1. Developments in Agricultural Policy and Support

This chapter first provides an overview on recent economic and market developments that provide the context for the implementation of agricultural policies. The second section presents main changes and initiatives in agricultural policies in 2020-21, focusing on policy responses to the COVID-19 pandemic that target, or strongly affect, agricultural producers, food consumers and other actors along the food supply chain. The subsequent analysis of levels and structures of agricultural support informs an assessment of the extent to which current support contributes to the food systems’ “triple challenge” of achieving food security and nutrition, providing livelihoods to those connected to the sector, and reducing the environmental footprint and greenhouse gas emissions of the sector. The chapter also explores how current policies perform across productivity, sustainability and resilience, key channels for contributing to addressing these challenges. It concludes with an assessment of policy developments, and with recommendations for concrete actions.

In 2020, agricultural policies and support to the sector were significantly affected by the outbreak of the coronavirus SARS-CoV-2, the subsequent spread of the COVID-19 virus, and substantial restrictions to populations and enterprises aimed at containing the virus. These factors caused economic growth to slow significantly or even turn strongly negative in all economies, while in many countries unemployment rose as companies were forced to lay off employees. Commodity markets were affected as well, but the implications for global agricultural markets remained comparatively limited as, despite some significant stresses, food systems and supply chains proved relatively robust.

The pandemic caused major dislocations to food markets, in particular with the closure of restaurants, and the shift in consumption away from food outside the home. But the overall demand for food was fairly stable, as food supply was generally recognised to be essential and thus exempt from lockdowns, while consumers prioritised food among their expenditures. However, several advanced economies saw increased recourse to food banks among low income consumers who had seen a drastic fall in their incomes. Labour intensive sectors, such as meat processing and sectors requiring seasonal labour for planting or harvesting, were also deeply affected by the virus and measures to contain it.

As a land based activity, the production of most commodities was generally able to withstand the pandemic, although those products requiring more labour input – principally fruits and vegetables – or where supply is destined primarily for the restaurant trade, were more affected. In general, developments on agricultural markets were driven as much by non-COVID factors as by the impacts of the pandemic. Overall, the agricultural sector proved remarkably resilient, with farm incomes increasing in 2020 for a majority of countries covered in this report.

To help people and companies to cope with the economic consequences of both the virus and containment strategies, governments introduced a wide set of policies as of early 2020. In looking at changes made to agricultural policies and support, this report therefore begins by discussing policy responses to the COVID-19 pandemic that focus on, or strongly affect, agricultural producers, other actors along the food supply chain, and food consumers.

The report then analyses the level and structure of agricultural support, in particular in terms of the extent to which they help or hinders the performance of food systems, gauged in terms of their contribution to the “triple challenge” of:

1. Achieving food security and nutrition for a growing world population.

2. Providing livelihoods to farmers and others connected to the sector, either vertically along the value chain or spatially across rural economies.

3. Reducing the environmental footprint of the sector and contributing to lower greenhouse gas (GHG) emissions.

Drawing on insights from the OECD Framework for Productivity, Sustainability and Resilience, this part of the report also explores how current policies perform across the three dimensions of productivity, sustainability and resilience, which are identified as key channels through which agriculture can contribute to the challenges facing food systems. Lastly, this part of the report concludes with an assessment of the developments in policies and support, and with recommendations for concrete actions to improve the performance of agricultural policies in meeting the challenges facing global food systems.

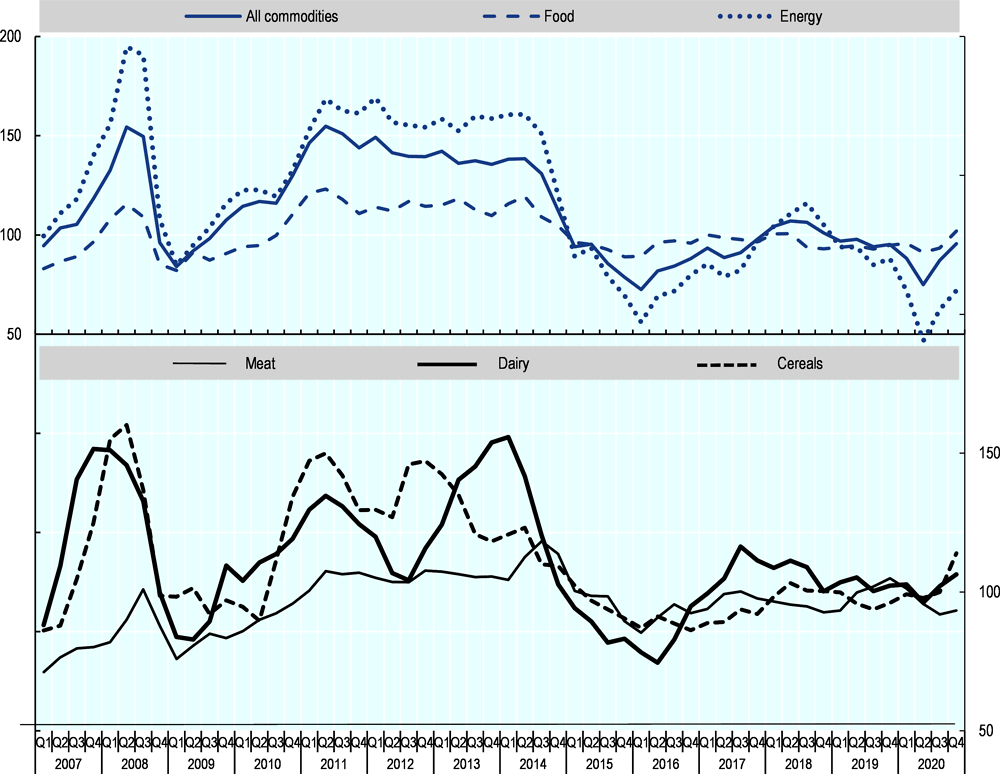

Conditions in agricultural markets are strongly influenced by macro-economic factors, such as economic growth (measured by gross domestic product, GDP), which generates the income supporting demand for agricultural and food products, as well as prices for crude oil and other energy sources which affect the prices of numerous production inputs in agriculture, such as fuel, chemicals and fertiliser. Energy prices also affect the demand for cereals, sugar crops and oilseeds through the market for biofuels produced from these feedstocks.

Global economic growth, which slowed to below 3% in 2019, came to an abrupt halt in the wake of the COVID-19 pandemic. Global output in 2020 is estimated to have been more than 4% below that in 2019, reflecting policy responses to the pandemic, which included substantial restrictions in both personal and economic activities (OECD, 2020[1]).1 GDP growth in all OECD economies turned negative. The contraction was particularly significant in the Euro area, where economic output declined by 7.5% in 2020, after low growth of 1.3% the year before. Japan was significantly hit as well, with GDP shrinking by 5.3% in 2020, after some first signs of rebounding growth in 2019 at +0.7%. The contraction was less pronounced in the United States, where economic output, which grew by more than 2% in 2019, declined by 3.7% in 2020.

The downturn in OECD economies was associated with a decreased demand for labour. Across the OECD area, unemployment, which had fallen slightly to 5.4% in 2019, increased to 7.2% in 2020. In many countries, the negative impact on employment was mitigated by substantial public interventions, including notably the widespread application of publicly supported short-time work.2 Average inflation declined further to 1.5%, driven in particular by falling energy prices (see below).

Growth in emerging economies also fell substantially, although the extent of the downturn varied strongly. Argentina’s GDP, which had seen negative growth for the last two years already, shrank by 12.9%, the first double-digit economic contraction since the currency and debt crisis of 2001-02. India’s GDP contracted by 9.9%, more than 14 percentage points below 2019 growth, while South Africa’s GDP fell by 8.1%, following stagnation in 2019. On the other hand, the People’s Republic of China (hereafter, “China”) is the only country covered in this report that maintained positive growth in 2020, at 1.8% compared with 6.1% the year before. The Indonesian economy also fared comparatively well, with a slight contraction of 2.4%, following 5% growth in 2019.

The consequences of the COVID-19 pandemic and of related restrictions are strongly visible in international trade. In real terms, global trade declined by more than 10% year-on-year, following already slow growth in 2019.

Lower economic growth and restrictions on personal and economic mobility put significant pressure on prices for energy and other non-food commodities (IMF, 2021[2]). On average, energy prices in 2020 were 30% lower than in 2019, and more than 40% below their 2018 levels. Crude oil prices, which had fallen to levels close to (and on certain markets even below) zero in April 2020, averaged 33% lower over the full year compared to 2019. Lower energy prices also pulled down fertiliser prices, which on average were 9% lower year-on-year.

In comparison, food prices remained robust. After dropping by 7% in the second quarter of 2020, average international food prices increased towards the end of the year, and annual averages ended 3% higher than in 2019, with contrasting movements between crop and livestock markets, as explained below.

Note: The top part of the graph relates to the left scale, while the bottom part of the graph to the right scale.

Source: IMF (2021), Commodity Market Review, for all commodities, food and energy indices (base year: 2016), www.imf.org/external/np/res/commod/index.aspx; FAO (2021), FAO Food Price Index dataset, for meat, dairy and cereal indices (base period: 2014-16), www.fao.org/worldfoodsituation/foodpricesindex/en.

Global food markets saw prices for crops and livestock products moving in opposite directions. World meat markets had seen production decline in 2019 primarily due to the impact of African Swine Fever (ASF) on China’s pig meat sector. While the disease continued to limit production in China and other countries such as Viet Nam during 2020, herds began to rebuild. In spite of the lower Chinese output, however, global meat prices were under significant downward pressure in 2020 due to logistical difficulties and reduced demand following the COVID-19 pandemic, which together dampened meat import demand from several key importing countries. On average, meat prices in 2020 fell by 4.5% year-on-year.

The pandemic also had significant, though varied, impacts on dairy markets. While away-from-home consumption in many countries suffered as a result of widespread confinement measures, larger retail sales for at-home consumption partly offset these losses. Fresh dairy products were particularly vulnerable to disruptions in supply chains, but many countries were able to adjust their production chains relatively quickly. As a consequence, while the effects of the pandemic varied across regions, global dairy prices changed only little year-on-year, with lower prices in the second quarter balanced by rising prices towards the end of the year.

In contrast to livestock markets, world prices for crop commodities mostly rose in 2020. Following short-term disruptions due to the COVID-19 pandemic, oilseeds markets were driven by strong demand notably for imported soybeans into China as the country began to rebuild pig herds. At the same time, lower supply growth of palm oil resulted in relatively short supplies on international markets. As a consequence, international prices rose significantly in 2020, with prices for soybeans and vegetable oils averaging 7% and almost 20% higher than in 2019.

Increased feed demand from the rebuilding pork sector in China, logistical difficulties in some major producing countries, and some temporary export restrictions following the COVID-19 pandemic, drove prices upwards in cereal markets. Pushed by increases notably towards the end of the year, average cereal prices were almost 7% higher in 2020 than in the preceding year.

Continued shortfalls in sugar production due to unfavourable weather conditions in some of the major producing countries offset lower import demand for sugar and notably reduced biofuel demand in light of reduced mobility due to the pandemic, resulting in average sugar prices increasing slightly year-on-year, but remaining well below levels seen in 2016.

Overall, food supply chains were recognised as essential services in most countries implementing COVID-19 related restrictions on economic activities, as a result of which the sector was affected by those restrictions more indirectly than directly. Often, both domestic and international trade in food products were facilitated through green corridors and other measures notwithstanding disruptions affecting trade overall. Labour shortages due to restrictions on people’s movement were alleviated through exceptions for agricultural and food chain workers, and through schemes encouraging workers laid off in other sectors or students to temporarily work in agriculture and the food industry. However, income losses and economic uncertainties, together with restrictions for restaurants and other away-from-home food suppliers, generated changes in food demand which the industry needed to cope with. But the impact of economic contractions on food expenditure was mitigated through public support partly compensating for income losses, and reductions in disposable incomes seem to have led to higher shares of income being spent on food. Partly with the help of government policy responses, food systems have therefore proven remarkably resilient. Indeed, after short-term disruptions in international food markets in the early phase of the pandemic, these markets appear to have been impacted more by other factors such as livestock diseases and climatic conditions than by the pandemic itself.

As governments started implementing containment measures to slow the spread of the COVID-19 virus early in 2020, they also began introducing measures to limit impacts of the virus and associated containment measures on the agriculture and agro-food supply chains.3 Most government responses in the sector were introduced in the first few months of the pandemic, largely in response to the shock to specific subsectors. Still, as the year went by, as new waves and strands of infection developed, governments in many countries shifted their attention towards medium-term issues by bolstering early relief measures and introducing economic recovery packages.

This section presents an overview of government measures introduced in 2020 in the 54 countries covered in this report, using different categorisations, focusing mainly on the number and type of measures, and associated budget figures. The dataset used for analysis was compiled based on the information on domestic and international trade related COVID-19 policy developments provided in country chapters in this report.4 While the reported set of measures is comprehensive, and covers all the most important policy responses, it does not claim to capture all measures in place in all countries covered in the study.

Countries implemented a diverse set of responses to COVID-19

Governments of the covered countries and the European Union introduced 776 unique policy measures to respond to the COVID-19 related crisis during 2020, of which 496 were introduced in the first four months of 2020 (OECD, 2020[3]; Gruère and Brooks, 2021[4]). The overall number of unique measures for the year 2020 increases to 1 086 applied policy measures if EU-wide measures, applicable to all member states, are added to unique measures for each of the EU Member States (including for the period covered, the United Kingdom).

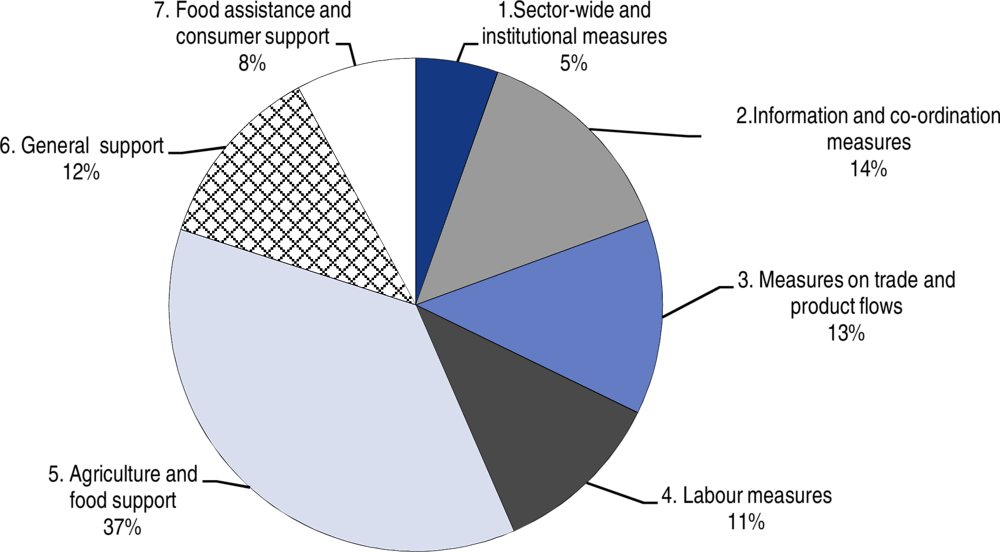

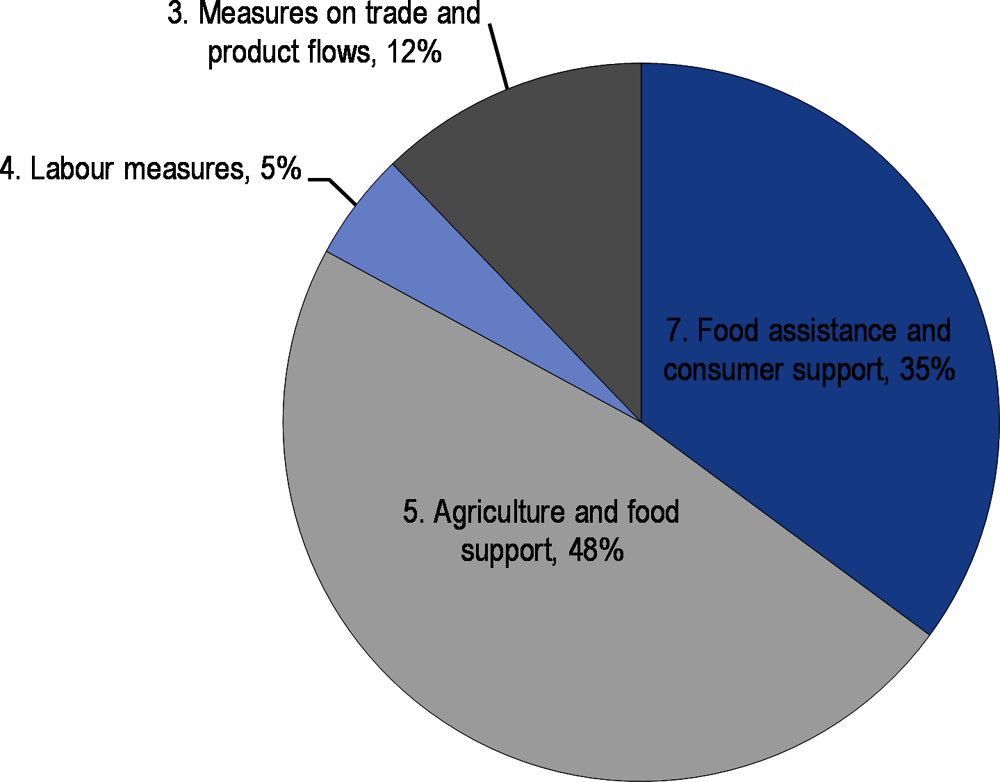

The nature of the government responses varied widely. OECD (2020[3]) distinguished seven categories of measures: 1) Sector-wide and institutional measures; 2) Information and co-ordination measures; 3) Measures on trade and product flows (enhancing trade or restricting trade); 4) Labour measures (biosecurity and workforce related measures); 5) Agriculture and food support (or support for agriculture and food companies); 6) General support (including packages that apply to the sector); and 7) Food assistance and consumer support (demand side interventions).5 Unique government measures were distributed across those categories, with 37% of the 776 measures focusing on agriculture and food support, 5% on institutional measures, and 8% on food assistance measures, with the remaining four categories covering between 11% and 14% of measures (Figure 1.2).

These proportions changed since the four first months of 2020, from a focus on information and co-ordination to agriculture and food support measures. The share of agriculture and food support measures increased by 14 percentage points over the year, while the share of measures on information and co-ordination and general support declined by 7 and 4 percentage points, respectively. This evolution might reflect the need for information and communication in the early period, followed by the increased importance that some governments attached to providing support to agriculture and food companies to cushion the impact of the first wave of the virus. Shares for other categories of measures remained stable, indicating a moderate increase in the use of these measures across countries.

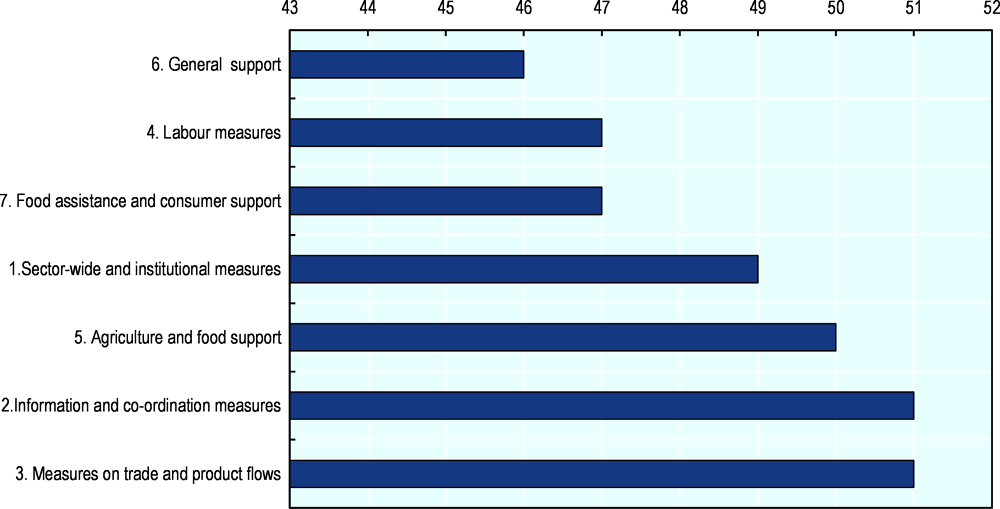

A wide range of measures adopted is also observed among the 54 covered countries, underscoring the comprehensiveness of government responses. Thirty-eight of the covered countries applied measures in all seven categories, while ten countries applied measures in six of the seven categories. Fifty or more countries applied trade and product flow measures, information measures or agriculture and food support measures, while the other categories of measures were each applied by at least 46 countries (Figure 1.3).

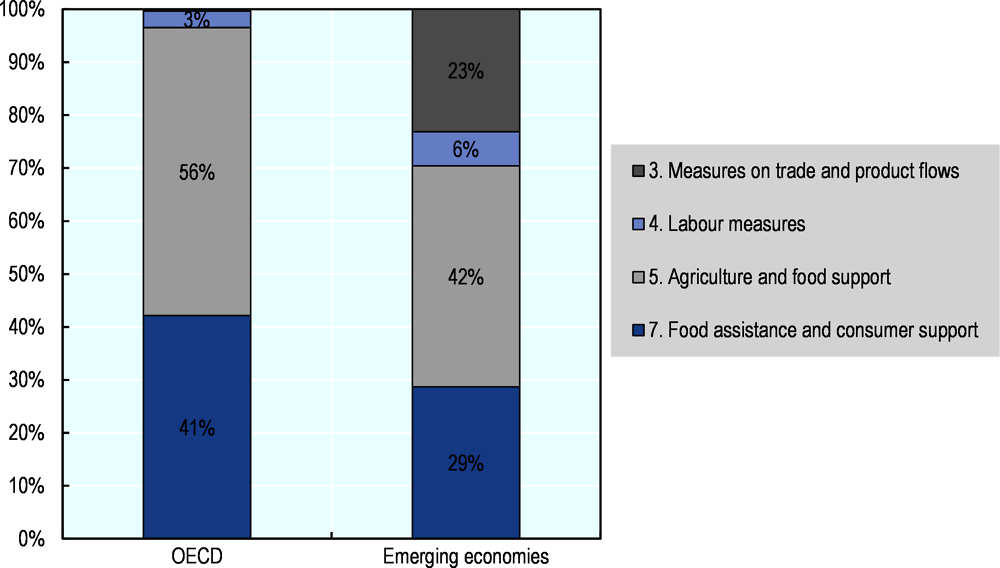

At the same time, differences in the number of measures by category can be seen among regions and countries. In particular, 54% of measures undertaken by governments in OECD countries focused on the three categories of support (agriculture and food support, general support and food assistance and consumer support measures), including the largest proportion on agriculture and food support (35%), while 58% of measures undertaken by emerging economies were in the non-support categories of measures (sector wide and institutional, information and co-ordination, trade and product flows and labour measures), including the largest proportion of measures (26%) in the trade and product flow category. This difference may reflect the existing policies covering the sector in the respective groups of countries, but may also be due to differences in structures of the sector as well as the type of shocks associated with the COVID-19 pandemic and associated containment measures. A further factor may be differences in budgetary and fiscal scope to provide additional support. Among OECD countries, Asian and European countries favoured agriculture and food support measures, South American countries focused on information and co-ordination measures, Oceanian countries prioritised labour measures, and North American countries displayed no clear dominance across categories of measures.

Only 11% of the unique measures recorded explicitly built on existing policy measures already in place, almost all in the agriculture and food support category in the form of flexibility or changes in existing policy programmes. This suggests that governments often introduced new programmes, funding or approaches to respond to the crisis, or that they relied on existing policies without making notable changes. Innovative approaches were used for instance to re-channel food unused by closed schools towards families, to hire temporarily unemployed workers from cities in fields, or via the use of digital tools to ease market transactions and custom controls.

Measures varied in their purpose, timing, scope and potential impacts

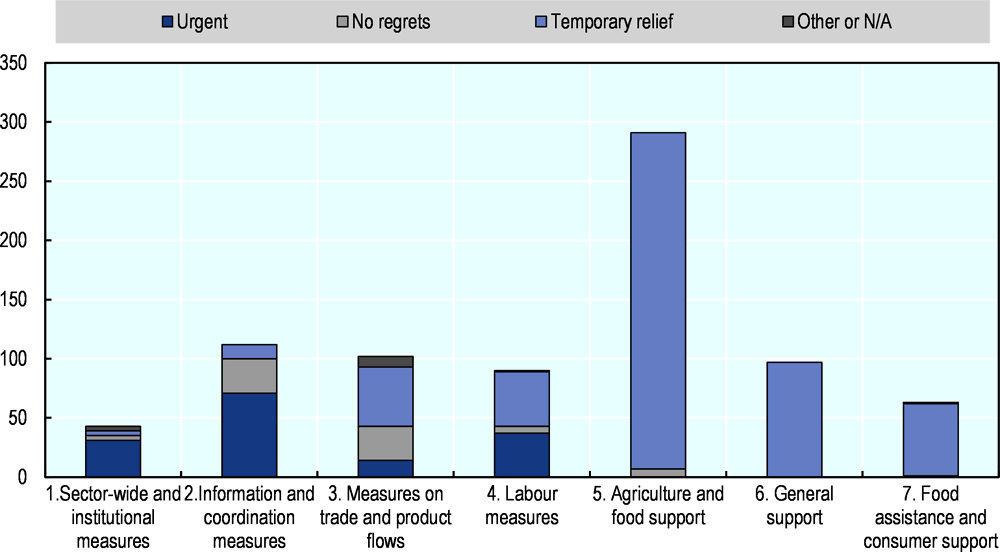

Government responses also differed in their timing and scope, from the initial imposition of lockdown measures, to policies aiming to temper the impacts of the crisis on specific supply chains or consumers or in the medium term. At the same time, several measures taken to facilitate the functioning of production or supply chains could usefully have been taken before of the COVID-19 crisis. To highlight these distinctions and better understand the implication of government responses, measures were organised in three groups:6

Urgent measures to ensure supply: these emergency measures were taken at the onset of the crisis to ensure supply and keep the sector functioning. Examples include biosafety measures; declaring agriculture and food as an essential sector; measures to ensure the functioning of government agencies; co-ordination of responses with the private sector; and national and international logistic and transport measures, including setting up green lanes to ensure the continuation of trade. These measures are intrinsically linked to the pandemic, and would either be lifted or no longer relevant after the COVID-19 crisis. This group includes 150 unique measures (19% of the total).

No regrets measures: these measures improve market functioning and thereby contribute to improved resilience. They could have been taken before, and should be maintained or even scaled up after the COVID-19 crisis. This group includes measures supporting digital innovations that facilitate e-commerce; exchange of information; agriculture job-matching information centres; and training or trade facilitation measures. This group includes 75 unique measures (10% of the total).

Temporary relief measures: these measures seek to contain the impact of the crisis on agriculture and food sector actors, from producers to consumers. Governments considered them necessary but they should include sunset clauses to avoid outliving their original rationale. These measures comprise largely temporary trade and markets measures to relieve domestic economic pressure, agricultural support measures, including those that compensate producers and agro-food chain actors for damages incurred; consumer and food assistance7 measures and measures that lifted or limited regulatory requirements for farmers. This group is the largest, with 537 unique measures (69% of the total).

The remaining 14 measures (2%) could not be attributed to any of the groups.

As expected, measures in the three support categories (5, 6 and 7) are overwhelmingly temporary relief measures, but measures in other categories, belong to different groups (Figure 1.4). Urgent measures to ensure supply include institutional and informational measures, but also labour measures and trade and product flow measures (categories 1 to 4). No regrets measures were mostly information and co-ordination measures and product and trade flow measures that enhance the functioning of markets (categories 2 and 3).

Source: Information collected from the 54 countries.

A large majority of countries implemented measures that belong to each of these groups, even if some differences are observed among countries. All but two countries applied one or more urgent measures to ensure supply, and the same number of countries applied temporary relief measures; fewer countries (46) applied at least one no regrets measure. OECD countries applied relatively more temporary relief measures than emerging economies, who applied relatively more of measures in the other two groups.

An additional distinction was made to identify measures that could at least temporarily be potentially market and trade distorting or environmentally harmful.8 These mostly temporary relief measures include trade bans or export restrictions that were temporarily put in place by several countries, but also market price controls, relaxed environmental regulations, and specific agricultural support measures for different agricultural commodities. Eighty-five unique measures (11% of the total) introduced by 47 countries were identified to have potential impact on markets or the environment, belonging to the agriculture and food support category, the trade and product flow, and the food assistance categories.

Governments allocated at least USD 157 billion to respond to impacts in the agriculture and food sector

One of the key ways in which governments have addressed the economic impact of the COVID-19 pandemic and associated lockdowns is by offering liquidity, credits, and funding for relief measures. Governments in many countries have adopted comprehensive economic recovery packages, with measures that included new lines of credits, subsidised loans, flexibilities in taxes, or subsidies and which included firms in the agriculture and food sector. At the same time, governments in many countries created specific financial support measures to the agriculture and food sector.

This section provides a preliminary assessment of budgetary allocation in response to the COVID-19 impact based on collected information. It therefore only focuses on the subset of measures for which financial information was available (in total 119 unique measures in 41 countries).

A review of the reported budgetary figures associated with the collected COVID-19 responses comes with several important caveats. First, it is impossible to track how much of the general recovery packages were used on the agricultural sector, so these are largely excluded from the assessment. Second, while these numbers include some expenditures incurred in 2020, a larger set of programmes that were announced in 2020 has not yet been delivered to the sector. As such, a majority of the numbers presented are not reflected in the 2020 data in this year’s agriculture support estimate database. Third, funding for sector-wide and institutional measures (category 1) and information and co-ordination measures (category 2) was not available. Fourth, some of the measures provide support for targeted or affected individuals on the basis of unit costs, but there is no estimate of the number of individuals or firms that benefitted from the support, so these support measures are excluded from the assessment. Fourth, governments may have used existing policies and measures, potentially with budget adjustments or changes in implementation, without reporting those as related to COVID-19. All these caveats suggest the reported figures are likely to represent minimum estimates of financial support measures in the 54 countries.

In total, governments dedicated USD 157 billion in response to impacts to the sector (Table 1.2). Of this total, USD 116 billion was earmarked in the form of grants, payments or other funding, while USD 41 billion was offered in in the form of subsidised rates loans, new credit lines, and other mechanisms. At the same time, USD 5.6 trillion was provisionally identified in general recovery packages that included the food and agriculture sector (category 6 - general support). This support was not specific to the sector.

Sector specific earmarked funding primarily focused on relief measures for agriculture and food actors, and food assistance measures (83% as shown in Figure 1.5). Twelve per cent of financial support focused on general services, such as infrastructure development, e-commerce development and measures easing trade, which are listed under the category of measures on product and trade flows. The remaining 5% of support was directed towards addressing labour shortfall, via compensation mechanisms for migrant or new farm workers, and implementing bio-sanitary measures, including compensation to the culling of minks potentially infected by the COVID-19 virus as well as equipment support.

Notes: This includes promised funding, credits, loans and other support mechanism. Category 3 measures are those facilitating market functioning, logistics and infrastructure (general services), category 4 measures are labour and biosecurity measures, and category 7 measures are food assistance measures.

Source: Information collected from the 54 countries.

There are significant differences in the reported financial support between OECD countries and emerging economies (Figure 1.6). OECD countries’ financial support amounted to USD 75 billion, almost entirely dedicated to relief measures expressed in terms of agriculture and food support (USD 32 billion) and food assistance (USD 41 billion), with the remaining funding going towards labour and biosafety measures. New and expanding food assistance programmes were observed in OECD countries (Box 1.1). In contrast, emerging economies reported USD 82 billion of financial support, with USD 34 billion going to agriculture and food support and USD 24 billion to food assistance, implying lower shares of overall support in these categories, with a higher share (23%) dedicated to general services enhancing market and trade.

Note: Non OECD EU Member States do not feature in this figure. Category 3 measures are those facilitating market functioning, logistics and infrastructure (general services), category 4 measures are labour and biosecurity measures, and category 7 measures are food assistance measures.

Source: Information collected from the 54 countries.

Many countries deployed public emergency food assistance measures to prevent rising food insecurity resulting from the COVID-19 crisis. These complemented other livelihood support measures that aimed to contain the pandemic’s socio-economic consequences and thus the spread of poverty across OECD countries (OECD, 2020[5]).

Countries have reinforced existing food assistance programmes1 or deployed new schemes to suit the needs of their vulnerable populations. Food assistance programmes have targeted low-income households with a particular focus on infants, children, students, the vulnerable and elderly people. Some eligibility criteria that had constrained access to pre-existing schemes were eased during the pandemic. The programmes fall into two categories:

The provision of vouchers that can be used to buy food without restrictions or to buy certain types of (healthy) food products. Some countries have used digital technologies to issue benefits electronically to some vulnerable population groups and to provide information on food assistance packages for which households might be entitled (Baragwanath, 2021[6]).

The provision of free or subsidised meals either in canteens or in other public places when this is possible, or by home-delivery. Home-delivery of meals required logistical adaptation and often involved partnerships with private caterers.

Governments also provided additional support for food bank operations to respond to growing emergency food aid demand. In pre-COVID-19 times, about 25% of food banks’ food supply depended on public support. The COVID-19 crisis further increased the need for public support (GFN, 2020[7]). To facilitate continued operation of food banks , OECD governments provided three types of support measures:

Operational and financial support: Mostly offered by local authorities, such support provided storage, cooking and distribution facilities, as well as protection materials and staff. Several governments also provided financial support for food purchases and to cover additional operating costs related to sanitary protocols.

Flexibility in existing programme implementation: The rules behind food banks’ public support were relaxed as a result of the COVID-19 pandemic. For instance, the European Union’s Coronavirus Response Investment Initiative Plus (CRII+) made it possible to provide food assistance indirectly via food vouchers for food banks supported by the Fund for European Aid to the Most Deprived (FEAD).

Food donations: Ministries, mostly those in charge of agriculture, were involved in programmes recovering food products that were supposed to be served in schools or in restaurants. For example, the United States Department of Agriculture (USDA) was involved, via the pre-existing Emergency Food Assistance Programme (TEFAP) and the new Farmers to Families Food Box Program, in the purchase of domestically-grown food products to be provided to vulnerable population. Food donations programmes in the United States (USDA, 2021[8]) and also in the European Union (FEBA, 2020[9]) are expected to continue in 2021.

← 1. Information on existing programmes can be found in (Placzek, 2021[10]).

With regard to agriculture and food support measures, OECD countries favoured funding mechanisms, such as direct payments, grants or increased allocation to existing support programmes (83%), while emerging economies supported the sector via preferential loans and credit mechanisms (99%). Large countries on both sides drive this pattern, with the United States accounting for 69% of total agriculture and food support via earmarked funding, and India accounting for 90% of loans and credits to be granted to the sector in response to the COVID-19 crisis.

Sixteen of the 119 measures displaying financial support were identified as potentially market and trade distorting or environmentally harmful. These agriculture and support measures amounted to USD 731 million, which is significant but remains marginal compared to the total earmarked funds dedicated to the agriculture and food support (USD 35 billion) or to the global agriculture support estimates conveyed in this report.

Other key policy trends and developments in 2020

While policies for agriculture and food have been strongly influenced by the COVID-19 pandemic, other changes were also made in 2020. Specific information on the developments is summarised below, with details on adjustments made to policies and programmes within countries available in the country chapters within this report.

Several countries have revised their agricultural policy frameworks. Colombia introduced the “Together for the Countryside” (Juntos por el campo) initiative, including a range of new policy programmes and subsidies for transportation, machinery and equipment, and variable inputs. Indonesia introduced specific programmes to increase production capacity on about 165 000 hectares of swampy land in Central Kalimantan, and to expand rice planting areas with 250 000 hectares of rice, maize, shallots and chilies in deficit areas. Japan revised its “Basic Plan for Food, Agriculture and Rural Areas”, which sets out policy directions, food self-sufficiency goals and commodity production targets for the next ten years. Mexico published the Sectoral Programme for Agriculture and Rural Development 2019-2024, focusing on improving agricultural productivity for food self-sufficiency, reducing poverty rates in rural areas, and increasing small-scale agricultural producers’ incomes. Viet Nam approved a series of strategies, plans and programmes to promote agricultural and rural development, including a new Livestock Development Strategy for 2021-30; a plan to promote investment in the agricultural and rural sector for 2021-25; a Master Programme on Sustainable Agricultural Development and Adaptation to Climate Change in the Mekong River Delta for 2030; a Scheme for Developing Organic Agriculture for 2020-30; and an irrigation strategy for 2030.

The European Union also released a number of major policy initiatives: the European Parliament and the Council agreed on transitional rules for the Common Agricultural Policy (CAP) for 2021-22, while negotiations continue on CAP reform. In May 2020, the European Commission released more details on proposed Green Deal initiatives most relevant to the agricultural sector – specifically, the Farm to Fork and the Biodiversity strategies, which seek to halt biodiversity loss in Europe, transform EU food systems into global standards for competitive sustainability, protect human and planetary health and safeguard the livelihoods of all actors in the food value chain.

New support measures and reforms to existing policies were introduced. Argentina shifted to more active export restrictions, reintroducing taxes that were reduced or eliminated between 2015 and 2018. Brazil created financial mechanisms to attract funds for rural credit, reducing preferential annual interest rates provided by Pronaf, the main credit programme for small farmers. Korea established a new direct payment system, combining the direct payments for rice, upland crops and less favoured areas into a single scheme. The income compensation scheme for rice, which has been the main payment scheme in Korea, was converted into a decoupled payment programme and accompanied by environmental cross compliance regulations. Norway eliminated its last export subsidies on cheese and processed agricultural products as of the end of 2020. The Philippines established a Rice Competitiveness Enhancement Fund to support investments in machinery and equipment, breeding and distribution of high quality rice seeds, credit and expansion. The Russian Federation (hereafter “Russia”) expanded its railroad tariff subsidies to cover the transportation of soybean meal, vegetables and mineral fertilisers. Viet Nam extended a land tax exemption to the end of 2025, allowing farm households and organisations to avoid paying an agricultural land use tax or continue benefiting from a land tax reduction.

A number of countries developed new climate-related policies and strategies. Canada has established a new Natural Climate Solutions for Agriculture Fund, which will support carbon sequestration and beneficial management practices, such as cover crops or shelterbelts, through development, testing, peer-to-peer learning and solution sharing with farmers. Furthermore, under the “A Healthy Environment and A Healthy Economy” plan, the government of Canada plans to invest USD 123 million over seven years to support the agricultural sector in developing transformative clean technologies, reducing emissions from fertilisers to 30% below 2020 levels, boosting climate-smart agriculture, and supporting the production and use of low-carbon fuels. Japan published a national Green Growth Strategy in December 2020, outlining a comprehensive plan to achieve net-zero GHG emissions across the economy by 2050. The Ministry of Agriculture, Forestry and Fisheries has also announced a strategy for sustainable food systems, named “Measures for Achievement of Decarbonisation and Resilience with Innovation”, which aims to achieve zero CO2 emissions from agriculture, reduce the use of chemical pesticides and fertilisers, and make all subsidies carbon neutral by 2040. Korea released the 2050 Carbon Neutral Strategy, a long-term plan for GHG emissions mitigation. The strategy sets out four tasks for the agricultural sector: transition to smart farming; develop and deploy low-carbon agricultural practices; promote participatory policies for farmers and consumers; and scale up the deployment of eco-friendly energy. New Zealand has developed a ten-year roadmap for boosting primary sector export earnings while reducing biogenic methane emissions in accordance with the 2019 Zero Carbon Act. In addition, the “He Waka Eke Noa – Primary Sector Climate Action Partnership” seeks to reduce agricultural GHG emissions and enhance the sector’s resilience to climate change. Ukraine introduced new legislation to outline its strategy on environmental policies, along with a framework to monitor, report and verify the country’s GHG emissions. Chile, Iceland, Israel and Viet Nam also outlined new strategies and objectives in 2020 to reduce their GHG emissions from agriculture.

In addition, several countries took steps to improve the sustainable management of their water resources. This group includes Chile (currently developing a Ministerial water plan), New Zealand (through the 2020 National Environment Standards for Freshwater), and Viet Nam (via the Irrigation Strategy to 2030). This follows a more general trend in OECD countries, where governments changed their agriculture and water policies, in the last decade, broadly in line with the OECD Council Recommendation on Water (Gruère, Shigemitsu and Crawford, 2020[11]; OECD, 2021[12]).9

Several countries strengthened their promotion of organic farming. Notably, the European Union’s Farm to Fork Strategy includes several agriculture-specific targets, one of which is to increase the share of farmland under organic farming to at least 25%. Furthermore, increasing the area of organic farming is also a key policy objective of Japan’s Ministry of Agriculture, Forestry and Fisheries. Russia introduced a new law providing requirements for the production and labelling of organic products. The creation of a system of certification for organic products is ongoing, with 64 producers currently certified. Viet Nam approved a Scheme for Developing Organic Agriculture in 2020-30, setting out specific goals to increase the share of organic production in agricultural land use and for improving the value per hectare of organic production by 2030.

Some countries developed new solutions to tackle food loss and waste. Canada is investing USD 15 million to establish the Food Waste Reduction Challenge, encouraging innovative business models to develop solutions to prevent or divert food waste along the food supply chain. Turkey published a national strategy document and action plan on Prevention, Reduction and Monitoring of Food Loss and Waste, setting four strategic goals and 13 targets.

Risk management and disaster assistance policies were strengthened. Australia introduced drought resilience response programmes through the Future Drought Fund, and provided support to farm clean up and emergency response activities through the National Bushfire Recovery Fund. China’s Ministry of Agriculture and Rural Development and the Ministry of Finance jointly allocated USD 47 million to a new disaster relief fund assisting agricultural producers in flood-hit southern provinces. Kazakhstan’s mandatory crop insurance system was transformed into a voluntary insurance scheme with a view towards expanding crop and livestock insurance markets in the country. In New Zealand, a flooding event and significant drought affecting large parts of the country triggered public support for recovery and relief, as well as to individual farmers in hardship through Rural Assistance Payments. Turkey provided additional coverage through the state-supported agricultural insurance scheme, issuing 2.1 million insurance policies and USD 250 million of state insurance premium support. The United States provided an additional USD 1.5 billion for the continuation of disaster assistance programme delivery, adding several new qualifying disaster events and eligible participants under the Wildfire and Hurricane Indemnity Program Plus (WHIP+). The USDA’s Risk Management Agency also introduced a new policy to help farmers recover from hurricanes, covering 70 different crops.

New laws and regulations on animal and plant health were introduced. Chile’s animal and plant health agency promoted electronic certification, now established for exports to 34 countries and covering around 70% of all phytosanitary certificates. Costa Rica’s animal and plant health institutions established a single export window to deal with sanitary and phytosanitary procedures, and created an online system for consulting phytosanitary certificates for agricultural exports in real time. Switzerland introduced new plant health legislation, requiring stricter regulations and stronger preventive measures to protect plants from harmful pests. In the United States, the USDA’s Animal and Plant Health Inspection Service (APHIS) published the Sustainable, Ecological, Consistent, Uniform, Responsible, Efficient (SECURE) rule, the first comprehensive revision of the Agency’s biotechnology regulations in over 30 years. The new rule puts in place a more efficient process to identify plants that would be subject to regulation, focusing on the properties of the plant rather than on its method of production.

Concerning land reform and investment, Russia increased support for investments in agriculture, including purchases of agricultural machinery, goods and processing equipment. The company Rosagroleasing aims to supply 9 000 units of equipment in one year, which represents a 40% increase on last year’s numbers. South Africa established the Agriculture Development Agency to support the development of sustainable land reform programmes and reduce barriers to the commercialisation of small-scale farmers. Ukraine passed new legislation ending the ban on the sale of agricultural land. As of July 2021, individual citizens of Ukraine will be permitted to purchase up to 100 hectares of land, while from January 2024 purchases of up to 10 000 hectares will be made available to legal entities whose founders or final beneficiaries are Ukrainians, and which do not have business abroad or in offshore companies. Viet Nam approved a plan to promote investment in the agricultural and rural sector in 2021-25, including the following priorities: evaluating market potentials, trends and investment partners; building a database on investment promotion activities; establishing a list of projects calling for investment; and providing support to enterprises and investors.

Some countries provided new support to agricultural innovation and the development of digital technologies. Japan published the Smart Agriculture Comprehensive Policy Package, identifying key measures to advance data-driven agriculture over the next five years. The Ministry of Agriculture, Forestry and Fisheries also established the Conception and Projects for DX of Agriculture Initiative, which provides a roadmap for the development of artificial intelligence, big data, and the digitalisation of administrative procedures. Korea established the Smart Agriculture Project, which aims to promote the application of new technologies and attract young and innovative farmers to the agricultural sector. Young farmers can benefit from concessional leasing of agricultural facilities and farmlands in smart farm complexes, and cross-sectoral R&D projects will be conducted to support the development of new technologies. Turkey introduced the Digital Agriculture Market (DITAP), a digital platform to help develop supplier linkages between smallholders and large-scale food processing and retail firms. DITAP also helps small farmers to access markets for inputs such as seeds and fertilisers, and provides a platform for farmers to lease their land.

Numerous countries have concluded bilateral and regional trade agreements. On 15 November 2020, the Regional Comprehensive Economic Partnership (RCEP) was concluded by fifteen countries in the Asia-Pacific region, including Australia, China, Indonesia, Japan, New Zealand, the Philippines, Korea and Viet Nam. The Agreement will reduce tariffs on goods among the 15 participating economies by 90% over two decades from entry into force, and provides a framework for strengthening co-operation in the areas of standards, technical regulations, and conformity assessment procedures, as well as for streamlining rules of origin and border processes for perishable goods. The Canada-United States-Mexico Agreement (CUSMA) entered into force on 1 July 2020, preserving the existing agricultural commitments under the North American Free Trade Agreement (NAFTA). The European Union and Mexico finished negotiations on a new EU-Mexico trade agreement, which will further liberalise more than 85% of the agricultural tariff lines that were left out of the original EU-Mexico Global Agreement that has been in force since 2000. On 31 January 2020, the United Kingdom left the EU Single Market and Customs Union, ending the free movement of people, goods and services with the European Union. The rules governing trade and movement between the two are laid down in the draft EU-UK Trade and Cooperation Agreement, which was agreed on 24 December 2020 and ratified by the European Parliament on 27 April 2021. Of particular relevance to agriculture, the trade component of the agreement includes duty- and quota-free imports on all goods that comply with rules-of-origin provisions.

Several additional bilateral free trade agreements (FTAs) were negotiated or came into effect in 2020 and 2021, helping to facilitate bilateral trade in agricultural products. These include: the Canada–United Kingdom Trade Continuity Agreement; Colombia-Israel FTA; European Union-Viet Nam FTA; Indonesia-Australia Comprehensive Economic Partnership Agreement (CEPA); Indonesia-Korea CEPA; Japan-US FTA; Korea-Israel FTA; Ukraine-Israel FTA; United Kingdom-Israel FTA (and related protocol for the mutual recognition of organic produce); United Kingdom-Japan CEPA; United Kingdom-Korea FTA; United Kingdom-Mexico Trade Continuity Agreement; United Kingdom-Ukraine political, free trade and strategic partnership agreement; United Kingdom-Viet Nam FTA; United States-China Phase One Trade Agreement. Numerous other FTA negotiations are ongoing.

Trade promotion and market development policies were introduced by a number of countries. India initiated reforms to remove limits on private stocking, trading or buying of commodities, allow farmers to sell their agricultural products outside of government-regulated markets, and promote barrier-free inter and intra-state trade of agricultural commodities. The government also established a new Agriculture Infrastructure Fund to support farmers, producer organisations and agribusinesses through subsidised loans for post-harvest infrastructure such as cold storage, collection centres and processing units. To facilitate the exports of processed food products, the Ministry of Trade of Indonesia adopted measures to simplify the certificate of origin service and introduce automatic authentication procedures in licensing processes. Japan introduced the Act on Facilitating the Export of Agricultural, Forestry and Fishery Products and Food, which streamlines export policies for these products. The Strategy to Realize Export Expansion of Agricultural, Forestry, Fishery Products and Food designates products to prioritise resources and actions for agricultural export expansion. Russia introduced a programme to support exports of agricultural products, including additional financing for export infrastructure, simplification of border procedures, veterinary and phytosanitary services, information support, and support to promotion and market access.

Food systems face a daunting “triple challenge”. First and foremost, they are expected to achieve food security and nutrition for a growing world population. Second, they have an essential role to play in providing incomes and livelihoods for hundreds of millions of people involved in farming and other segments of the food chain. And third, they must do so in a sustainable manner, without depleting land, water and biodiversity resources, while contributing to reductions in greenhouse gas (GHG) emissions. The urgency of these challenges is reflected in the international political timetable, with food and agriculture at the heart of foreseen discussions in 2021 at the COP-26 UN Climate Change Conference, the COP-15 meeting of the Conference of the Parties to the Convention on Biological Diversity, and the UN Food Systems Summit.

Agricultural support policies have played a major role in shaping today’s food systems. Historically, the provision of support to agriculture has been motivated by a variety of policy objectives, which have included ensuring food security, supporting farmers’ incomes and livelihoods and improving environmental outcomes – key components of the “triple challenge”. The instruments chosen to pursue these objectives have varied widely. Some countries have relied on trade and open access to markets to ensure food security, while others have stressed domestic production and high rates of self-sufficiency, maintained via subsidies and trade protection. Countries have similarly varied in the extent to which they see income support as a goal for agricultural policy (as opposed to being covered by wider social protection programmes), and in the instruments they have chosen to deliver it. Most countries also have specific agri-environmental programmes, but many of the environmental impacts of agricultural policies stem from the choice of policies to address the first two objectives.

This section begins with an overview of the level and composition of agricultural support policies across countries. This is followed by an assessment of the implications of agricultural support for the performance of food systems, reflected in the extent to which they may be helping or hindering progress in meeting the triple challenge. Finally, the section considers the effectiveness of agricultural support policies in strengthening the overall productivity, sustainability and resilience of the agricultural sector – key channels for improving the performance of food systems.

An overview of support to agriculture

The OECD has been monitoring developments in agricultural support in OECD countries on an annual basis since 1988, with an increasing number of economies outside the OECD area included since then. This exercise quantifies different forms of policy intervention according to their implementation criteria, and forms the basis for an assessment of policy performance against stated objectives.

The current assessment covers 54 countries across six continents, including all OECD member countries, 5 non-OECD EU Member States, and 12 emerging and developing economies.10 Together, these countries represent three-quarters of global agricultural value-added. The assessment also discusses aggregate results for OECD member countries, the emerging economies, and all countries combined. In these aggregates, however, Costa Rica, which became the 38th Member of the OECD in May 2021, is included as one of the 12 Emerging Economies. The European Union is presented as one economic region, and includes the United Kingdom, which has left the European Union in early 2020 but remained part of the single market and continued to implement the Common Agricultural Policy through to the end of 2020 (a separate set of support indicators is presented in this report for the United Kingdom for 2017-20).

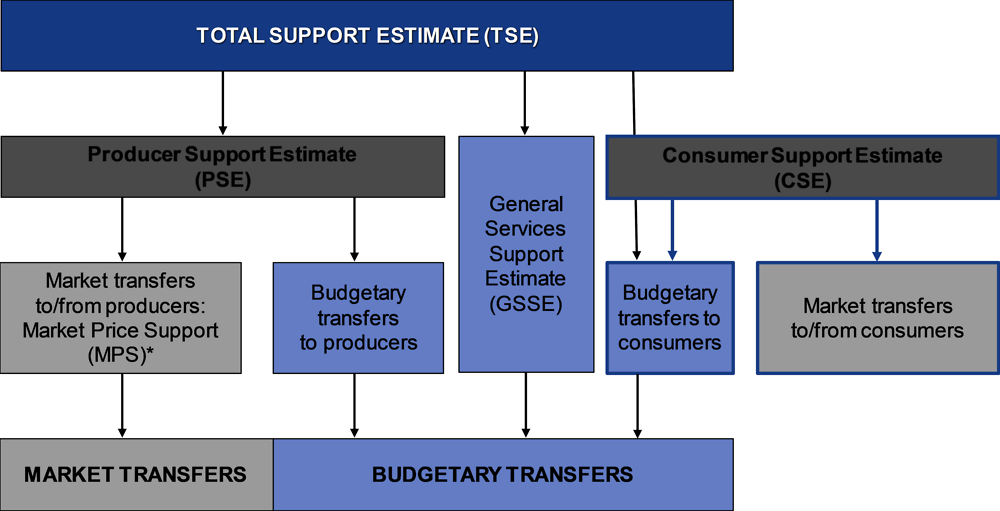

Figure 1.7 provides an overview of the structure of agricultural support indicators. The Total Support Estimate (TSE) is the OECD’s broadest indicator of support. It comprises policy expenditures in general services for primary agriculture that benefit the sector as a whole (General Services Support Estimate or GSSE); policy transfers to individual producers (Producer Support Estimate or PSE); and budgetary support to consumers included in the Consumer Support Estimate (CSE). Annex 1.A provides definitions of the OECD indicators of agricultural policy support.

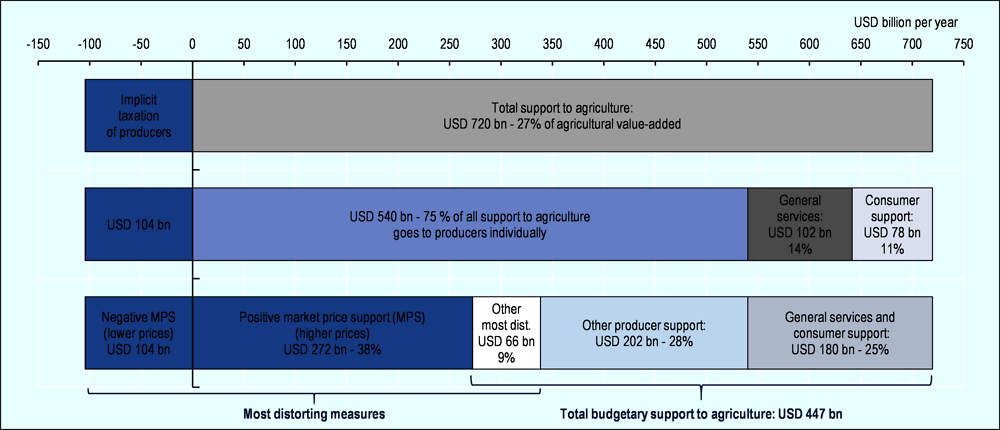

In 2018-20, agricultural support policies across the 54 countries covered in this report generated USD 720 billion per year in transfers to agriculture. This was counter-acted by more than USD 104 billion per year in implicit taxation of farmers. Individual producers received USD 540 billion in support per year (about 75% of all positive transfers to agriculture) through various support measures, including higher prices paid by consumers.

Governments employ a variety of different policy measures to deliver agricultural support (Figure 1.8). An important share of support is delivered through measures that modify domestic prices relative to world market prices. These policies do not result in government expenditures per se, but rather represent market transfers from consumers to producers, or vice-versa:

Market price support (MPS) arises from policies that create a price gap between domestic market prices and border prices for specific agricultural commodities (Box 1.2). Import licences, tariffs, tariff rate quotas and minimum prices are examples of measures that would result in higher prices paid by consumers. Total positive MPS amounted to USD 272 billion per year in 2018-20.

Some emerging and developing countries (Argentina, India, Viet Nam, Kazakhstan, Russia and Indonesia) implicitly tax producers on some or all agricultural commodities through measures that depress the domestic prices of these products, such as export taxes and export restrictions (resulting in negative market price support). Overall, negative MPS amounts to more than USD 104 billion per year.

The remaining support measures amounted to USD 447 billion per year, and are delivered in the form of budgetary payments and expenditures targeted to the agricultural sector (i.e. they represent transfers from taxpayers to producers, consumers, or to the sector as a whole):

Other most distorting support refers to subsidies linked to output or the unconstrained use of variable inputs (USD 66 billion per year), which have similar propensity to create market distortions to those generated by MPS.

Other producer support (USD 202 billion per year) includes payments based on land area, animal numbers, receipts or income, or payments not linked to the production of agricultural commodities, such as payments based on historical entitlements. These subsidies are considered to be “less coupled” to production and therefore more efficient in transferring income to the owners of land and other production factors. Payments can also be conditional on specific production practices and input uses designed to support environmental objectives. This category also includes specific payments designed to encourage farmers to adopt environmentally friendly technologies and practices.

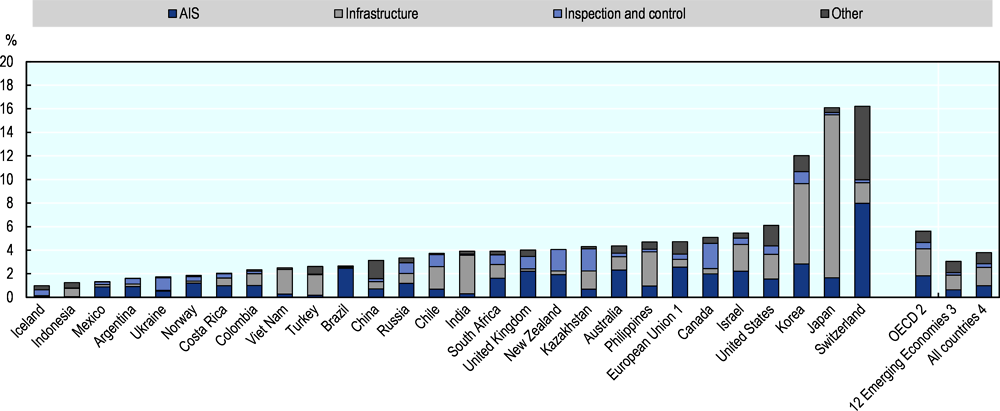

Policies that benefit the agricultural sector as a whole include investments in R&D and innovation, infrastructure (including off-farm irrigation systems, transportation and the provision of information and communication technologies), biosecurity, marketing and public stockholding. These policies are measured by the General Services Support Estimate (GSSE), which amounted to USD 102 billion per year, or 14% of all positive transfers to agriculture.

Subsidies for consumers (such as food assistance programmes) amounted to USD 78 billion per year, or 11% of all positive transfers to agriculture.

Notes: Data refer to the All countries total, including all OECD countries, non-OECD EU Member States, and the 12 Emerging Economies.

“Implicit taxation" of producers refers to negative market price support, “General services” refers to the General services support estimate, “Consumer support” is transfers to consumers from taxpayers, “Other most dist.” refers to the most distorting producer support measures other than market price support (i.e. support based on output payments and on the unconstrained use of variable inputs).

Due to missing value-added data, the Total support to agriculture in 2018-20 is related to agricultural value-added data for 2017-19.

Source: Based on OECD (2021), “Producer and Consumer Support Estimates”, OECD Agriculture statistics (database), https://doi.org/10.1787/agr-pcse-data-en.

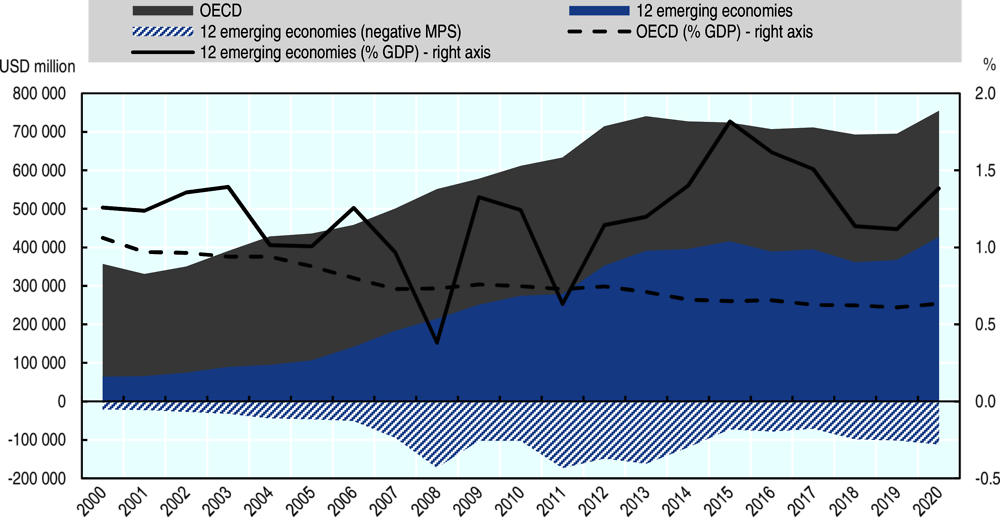

Total support to agriculture has grown considerably in nominal terms over the past two decades, largely driven by increasing support in large emerging economies (Figure 1.9). The nominal value of the total support estimate (TSE) for OECD countries has remained relatively stable, reaching USD 329 billion in 2018-20, with reforms stalling over the last decade following some previous reforms. At the same time, the share of total support in GDP has declined steadily from 1.0% in 2000-02 to 0.6% in 2018-20, reflecting the declining importance of the sector. In the 12 emerging economies, the TSE grew from USD 44 billion in 2000-02 to USD 280 billion in 2018-20, driven by increasing rates of producer support in the largest emerging economies – in particular, China, India and Indonesia. The TSE for emerging economies averaged 1.2% of GDP in 2018-20, reflecting the importance of support in the largest emerging economies, which are home to large agricultural sectors with sizeable agricultural populations. Additionally, emerging economies subjected their producers to more than USD 104 billion in negative market price support (i.e. implicit taxation) in 2018-20.

Notes: Negative MPS for OECD countries, mostly reflecting adjustments for higher feed costs due to positive MPS for feed commodities, averaged USD 427 million per year between 2000 and 2020, and is therefore too small to be visible on the graph.

The OECD total does not include the non-OECD EU Member States. Latvia and Lithuania are included only from 2004.

The 12 Emerging Economies include Argentina, Brazil, China, Costa Rica, India, Indonesia, Kazakhstan, the Philippines, Russian Federation, South Africa, Ukraine and Viet Nam.

Source: OECD (2021), “Producer and Consumer Support Estimates”, OECD Agriculture statistics (database), https://doi.org/10.1787/agr-pcse-data-en.

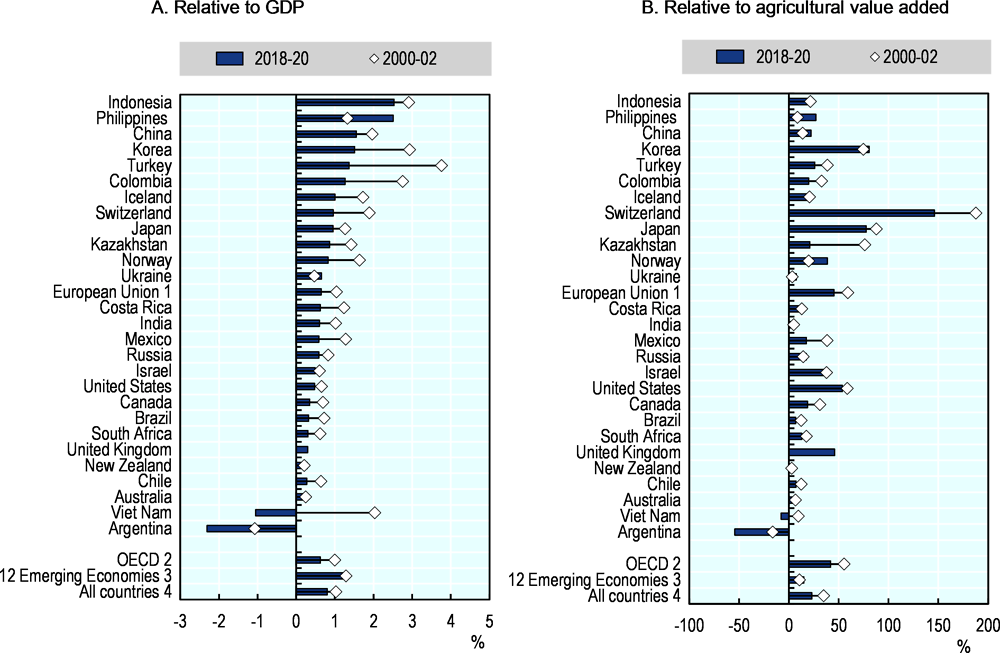

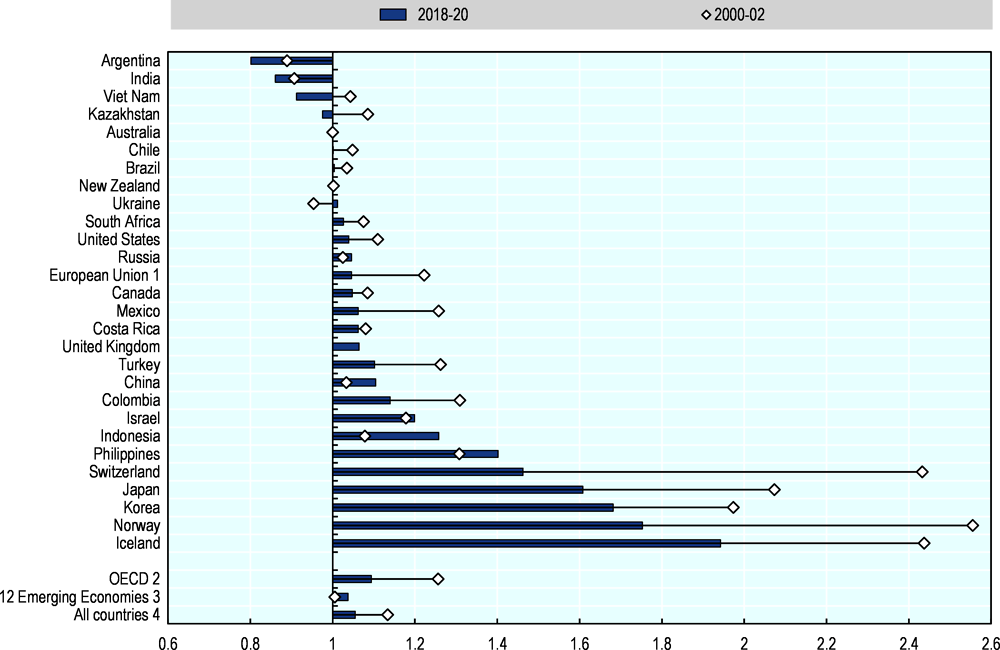

Aggregate figures mask the diversity in levels of support across countries (Panel A in Figure 1.10). The share of TSE in GDP (%TSE) indicates the cost of support to the sector for the overall economy. It was highest in Indonesia (2.5%), the Philippines (2.5%), and China (1.6%), partly reflecting the fact that agriculture has a comparatively high weight in the economies of these countries. The largest reductions in the %TSE since 2000-02 (in percentage points) have occurred in Turkey, Colombia and Korea – countries where the burden of support was initially high, but nonetheless still remained above 1.2% in 2018-20.

The level of total support in OECD countries continues to be high when measured relative to agricultural value added, amounting to 42% in 2018-20 (Panel B in Figure 1.10). Total support relative to the size of the sector varies widely across OECD countries, from 146% in Switzerland, 81% in Korea, and 78% in Japan, to less than 10% in just three countries: Australia, Chile and New Zealand. In comparison, total support in the 12 emerging economies represented just 15% of agricultural value added in 2018-20. The importance of support to the sector is highest in the Philippines (27%), China (22%), and Kazakhstan (21%). Total support is low relative to agricultural value added in India (4%) and Brazil (7%), and negative in Argentina and Viet Nam. The total effective tax on agriculture relative to the size of the sector was 54% in Argentina and 8% in Viet Nam.

Notes: Countries are ranked according to the %TSE in 2018-20.

Due to missing value-added data, the 2018-20 average TSE is related to agricultural value-added data for 2017-19 except for Japan and the United States (2016-18) and for Canada and New Zealand (2015-17).

1. EU15 for 2000-02, EU28 for 2018-19 and EU27 plus UK for 2020.

2. The OECD total does not include the non-OECD EU Member States. Latvia and Lithuania are included only for 2018-20.

3. The 12 Emerging Economies include Argentina, Brazil, China, Costa Rica, India, Indonesia, Kazakhstan, the Philippines, Russian Federation, South Africa, Ukraine and Viet Nam.

4. The All countries total includes all OECD countries, non-OECD EU Member States, and the Emerging Economies.

Source: OECD (2021), “Producer and Consumer Support Estimates”, OECD Agriculture statistics (database), https://doi.org/10.1787/agr-pcse-data-en.

The Producer Support Estimate (PSE) measures policy transfers to individual agricultural producers. Transfers to producers in the PSE comprise market price support (MPS) provided through domestic market prices that are higher (or lower if support is negative) than world prices, and budgetary payments from the government to farmers (Figure 1.7). The price gaps generated by trade policies and domestic market interventions are typically calculated as a differential between domestic and reference prices, but in some cases alternative methods are used for these calculations (Box 1.2).

Market price support (MPS) is defined as the “annual monetary value of gross transfers from consumers and taxpayers to agricultural producers, arising from policy measures that create a gap between domestic market prices and border prices of a specific agricultural commodity, measured at the farm gate level” (OECD, 2016[13]). It is calculated for individual commodities, as the gap between the domestic price paid to producers and the equivalent price at the border (market price differential, MPD), multiplied by the quantity produced, and aggregated to the national level.

This definition contains three key elements. First, it measures the transfers that arise from policy measures that create a price gap (e.g. import tariffs, minimum prices, export taxes, etc.). Second, it measures gross transfers (positive or negative) to agricultural producers from consumers and taxpayers. Third, it is measured at the farm gate level to ensure that MPS values are consistent with the production and price data for the farming sector overall.

The price gap (MPD) is calculated only if policies exist that can cause the gap such as border measures that restrict or promote imports or exports, and government purchases, sales and intervention prices in the domestic market. If countries do not implement such policies, the MPD is assumed to be zero. A non-zero MPD, whether positive or negative, originates from price-distorting policies. It is important to note that MPS measures the “policy effort” (or level of support to prices), not the policy effect (e.g. the impact on farm income). In addition to policy instruments that restrict price transmission (say, a target price), market developments (such as exchange rate movements affecting world prices expressed in local currencies) may influence the implied policy effort and, hence, the resulting transfers.

The calculation of the MPD for individual commodities based on prices requires information not only on product prices, but also on differences in product qualities, processing and transportation margins, to compare like with like. In some cases, difficulties in identifying and obtaining relevant prices or other required information prevent the MPD calculation from being based on observed price gaps. An alternative option for calculating the MPD is the use of import tariffs or export taxes (OECD, 2016[13]), which is likely to provide accurate MPS estimates only if a uniform tariff or tax rate is the sole border measures in place.

The use of tariffs rather than price gap data comes with a number of complex measurement issues, covering issues such as the composition of product groups across tariff lines and the seasonality of production and trade. Moreover, in order to capture the marginal rather than the average import protection rate, the statutory applied MFN tariffs are used. In light of the growing number of preferential trade agreements (PTAs) engaged in by countries covered by this report, an important caveat therefore relates to the fact that the statutory applied MFN tariffs remain unchanged even when increased quantities of products are imported under preferential tariffs or duty-free within such PTAs. As a consequence, potential liberalising effects of new PTAs are not reflected in the MPS estimates when tariffs are used to calculate them. With the increased relevance of PTAs for international trade, it therefore becomes even more important to base the MPD calculations on price gap calculations whenever data allow.

When interpreting MPS values, it is important to bear in mind that MPS is not a measure of public expenditures but an estimation of implicit or explicit transfers. MPS estimates published by the OECD therefore often differ from, and should not be confused with, those published by other organisations, including by the World Trade Organization, which may use very different concepts to calculate their indicators, despite similar names (Diakosavvas, 2002[14]; Effland, 2011[15]; Brink, 2018[16]).

Source: (OECD, 2020[3]).

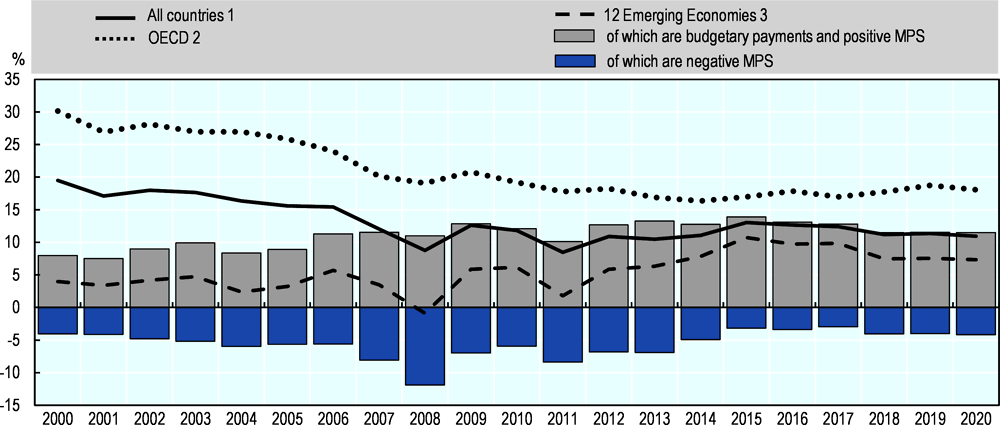

The average %PSE (producer support as a share of gross farm receipts) for all 54 countries has been declining over the past two decades, from 18% in 2000-02 to 11% in 2018-20 (Figure 1.11). Within this average is a clear pattern of a decreasing rate of producer support in OECD countries and increasing rate of producer support in emerging and developing economies from the beginning of the century until 2015. In OECD countries, the %PSE fell from 28% in 2000-02 to 18% in 2018-20. Most of this decline was driven by reforms initiated prior to 2008; the pace of decline has been markedly slower since and reversed to a slight increase after 2014. In contrast, the %PSE in emerging economies almost doubled from 3.8% in 2000-02 to 7.4% in 2018-20.

Notes: The two bars relate to the 12 Emerging Economies and represent a decomposition of PSE into its positive and negative parts.

1. The All countries total includes all OECD countries, non-OECD EU Member States, and the 12 Emerging Economies.

2. The OECD total does not include the non-OECD EU Member States. Latvia and Lithuania are included only from 2004.

3. The 12 Emerging Economies include Argentina, Brazil, China, Costa Rica, India, Indonesia, Kazakhstan, the Philippines, Russian Federation, South Africa, Ukraine and Viet Nam.

Source: OECD (2021), “Producer and Consumer Support Estimates”, OECD Agriculture statistics (database), https://doi.org/10.1787/agr-pcse-data-en.

The %PSE in emerging economies reached a peak of 10.8% in 2015 and subsequently declined to 7.4% in 2020. This is in part due to higher levels of negative market price support, which depressed the domestic prices of certain commodities in some of these countries. Indeed, the %PSE represents the balance of positive and negative MPS elements, and tends to underestimate the extent of price distortions when both positive and negative price support are present.

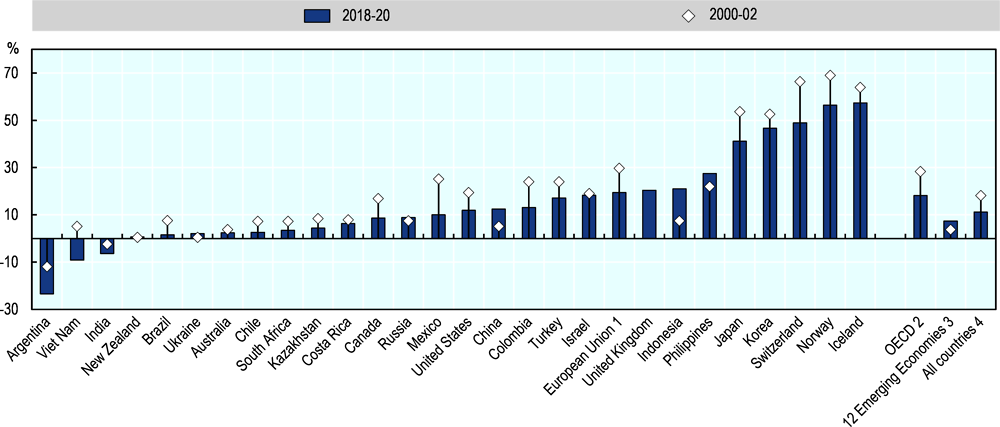

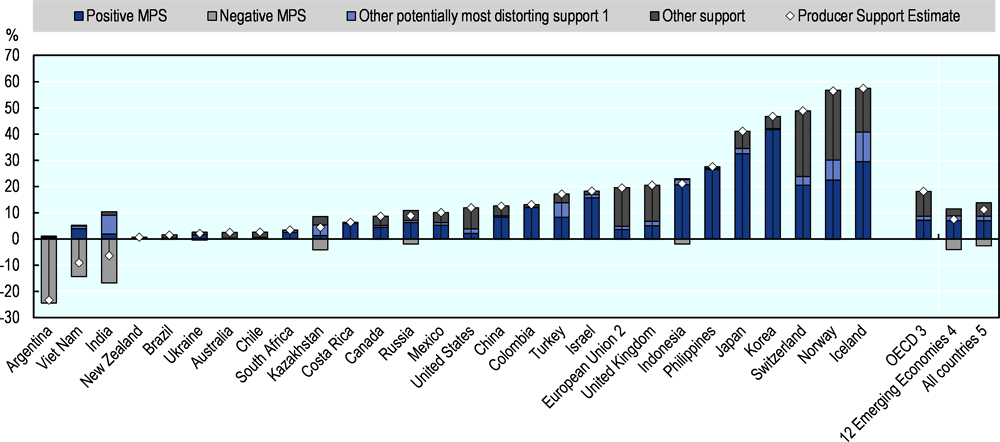

Support remains highly concentrated. In 2000-02 the overall value of producer support was concentrated in OECD countries, in particular the European Union, the United States and Japan. Since then, support in some large emerging economies (China, India and Indonesia) has become increasingly important. Four countries accounted for the vast majority of the aggregate net Producer Support Estimate in 2018-20: China (44%), the European Union (24%), the United States (10%) and Japan (9%). Negative market price support was predominantly provided by India (78%). The size of the agricultural sectors in these countries means that any policy will automatically result in large absolute numbers. For this reason, it is often useful to express the producer support estimate relative to gross farm receipts, as is done in Figure 1.12 below.

Countries differ widely in their tendency to support (or tax) their farmers. The countries with the highest levels of producer support when measured as a share of gross farm receipts are all in the OECD area. In Norway, Iceland, Switzerland, Korea and Japan, agricultural policy transfers arising from tariffs and other support measures generate between 40% and 60% of the revenues received by farmers. Producer support is above the OECD average of 18% in the Philippines, Indonesia, the United Kingdom, the European Union, and Israel. Seven countries have low levels of support, below 5%: Kazakhstan, South Africa, Chile, Australia, Ukraine, Brazil and New Zealand. Finally, three countries have negative levels of producer support, as a consequence of farmers facing implicit taxation through suppressed producer prices: Argentina, Viet Nam and India.

The level of producer support as a share of gross farm receipts has declined across OECD countries relative to the levels observed in 2000-02. Support has also declined in a number of emerging economies, notably Brazil, South Africa, Kazakhstan and Costa Rica. As mentioned previously, some of the larger emerging economies increased their level of support as measured by the %PSE, including Ukraine, Indonesia, China, the Philippines and Russia. Support to producers became more negative in Argentina and India, while Viet Nam’s %PSE turned from positive in 2000-02 to negative in 2018-20.

Notes: Countries are ranked according to the 2018-20 levels.

1. EU15 for 2000-02, EU28 for 2018-19 and EU27 plus UK for 2020.

2. The OECD total does not include the non-OECD EU Member States. Latvia and Lithuania are included only for 2018-20.

3. The 12 Emerging Economies include Argentina, Brazil, China, Costa Rica, India, Indonesia, Kazakhstan, the Philippines, Russian Federation, South Africa, Ukraine and Viet Nam.

4. The All countries total includes all OECD countries, non-OECD EU Member States, and the Emerging Economies.

Source: OECD (2021), “Producer and Consumer Support Estimates”, OECD Agriculture statistics (database), https://doi.org/10.1787/agr-pcse-data-en.

How do agricultural support policies affect food security and nutrition?

According to the FAO, “a person is food insecure when they lack regular access to enough safe and nutritious food for normal growth and development and an active and healthy life.” The severity of food insecurity can vary by time and degree, ranging from mild (uncertainty regarding one’s ability to obtain food) to moderate (compromising on food quality and variety, reducing food quantity, skipping meals) to severe food insecurity (no access to food for more than a day) (FAO, 2020[17]).

The world as a whole is not on target to achieve the United Nations Sustainable Development Goals target 2.1, of “ensuring access to safe, nutritious and sufficient food for all people all year round”, nor target 2.2, of “eradicating all forms of malnutrition”. While the proportion of people who are undernourished declined significantly over the past few decades, this trend has reversed in recent years. The prevalence of undernourishment increased from 8.6% in 2014 to 8.9% in 2019, and the absolute number of people affected by hunger increased by 60 million over the same period. Nearly 750 million people, or 10% of the world’s population, were considered to be severely food insecure in 2019, while an estimated 2 billion people (26% of the global population) experienced moderate or severe food insecurity, meaning that they did not have regular access to safe, nutritious and sufficient food.

Africa and Asia currently account for 92% of the world’s undernourished, or 631 million out of 688 million people. If current trends persist, the number of people affected by hunger is projected to exceed 840 million in 2030, of which 762 million (91%) will be in Africa and Asia. The COVID-19 pandemic has also led to a significant worsening of the situation, potentially resulting in an additional 83-132 million undernourished people in the world in 2020 (FAO, IFAD, UNICEF, WFP and WHO, 2020[18]).

Food security is linked to multiple areas of government policy, including macroeconomic policies that raise incomes and thereby improve access to food, trade policies that influence food availability, and public health and sanitation policies that improve food safety and nutritional outcomes. Tackling this complex and multi-faceted problem requires ensuring that sufficient food is available, that people have access11 to food, and that food leads to good nutritional outcomes. A fourth requirement is the stability of these three dimensions over time, which implies effective risk management (OECD, 2013[19]). This section assesses the specific impact of agricultural support policies on the four dimensions of food security: availability, access, nutrition, and stability.

Food availability

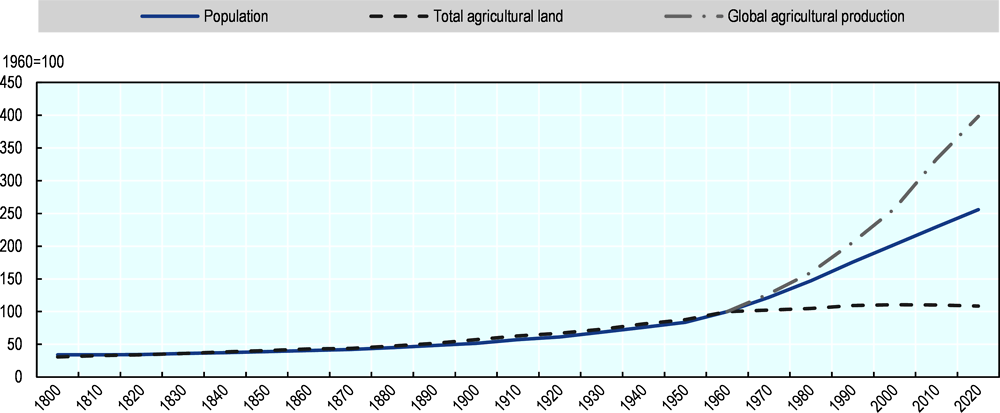

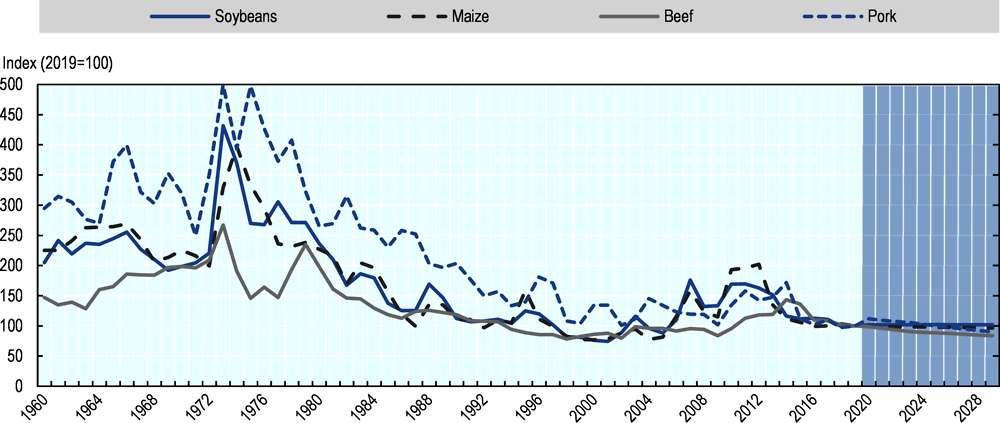

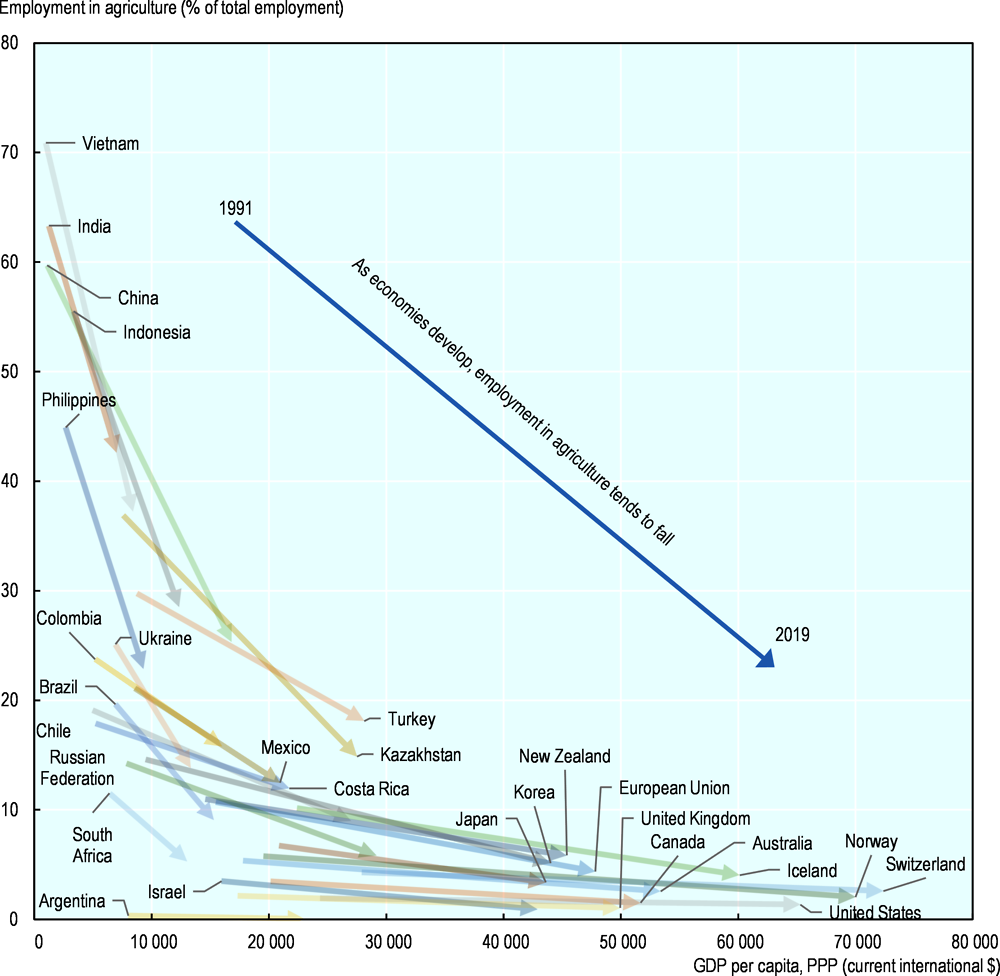

A global lack of food has not been a fundamental cause of continued food insecurity around the world. Global agricultural production has increased four-fold since 1960, with the amount of food available per person growing by 56%. This remarkable growth in supply can be largely attributed to productivity growth and yield improvements, as agricultural production has rapidly outpaced population growth and the expansion of agricultural land (Figure 1.13). The OECD-FAO Agricultural Outlook 2020-2029 projects that the pace of demand growth for agricultural commodities will slow over the coming decade, and will continue to be outpaced by efficiency gains in crop and livestock production (OECD/FAO, 2020[20]).

Sources: Population data from Maddison's historical statistics for 1820-1940; UN Population Division for 1950-2010; 1800 and 1810 extrapolated from Maddison. Agricultural (crops and pasture) land data for 1800-2010 from the History Database of the Global Environment (HYDE 3.2), Klein Goldewijk et al. (2017). Global agricultural production data for 1960-2010 from FAOSTAT (Net Agricultural Production Index); data for 2020 from OECD/FAO (2020), “OECD-FAO Agricultural Outlook”, OECD Agriculture statistics (database), https://doi.org/10.1787/agr-outl-data-en.

Even so, some countries have suffered from a lack of food availability due to prolonged conflicts and extreme fragility. More commonly, however, food insecurity in these countries is driven by poverty and a lack of access to food. Across 15 countries with a protracted crisis for which food price data are available, the cost of a healthy diet (USD 3.80) is roughly in line with the global average (USD 3.75), yet healthy diets are unaffordable for 86% of the population (compared with the global average of 38%) (FAO, IFAD, UNICEF, WFP and WHO, 2020[18]). Thus, the notions of food availability and access to food are closely linked.

Governments can improve the availability of food by stimulating the domestic supply of food with non-distorting policies (e.g. through productivity improvements, reduced post-harvest losses, or reduced diversion of food crops to biofuels), and by limiting excess food demand (e.g. through reductions in over-consumption and consumer waste). International trade also plays a vital role in increasing the availability of food by balancing the deficits of net food importers with the surpluses of net food exporters, and permitting an allocation of production across countries that reflects relative differences in resource abundance. Trade is particularly important for the food security of regions experiencing growing food demand, which often do not correspond to the areas in which supply can be increased in an efficient and sustainable manner.

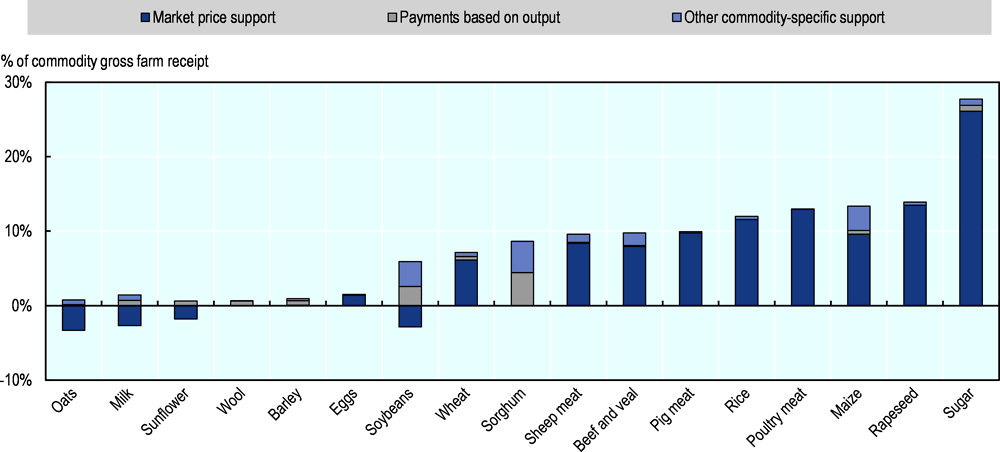

Agricultural support policies have adverse implications for global food availability by encouraging a sub-optimal allocation of resources, altering the relative mix of products grown, and displacing production to less efficient locations (OECD, 2016[21]). Many countries provide support to their agricultural sectors through measures that artificially stimulate domestic production and distort trade, with potentially significant consequences for global food availability. The most distorting measures – market price support, payments based on output and payments based on variable inputs without constraints – represent more than half of all transfers to and from producers in many countries, although some countries have implemented reforms that have decoupled support from production levels (Figure 1.14).

Agricultural support policies are therefore concentrated on measures that seek to increase domestic food availability, but often do so in an inefficient way (e.g. by raising prices), rather than through productivity-enhancing investments in R&D, innovation and infrastructure. These policies may contribute to domestic supply increases, but also encourage crops to be diverted away from human food consumption and towards the production of animal feed, biofuels, and the expansion of stocks (Pingali, 2015[22]). Policies to reduce the overconsumption of food and reduce food waste have so far had limited success, but can also play an important role in increasing domestic food availability.

Notes: Countries are ranked according to the %PSE levels.

1. Support based on output payments and on the unconstrained use of variable inputs.

2. EU28 for 2018-19, EU27 plus UK for 2020.

3. The OECD total does not include the non-OECD EU Member States.