub-sectors. Strategies include enhancing access to entrepreneurial training, coaching and mentoring programmes and developing skills strategies at the appropriate geographic scale.

Supporting the sector’s digital transition, including addressing divides in digital infrastructure, tools and skills across workers and firms.

Maximising the full potential of the synergies between cultural and creative sectors (CCS) and other sectors such as education and health. This implies a need for new professional training that combines cultural skills with those of education, nursing, medical or social services.

Strengthening the data and evidence base to better understand the strengths and challenges for the sector at a more granular level, build public awareness of the importance of the sector, and design more effective and efficient policies to support it.

Cultural and creative employment is not a niche issue – it accounts for up to 1 in 20 jobs in some countries, and up to 1 in 10 in some regions and cities. Cultural and creative professionals can be found in almost all sectors of the economy and help to drive innovation more generally. In fact, creative professionals working outside of cultural and creative sectors (CCS) account for over 40% of cultural and creative employment.

While COVID-19 put a dent in longer-term growth in cultural and creative employment, its importance is likely to continue to grow in the future. Cultural and creative jobs tend to be highly skilled, and a lower share (10%) are at high risk of automation than in the labour market more generally (14%). Digitalisation will likely lead to an uptick in the demand for cultural and creative skills, while also transforming these jobs in other ways, for example in terms of how cultural goods and services are produced and disseminated.

Despite the growing importance of these jobs, there are still underlying vulnerabilities to address. In particular, cultural and creative jobs are, on average, more precarious than other types of jobs when looking at issues such as contract stability, fluctuations in income, and access to social protection. Across OECD countries, 29% of cultural and creative employees are self-employed, just over twice the average rate for all workers. Skills shortages also hold the sector back, particularly in relation to entrepreneurship skills, for some specific sub-groups (e.g., indigenous or other marginalised groups) and related to technical skills for specific sub-sectors, such as traditional crafts.

Maximising the contributions of cultural and creative employment to drive growth, innovation and inclusion requires actions on a number of fronts. Policymakers at all levels – from local to national – as well as the philanthropic and private sector all have a role to play. Priorities include addressing high rates of precariousness in the sector, closing skills gaps, enhancing diversity, helping the sector seize the potential of digitalisation and cross-overs with other sectors, and improving data collection and analysis.

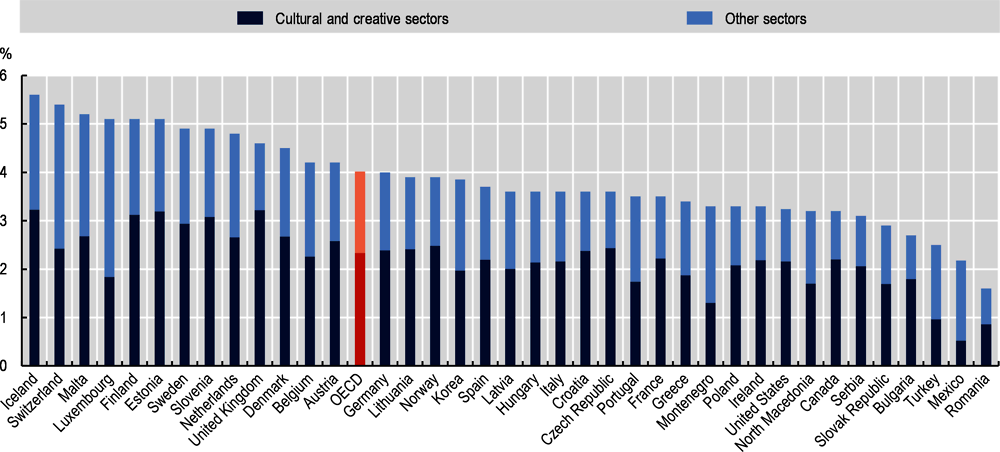

In OECD and EU countries with available data, cultural and creative employment accounts for between 1.4% and 5.7% of all employment (see Figure 3.1). Cultural and creative employment encompasses a wide range of jobs across the economy, from architects to librarians, to interior designers, video game programmers and ceramicists. Beyond the emblematic examples of musicians, actors and artists, it also includes the workers like accountants and HR advisors in the film and broadcasting industry, as well as creative professionals working outside creative sectors, such as industrial designers in the automotive industry or interpreters working in the public sector (see Box 3.1).

Across countries, academic studies and research by international organisations, many different concepts and methodologies are used to identify and measure employment in cultural and creative sectors. In general, cultural and creative employment is often underestimated in official statistics for a number of reasons. Often only activities and occupations in cultural and creative sectors are measured. However, cultural and creative workers can be employed in non-cultural and creative sectors (e.g. designers working in automotive industries). In addition, labour force surveys include a respondent’s main paid job but do not always capture secondary employment, which is highly relevant to work in CCS. It is also important to note that the sector includes high shares of volunteers or those who engage in cultural production outside of remunerated work. This accounts for a considerable share of unpaid work that is not captured by the national accounting systems. They are sometimes included in cultural participation statistics but not in employment figures.

To the degree possible, this chapter uses the “trident” approach to measuring cultural and creative employment. This approach is recommended by the European Statistical System Network on Culture (ESSnet-Culture). Further details on the industry sectors (NACE classifications) and the cultural and creative occupations (ISCO-08) included in these calculations can be found in Chapter 1, but generally this includes:

Specialist workers: cultural and creative professionals (e.g. those working in cultural and creative occupations) within cultural and creative sectors;

Support workers: non-cultural and creative professionals working in cultural and creative sectors; and

Embedded workers: creative professionals working in other sectors outside CCS.

However, to be able to draw on a wider range of statistics and research, other definitions of cultural and creative employment and cultural and creative professionals are sometimes used in this chapter. This is the case when information is not available for this grouping, or to disaggregate some of the issues raised in this chapter for different occupations or sub-sectors. This includes:

Employment from cultural and creative sectors only, using the NACE classifications described in Chapter 1 (e.g. excluding embedded cultural and creative professionals working in sectors outside of CCS);

Internationally comparable proxies for cultural and creative sectors, such as the broader NACE category of “arts, entertainment and recreation” which may be less precise but for which a broader range of data is available;

Country specific definitions of cultural and creative sectors and occupations, for example in relation to literature on trends or patterns in specific countries; and

Specific sub-categories of cultural and creative employees, whether those working specifically in CCS or specific cultural and creative occupations (e.g. visual artists).

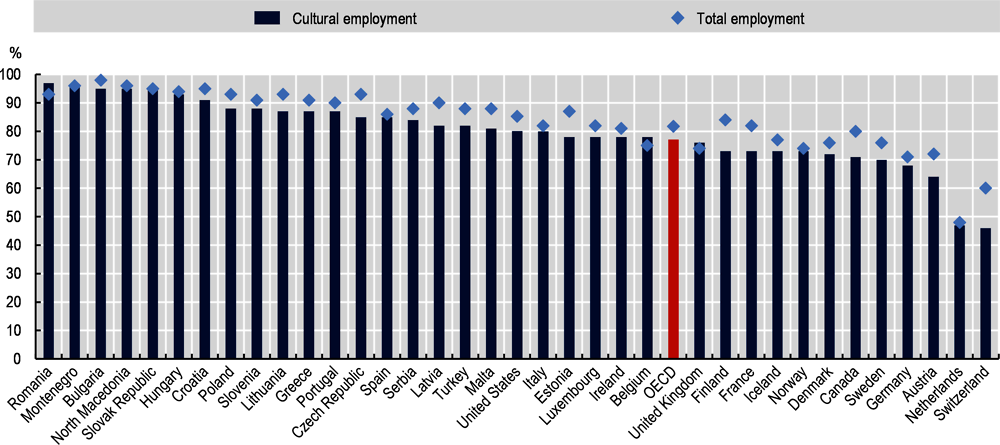

In Iceland, Switzerland, Slovenia, Malta, Estonia, Luxembourg and Finland, cultural and creative employment accounts for about one in twenty jobs. In Switzerland and Luxembourg, high shares “embedded workers” drive these relatively high rates – in both countries, 3% of more of the overall workforce are cultural and creative professionals working in other sectors. For the others, the high rates are driven more by employment in cultural and creative sectors specifically (see Box 3.2 for further descriptions of employment in these specific sectors). In contrast, shares of cultural and creative employment are lower in Bulgaria, Mexico, Romania, the Slovak Republic and Turkey, where it accounts for less than 3% of jobs.

Forward and backwards linkages in cultural supply chains mean an even larger share of overall employment. In London, for example, one study suggests that for every 4 jobs in creative industries, there is an additional 3 jobs in the broader creative supply chain and that 50% of supply chain spending by CCS falls outside of creative industries. Looking at the National Theatre in London, for example, over 200 businesses supply goods and services to maintain the premises (cleaning, electrical, etc.), support daily operations and host the public (catering, food and drink, printing) and support in-house productions (lighting technicians, set designers, etc.) (Greater London Authority, 2019[1]). Digital cultural goods, which were estimated to generate USD 66 billion of business-to-consumer (B2C) sales in 2013, also drive sales of electronic devices (tablets, smartphones, e-readers, television, DVD players) as well as high-bandwidth telecoms services (CISAC, 2015[2]).

Note: Data for Canada, Mexico, the United Kingdom, and the United States are from 2019. Data for Australia is from 2016. Regions for Serbia, Croatia, Bulgaria, Poland, Romania, and Spain are based on Nomenclature of Territorial Units for Statistics 1 (NUTS 1) while the remaining regional classifications are based on Territorial Level (TL). The minimum and maximum regional employment shares are only reported for countries with sufficient data for at least two regions.

Source: Eurostat (2021[3]) Cultural employment by NUTS 2 regions, https://ec.europa.eu/eurostat/web/culture/data/database; OECD calculations on American Community Survey, 2019, Canadian Labour Force Survey, March 2019, Mexican National Survey of Occupation and Employment, 2019 quarter 4, Australian Census, 2016, and Statistics Korea, 2020.

Looking specifically at culture and creative sectors, one estimate suggests that they account for 29.5 million jobs globally and generate annual revenues of USD 2.25 trillion (more than the telecoms or automotive sector in many economies) (EY, 2015[4]). These sectors specifically account for about 2.3% of all employment on average within the OECD, but up to 3.2% in some countries (e.g. Estonia, Iceland) (see Annex Figure 3.A.1. ). Rates can be even higher in some non-OECD countries. Other international studies show that developing countries such as Bolivia, Pakistan and Togo are among the countries with the highest share of employment in cultural and creative sectors (UNESCO/World Bank, 2021[5]).

Note: OECD average includes Australia, Austria, Belgium, Canada, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Korea, Latvia, Lithuania, Luxembourg, Mexico, the Netherlands, Norway, Poland, Portugal, the Slovak Republic, Slovenia, Spain, Sweden, Switzerland, Turkey, the United Kingdom, and the United States. Data for Canada, Mexico, the United Kingdom, and the United States are from 2019. Other professional, scientific and technical activities include specialised design activities, photographic activities and translation and interpretation activities. Data for Canada, Mexico, the United Kingdom, and the United States are from 2019.

Source: OECD calculations on Eurostat (2021[3]) Cultural employment by NUTS regions, https://ec.europa.eu/eurostat/web/culture/data/database; American Community Survey, 2019; Canadian Labour Force Survey, March 2019; Mexican National Survey of Occupation and Employment, 2019 quarter 4.

Within cultural and creative sectors, the “creative, arts and entertainment activities” sub-sector accounts for nearly one-quarter of jobs. This includes, for example, performing arts such as live theatre, concerts and opera, as well as the activities of individual artists, writers, journalists and art restoration. “Libraries, archives, museums and other cultural activities” account for another 17% of jobs on average, as do “other professional, scientific and technical activities”, which include, amongst other activities, specialised design, photography, translation and interpretation.

Source: EY (2015[4]), Cultural Times: The First Global Map of Cultural and Creative Industries; UNESCO/World Bank (2021[5]), Cities, Culture, Creativity – Leveraging Culture and Creativity for Sustainable Urban Development and Inclusive Growth, https://doi.org/10.1596/35621.

Cultural and creative jobs tend to concentrate in cities and capital regions (OECD, 2020[6]). In almost all (90%) of countries with available regional data, capital regions, which typically have a country’s largest city, have the highest shares of cultural and creative employment (see Figure 3.1). Other studies, using varying methodologies, estimate that the share of jobs in cultural and creative sectors is over 10% in cities such as Austin (US), Guangzhou (China), London (UK), Los Angeles (US), Milan (Italy), Seoul (South Korea), and Tokyo (Japan) (OECD, 2021[7]).1

London: According to the 2019 Creative Supply Chains Study, the creative industries contribute GBP 52 billion to London’s economy, and spend an estimated GBP 40 billion within their London supply chain – boosting a wide range of other sectors. London’s creative sector is also generating business activity across the United Kingdom, with case studies of eight London-based organisations showing that 40% of their suppliers are located outside of London. Employment in the creative industries was growing four times the rate of other areas of the economy. In total, 267 500 people were working in London’s creative industries in 2017, with 203 200 in creative supply chain employment – more than in the legal and accounting sectors combined.

New York: Some 15 000 cultural firms and institutions provided employment to over 231 000 people in New York City’s creative sector in 2017. In addition, over 62 000 workers in the sector are self-employed – a figure which has grown at nearly twice the rate of growth of those employed in a business or non-profit organisation. Altogether, New York City’s creative sector represents about 5.4% of private employment in the city, and 6.7% of wages paid. The creative sector accounts for 13% of total economic output. In total, one out of every eight dollars of economic activity in the city – USD 110 billion in 2017 – can be traced directly or indirectly to the sector.

Source: Greater London Authority (2019[1]), Mayor of London Creative Supply Chains Study, https://www.london.gov.uk/sites/default/files/creative_supply_chains_study_final_191011.pdf; Office of the New York City Comptroller (2019[8]), The Creative Economy: Art, Culture and Creativity in New York City, https://comptroller.nyc.gov/wp-content/uploads/documents/Creative_Economy_102519.pdf.

The concentration of cultural and creative sectors in large cities has increased in recent decades. This suggests that “success breeds success”, with CCS in large cities growing and diversifying into new sub-sectors over time (UNESCO/World Bank, 2021[5]). Research in the United States on employment in core arts industries shows that while it grew and became more diffuse across places between 1980 and 2000, in the following decade, it shrunk and reconcentrated (Grodach, 2014[9]). However, there are different patterns across countries. In the US, for example, larger metropolitan areas host more diversified creative economies than smaller urban areas. While London shows similar diversification patterns as large US metropolitan areas, the relationship between size and diversity is weaker in other UK regions (Kemeny, Nathan and O’Brien, 2019[10]).

Creative professionals are attracted to specific cities and regions for a variety of reasons. Artists have been found to be more mobile than average, with factors such as a nurturing artistic and patron community, amenities and affordable cost of living driving residential decisions (Markusen and Schrock, 2006[11]). Other research has suggested that factors such as tolerance are more important for attracting a creative workforce than the population more generally (Florida, 2014[12]; Boschma and Fritsch, 2009[13]). It has also been found that artists who enter self-employment are much more likely to live in cities with a high concentration of other artists (Woronkowicz and Noonan, 2017[14]).

On average, about 40% of cultural and creative employment can be found outside of cultural and creative sectors, i.e. the “embedded” cultural and creative professionals working across the economy. The share ranges from 30% in the United Kingdom to 64% in Luxembourg. In Australia, for example, creative workers make up over 10% of the workforce in manufacturing, wholesale trade and professional scientific and technical services (SGS Economics and Planning, 2013[15]), and design professionals can be found across 129 different industries (Cunningham, 2011[16]). Data from the United States show that specialist cultural and creative workers, i.e. cultural and creative professionals working in cultural and creative sectors, only account for just under one-fourth of all cultural and creative employment.

Note: Data for Canada, Mexico, the United Kingdom, and the United States are from 2019. Please refer to Eurostat (2018[17]) for the list of cultural and creative sectors included in the calculation.

Source: OECD calculations on Eurostat (2021[3]) Cultural Statistics, https://ec.europa.eu/eurostat/web/culture/data/database; American Community Survey, 2019; Canadian Labour Force Survey, March 2019; Mexican National Survey of Occupation and Employment, 2019 quarter 4; and Australian Census, 2016.

These “embedded creatives” help to drive innovation and competitiveness across the economy. Research on SMEs in the UK suggests that cultural and creative professionals may actually be more robust drivers of innovation than cultural and creative sectors themselves (Lee and Rodríguez-Pose, 2014[18]). Indeed, tertiary graduates in the arts play an important role in innovation, with one study finding that they are just as likely to participate in product innovation as graduates in engineering and computing (Avvisati, Jacotin and Vincent-Lancrin, 2014[19]). At the regional level, a positive relationship between a large presence of the “creative class” – which includes a broader range of workers than the definition of cultural and creative employment in this chapter2 – and growth, entrepreneurship and innovation has been documented in both the US and Europe (Boschma and Fritsch, 2009[13]; Florida, 2002[20]). However, there is significant debate as to whether this is linked to creativity specifically or just higher levels of human capital more generally (Florida, 2014[12]; Peck, 2005[21]; Glaeser, 2005[22]).

Artist-in-residence programmes, which embed artists within non-arts organizations, are another example of how the talents and expertise of cultural and creative professionals can drive innovation in other sectors (EC, 2014[23]; Stephens, 2001[24]). Used in both public and private organisations, these programmes integrate artists in university learning curricula (Stephens, 2001[24]), technology corporations (Voight, 2017[25]), and government agencies (Civic Artists Project, 2020[26]), among other types of organizations. For example, inspired by the longstanding artist-in-residence programme in the Department of Sanitation, New York City’s Public Artists in Residence program (PAIR) was launched in 2015. It matches artists with city agencies such as health, sanitation, and sustainability, so that artists can work “collaboratively” to “propose and implement creative solutions to pressing civic challenges.” Likewise, Los Angeles named oral historian and artist Alan Nakagawa as the city’s first “Creative Catalyst” to support the Department of Transportation with its Vision Zero initiative (Woronkowicz and Schert, 2020[27]).

Women are well represented in cultural and creative employment in general, but face significant barriers in terms of seniority, pay and market access

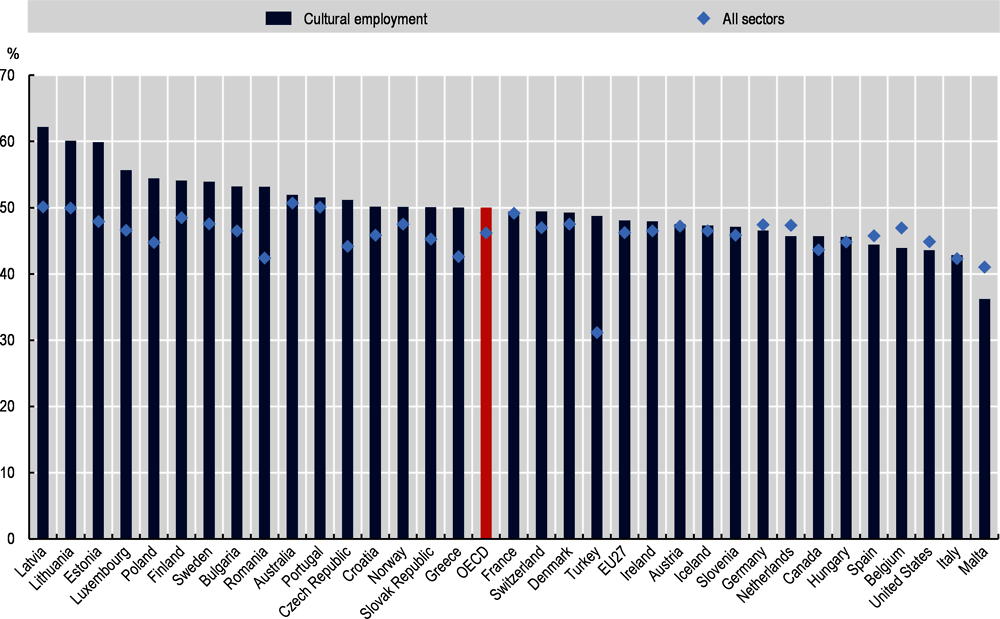

In general, women are well represented in cultural and creative employment. In 2020, the proportion of women in full-time cultural and creative employment across the OECD (50%) was slightly higher than the average share of women in employment across the whole of the economy (46%) (Figure 3.4). Only in a handful of countries are women more poorly represented in cultural and creative employment than employment overall (e.g. Belgium, Malta and the Netherlands). On the other hand, the Baltic States, as well as Luxembourg, Poland, Finland, and Sweden have particularly high shares of women in cultural and creative employment.

Note: Data for Canada and United States are from 2019. Data for Australia is for 2016 and includes both full-time and part-time workers.

Source: Eurostat (2021[3]), Cultural Employment by Sex, https://ec.europa.eu/eurostat/web/culture/data/database; Eurostat (n.d.[28]) Employment and Activity by Sex and Age – Annual Data (15-64 year-olds), https://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=lfsi_emp_a&lang=en; OECD calculations on American Community Survey, 2019, Canadian Labour Force Survey, March 2019, and Australian census, 2016.

Despite the strong representation overall, significant disparities exist at more senior levels and as well in relation to pay, access to creation and production resources, and representation in the art market (EU, 2018[29]).In the field of arts, entertainment and recreation worldwide, women make up 30% of less of senior management positions in over half of firms (ILO, 2019[30]). In the museum sector in the United States, 61% of museum staff are women, compared to only 46% of museum directors (Schonfeld and Westermann, 2018[31]). In France, women make up only 9% of directors at the 100 largest cultural enterprises, and receive only 28% of public funds given to arts and cultural producers (UNESCO, 2020[32]). Women comprised only 21% of all directors, writers, producers, executive producers, editors, and cinematographers in the top 100 grossing films of 2020 (Lauzen, 2021[33]).

Likewise, more can be done to make the sector more diverse in other ways. One study of galleries in New York City found that of the 1 300 artists represented by the city’s top 45 commercial galleries, 81% are white, 9% were African American, and only 1% were Latino (Neuendorf, 2017[34]). Other work in the United Kingdom has found that while representation of Black, Asian and ethnic minorities in cultural and creative sectors is growing, they remain underrepresented compared to the demographics of the places where these sectors are concentrated (Easton, 2015[35]). Other research from the UK suggests that those from privileged social origins (i.e. those from managerial and professional social origins) are overrepresented in cultural and creative occupations, that the rates of absolute social mobility are declining for these occupations (Brook, O’Brien and Taylor, 2018[36]), and that the class divide in creative sectors is worse than any in any other industrial sector (Carey, O’Brien and Gable, 2021[37]). Similarly, women, people of colour, and those who have large amounts of student debt who graduate with arts degrees in the US were found to be less likely to persist in arts-related careers over time (Frenette and Dowd, 2018[38]).

Cultural and creative employment has outpaced overall employment growth in recent years, but COVID-19 has likely left a dent. Public and private relief schemes played an important role in buffering these shocks, but were not always well-suited to the specificities of the sector or to support longer-term growth and resilience. While COVID-19 is unlikely to radically alter longer-term growth patterns for the sector overall, some specific occupations and sub-sectors may struggle to bounce back quickly.

Prior to COVID-19, cultural and creative employment was growing

Between 2011 and 2019, cultural and creative employment grew by 13.4%, compared to 9.1% for overall employment across OECD and EU countries (see Figure 3.5). Only in a handful of countries – including Luxembourg, Hungary, Ireland, the United States and Norway – did overall employment growth outpace cultural and creative employment growth over this period (and the latter two are the only countries where cultural and creative employment actually declined over this period). However, specific cultural and creative sub-sectors have experienced markedly different employment growth rates. In the EU-27, employment in “other professional, scientific and technical activities”, which includes specialised design activities, photographic activities and translation and interpretation activities, grew by 39% between 2011 and 2019. In contrast, printing and reproduction of recorded media; and publishing saw significant employment declines (-17% and -19% respectively).

Note: Growth rate in Panel A for Korea refers to the period, 2013 to 2019.

Considering sectoral data available across years, the OECD average in Panel B includes Austria, Belgium, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Latvia, Lithuania, Luxembourg, the Netherlands, Norway, Poland, Portugal, the Slovak Republic, Slovenia, Spain, Sweden, Switzerland, Turkey, the United Kingdom, and the United States. Other professional, scientific and technical activities include specialised design activities, photographic activities and translation and interpretation activities.

Source: OECD calculations on Eurostat (2021[3]), Cultural Employment, https://ec.europa.eu/eurostat/web/culture/data/database, American Community Survey, 2019; and Statistics Korea, 2019.

COVID-19 had hard-hitting but diverse impacts on jobs and livelihoods in the sector

Cultural and creative sectors were heavily affected by COVID-19, particularly venue-based sectors like museums, theatres, cinema, performing and live arts (OECD, 2020[6]). In comparison with 2019, in 2020, the cultural and creative employment in the EU fall by 2.6 % compared with 1.3 % reported for the total employment (Eurostat, 2021[3]). The total turnover of the sector in the EU-27 plus the United Kingdom is estimated to have fallen by over 30% (almost EUR 200 billion) between 2019 and 2020 (EY, 2021[39]). In Q2 of 2020, 36% of private sector-dependent employees in the arts, entertainment and recreation sector were on job retention schemes in selected countries, compared to 19% overall, and hours worked for employees in this sector had fallen by 42%. The only industry which saw a greater reduction in hours worked was the accommodation and food sector (OECD, 2021[40]). While initially, most of the reduction in hours worked was due to the use of job retention schemes, as the pandemic persisted, job destruction accounted for a growing share of lost working hours (see Figure 3.6).

Note: The figure reports the contribution of each category to the change in total hours. Average of EU countries (excluding Germany), Chile, Japan, Mexico, Norway, Switzerland, Turkey, the United Kingdom and the United States.

Source: OECD (2021[40]), OECD Employment Outlook 2021: Navigating the COVID-19 Crisis and Recovery, https://dx.doi.org/10.1787/5a700c4b-en.

Online job postings for cultural and creative employment decreased by over 50% in most OECD and EU countries with available data in April 2020 compared to April 2019 (Panel A in Figure 3.7). In countries such as Austria, Greece, and the United Kingdom, cultural and creative employment took particularly large hits compared to other sectors. By December 2021, job postings for cultural and creative roles were higher than April 2019 levels for some countries but had not yet recovered to April 2019 levels for other countries (Panel B in Figure 3.7).

Lockdowns and social distancing rules were clearly a large driver of job losses in CCS, but so too was the particular structure of these industries and the nature of cultural and creative work. Throughout the pandemic, government lockdowns forced many businesses to close their doors to the public. Venue-based businesses and institutions, such as museums and live music venues were often some of the last to be able to re-open to the public and typically faced restrictions in visitor numbers due to social distancing measures. The abrupt and often prolonged halting of activities in this sector caused serve loss in revenues (IDEA Consult/Goethe-Institut, 2021[41]). While this was a clear driver of job losses in the sector, the high proportion of small- and medium-sized enterprises (SMEs) and micro enterprises in CCS and the sector's reliance on freelance workers with short term or temporary contracts also contributed to its vulnerability. Smaller firms typically have low cash buffers, making them more susceptible to external shocks, and also typically have lesser flexibility to adapt to lockdown-proof business models than larger firms (OECD, 2021[42]). Moreover, non-standard forms of work are common place in cultural and creative employment and this type of employment was particularly vulnerable to job loss (OECD, 2020[43]).

Note: Cultural and creative job vacancies were identified based on the Eurostat definition of cultural and creative employment (i.e. the trident approach). Due to a lack of detailed sector data for EU countries, two-digit NACE rev. 2 codes were used.

Source: OECD calculations on Burning Glass Technologies data.

Artists and writers were particularly at risk, due to high levels of self-employment. Evidence from the European Commission shows that 44% of artists (including creative and performing artists such as visual artists, musicians, dancers, actors, film directors etc) and writers (including authors, journalists and linguists) across the EU27 were self-employed in 2018 (EC, 2020[44]). This figure was over 50% in some countries such as the Czech Republic, Germany, Italy and the Netherlands. Artists and writers typically work on a project basis, meaning they are often not covered by long-term contracts. Consequently, these types of workers were more at risk due to uncertain income streams.

However, within culture and creative sub-sectors, the impacts of COVID-19 have been extremely diverse. For museum and heritage sites, COVID-19 resulted in unprecedented closures and revenue losses. An estimated 95% of museums globally were forced to close at some point during the crisis. In a spring 2021 survey of museums and museum professionals, over one-quarter of respondents said the longer-term impacts of COVID-19 will result in downsizing staff (27%) and suspending freelance/temporary contracts (44%) (ICOM, 2020[45]). Likewise, festivals around the world were cancelled, with ripple effects throughout their large supply chains (e.g. related to infrastructure requirements such as stages, tents, catering, etc.) Moreover, COVID-19 cast longer-term uncertainty on future festival programming, which has to be defined long in advance. Within the film industry, the global box office market decreased by 72% in 2020 compared to 2019 (Motion Pictures Association, 2020[46]).

Other sub-sectors such as video games, television, radio and home entertainment actually benefitted from increased demand for home entertainment as a result of social distancing measures. For example, video game sales in North America in March 2020 were up 34% from those in March 2019, and video game hardware up by 63% (Bloomberg, 2020[47]). It is still uncertain how this trend will persist, but the crisis has clearly further boosted a sector that even before the crisis was on a long-term growth trajectory. Similarly, the global home/mobile entertainment market (i.e. content released digitally and on disc) grew by 23% in 2020 compared to 2019 (Motion Pictures Association, 2020[46]).

The long shadow of COVID-19: destruction not just of cultural and creative jobs, but cultural and creative careers?

COVID-19 could have longer-lasting impacts on cultural and creative employment in the hardest hit sub-sectors.3 The cancellation of festivals, trade fairs and other similar events where artists, writers, filmmakers, software designers etc. sell their work and conclude deals for future production means that the effect of this loss of investment will be felt over the medium, rather than short-term. An investment shock will also affect creative professionals and businesses that trade with legal rights (copyright industries, e.g. music, cinema). Artists that were unable to sell their production due to the cancellation of events will not receive any copyright revenue in the year to come and thus will have reduced funds to invest in new production (OECD, 2020[6]).

Artists tend to transition to work outside the sector during recessionary periods and may even stay outside the sector post-recession (Woronkowicz, 2015[48]). Avenues, such as multiple jobholding and self-employment opportunities do exist for helping buffer these negative effects. However, even those avenues can put undue strain on workers and likely incentivise many to find alternative careers. This leaves only those who can “afford” to sustain careers in cultural and creative work (Brook, O’Brien and Taylor, 2020[49]). Indeed, in a September 2020 survey, over one-quarter of freelance museum professionals reported that they were considering changing their career entirely (ICOM, 2020[50]).

Hard economic times can also impact the pipeline of college-educated artists going forward. Traditional arts majors graduating during or after the Great Recession were more likely to complete a double major, be self-employed, be unemployed, work longer hours, and earn less income than those graduating prior to the recession. It also negatively impacted the share of graduates in traditional arts fields, but positively impacted the share of graduates in related creative fields (Paulsen, 2021[51]).

All told, the resulting skills losses and shortages could slow the sector’s recovery, with longer-term implications. Women will likely face a disproportionate burden of these employment and career losses, particularly those who are caregivers of young children. This is due to the combination of their high representation in the sector and the disproportionate share of child and family care responsibilities they shouldered during the pandemic.

COVID-19 relief measures were not always well-suited for cultural and creative professionals and strengthening the sector over the longer-term

Emergency relief measures, such as furlough schemes and income support for the self-employed, were put in place in many countries to support workers throughout the economy. Along with the government, philanthropic and private sector organisations also implemented programmes for addressing the contraction of CCS employment as a result of the COVID-19 pandemic (OECD, 2020[52]). This includes direct grant schemes, indirect financial instruments (such as postponement of tax payment or rent exemptions), compensation or other financial support for cancelled events or projects, and other forms of non-financial support such as information services for cultural and creative workers (EC, 2020[44]).

In Europe, the European Commission put in place a range of funding mechanisms to support cultural and creative work across member states. This included a number of broad support packages to help Member States protect jobs, employees and the self-employed and to support SMEs during the crisis, alongside a number of CCS specific support measures (EC, 2022[53]). In response to the pressing need to gather in one place pertinent initiatives and information related to the CCS in the EU in response to the COVID crisis, the Creative FLIP Pilot project, co-funded by the European Union, launched the Creative Unite platform to help share challenges and solutions at the EU level in relation to the COVID-19 impact on the cultural and creative sectors (Creative FLIP, 2022[54]).

While COVID-19 support schemes tended to cover a broader range of workers than standard social protection schemes, cultural and creative professionals still fell through the cracks in some cases (OECD, 2020[6]). For example, self-employment support schemes were not always well adapted to the types of portfolio working and hybrid working that are more common for cultural and creative professions. Minimum income requirements for eligibility in some relief packages for instance, may exclude hybrid workers that derive only part of their income from freelance cultural and creative work. Relief schemes were also not always well-suited to provide income support to the sole proprietors of incorporated companies, which is the case for many creative professionals. In some cases, these professionals also do not earn incomes via salaries, but rather via dividends.

Many of the other types of support programmes have been stop-gap, where the goal has been to support workers in the CCS for the short term. Stop-gap measures have typically included grants and subsidies for CCS workers, in addition to loans. While stop-gap measures have been critical to the survival of so many individual CCS workers who have been adversely impacted by the pandemic, they are less effective at growing the sector since there is often no way to assure that workers who receive emergency aid continue working in cultural and creative jobs (UNESCO, 2020[55]), or that firms receiving aid used them to support employees rather than overhead costs.

Hardship Fund for Creative Freelancers (Creative Scotland) & The Screen Freelancers Hardship Fund (Screen Scotland)

The Scottish Government’s GBP 17 million commitment to creative freelancers is channelled through Creative Scotland and Screen Scotland Hardship Funds. The Hardship Funds were established for freelancers who have lost income from work and/or practice in the creative sector due to the pandemic, the Screen Fund specifically administering funds for those working in screen or photography. The Funds provided bursaries to those most impacted by hardship due to cancellation of work and prioritises those who have been unable to access other forms of direct support.

The fund administered £8m in grants from October 2020 and a further £9m administered in March 2021 when a new application round began. Applicants could apply for bursaries of up to GBP 2 000 and those who have previously received funding were eligible to reapply.

Newly Self-Employed Hardship Fund (Scottish Government)

The Newly Self-Employed Hardship Fund is a grant scheme set by the Scottish Government for those newly self-employed who are ineligible for the UK government Self-Employment Income Support Scheme (SEISS). It offers one-off payments of GBP 4 000 to those who do not meet the criteria required to claim SEISS for not having been self-employed for long enough or derived enough of their income through self-employment. Those who applied in the first round in 2020 also still eligible to apply in the round closing in March 2021.

Bridging Bursary Fund (Creative Scotland & Screen Scotland)

The Bridging Bursary Fund consisted of a GBP 2 million Creative Scotland Bridging Bursary Fund to help sustain freelance creative and arts professionals and a GBP 1.5 million Screen Scotland Bridging Bursary Fund for freelance or self-employed screen practitioners who had lost earnings due to the cancellation of work as a result of COVID-19.

The scheme ran in March-May 2020 with a total of 2 293 awards given to a total value of over GBP 4 million. The largest professional groups being awarded by the creative and arts fund were music and visual arts, while for screen, TV and TV development or production. Awards were given in every local authority, with the largest number of awards going to applicants in Glasgow (689, totalling over GBP 1.2 million) and Edinburgh (358, totalling over GBP 640 000).

Sustaining Creative Practice Fund (Creative Scotland)

The GBP 5 million Sustaining Creative Practice Fund was launched to support artists to continue developing new creative work that would make a significant contribution to Scotland’s recovery from COVID-19. In addition to GBP 3.5 million added to Creative Scotland’s existing open fund, the Culture Collective was launched with a total of GBP 1.5 million to support organisations employing freelance artists to work in and with communities across Scotland.

Other sector-specific funds

The Events Industry Support Fund comprised of a GBP 6 million fund providing one-off grants of GBP 10 000 to support businesses in the events industry and the self-employed (through limited company or as a sole trader) whose primary income source was the events sector in Scotland.

It should also be noted that other smaller sector-specific funds have been distributed by different organisations within the sector, including BECTU, Federation of Scottish Theatre, Equity Hardship Fund, Help Musicians UK, Musicians Union, PRS Foundation, and the Society of Authors, etc.

Source: Creative Scotland (2021[56]) Hardship Fund for Creative Freelancers, Creative Scotland, https://www.creativescotland.com/funding/archive/hardship-fund-for-creative-freelancers; Creative Scotland (2020[57]), “Business support needs of cultural organisations”, Unpublished, Creative Scotland; Find Business Support (2021[58]), Newly Self-Employed Hardship Fund, https://findbusinesssupport.gov.scot/service/funding/newly-self-employed-hardship-fund; Screen Scotland (2021[59]), Screen Hardship Fund, https://www.screen.scot/funding-and-support/funding/screen-hardship-fund; Scottish Government (2021[60]), Coronavirus (COVID-19): Culture and Creative Sector Support, https://www.gov.scot/publications/coronavirus-covid-19-culture-and-creative-sector-support/pages/self-employed-support/; Visit Scotland (2020[61]), “Events industry support fund announced”, Visit Scotland, https://www.visitscotland.org/news/2020/events-industry-support-fund-announced.

A number of features distinguish cultural and creative employment from more general employment patterns. For one, it is characterised by a relatively high share of non-standard jobs, e.g. those that are not characterised by full-time, permanent contracts (although with important nuances for specific occupations and sub-sectors). Cultural and creative employment is also marked by a skills paradox -- although cultural and creative employees are more highly educated than average, there are also significant skills gaps that hold the sector back, such as those related to entrepreneurship skills. Due to the highly-skilled and non-repetitive nature of these types of jobs, they are also unlikely to be automated but will be transformed by digitalisation in other ways. Finally, cultural and creative employment has a unique role in driving innovation across the economy. Not only have cultural and creative sectors historically been digital pioneers, but also because of the role of embedded creatives and creative skills driving innovation across economic sectors.

The “starving artist” and precariousness in cultural and creative employment

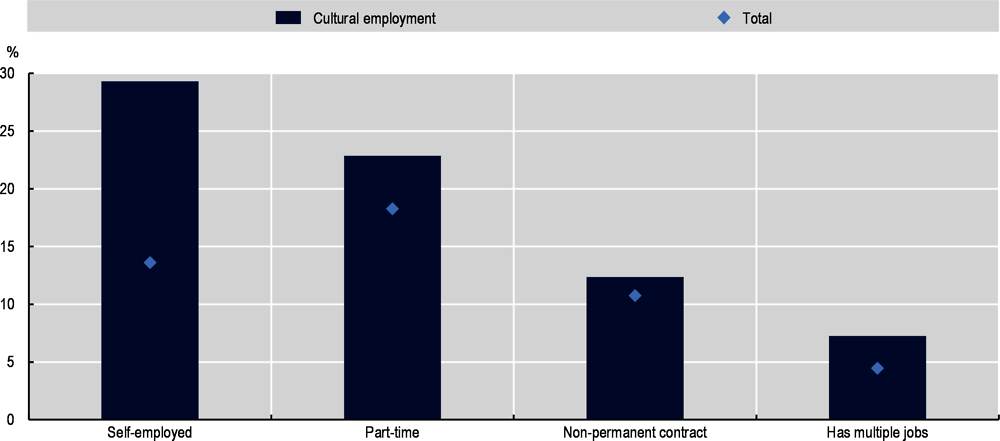

In general, cultural and creative workers are more likely to hold non-standard jobs – i.e. be self-employed, work part-time, or have temporary contracts – as well as to hold multiple jobs than other types of workers (Figure 3.8). These jobs are typically more precarious when considering issues such as contract stability, level and fluctuations of income, and access to social protection. Additionally, while informal employment in the sector is more widely spread in developing countries, even in more developed countries, informality in certain creative jobs (such as handicrafts) also exists (UNESCO, 2013[62])

Note: OECD average includes Austria, Belgium, Canada, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Latvia, Lithuania, Luxembourg, the Netherlands, Norway, Poland, Portugal, the Slovak Republic, Slovenia, Spain, Sweden, Switzerland, Turkey, the United Kingdom, and the United States. Data for Canada, the United Kingdom, and the United States are from 2019.

Source: OECD calculations on Eurostat (2021[3]), Cultural Employment Statistics, https://ec.europa.eu/eurostat/web/culture/data/database, American Community Survey, 2019, and Canadian Labour Force Survey, March 2019.

Non-standard work in the creative sector is distinctive from this type of work in other sectors. Many cultural and creative workers are highly-skilled with differentiated skills and abilities, whereas across the labour market, workers with lower levels of education tend to be overrepresented in non-standard work (OECD, 2015[63]). Creative professionals may actually be drawn to these types of working arrangements by design, as they provide more variety and novelty, as opposed to more routine, stable employment arrangements (Menger, 1999[64]). CCS workers often enter self-employment for reasons related to precarious work conditions and lack of stable jobs, compared to other types of workers who often choose to do so because of the flexibility and autonomy afforded (Feder and Woronkowicz, 2021[65]).

However, precariousness is not universal in the sector, with important divides within and across sectors and occupations, as well as across non-profit, public and for-profit models. In Germany, for example, 53% of employees in cultural and creative sectors were subject to social security contributions, but it ranges from 11% of the workforce in the art market compared to 79% in the software/games industry (Birkel et al., 2020[66]). CCS are also prone to rewarding “superstars” by concentrating income among very few individuals (Rosen, 1981[67]).

Project-based nature of work contributes to high shares of non-standard work

Much activity in CCS is project-based, leading to temporary forms of organisation and work. Both public cultural institutions and large private firms rely on an interconnected network of freelancers and micro-firms which provide cultural and creative content, goods and services. For example, directors work on individual films, often with separate production companies; theatres generally contract actors on a per-production basis, musicians perform one-off gigs, and festivals will employ people for a few months due to the seasonality of their production. Often, cultural and creative professionals (artists, writers, journalists, musicians, etc.) will have several project contracts as self-employed or a freelancer to make a living throughout the year.

Indeed, across OECD countries with available data, 29% of cultural and creative employees are self-employed, just over twice the average rate for all workers (see Figure 3.8). In some countries, the self-employed account for almost half of all cultural and creative employment (e.g. 47% in the Netherlands and 46% in Italy-see Annex 3.A). In New York City, 36% of creative workers were self-employed in 2017, compared to just 10% of the City’s overall workforce (Office of the New York City Comptroller, 2019[8]).

Project-based work is sometimes combined with a part-time salaried job, or a main salaried job (often in a non-CCS sector) combined with a “second” creative job. This practice is often referred to as “moonlighting” (Throsby and Zednik, 2011[68]; Alper and Wassall, 2006[69]). Alongside boosting earnings, having a second job can provide a degree of security for cultural and creative workers, through access to holiday and sick pay (in the case of salaried employment) and more stable income streams, compared to project-based work. However, having a second job puts time constraints on many cultural and creative workers in pursuing cultural and creative careers (EENCA, 2020[70]). Indeed, cultural and creative employees are more likely to work part-time in their main cultural and creative job – across OECD countries with data available, 23% of cultural and creative employees work part-time in their main job, compared to 18% overall (see Figure 3.8). Indeed, only established artists are able to afford to live entirely from their income as an artist (Snijders et al., 2021[71]).

Non-traditional career pathways

Many cultural and creative employees also have less traditional career pathways. Overall, creative and cultural careers are often rather fragmented with multiple entry and exit points throughout an individual’s lifetime. Longitudinal studies have also found that many people participate in the artistic labour market at some point in their working life, but few succeed to the point of being able to develop a career in the arts. Many actually transition to professional and managerial occupations, in part due to their relatively high education levels (Alper and Wassall, 2006[69]). Occupational persistence for artists is highly variable, especially when accounting for gender, age, and experience (Stohs, 1992[72]), and they are more likely to move in and out of self-employment compared to other types of workers (Woronkowicz and Noonan, 2017[14]). However, there are important nuances. In one survey of arts alumni, majoring in architecture or design increased the odds of persisting in an arts-based career over the longer term, compared to art history and several other arts-related majors (Frenette and Dowd, 2018[38]).

Even initial entry and exit from the labour market are often structured differently for creative professionals than other types of workers. For example, at the early stages of professional careers, many artists and performers produce serious work before their formal training is complete. On the other end, for some creative professionals, such as classical dancers, severe physical limitations at a relatively early age impact the longevity of their careers (Menger, 1999[64]). Likewise, artists and professionals often transition to different roles within sub-sectors, for example, from a dancer to a choreographer or a musician to a music teacher (EENCA, 2020[70]).

Cross-border mobility is especially important for cultural and creative workers in developing their careers. The ability to travel across national borders for educational, capacity-building, networking, or working purposes, forms an important component of career development for many cultural and creative workers (EENCA, 2020[70]). This is especially the case in the live performance sector, where international touring is commonplace, and for many writers and visual artists where having an international presence forms an important part of promoting a professional identity. However, this can create additional challenges for cultural and creative workers in regards to legal issues, such as visas and taxation, as well as the additional cost of travel or permanent or semi-permanent relocation, which can further entrench existing inequalities. For example, gender inequality in regards to caring responsibilities means that many female cultural and creative workers are less able to engage in mobility opportunities than their male counterparts.

In 2019, the European Commission funded the i-Portunus project as part of the Creative Europe program, to support the short-term mobility of artists and culture professionals. The i-Portunus project funds short-term mobilities for individuals to go abroad or for hosts to attract international talent. It aims to increase the opportunities for international collaborations, professional development and production-oriented residencies for artists and creative professionals, giving them access to different markets, helping them attract new audiences or followers, and start new or strengthen existing international collaborations. The scheme is open to artists, creators, cultural and creative professionals and hosts organisations (e.g. non-governmental organisations, museums, cultural institutions) working in any cultural sector (other than audio-visual) who reside in one of over 40 countries participating in the Creative Europe programme.

i-Portunus is still in a pilot phase with projects testing how to best organise the mobility scheme.

The first pilot project was launched in 2019, attracting over 3 000 applications and funding 337 individuals. The scheme was especially popular with women, young and emerging artists and people with lower incomes. The most important result was the impact that the participants attributed to their mobility experience: 97% acquired new skills/knowledge, 94% developed new audiences/outlets, 94% developed new co-productions/creations, and 49% received a job offer.

The second pilot ran from 2020 to 2021 and attracted over 1 880 applications. This second pilot granted funding to 320 individual grantees involved in 191 projects. Distributed through sector-specific calls, the i-Portunus 2020-2021 supported 96 projects from the Music sector, 50 from Cultural Heritage, 25 from Architecture and 20 from Literary Translation. Of the selected applicants, 48% had an annual income of less than EUR 10 000 and 8% of the selected applicants were unemployed.

Source: i-portunus (2021[73]), About the Programme, https://www.i-portunus.eu/. (accessed on 22 March 2022).

Reduced access to social protection

Access to social protection is also a challenge for many cultural and creative workers. This largely reflects the fact that across sectors, non-standard workers tend to have reduced access to social protection. In countries such as the Czech Republic, Estonia, Latvia, Portugal and the Slovak Republic, workers engaged in independent work, or short-duration or part-time employment are 40-50% less likely than standard employees to receive any form of income support during an out-of-work spell, with gaps particularly large for the self-employed. Even for those non-standard workers that do receive support, the level of benefits that are often markedly lower (OECD, 2019[74]). Specific features of CCS, e.g. irregular and varied types of remuneration, such as royalties, “hidden working time” that may be considered as inactivity from a traditional labour market perspective, may further exacerbate these gaps (Galian, Licata and Stern-Plaza, 2021[75]).

Some countries do have targeted social protection schemes for specific types of cultural and creative workers. Examples include the intermittent du spectacle in France or the German Artists’ Social Security Fund (OECD, 2018[76]). Likewise, Lithuania passed a social security program for artists in 2011 (UNESCO, 2012[77]), and starting in 2020, Korea introduced an employment benefits program through its Ministry of Culture, Sports and Tourism that expands access to unemployment benefits and allowances for the birth of a child for freelance artists (UNESCO, 2020[55]). While a more general scheme for the overall population, in the United States, the implementation of the Affordable Care Act disproportionately benefited CCS workers, especially those below the poverty line and young workers (Woronkowicz et al., 2019[78]).

Likewise, specific statutes or historical development have led to bespoke collective bargaining arrangements for the creative sector. For example, in the United States, following the historical example of screenwriters, other craftspeople in the film industry and related sectors have formed “guilds” that engage in multi-employer bargaining more similar to corporatist European countries than standard US practices. Other examples include Denmark, where, since 2002, unions can bargain on behalf of journalists, scenographers, and graphic designers classified as “freelance wage earners.” In 1995, Canada passed the Status of Artist Act, which allows self-employed artists to be recognised and certified by the Canadian Industrial Relations Board (CIRB) as an artists’ association with the exclusive right to negotiate collective agreements with producers, following the UNESCO Recommendation Concerning the Status of Artists (OECD, 2019[74]).

Highly educated but persistent skills gaps

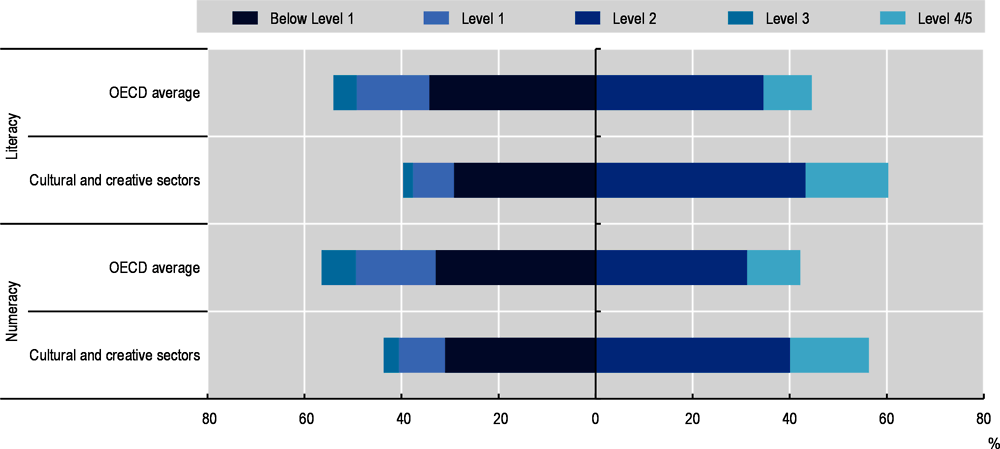

Cultural and creative workers tend to be highly educated and skilled compared to the overall workforce. On average across OECD countries, 62% of cultural and creative employees hold a tertiary degree, compared to 40% of the workforce more generally (Figure 3.9). Those working in cultural and creative sectors also have higher literacy and numeracy skills than the overall average based on the results of the OECD’s Survey of Adult Skills (PIAAC) (Figure 3.10).

Despite this general, high level of skills, there are persistent skills gaps and shortages in the sector (although evidence suggests that these are not significantly greater than for the economy overall). These impact both employers who struggle to find workers with the skills they need and creative workers themselves, particularly those in self-employment or who work freelance. Broader shifts in the sector, such as changes in business models or the uptake of digitalisation (discussed further in the next section) are also shifting the skills landscape, which may lead to increasing skills gaps and shortages. For example, a shortage of translators has been identified as a result of the expansion and internationalisation of online streaming content (although there is an ongoing debate about job quality in the sector that could contribute to a labour shortage) (Deck, 2021[79]).

Note: Education level is based on ISCED 2011. Please refer to the European Union Labour Force Survey user guide for details. Data for the United States and Canada are from 2019. OECD average is based on the OECD countries that appear in the graph

Source: Eurostat (2021[3]) Cultural Employment by Educational Attainment, https://ec.europa.eu/eurostat/web/culture/data/database; Eurostat (n.d.[80]), Employment by Educational Attainment Level – Annual Data (15-64 year--olds), https://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=lfsi_educ_a&lang=en; American Community Survey, 2019; Canadian Labour Force Survey, March 2019.

Note: Cultural and creative sectors in this figure are based on ISIC Rev. 2, 2-digit codes. Available cultural and creative sectors include: Printing and reproduction of recorded media (18); Publishing activities (58); Motion picture, video and television programme production, sound recording and music publishing activities (59); Programming and broadcasting activities (60); Creative, arts and entertainment activities (90); and Libraries, archives, museums and other cultural activities (91). Data bars may not sum exactly to 100% due to missing responses (OECD, 2019[81]). Countries included: Australia, Austria, Canada, Chile, the Czech Republic, Denmark, England (United Kingdom), Estonia, Finland, Flanders (Belgium), France, Germany, Greece, Hungary, Ireland, Israel, Italy, Japan, Korea, Lithuania, Mexico, the Netherlands, New Zealand, Northern Ireland (United Kingdom), Norway, Poland, the Slovak Republic, Slovenia, Spain, Sweden and the United States.

Source: OECD calculations on OECD (2012[82]; 2015[83]; 2018[84]) Survey of Adult Skills (PIAAC), https://www.oecd.org/skills/piaac/.

Soft skills, technical skills and managerial/entrepreneurial skills are all required for cultural and creative work, but technical and managerial skills gaps are particularly prevalent in CCS. In regards to specific skills needs, a recent study of CCS in Europe found technical and managerial skills gaps were pervasive across CCS, alongside some gaps in soft skills (VVA, 2021[85]). Much cultural and creative work requires very specific technical skills, for example, a Goldsmith or jewellery maker requires both metal craftsmanship skills and the ability to use and operate different digital tools (such as CAD/CAM, 3D modelling, 3D printing etc). Skills gaps were often found in these more technical domains, which require very specific training. Moreover, the report identified significant skills gaps in managerial/entrepreneurial skills such as marketing, project management and negotiation.

However, there are important distinctions by sub-sector. For example, in the UK, employers report the hardest time recruiting people with relevant skills for those in crafts; IT, software and computer services; and architecture, while skills gaps (i.e. mismatch between skills of the current workforce and the skills needed) are largest for museums, galleries and libraries; and businesses in IT, and advertising and marketing (Giles, Spilsbury and Carey, 2020[86]). There are also concerns about emerging challenges in “master crafts” as the existing workforce ages and eventually retires (Bowes et al., 2018[87]).

There is also evidence to suggest that skills gaps and shortages are larger for generic, transferrable skills (e.g. time or people management, or customer service), than specialist, creative skills (Bowes et al., 2018[87]). In one study, one-third of employers reported skills gaps, with business marketing and communications skills (53.1%), problem-solving skills (47.1%), vocational; skills relating to business support occupations (45.0%), fundraising skills (43.8%), and social media skills (40.0%) as the largest challenges (VVA, 2021[85]). These shortcomings tend to be greater for high-skilled roles (Giles, Spilsbury and Carey, 2020[86]), and finding senior leaders who have both a creative background and leadership skills has been identified as a particular challenge (Bowes et al., 2018[87]).

Gaps in entrepreneurial skills are particularly problematic given the high rates of self-employment in the sector. As discussed in Chapter 4, entrepreneurship and business skills are particularly important for CCS, given the high number of self-employed and freelance workers in these sectors. Moreover, these skills gaps are also prevalent across CCS businesses and not-for-profit organisations.

Again, there are important nuances. Workers in subsectors such as design, architecture, even theatre, often have the entrepreneurial training (or experience) they need to build careers. In comparison, in other subsectors, like traditional crafts, there is less professionalization and many need further training and support to understand how to successfully commodify their work. Other work on entrepreneurship more generally points to the need to close gaps in entrepreneurship skills for specific populations, such as indigenous populations, ethnic minorities and women (OECD/EC, 2021[88]; OECD, 2019[89]).

Not likely to be automated, but will be transformed by digitalisation

Overall, cultural and creative jobs have a lower risk of automation than jobs overall. Analysis of PIAAC data shows that 10% of cultural and creative jobs across the OECD are at high risk of automation, compared to 14% of jobs overall (based on the estimate and methodology in Nedelkoska and Quintini (2018[90])). This aligns with other analysis that shows that creative jobs are more “future-proof” to automation, and that the further digitalisation of the economy may actually lead to further demand for creative skills (Bakhshi, Frey and Osborne, 2015[91]). However, digitalisation will transform these jobs in other ways.

Cultural and creative sectors have long been at the vanguard of experimenting with innovative models of digital production and distribution. For example, with the release of the transistor radio in the 1950s, Sony helped revolutionise how people listened to music (Transistorized, 1999[92]), and in 1975, Steve Sasson, an engineer at Kodak invented the first digital camera (Estrin, 2015[93]). The transistor radio helped fuel the rock and roll movement in the 1950s and 1960s by enabling easy access to popular music for audiences, while the invention of the digital camera made photography accessible to the masses, blurring the line between amateurs and professionals.

Digitalisation continues to rapidly transform how creative firms and workers produce and disseminate goods and services, as well as how end users consume them. Digitalisation has contributed to a democratisation of cultural participation and production, which has made creating, sharing and collaborating on artistic endeavours more affordable and accessible (Swerdlow, 2008[94]; Kulesz, 2020[95]). Anyone with Internet access can now try their hand at producing creative work as a result lowering the entry barriers to careers in the CCS. Creating art through digital means and sharing it through social media platforms is nearly ubiquitous among young people (Swerdlow, 2008[94]). Digitalisation in CCS has also made it easier to experiment, since the costs of producing creative products through digital means are generally much lower than using non-digital means and allows users to edit for perfection. Collaboration among CCS workers is also much easier using digital technologies (Kulesz, 2020[95]). Artists and creative workers can broaden their portfolios by expanding their skillsets in different creative technologies, which in turn has made it far easier to become a multi-disciplinary creative worker (Martel, Page and Schmuki, 2018[96]).

The COVID-19 pandemic has accelerated digitalisation even further, as workers, organisations, and audiences have had to adapt to new ways of engaging with culture and creativity due to lockdowns and social distancing guidelines. For example, there was a stark increase in the demand for online content, which has benefited streaming platforms for music, cinema and television. Many cultural institutions such as museums and theatres also rapidly expanded efforts to digitise and provide online access, albeit not necessarily as a revenue-generating mechanism. This will likely bring about permanent changes in audience engagement and content provision models, creating new opportunities for innovation and growth going forward. However, digital access does not replace a live cultural experience or all the jobs that go with it, and questions remain about how revenues from streaming platforms are shared.

Accordingly, digitalisation is both an opportunity and a challenge for workers in the sector. Digital skills, tools and infrastructure are unequally distributed among firms and workers, as well as consumers of CCS products, creating and perpetuating structural inequities among producers and consumers. Promoting policies that provide widespread broadband internet access to the general public is the first step in levelling the digital CCS playing field. A second step is to make accessible to CCS workers and firms tools for digital creative production, many of which are cost-prohibitive especially for small and mid-sized firms and early-career workers. Partnerships between the public sector and technology companies could help facilitate digital access in the CCS, such as they do in other sectors (Kokalitcheva and Fried, 2020[97]). Upgrading the digital skills of workers and firms in the sector is also crucial. There are also serious complications with broadening digital access in the production of cultural and creative works, mainly concerning the ownership of cultural and creative products and remuneration for digital content.

Cultural and creative jobs and creative skills drive innovation across the economy

CCS drive innovation across the economy. Cultural and creative sectors produce a multitude of new products and services, and they are also important suppliers of ideas and new approaches for other activities (see Chapter 4 for further discussion). Arts and culture are increasingly recognised as part of a wider innovation system though cross-innovation in other sectors, including through “embedded creatives” and spillovers of innovations developed in CCS to other sectors (Crossick and Kaszynska, 2016[98]). An example of such innovation is the capacity to engage audiences (consumers) in the co-production/co-creation of content, for example when users (creative enterprises, other businesses and consumers) engage with the innovation process, especially in video games, music and design.

Creative skills more generally are also crucial for innovation, beyond the direct contributions of CCS and cultural and creative professionals. Creativity and critical thinking have been identified as the most important skills distinguishing “innovators” from “non-innovators” (Vincent-Lancrin et al., 2019[99]). Indeed, creative practices are being integrated into non-creative learning environments for the purpose of training individuals to use creativity in other realms. For example, the STEM (Science, Technology, Engineering and Mathematics) to STEAM (Science, Technology, Engineering, Arts and Mathematics) movement has gained steam in education circles and focuses on integrating divergent thinking skills among skillsets typically taught in STEM curricula, such as critical thinking and problem-solving (Sousa and Pilecki, 2013[100]). The advent of design thinking outside of design fields, including in public policy, is another example.

Maximising the contributions of cultural and creative employment to drive growth, innovation and inclusion requires actions on a number of fronts. Policymakers at all levels – from local to national – as well as the philanthropic and private sector all have a role to play. Key priorities include addressing high rates of precariousness in the sector; closing skills gaps; enhancing diversity; creating the enabling conditions for the sector to seize the potential of digitalisation and cross-overs with other sectors; and improving data collection and analysis to underpin all of this work.

Addressing high rates of precariousness and gaps in social protection coverage

Particularly in light of the increased visibility of “gig workers”, job quality more generally is an increasingly important topic in public discourse and policy debates. As evidenced by the European Council adopting the Recommendation “Access to social protection for all” in 2019, the question of social protection for non-standard workers is an area of policy action. COVID-19 brought even further attention to these questions and catalysed the extension of social protection through temporary emergency measures to previously non-covered groups in many countries, providing models for what more general schemes could entail (OECD/EC, 2021[88]).

These questions are particularly relevant for cultural and creative sectors, given the high rates of non-standard work and the stark divides within the sector. Beyond cultural and creative professionals themselves, considering job quality for support workers in culture and creative sectors is an important related issue, from security guards in museums to food service workers in theatres.

As part of general considerations around strengthening and expanding social protection schemes, the specificities of cultural and creative workers should be taken into account. This includes, for example, how social protection coverage interacts with the tendency to “moonlight” and the portability of benefits linked to frequent transitions in and out of the sector. Depending on national contexts, these issues could be addressed through more general social protection schemes, or through specialised schemes targeted specifically to the sector. While regional and local governments in many countries stepped in to provide emergency financial support to cultural and creative workers as part of COVID-19 emergency schemes, in most countries, filling these gaps over the long-term requires action at the national level, where core competencies for social protection schemes are typically held.

There are also other levers policymakers can use to improve job quality in the sector. Depending on relevant legal and regulatory frameworks, financial support, for example through grants, or procurement contracts can stipulate a certain level of working conditions or employment contract modalities, or require a commitment to providing high-quality training or apprenticeships. Other aspects of grant funding and procurement can also impact job quality. For example, longer-term more stable funding arrangements can encourage hiring of employees on longer-term contracts, rather than short-term or project-based work.

Skills strategies (see following section) can take a sectoral approach that considers skills demand, such as work organisation and skills utilisation, not just skills supply questions. Career pathways approaches within such strategies can also help to ensure quality progression opportunities over time. Related, while volunteers are a vital resource for the sector and an important dimension of cultural participation, developing shared standards for voluntary work can also help to ensure that they are not merely a lower cost alternative to paid employment or an implied “rite of passage” for new cultural and creative professionals entering the sector.

Closing skills gaps

Although cultural and creative employees have higher education and skills levels on average, important skills gaps remain. Specifically, digital and entrepreneurial skills, which are particularly important due to the rates of self-employment and micro-enterprises in the sector as well as more technical skills gaps in specific sub-sectors, such as traditional crafts.

Several strategies can be used to boost entrepreneurial skills of creative workers, including enhanced training, coaching and mentoring (see also Chapter 4). This includes better integrating entrepreneurship-related curriculum as part of initial arts and culture education and training programmes, for example in universities and vocational institutions, as well as expanding access to entrepreneurship training programmes as part of lifelong learning and business development support programmes. In some cases, these may need to be specifically tailored to address the unique business models and economic considerations in the sector. Mentoring and coaching, which support the development of entrepreneurial skills through more personal relationships, are another strategy that has proven to be effective. Business consultancy services are another model for transferring expert knowledge from a consultant to an entrepreneur in a bespoke way. Often, these latter types of support are offered through integrated support packages for business development, including financing. This type of “packaging” can be more effective than relying on a single, narrowly defined support instrument (OECD, 2014[101]).

To address skills gaps in specific sub-sectors or places, more comprehensive sector-based skills strategies may be needed. Such strategies should be built on robust analysis of current and future skills needs and gaps, developed in close cooperation with sector representatives. This may look different than typical employer engagement strategies for other sectors, given the high shares of freelancers and self-employed in CCS.

Attention is also needed for the appropriate scale of these strategies. Regional or local skills strategies, that bring together local authorities, education and training organisations, employment services, and employers are particularly important when these sub-sectors are strongly embedded in local communities and are unlikely to delocalise. In other cases, the national level may be the more appropriate scale when the sub-sector encompasses a high share of jobs performed remotely or with significant labour mobility (for example, related to the interpreter talent pool).