copy the linklink copied!Chapter 3. Are funded pensions well designed to adapt to non-standard forms of work?

This chapter looks at the design features of funded pension arrangements to see how they may affect participation, contributions and pension outcomes of different categories of workers. The purpose is to determine whether their design is well adapted to the situation of workers in non-standard forms of work to help them save for retirement.

copy the linklink copied!Introduction

This chapter considers the situation of workers in non-standard forms of work with respect to funded pension systems, continuing with the topic addressed in Chapter 2. Given that workers not in a full-time permanent employment relationship sometimes have more limited access to pay-as-you-go (PAYG) pensions and build up lower entitlements, supplementary funded pension arrangements could be one solution to improve their retirement prospects. This would require, however, that the design of funded pension arrangements suits the specific needs and circumstances of these workers to help them complement their retirement income.

This chapter analyses whether the design of funded pension arrangements is well adapted to the situation of workers in non-standard forms of work to help them save for retirement. It looks at the design features of funded pension arrangements to see how they may affect participation, contributions and pension outcomes of different categories of workers.1 This analysis is part of the OECD study on “The role of funded pensions in providing retirement income to people in non-standard forms of work”, which aims at shedding light on the current access to funded pensions of different categories of workers in non-standard forms of work, and assessing different approaches to increasing coverage and contribution levels.2

Workers in non-standard forms of work have more limited access to, and lower pension income prospects from, funded pension arrangements than full-time permanent employees. Self-employed workers participate less in funded pensions than employees do when funded pension systems are organised mostly through occupational plans, to which the self-employed usually lack access. Some countries require lower contribution levels from the self-employed or do not allow them to save as much as employees in funded pensions, thereby reducing their future potential retirement income. Part-time and temporary employees also participate less in funded pensions than full-time permanent employees do. They indeed have worse access to occupational pension plans when a minimum income, a minimum number of working hours or a minimum length of employment is required to be able to join a plan. In addition, vesting periods and the limited portability of occupational pension rights and assets affect the pension income outcomes of workers switching jobs frequently, in particular temporary employees. Finally, the possibility of accessing funds before the age of retirement may remove a barrier for participating for workers with unstable and fluctuating earnings, but raises issues of retirement income adequacy.

As a response to the growing workforce in non-standard forms of work, some countries should improve the design of funded pension arrangements and align it further with the OECD Core Principles of Private Pension Regulation in order to offer these workers the possibility of saving in complementary pension plans. Policy makers should aim to prevent exclusion from plan participation for workers in non-standard forms of work, limiting the use, or eliminating, eligibility criteria based on salary, working hours, length of employment and type of contract. Access to personal pension plans should not discriminate between different types of workers. In addition, vesting periods should be minimised to allow workers to accrue entitlements as early as possible. Countries should also facilitate the portability of pension rights and assets upon changing jobs.

This chapter is structured as follows. Section 2 analyses the formal and effective access to funded pensions of different categories of workers. Section 3 looks at differences across workers with respect to contribution rates, contribution caps, and the possibility to suspend the payment of contributions. Section 4 analyses design features of funded pensions that may influence pension income outcomes differently across various categories of workers. Finally, Section 5 concludes.

copy the linklink copied!Formal and effective access to funded pensions

The combination of different formal access and eligibility criteria results in different effective access to funded pensions for various categories of workers. The extent to which different categories of workers can access to funded pension arrangements may affect their capacity to accumulate enough resources to finance their retirement and thereby to avoid a large fall in their standard of living when retiring. This section therefore first describes the current formal access of different categories of workers to funded pensions. It then provides details on the different eligibility criteria that workers need to fulfil in order to effectively join funded pensions. It ends with statistics on effective participation rates by types of workers for countries with available data.

Formal access

Formal access of different categories of workers to funded pensions depends first on the structure of the funded pension system. Formal access indeed varies whether the funded pension system is occupational or personal. An individual can join an occupational pension plan only if there is an employment or professional relationship between that individual and the entity that establishes the plan (the plan sponsor). Employers or groups thereof, as well as labour or professional associations (e.g. self-employed professionals) may establish occupational plans, jointly or separately. By contrast, access to personal pension plans does not have to be linked to an employment relationship. A pension fund or a financial institution acting as pension provider directly establishes and administers the plans. In addition, within occupational and personal systems, participation of employers and/or employees may be mandatory or voluntary. This affects the actual participation level, or effective access, to funded pensions of different types of workers, which will be analysed later.

Access to funded pension plans for different types of workers varies across countries. Table 3.1 presents a summary of the extent to which different types of workers have access to occupational and personal pension plans in OECD and selected non-OECD G20 countries. The access of a category of workers to a particular type of plan is qualified as “Full” in Table 3.1 when all workers of that category can or have to join the plan. The access is qualified as “Partial” when there are eligibility criteria limiting the possibility of certain workers in the respective category to join the plan, such as thresholds on earnings or number of working hours. For example, in the second row (quasi-mandatory occupational pension systems) and third column (temporary employees), the cell indicates “Full” for Denmark and Sweden as all employees are covered by collective agreements, including those with temporary contracts. By contrast, for the Netherlands, the cell indicates “Partial” because some types of seasonal employees (such as agricultural) are exempt from accumulating occupational pension entitlements. Finally, certain types of plans are not available (“NA”) to certain categories of workers.

While employees always have access (fully or partially) to mandatory or quasi-mandatory occupational pension plans, access by the self-employed varies across countries. In mandatory occupational pension systems, the law mandates employers to set up and participate in a plan, and all eligible employees have to join that plan. The mandate to join an occupational pension plan is extended to the self-employed in Iceland, but not in Australia, Norway and Switzerland.3 However, in Australia, contractors paid fully or principally for their labour are considered as employees for pension purposes and entitled to mandatory superannuation contributions by the employer. In Switzerland, the self-employed can usually join profession-wide arrangements, the pension institution established for their employees, or the Substitute Occupational Benefit Institution on a voluntary basis. In addition, in some countries, the mandate on employers to establish pension plans for their employees comes from industry-wide or nation-wide collective bargaining agreements. As such agreements may not cover all sectors, these systems are classified as quasi-mandatory. Participation is mandatory for all employees to whom the collective agreement creating the plan applies. Occupational pension plans under profession-wide agreements for the self-employed can be set up in Denmark and the Netherlands; they are rare in Sweden.

Access to voluntary occupational pension plans is usually restricted to employees as it commonly depends on whether employers establish such plans for their employees. In voluntary occupational pension systems, employers can freely decide whether to establish a pension plan for all or part of their employees. In most cases, participation is also voluntary for eligible employees. There are exceptions in Belgium, France, Japan (employee’s pension funds), Luxembourg and South Africa, where employees fitting the eligibility criteria must join the plan set up by their employer. In Canada, Germany and Ireland, the mandatory or voluntary nature of employees’ participation depends on plan rules.4

Self-employed workers are usually not covered by voluntary occupational pension plans, as they do not have an employer setting one up for them. In some countries, however, profession-wide associations of self-employed workers may establish, on a voluntary basis, an occupational pension plan for their members. This is the case in Greece, Italy, Norway, Portugal, and Brazil.5

Alternative options are available in the workplace to employees not covered by a voluntary occupational pension plan in Germany and Ireland. In Germany, employees who are compulsorily covered by the social security pension scheme can require their employer to deduct part of their salary and contribute it to an occupational pension plan (co-called “salary conversion”). In Ireland, all employers are required to enter into a contract with a Personal Retirement Savings Accounts (PRSA) provider to allow all employees not covered by an occupational pension plan access to at least one standard PRSA.

While the automatic enrolment of individuals into a pension plan usually targets employees, the plan itself may be accessible to the self-employed as well. In most automatic enrolment systems, employers enrol their employees automatically into a pension plan. Participation from employees is still voluntary as they can opt out of the plan. In New Zealand (KiwiSaver), Poland (Employee Capital Plans, PPK), Turkey and the United Kingdom, employers are required to offer access to a pension plan (either occupational or personal) and to enrol their employees automatically into that plan. In Canada (Pooled Registered Pension Plans) and the United States, employers can voluntarily offer a pension plan with an automatic enrolment feature. In addition, in Canada, New Zealand and the United Kingdom, the self-employed can voluntarily join the system by contracting directly with a plan provider.6 In Lithuania, all workers younger than 40, irrespective of their employment status, are automatically enrolled into a pension fund by a public entity, with the possibility to opt out.

Mandatory personal pension plans cover both employees and self-employed workers (fully or partially) in most countries. In mandatory personal pension systems, the law mandates individuals to join a plan. This obligation covers all workers in Estonia, Israel, Latvia, Sweden and China. In Chile, among self-employed workers, only those issuing invoices have the obligation to contribute to a pension plan. The self-employed are exempt from mandatory contributions to personal pension plans in Denmark (ATP), Mexico and Indonesia. In Denmark, however, self-employed workers who have been in the ATP scheme as employees for at least three years can remain members and contribute voluntarily into the scheme. In the same way, in Mexico, self-employed workers who have been in the formal system can continue making voluntary contributions to the mandatory scheme of the Social Security Institute.

In all countries, all workers have access to, and can open, a voluntary personal pension plan by contracting directly with a pension provider. Participation is voluntary for individuals. Access to these plans is usually granted to labour income earners only, but in some countries, individuals without earnings (e.g. Chile, Germany) and even children (e.g. Chile, the Czech Republic, New Zealand) can access them. Individuals can usually choose the level and regularity of contributions. By contrast, in Japan (national pension funds), Portugal (public funded scheme), the Slovak Republic (second pillar pension funds) and India (APY and PM-SYM schemes), plan rules define the level and regularity of contributions into voluntary personal plans.

Some countries provide different types of voluntary personal pension plans to different types of workers. For example, in Belgium, France and Japan, self-employed workers have access to specific plans that employees usually cannot join.7 8 This may be to compensate for the existence of pension plans that only employees can join, in particular occupational ones. In India, the PM-SYM scheme is dedicated to informal workers (so-called unorganised workers).

Eligibility criteria

Some plans establish eligibility criteria to limit the population effectively allowed to join. These criteria include minimum income thresholds, minimum number of working hours and minimum length of employment. Legislation may provide minimum standards for eligibility, meaning that, once the thresholds are met, workers can have access to the plans. Employers and providers may still, however, offer pension plans to workers who have not met the thresholds (e.g. Canada, the United States).

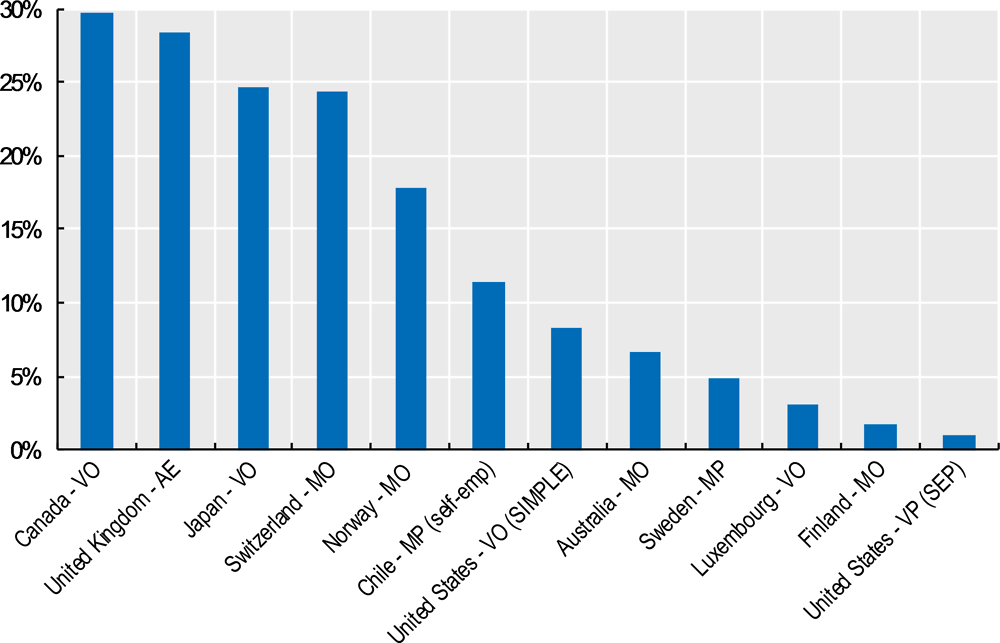

Minimum income thresholds restrict access to funded pension plans by low-income earners. This may have a larger effect on part-time employees, as they may find it harder to reach the threshold given their lower number of hours worked with a given employer. Figure 3.1 shows that the thresholds that workers’ income should exceed in order to be eligible to join a pension plan represent 25% to 30% of the average wage in the economy in Switzerland, Japan, the United Kingdom and Canada. They represent less than 5% of the average wage in Sweden, Luxembourg and Finland.9 In the United States, employers offering a retirement plan (e.g. SIMPLE or SEP) must cover employees receiving compensations above certain thresholds, although they are free to offer the plans to employees who do not meet those earnings thresholds. By contrast, India has a maximum income threshold for the PM-SYM scheme, in which only unorganised workers with a monthly income up to INR 15 000 are eligible to participate. Other countries do not apply income thresholds.

Notes: Average annual wages per full-time and full-year equivalent employee. Pension systems are classified between occupational (mandatory “MO”, quasi-mandatory “QMO” and voluntary “VO”), personal (mandatory “MP” and voluntary “VP”) and automatic enrolment (in personal or occupational plans, “AE”). For the United States, “SEP” means Simplified Employee Pension and “SIMPLE” means Savings Incentive Match Plans for Employees. The limits represent the maximum income that employers can require before joining a funded pension plan.

Source: Calculations based on the OECD Average annual wages database.

Minimum income thresholds can be designed in such a way that part-time employees are not at a disadvantage. In the Netherlands for example, the number of working hours does not penalise part-time employees when there is an income threshold established to join an occupational pension plan. This is because the salary of a part-time employee is converted into the salary that would be earned at the full-time rate of employment before the application of the threshold.

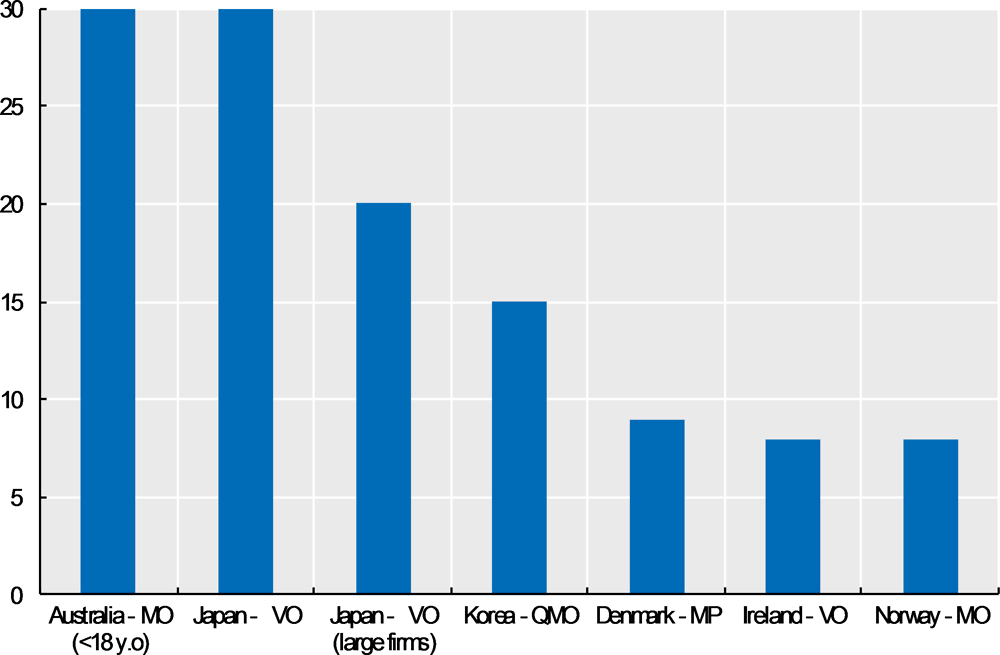

Establishing a minimum number of working hours to be able to join a plan excludes some part-time employees from the eligible population of funded pension plans. This is more common in occupational pension systems, as shown in Figure 3.2. In Australia, in addition to the monthly non-uprated earnings threshold that applies to all workers, those younger than 18 or working as a private or domestic worker (such as a nanny or housekeeper) need to work at least 30 hours per week to be entitled to mandatory employer contributions into the superannuation system. In Japan, voluntary occupational pension plans require 75% of full-time working hours, although for large firms (with 501 and more employees) the requirement is reduced to 20 hours a week if the employee (excluding students) receives a monthly pay of at least JPY 88 000 and can expect to work continuously for at least one year. In Denmark, Ireland and Norway, between 8 and 9 working hours per week are necessary to be eligible to join a pension plan.10 Other countries do not apply thresholds on the number of working hours.

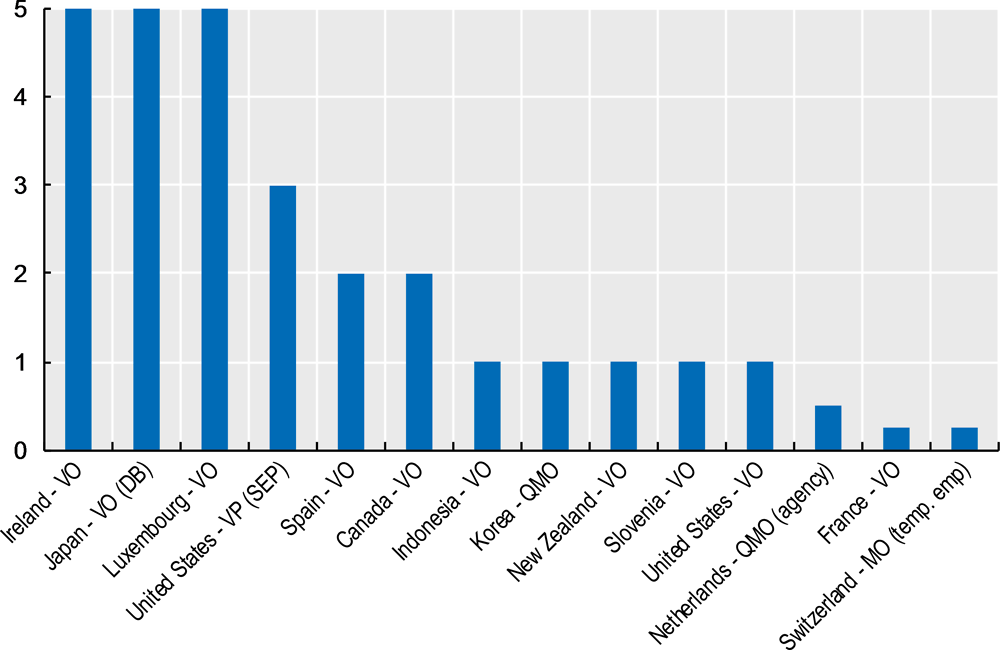

Finally, minimum length of employment or contract duration requirements may also restrict access to occupational pension plans by temporary employees. Employees may not be allowed to join an occupational pension plan from the first day of employment. This may penalise temporary employees the most as their contract duration may be shorter than the qualifying period. Figure 3.3 shows that the minimum length of employment required before joining an occupational pension plan varies from 13 weeks in Switzerland (for temporary employees) to 5 years in Ireland, Japan (DB) and Luxembourg. These are maximum limits. In Japan for example, normal practice is three years and some companies allow new employees to join the plan immediately. Five countries use a minimum length of employment of one year. In the United States, one year of employment would normally be required in an occupational plan. However, a traditional 401(k) plan may require two years of employment for eligibility to receive an employer contribution if the plan provides for immediate vesting. In addition, in Norway, seasonal workers must be covered by a mandatory occupational pension plan only if they work at least 20% of full-year employment. Other countries do not require minimum length of employment or contract duration, or do not have legal rules.

Notes: When the requirement is expressed as a percentage of full-time working hours (Ireland, Japan and Norway), the calculations assume that a full-time job requires 40 hours of work per week to get a number of hours. Pension systems are classified between occupational (mandatory “MO”, quasi-mandatory “QMO” and voluntary “VO”), personal (mandatory “MP” and voluntary “VP”) and automatic enrolment (in personal or occupational plans, “AE”).

Notes: Pension systems are classified between occupational (mandatory “MO”, quasi-mandatory “QMO” and voluntary “VO”), personal (mandatory “MP” and voluntary “VP”) and automatic enrolment (in personal or occupational plans, “AE”). For the United States, “SEP” means Simplified Employee Pension. Employees must be included in the SEP plan if they have worked for the employer in at least 3 of the last 5 years. For the Netherlands, the information refers to temporary agency workers. For Switzerland, the information refers to temporary employees.

Effective access

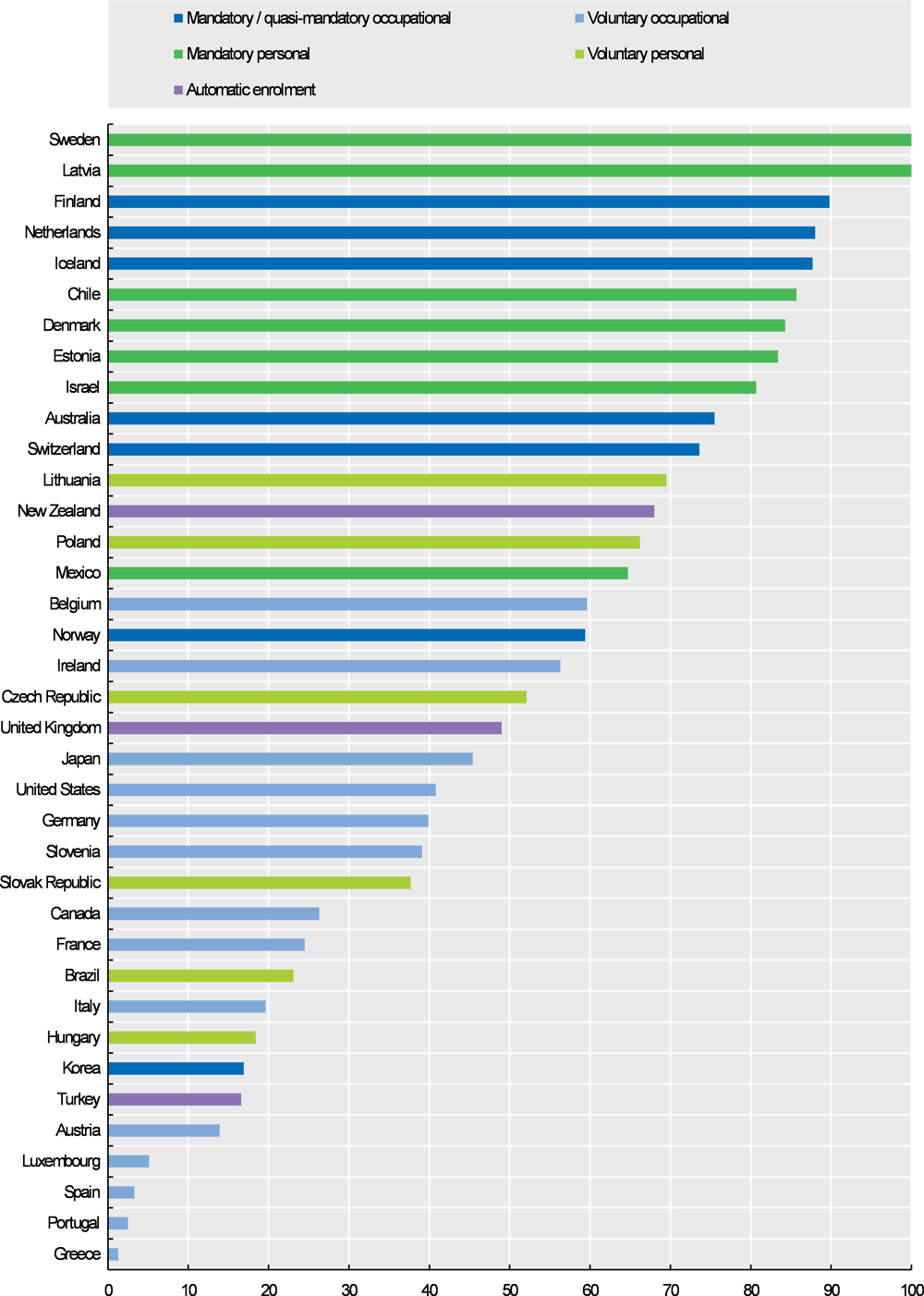

Mandatory and quasi-mandatory pension systems usually achieve higher overall participation rates than voluntary systems. Figure 3.4 shows that, in most countries with mandatory systems, more than 70% of the working-age population participates in a funded pension plan. However, countries with high levels of informality (e.g. Mexico) do not reach this threshold.11 By contrast, no single country with a voluntary system achieves participation rates above 70%. Voluntary personal plans linked to the public pension system (e.g. the second pillar in Lithuania, Poland and the Slovak Republic) achieve relatively high participation rates of between 40% and 70%. Finally, participation rates in voluntary occupational plans can be quite low (e.g. below 15% in Austria, Luxembourg, Spain, Portugal and Greece). Indeed, participation in voluntary occupational plans requires a combination of three elements: i) that the employer offers a plan, ii) that the employee is eligible to join that plan and iii) that the eligible employee chooses to join that plan.

Source: OECD Global Pension Statistics.

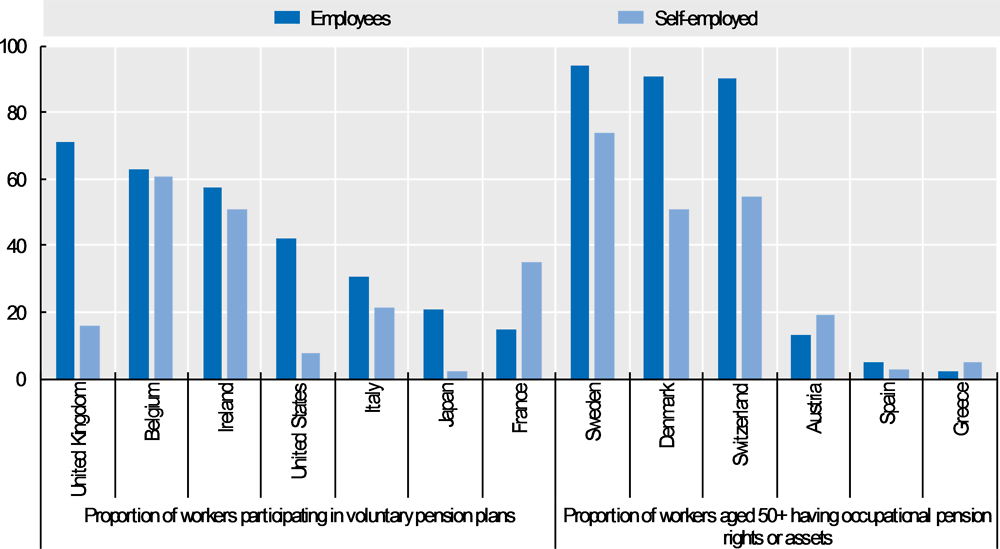

In pension systems organised mostly through occupational plans, self-employed workers tend to participate less than employees do. Data on participation rates in funded pensions by employment status are scarce. The left panel of Figure 3.5 shows participation rates in voluntary pension plans (both occupational and personal) for seven countries, while the right panel shows the proportion of workers aged 50 and older having occupational pension rights or assets for six countries. In Denmark, Ireland, Italy, Japan, Sweden, Switzerland, the United Kingdom and the United States, employees are more likely to participate in a funded pension arrangement than self-employed workers. These countries are mostly organised through occupational pension systems (either voluntary or mandatory), which usually do not cover the self-employed. In addition, in the Netherlands, only about 20% of self-employed workers declared in a survey that their current or last job before retirement entitles them to a retirement pension, compared with 84% for the total surveyed employed population (Karpowicz, 2019[1]). In Australia, while contributing to superannuation funds is nearly universal among employees, only 27% of the self-employed made contributions in 2016-17.12 In Chile, in 2017, 86% of employees contributed regularly to the pension system, as opposed to only 6% of the self-employed.13 In Denmark, 81% of employees paid into an occupational or personal pension plan in 2017, as opposed to 53% of the self-employed. In addition, 66% of the self-employed saved less than 5% of gross income that year, while only 16% of the employees saved that little.14 Finally, it is noteworthy that still large proportions of the self-employed expect to receive pension benefits from mandatory or quasi-mandatory occupational pension plans in Denmark (51%), Sweden (74%) and Switzerland (55%), as they accumulated pension rights or assets from past jobs as employees.

Source: National sources for participation in voluntary pension plans and SHARE wave 7 for workers aged 50 and older having occupational pension entitlements (Technical Report: Using SHARE data to measure pension adequacy in Europe)

Dedicated pension arrangements for the self-employed may help in bridging the gap of pension participation between employees and the self-employed. In Belgium, France and Japan, the self-employed have access to dedicated voluntary personal pension plans that employees cannot join. In addition, in Germany, basic pensions (“Rürup”) are designed to target the self-employed, although any other taxpayer can join these plans as well. Figure 3.5 shows that, in Belgium, participation in voluntary plans is the same for employees (via occupational plans) and the self-employed (via dedicated personal plans). In France, 35% of self-employed workers contribute to dedicated personal plans (called Madelin contracts), while only 15% of employees contribute to an occupational pension plan (6% to a PERCO and 9% to other occupational plans). In Germany, 11.5% of self-employed workers aged 40 to 59 have a basic pension contract, as opposed to only 1.8% for employees.15 In Japan, however, very few self-employed workers participate in national pension funds, the dedicated voluntary personal plans. The fact that participation in these plans becomes mandatory after joining may restrain take up.

Notes: Pension systems are classified between occupational (mandatory “MO”, quasi-mandatory “QMO” and voluntary “VO”), personal (mandatory “MP” and voluntary “VP”) and automatic enrolment (in personal or occupational plans, “AE”). For the United Kingdom, participation refers to workplace pensions, which include voluntary occupational plans and group personal plans.

Source: Chapter 4 of the OECD Pensions Outlook 2012 and national sources.

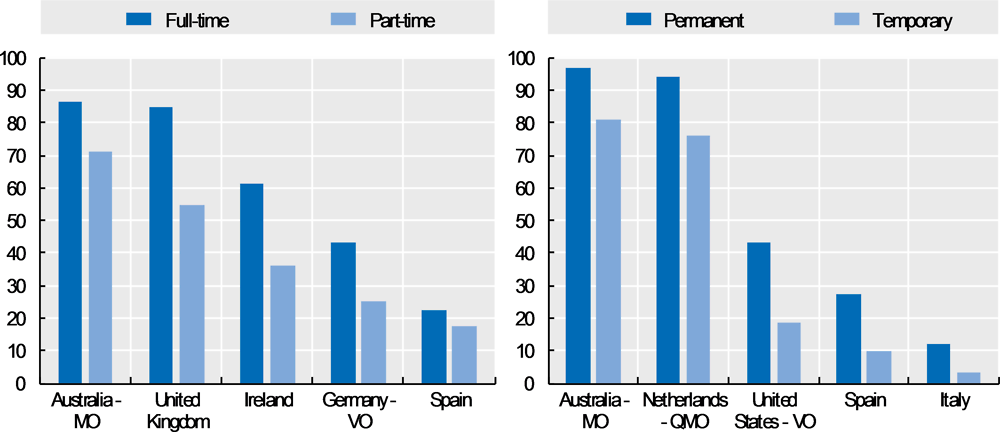

Part-time and temporary employees participate less in funded pensions than full-time and permanent employees do. Participation rates by type of contract are only available for a few countries. As shown in the left panel of Figure 3.6, in the five countries with available data, part-time employees participate less in funded pensions than full-time employees do. Minimum thresholds on earnings and working hours tend to exclude part-time workers from the population eligible to join occupational pension plans. Minimum requirements on length of employment and contract duration may also partially explain why temporary workers participate less in occupational pension plans than permanent employees do, as illustrated in the right panel of Figure 3.6.

copy the linklink copied!Contribution levels

Different categories of workers may face dissimilar rules concerning contributions on top of different access rules, potentially inducing some workers to save less for their retirement than others. This may happen because employees and self-employed workers are members of different types of plans to which different contribution rules apply, or because contribution rules vary according to the type of worker within a plan. There are differences across workers with respect to contribution rates, contribution caps, and the possibility to suspend the payment of contributions.

Contribution rates

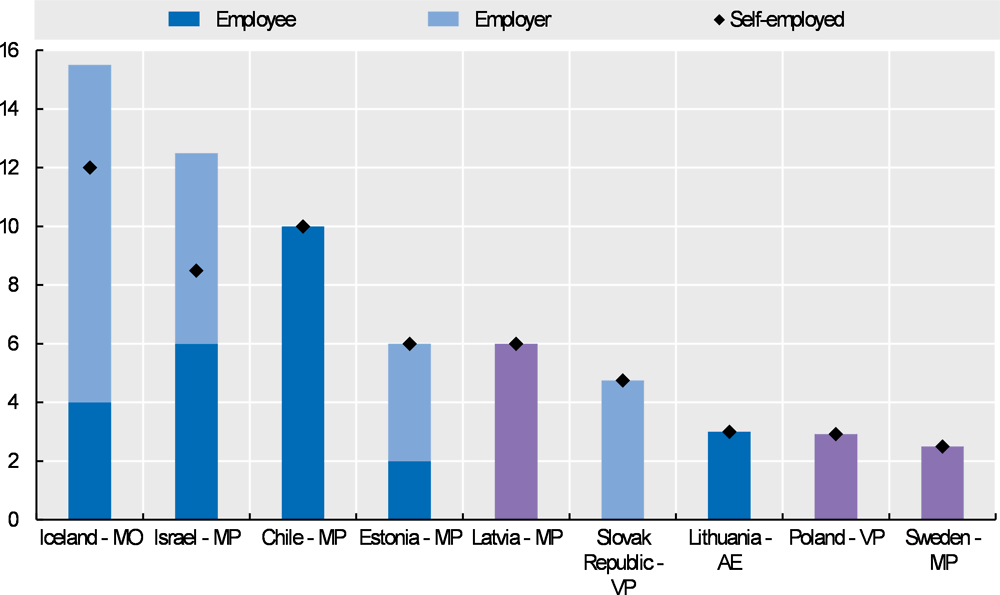

Minimum or mandatory contribution rates required from self-employed workers are either equal to or lower than those required from employees, who may share the burden with their employer. Figure 3.7 shows the minimum or mandatory contribution rates that apply to pension plans covering all types of workers. For employees, the contribution rate is split between the individual part and the employer part. In Iceland and Israel, mandatory contributions to funded pensions are lower for the self-employed than for employees. The difference is 4 percentage points (pp) in Israel and 3.5 pp in Iceland. In China, employees pay 8% of wages to the basic urban worker pension scheme, while the self-employed can choose to pay between RMB 100 and RMB 2 000 per year in the equivalent basic national resident pension scheme (pillar 1b). In the other countries, overall contribution rates are the same for all types of workers. While self-employed workers have to pay the full amount by themselves, employees share the contribution burden with employers in all countries in Figure 3.7, except Chile and Lithuania.

Notes: Pension systems are classified between occupational (mandatory “MO”, quasi-mandatory “QMO” and voluntary “VO”), personal (mandatory “MP” and voluntary “VP”) and automatic enrolment (in personal or occupational plans, “AE”). Purple colour represents cases where the contribution rate cannot be split precisely between the employee and the employer parts.

Different requirements in terms of contributions to mandatory funded pension plans for different types of workers may result in differences in take-home pay. It may also give an incentive to provide services through self-employed arrangements (e.g. contractors) rather than through an employment relationship with employees. When the overall contribution rate of employees, which includes the employee and the employer contribution, is higher than that of the self-employed, the self-employed will have a higher take-home income ceteris paribus. Providing services through self-employed arrangements may look more attractive as it could lead to a higher take-home income or lower employment cost to invest more or reduce prices potentially gaining market share. Unfortunately, this could also lead to a higher risk of a larger fall in their standard of living upon retirement if they fail to save more by themselves into a voluntary pension plan. Having the same overall contribution rate across employees and the self-employed in mandatory pension systems ensures that all workers will achieve the same replacement rate at retirement. Some categories of self-employed workers may find it hard, however, to pay the equivalent of both employer and employee pension contributions, in particular when they have low and fluctuating earnings.

In voluntary pension systems, the prospect of getting employer contributions creates an incentive for employees to contribute themselves to funded pensions. This type of incentive is not available to the self-employed, who may therefore contribute less in voluntary systems. Employees may indeed benefit from employer contributions in occupational or even sometimes personal pension plans (e.g. employers can contribute to their employees’ voluntary personal pension plan in the Czech Republic, Estonia, Finland and Iceland). In voluntary systems where employees can decide whether or not to participate in a pension plan offered at their workplace, an employer contribution may provide an incentive to participate in that plan, as only employees who decide to participate get the employer contribution. The literature shows that employer matching contributions in occupational pension plans in the United States increase participation levels (Choi, 2015[2]; Madrian, 2013[3]). This sort of incentive is not available to the self-employed. If self-employed workers contribute to voluntary pension plans, but do not cover the employer part of the contributions additionally, they will have lower assets accumulated at retirement and smaller pension benefits.

Contribution caps

Contribution caps can also influence contribution levels, although most countries do not differentiate them by type of worker. Table 3.2 lists the countries according to whether the contribution cap is the same or differs across employees and self-employed workers. Contributions to funded pension arrangements are usually capped, especially when these contributions can be deducted from an individual’s taxable income. Although individuals and employers may not contribute up to the maximum amount, the cap determines the maximum contribution level and can eventually influence future retirement income. Most countries apply the same contribution cap to all types of workers. This means that the overall cap for employee and employer contributions is the same as the cap for contributions done by self-employed workers alone.

In some countries, the cap for contributions made by or on behalf of employees is higher than the one for the self-employed. In the case of the Czech Republic, Finland, Ireland, Korea, Luxembourg, Norway, Poland and Brazil, two different caps apply to employee/individual contributions and employer contributions. While the same cap may apply to individual contributions irrespective of the type of worker, the fact that employees may also receive an employer contribution increases their overall cap as compared to self-employed workers. For example, in Luxembourg, any worker may contribute up to EUR 3 200 in voluntary personal plans. However, employees may also receive an employer contribution in an occupational plan, capped at 20% of the employee’s ordinary earnings. In the case of China, employees and the self-employed have access to different plans, to which different contribution caps apply.

Finally, in Belgium, France, Japan and Switzerland, the self-employed can contribute more in selected funded pension plans than employees. In Belgium, employees not covered by an occupational pension plan and self-employed workers can access pension plans called “free supplementary pensions”. The cap for employees is the highest of EUR 1 600 or 3% of gross salary received two years before. By contrast, the self-employed may contribute up to the highest of 8.17% of professional income or EUR 3 187.04. In France, the overall contribution limit for employees in occupational plans is 8% of 8 times the annual social security ceiling. Self-employed workers with high taxable profit may contribute up to 10% of 8 times the annual social security ceiling plus 15% of 7 times the annual social security ceiling in so-called Madelin contracts. In Japan, the self-employed benefit from a higher overall cap (JPY 816 000) than employees offered an occupational plan by their employer (JPY 660 000 combining any occupational and personal plan). The relatively higher cap for the self-employed may be to compensate for the fact that they are excluded from the earnings-related public pension scheme. Finally, in Switzerland, the self-employed can contribute 20% of taxable income up to CHF 34 128 in personal plans, as opposed to only CHF 6 826 for employees, in order to account for the fact that the self-employed do not have compulsory contributions paid into occupational plans.16

Suspension of contributions

The possibility of suspending the payment of contributions tends to be more readily available to the self-employed than to employees. This suspension also influences the total amount of contributions paid over a lifetime. In general, contributions to occupational pension plans cannot be paused during employment, whereas workers can usually decide freely to increase, decrease or stop contributing at any time in personal pension plans. While flexibility in the payment schedule of contributions may be welcomed for certain categories of workers, in particular those with volatile earnings, it also raises adequacy concerns if people do not increase their contributions afterwards to fill the gap.

copy the linklink copied!Pension income outcomes

There are certain design features of funded pension arrangements that may influence pension income outcomes differently across various categories of workers. When vesting periods apply, in particular in occupational plans, workers participating in and contributing to funded pensions may lose some of their pension rights (in DB plans) or the part of the assets (in DC plans) linked to the employer contributions when changing jobs. In addition, there may be leakages from the funded pension system when individuals change jobs (lack of portability) or when they have the possibility of accessing their funds before retirement age (early access), ultimately affecting future retirement income.

Vesting period

Being a member of an occupational pension plan does not necessarily mean that employees start accruing pension rights or accumulating assets from the first day of membership. Some pension plans apply a vesting period, which is the length of time an individual must be a member of the plan (i.e. contributing to the plan or having contributions being made on his/her behalf) before he or she becomes fully the owner of the rights accruing, or assets accumulating, within the plan. This vesting period comes on top of any number of years of employment that the worker had to fulfil before becoming a member of the plan (Figure 3.3). While employee contributions vest immediately in all countries and for all types of plans, it is not always the case for employer contributions. This may penalise temporary workers and workers switching jobs frequently, including between the formal and informal sectors, as they may not work long enough with the employer to vest the contributions, which would then be lost.

In a majority of countries, employer contributions to occupational pension plans vest immediately to the employee. With the exception of Norway, immediate vesting is the rule for mandatory and quasi-mandatory occupational pension plans.17 Immediate vesting of employer contributions also applies to voluntary plans in Austria (direct insurance and occupational group insurance), Belgium, Canada (federal jurisdiction), Greece (occupational insurance funds), Italy, Japan (corporate DC plans), Latvia, New Zealand (KiwiSaver), Poland, Slovenia, Spain, the United Kingdom, India (national pension system) and South Africa.

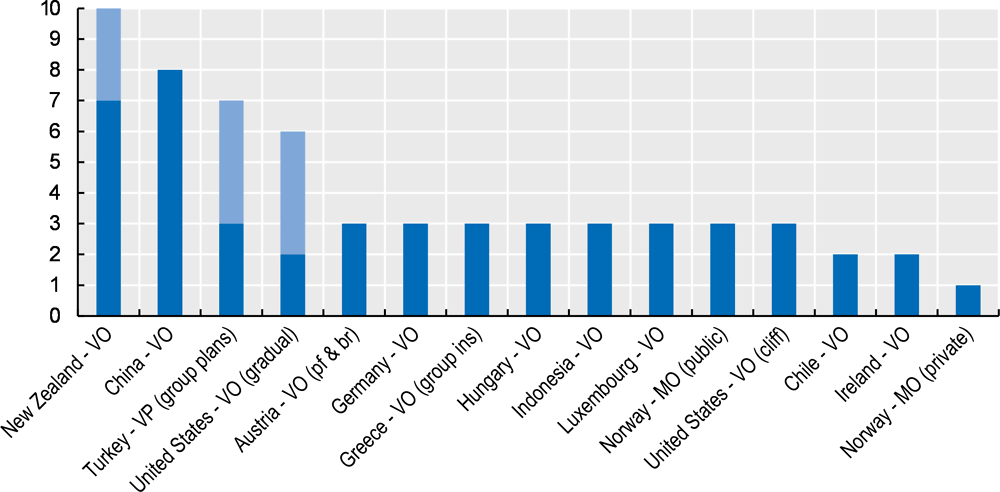

Notes: The figure represents the maximum allowed and employers can choose to set a shorter vesting period. Lighter blue colour represents graduated vesting. The numbers for the United States represent the case of traditional 401(k) plans. Other rules apply to DB plans and safe harbour plans. Pension systems are classified between occupational (mandatory “MO”, quasi-mandatory “QMO” and voluntary “VO”), personal (mandatory “MP” and voluntary “VP”) and automatic enrolment (in personal or occupational plans, “AE”).

The maximum length of the vesting period for employer contributions within each occupational plan varies widely across countries. As shown in Figure 3.8, it is only one year in Norway for private sector employees and two years in Chile and Ireland. A maximum vesting period of three years applies in Austria (pension funds and book reserves), Germany, Greece (group pension insurance), Hungary, Luxembourg, Norway (for public sector employees) and Indonesia. In the United States, occupational pension plans may apply “cliff” vesting or “graduated” vesting.18 For example, for 401(k) plans, cliff vesting implies a 100% vesting after no more than three years of membership. With graduated vesting, 20% of employer contributions vest after 2 years, 40% after 3 years, 60% after 4 years, 80% after 5 years, and 100% after 6 years.19 Finally, in Austria (support funds), France (article 39 plans) and Norway (AFP plans), employees only fully acquire the accrued benefits in their occupational DB plan when they leave the employer for retirement. This means that all the rights are lost if the employee changes employer or leave the labour force before the retirement age specified in the plan rules. This affects negatively labour mobility.

Within the European Union, the vesting period cannot be longer than three years for workers moving to a different member state. The EU Portability Directive (or “Directive on minimum requirements for enhancing worker mobility by improving the acquisition and preservation of supplementary pension rights”) places a limit of three years on the combined length of any minimum waiting period and vesting period applied in occupational pension plans. The Directive only refers, however, to “outgoing” workers, i.e. plan members moving between member states. There is no EU rule governing the maximum vesting period for members staying in a given member state. However, the expectation is that countries do not differentiate between mobile and non-mobile workers when applying the Directive, so that all workers covered by an occupational pension plan would have to work for a maximum of three years with the employer before acquiring rights.

Portability of pension rights and assets

Issues related to the portability of pension rights and assets arise essentially with occupational pension plans and can have a negative impact on workers switching jobs frequently, including employees on temporary contracts. When changing employers, members of an occupational pension plan with their former employer usually cannot continue contributing into the same plan. In addition, the new employer may not offer an occupational plan, leading to the risk that workers may stop saving for retirement. When the new employer offers a plan, the consolidation of past and current occupational plans is not always possible, in particular with DB plans, potentially leaving employees with multiple inactive pension accounts from past employment. By contrast, pension systems operating mainly through personal pension plans are, by definition, fully portable. Personal pension plans can follow members throughout their career and accept contributions, irrespective of the employer and the type of work.

Workers in most countries have the option of keeping their accrued rights and assets in the occupational plan of their former employer or transfer them into their new employer’s occupational plan upon changing jobs. Table 3.3 lists the options available to workers with their occupational pension rights and assets when leaving their employer. In a majority of countries, the options of keeping deferred rights and assets in the plan or transferring them to a new occupational plan are available. Only in Korea and Turkey neither of these two options are available, an employee who terminates employment before reaching retirement age can receive a payment for the years of service rendered. In Turkey, they can also transfer the assets to a personal plan. In Canada and Japan, workers can start getting a pension income from their occupational plan when leaving an employer, even when this occurs before the age of retirement.

Transfers of occupational pension entitlements into personal pension plans are more rarely available. Upon leaving an employer, accrued occupational pension rights and assets can be transferred into a personal pension plan in Canada, Chile, Denmark, France, Ireland, Italy, Japan, Poland, Portugal, Spain, Turkey, the United Kingdom, the United States, Indonesia and South Africa. In Canada, such transfers are only possible to locked-in personal plans, from which the funds cannot normally be used for any purpose other than to provide the individual with a retirement pension. In Denmark, only the self-employed can transfer their pension entitlements from a previous job as an employee into a personal plan. In Japan, entitlements in DB and DC plans can be transferred to the personal DC plan of the National Pension Fund Association.

Former employees can cash in their small accrued benefits in some countries. In Australia, Austria, Germany, Luxembourg, the Netherlands and Switzerland, small entitlements are directly paid to the individual rather than kept as deferred rights or transferred to another plan (Table 3.3). This may avoid that administration fees eat up all the assets if they were to remain in the plan. In the United Kingdom, employees leaving their employer after less than two years of work may be able to get a refund on their contributions. This more likely concerns temporary workers. In the United States, employers can force leaving employees to take account balances of up to USD 1 000 out of the plan. In Brazil and Indonesia, employees can receive a refund of their own contributions plus interest. In Switzerland, individuals can receive their vested benefit as a lump sum if they establish an independent business and are no longer covered by the mandatory occupational pension system.

Upon changing jobs, workers can keep contributing to the same occupational plan in selected countries. In occupational pension systems structured in part through collective agreements (industry-wide or sector-wide pension plans), if an employee moves to an employer covered by the same agreement, the employee will stay in the same pension fund and portability is automatic. This applies in Australia, Belgium, Denmark, Finland, Iceland, the Netherlands, Sweden, the United States and South Africa. In the absence of collective agreements, it is still possible to continue contributing into the same plan in Australia, Austria (except book reserves and support funds), Canada (PRPP), France, Greece, the United Kingdom and Brazil. In particular, in the United Kingdom, workers becoming self-employed can use the National Employment Saving Trust (NEST). In the Netherlands, self-employed workers may be allowed to continue contributing voluntarily to the plan they have been a member of as an employee for up to ten years following the termination of employment.

Early access to funds

Flexibility in accessing funds accumulated in funded pensions before the age of retirement should be restricted to exceptional circumstances as it reduces future retirement income. Workers with unstable and fluctuating earnings, however, may value this option and may be more willing to participate in funded pensions when they are given the possibility of withdrawing money in order to cope with unplanned contingencies. Unfortunately, this raises issues of retirement income adequacy, as the funds accessed early may not be compensated for afterwards.

The most common conditions required to be able to access funds early are for the purchase of a home or its repair, upon reaching a certain age or membership duration, and in case of disability. Homeownership is considered in many countries as a mean to achieve financial security in retirement, and is therefore considered as an asset for retirement.20 As shown in Table 3.4, 15 of the countries analysed allow individuals to either withdraw or borrow money from selected pension plans to buy a home or make reparations. Twenty countries constrain withdrawals to individuals reaching a certain age or after a certain membership period, recognising the long-term saving nature of pension plans. These requirements more often relate to personal pension plans than to occupational plans. In some cases, withdrawals are possible at any time, but the minimum age or membership period define when these withdrawals become tax free. The age requirement varies from 40 in Austria to 62 in Germany (for Riester and basic pension schemes), and the membership period requirement from 5 years in Mexico to 10 years in Austria, Hungary, the Slovak Republic, Spain, India (depending on entry age and sector) and Indonesia. The two requirements are combined in Estonia, Japan, Luxembourg and Turkey. Finally, members becoming disabled, either temporarily or permanently, may withdraw their funds early in 17 countries.21 This possibility is more frequent for voluntary personal pension plans.

Periods of vulnerability may also trigger the possibility of accessing funds early. Individuals suffering from terminal medical conditions, having shorter life expectancies due to physical or mental disability, or having reduced work capacity due to an accident or illness may withdraw their assets early in 13 countries, mostly from voluntary systems. Suffering financial hardship, unemployment (usually long-term) or facing exceptional expenses for medical reasons or to cover the funerals of relatives are other conditions that individuals may use to access their funds in some countries. Other qualifying motives, such as wedding expenses, training or education expenses, or leaving the country are less common. Switzerland is the only country allowing members to take all of their vested rights in their mandatory occupational pension scheme as a lump sum when establishing an independent business.

Another way of accessing funds before the age of retirement is through loans. Pension funds are allowed to lend money to plan members in 13 countries. It may be for the purchase of a property (e.g. Canada, Iceland, Mexico, Poland and South Africa) or for any other motive.22 In Switzerland, members of occupational plans may pledge their right to future benefits not yet accrued or a sum up to the amount of their vested rights in order to finance the purchase of a principal residence for their use, or to amortise a mortgage on such a residence. Pension assets may also be used as a collateral in the United Kingdom.

copy the linklink copied!Conclusion

This chapter has shown that workers in non-standard forms of work, i.e. workers in non-standard forms of employment (part-time and/or temporary salaried employees) and self-employed workers, participate less in funded pensions than full-time permanent employees do. This relates to four main factors:

-

Self-employed workers lack mandatory coverage in selected funded pension systems. The mandatory or voluntary nature of enrolment strongly influences participation rates. Mandatory and quasi-mandatory pension systems achieve higher overall participation rates than voluntary systems. However, the obligation to join the funded pension system is not always extended to self-employed workers. For example, the self-employed are not mandatorily covered by funded schemes in Australia, Denmark, Mexico, the Netherlands, Norway and Switzerland.

-

In pension systems organised mostly through occupational plans, self-employed workers tend to participate less than employees do because access to such plans requires an employment or professional relationship between workers and the entity that establishes the plan. Dedicated pension arrangements for the self-employed, such as those in Belgium and France, may, however, help to bridge the gap of pension participation between employees and the self-employed.

-

In most countries with automatic enrolment schemes, the self-employed are not automatically enrolled into a pension plan, except in Lithuania. In Canada, New Zealand and the United Kingdom, the self-employed can voluntarily join the system by contracting directly with a plan provider.

-

Some plans establish eligibility criteria to limit the population effectively allowed to join, affecting in particular part-time and temporary employees. These criteria include minimum income thresholds (e.g. Canada, Japan, Switzerland and the United Kingdom), minimum number of working hours (e.g. Australian, Japan and Korea) and minimum length of employment (e.g. Ireland, Japan and Luxembourg). They restrict access by part-time and temporary employees to occupational pension plans.

In most countries, mandatory contribution rates in compulsory funded systems, as well as minimum contribution rates and overall contribution caps in voluntary systems, are identical across all categories of workers. In some countries, however, the self-employed are required to contribute less than employees or are not allowed to save overall as much as employees (who may also receive employer contributions). For example, in Iceland and Israel, the self-employed have a lower mandatory contribution rate than employees. In other countries, the self-employed actually enjoy higher contribution caps in selected pension arrangements, probably to reflect the fact they cannot participate in occupational plans, do not benefit from employer contributions, and sometimes contribute less to public pension schemes.

Several design features affect negatively the pension income outcomes of workers in non-standard forms of work:

-

Vesting periods penalise workers switching jobs frequently. While contributions done by the workers themselves vest immediately in all types of funded pension arrangements, employees may not start getting ownership of their employer’s contributions as of the first day of membership in a plan. Temporary employees may lose the benefit of employer contributions if their employment contract is shorter than the vesting period. A maximum vesting period of three years can be found in selected schemes in Austria, Germany, Greece, Hungary and Norway.

-

Lack of portability of occupational pension rights and assets affects workers switching jobs frequently. In most countries, workers have the option of keeping their accrued rights and assets in the occupational plan of their former employer or transfer them to their new employer’s occupational plan upon changing jobs. In occupational pension systems structured through collective agreements (industry-wide or sector-wide pension plans), if an employee moves to an employer covered by the same agreement, the employee will stay in the same pension fund and portability is automatic, as in Australia, Belgium, Denmark, Finland, Iceland, the Netherlands, Sweden and the United States. The option of cashing in pension entitlements when leaving an occupational pension plan before retirement creates leakages from the system but is usually restricted to small amounts, as in Australia, Austria, Germany, Luxembourg, the Netherlands, Switzerland and the United States.

-

Flexibility in accessing funds accumulated in funded pensions before the age of retirement may remove a barrier to the participation of workers with unstable and fluctuating earnings, but raises issues of retirement income adequacy. The most common conditions required to be able to access funds early are for the purchase of a home or its repair, upon reaching a certain age or membership duration, and in case of disability. This may be too lenient and put individuals at risk of suffering a fall in their standard of living upon retirement.

Countries willing to enhance or develop the role of the funded pension system for non-standard workers and offer them complementary pension plans to save for retirement, need to adjust the design of these plans. A better alignment with the OECD Core Principles of Private Pension Regulation, in particular Core Principles 8 and 10, could help some countries to have a more inclusive funded pension system, which does not penalise a growing proportion of the workforce (OECD, 2016[4]).

Policy makers should aim to prevent exclusion from plan participation for workers in non-standard forms of work. Regulation should ensure non-discriminatory access to occupational pension plans. This implies limiting the use of, or even eliminating, eligibility criteria based on salary, working hours, length of employment and type of contract (Core Principle 8). The equivalent principle applies to personal plans, which should be accessible to any individual (Core Principle 10).

Vesting periods should be minimised to allow workers to accrue entitlements as early as possible. While entitlements derived from member contributions should be vested immediately, vesting periods for employer contributions could be eliminated or kept short. Practices that substantially undermine benefit accrual and vesting rights should also be prohibited (Core Principle 8). This particularly concerns pension plans that only pay pension benefits to members who work with the same employer that promotes the plan until the age of retirement.

Finally, countries should limit leakages from the funded pension system originating from job changes and early withdrawal possibilities. Policy makers should facilitate the portability of pension rights and assets, allowing individuals who are changing jobs to keep saving in the same arrangement, or to transfer their vested rights to the plan of their current employer or to a similar alternative arrangement (Core Principle 8). Flexibility in accessing funds accumulated in funded pensions before the age of retirement should be restricted to exceptional circumstances as it reduces future retirement income.

Future work will assess different approaches to encouraging non-standard workers to save for retirement, taking into account the role already played by the PAYG system. Given the heterogeneity of this population, different solutions may be required. In addition, care should be given to performance and costs, so that workers in general are not discouraged from saving into funded pension arrangements.

References

[5] ATP (2019), “Selvstændiges pensionsindbetalinger er faldet”, Faktum 190, https://www.atp.dk/sites/default/files/faktum_190_september.pdf.

[2] Choi, J. (2015), “Contributions to defined contribution pension plans”, Annual Review of Financial Economics, Vol. 7/1, pp. 161-178.

[1] Karpowicz, I. (2019), “Self-Employment and Support for the Dutch Pension Reform”, IMF Working Paper WP/19/64.

[3] Madrian, B. (2013), “Matching contributions and savings outcomes: A behavioral economics perspective”, in Matching Contributions for Pensions: A Review of International Evidence, The World Bank, https://doi.org/10.1596/978-0-8213-9492-2.

[4] OECD (2016), OECD Core Principles of Private Pension Regulation, https://www.oecd.org/daf/fin/private-pensions/Core-Principles-Private-Pension-Regulation.pdf.

Notes

← 1. The analysis covers all OECD countries, as well as selected non-OECD G20 countries.

← 2. The project benefits from the collaboration with the European Commission’s DG Employment, Social Affairs and Inclusion and with Principal International Group.

← 3. In Finland, the statutory earnings-related pension scheme for the self-employed (YEL) is financed on a PAYG basis and therefore not considered in this analysis.

← 4. In the case of Canada, the analysis focuses on federally regulated registered pension plans (RPPs) and federal legislation for pooled registered pension plans (PRPPs). Each province has pension standards legislation with respect to provincially regulated RPPs. The province of Quebec has a version of PRPPs called Voluntary Retirement Savings Plans (VRSPs).

← 5. In the United States, the Department of Labor has issued a final regulation that would expand access to multiple employer retirement plans for small employers and self-employed workers.

← 6. In the United Kingdom, employees earning less than GBP 10 000 a year are not enrolled automatically in the plan by their employer but they can opt into the plan voluntarily.

← 7. In Germany, basic pensions are designed to target the self-employed, but any other taxpayers can join such plans.

← 8. In France, according to the PACTE Law, the plans dedicated to the self-employed (Madelin contracts) will be closed from 1 October 2020. New individual retirement savings plan available to any individual as of 1 October 2019 share most of the features of the Madelin contract for those joining the plan as self-employed workers.

← 9. In the case of Chile, the threshold represents the income under which self-employed workers issuing invoices are no longer mandated to contribute (but they can still contribute voluntarily).

← 10. In the United States, employers are permitted to exclude part-time workers. There is also a limit in the number of working hours, but over a full year. In general, an employee must be allowed to participate in a qualified retirement plan if he or she has reached age 21 and has at least one year of employment. One year of employment is considered 1 000 hours of work performed during the year, or approximately 19 hours per week.

← 11. Korea is also far below the threshold, as the obligation for employers to provide a retirement benefit scheme to their employees can be fulfilled by just offering a severance payment plan.

← 12. This may be partly explained by the fact that there is a AUD 500 000 lifetime capital gains tax exemption when an individual rolls over the sale proceeds from a sole proprietorship or stake in a general partnership business into a recognised retail or self-managed superannuation fund.

← 13. This number refers to self-employed workers contributing regularly to the pension system and does not include the self-employed contributing via the tax process. With the new law introduced in 2019, which makes contributing to the social security system compulsory for self-employed workers that invoice for their services, this participation rate will increase.

← 14. Source: ATP. A recent analysis shows that the proportion of self-employed workers paying into a pension fell between 1999 and 2017, due to the termination of the SP scheme and changes to tax rules (ATP, 2019[5]).

← 15. By contrast, 31.4% of employees have a Riester pension contract, as opposed to 20.3% for the self-employed (Source: LeA study).

← 16. Employees who are not member of a pension fund can also contribute 20% of their taxable income.

← 17. In Norway, for private sector workers, the parliament approved the abolishment of the one-year vesting period, but the rule has not yet entered into force. The vesting period in the public sector will fall to one year as of 1 January 2020.

← 18. According to the Bureau of Labor Statistics, 34% of workers participating in savings and thrift plans in 2017 enjoyed full immediate vesting, 34% were under graduated vesting and 24% under cliff vesting.

← 19. The gradual vesting in the case of New Zealand does not refer to KiwiSaver plans, but to occupational pension plans with low coverage rates, especially among new employees.

← 20. However, there may be a lack of financial instruments to make housing wealth partly liquid at retirement.

← 21. These individuals would most likely also receive disability benefits from the government.

← 22. In the case of Mexico, this is only possible with the housing sub-account.

Metadata, Legal and Rights

https://doi.org/10.1787/b6d3dcfc-en

© OECD 2019

The use of this work, whether digital or print, is governed by the Terms and Conditions to be found at http://www.oecd.org/termsandconditions.