Chapter 1. Environmental performance: Recent trends and developments

This chapter provides a snapshot of key environmental trends in Indonesia, highlighting some of the main achievements, remaining challenges and key policy responses. Beginning with an overview of the main socio-economic developments, the chapter presents Indonesia’s progress in moving towards i) an energy-efficient and low-carbon economy; ii) sustainable waste management and resource efficiency; and iii) sustainable management of its natural capital, such as biodiversity, forests and water resources.

The statistical data for Israel are supplied by and under the responsibility of the relevant Israeli authorities. The use of such data by the OECD is without prejudice to the status of the Golan Heights, East Jerusalem and Israeli settlements in the West Bank under the terms of international law.

1.1. Introduction

Indonesia is the world’s largest archipelagic country, and the fourth most populated one. It is one of the most biodiversity-rich countries worldwide, with extensive tropical rainforests, and possesses vast energy and mineral resources. The country has made great strides in improving its economic and social outcomes – it has enjoyed continuously strong economic growth since the end of the 1997-98 Asian financial crisis, reduced poverty and increased living standards. It has stabilised its democracy and devolved far-reaching decision-making and budgetary power to the local level.

Economic success has, however, come at high environmental costs. The expansion of agriculture to forests and peatlands, overuse of resources and pollution are putting serious pressure on Indonesia’s natural capital. Deforestation and forest degradation, combined with strong reliance on fossil fuels for energy generation, make Indonesia one of the world’s largest greenhouse gas (GHG) emitters. The rate of biodiversity loss is among the highest in the world and air pollution exceeds international guidelines. Infrastructure and service provision in the areas of waste, water and transport are not sufficiently developed to manage the pressures associated with population growth and urbanisation.

This chapter provides a snapshot of Indonesia’s main environmental achievements as well as remaining challenges on the path towards green growth. Based on the OECD green growth indicators as well as indicators from national and other international sources, the chapter reviews progress against national policy goals and international commitments, focusing on the period since 2005. To the extent possible, it compares environmental indicators with those of OECD member countries, other emerging economies and regional peers. The chapter summarises major policy developments in the main environmental sectors, including climate change, air, waste, water, and biodiversity and ecosystems.

1.2. Main economic and social developments

1.2.1. Economic performance

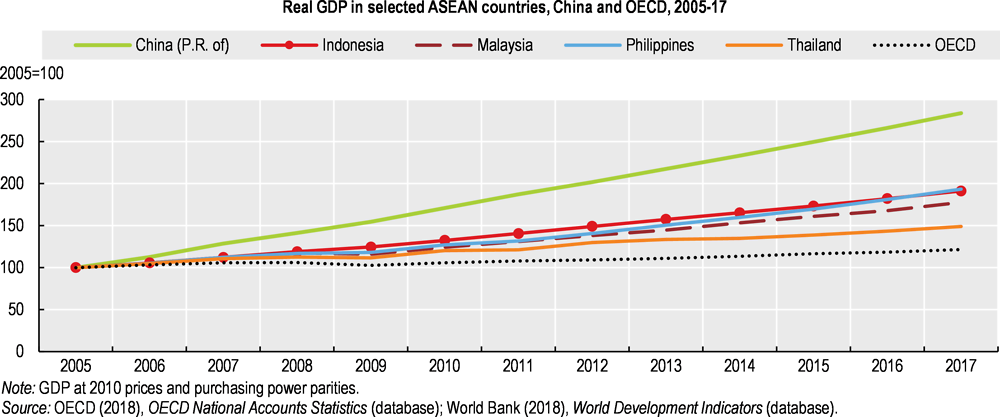

Indonesia is the largest economy in Southeast Asia and the 16th largest globally. Real gross domestic product (GDP) grew by 5.6% per year, on average, between 2005 and 2017, well above the OECD average and those of some regional peers (Figure 1.1). Growth was driven by a rising consumer base, improved labour market conditions, wage gains and effective poverty-alleviation programmes. As a natural resource-rich country, Indonesia also greatly benefited from the 2003-11 commodity boom (OECD, 2015). Relatively low dependence on international trade helped it weather the 2008-09 global financial crisis well. Growth decelerated to 4.9% in 2015 due to the commodity price slump, but edged back up to above 5% in 2016-18, aided by efforts to improve the business climate and public infrastructure investment.

The growth outlook is positive. Dynamic domestic consumption and continuously robust investment are expected to keep GDP growth above 5% in the years to come (OECD, 2018a; World Bank, 2018a). The main growth barriers include labour skill shortages, trade restrictions, infrastructure bottlenecks and a high (albeit declining) administrative burden. Reforms to fight corruption remain crucial to sustain strong growth (OECD, 2018a). OECD long-term projections suggest GDP growth will gradually flatten to just below 4% by 2030 and about 2.5% by 2050.1

Indonesia’s monetary and fiscal frameworks are strong. Monetary policy is supporting growth, and annual inflation is projected to remain stable. The government’s debt (28% of GDP) and fiscal position (2.5% of GDP) are below the constitution-set 60% and 3% ceilings and the respective OECD averages (see Basic statistics). Public spending is persistently low, constrained by low tax revenue. In 2014, Indonesia began to make the public spending mix more growth enhancing and efficient by reallocating expenditure from fossil-fuel subsidies towards investment in infrastructure, health and education (Chapter 2).

1.2.2. Structure of the economy and employment

Following the Asian financial crisis, Indonesia gradually moved away from an economy based on agricultural production to one based on manufacturing and services. The service sector has been the main growth engine and is now the largest contributor to the economy, accounting for 45% of GDP, with most value added coming from wholesale and retail trade, transport, communication and the finance, insurance and real estate sector. Tourism, at 4%, contributes a modest share by OECD standards but is growing fast, with an increasing number of visitors coming from China. Industry is the second-largest sector, accounting for 41% of GDP, with most value added coming from manufacturing, construction, and mining and quarrying. The agricultural sector accounts for 14% of GDP, which is high by international comparison, and it employs 30% of the population (compared to 17% in China or 43% in India). The service sector employed 48%, while manufacturing (14.1%), construction (6.7%) and mining (1.2%) accounted for the remainder (BPS, 2017; OECD, 2018a; World Bank, 2018b). According to OECD projections, the service sector will continue to expand to reach 57% in 2050, while the shares of industry and agriculture will decline to 38% and 5%, respectively.

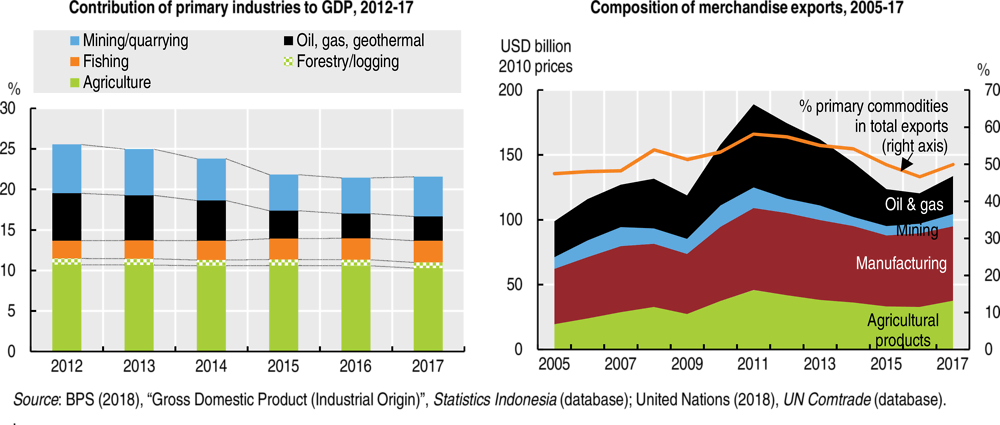

Natural resources are a pillar of the economy. The country is a major producer and exporter of minerals (e.g. nickel ore, bauxite, tin and copper), energy resources (steam coal, natural gas and crude oil) and agricultural products (crude palm oil, rubber, seafood, rice and spices). Taken together, natural resource-based activities accounted for 21.5% of value added in 2017 and made up half the country’s exports (Figure 1.2). Some provinces, including East Kalimantan, Riau and Papua, derive half their economy from natural resource-based activities. The contribution of extractive industries to GDP has declined since 2011 due to the fall in global commodity prices as well as legal and regulatory uncertainty, high administrative barriers, global competition and depletion of known reserves (particularly of tin, oil and gas). Non-oil and gas mining edged back up in 2017, however, aided by the recovery of global prices.

Indonesia is less integrated in the global economy than its regional peers. Trade accounts for a smaller share of GDP (42% in 2015) than in neighbouring Thailand, Malaysia and Viet Nam, and its share has been declining steadily since the Asian financial crisis. Restrictions on trade and foreign direct investment are relatively high, although some have been eased in recent years. For example, Indonesia imposed an export ban on unprocessed minerals in 2014, in a bid to support the domestic smelter industry, but later eased it in the face of dwindling revenue from mineral exports (Reuters, 2017; OECD, 2016a). Foreign direct investment remains constrained by foreign equity restrictions in several sectors, including energy and transport. Indonesia’s engagement in the ASEAN economic community since 2015 and the finalisation of pending free trade agreements (e.g. with Australia and the European Union) could help alleviate some of the pressures on trade (OECD, 2018a). Efforts to reduce burdensome administrative costs and increased investment in infrastructure should also help in this regard.

Labour market conditions have improved. The unemployment rate halved from 11.2% in 2005 to 5.5% in 2017 while real wages increased steadily, partially driven by rising minimum wages (BPS, 2017). However, stringent labour market regulations are curtailing formal-sector employment, particularly of low-skilled workers. An estimated 93% of firms and 70% of employment are informal (OECD, 2018a). Regional disparities are large, with unemployment ranging from 8.5% in Banten to 1.4% in Bali (Annex 1.A). The gender gap in the labour market has slowly improved but remains high, even by regional comparison. Youth unemployment stood at 19.4% in 2017, which is considerable given that half the population is under 30. Reaping the benefits of Indonesia’s youthful demographics will require shifting the job mix towards high-quality, high-productivity jobs in the formal sector (BPS, 2017; OECD, 2018a; ILO, 2017).

1.2.3. Inclusiveness of growth

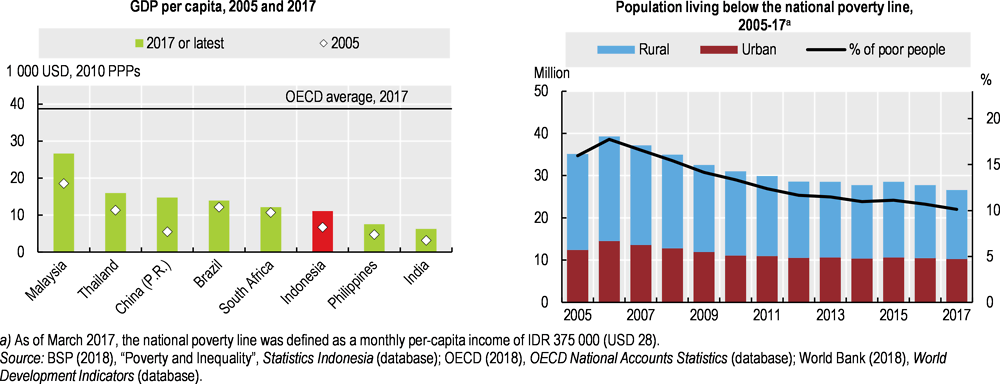

Robust economic growth was accompanied by a 64% increase in real GDP per capita over 2005-17, narrowing the income gap with other emerging economies, such as South Africa and Brazil (Figure 1.3). The share of people living in poverty declined from 16% from to 10% over the period, lifting 8 million people out of poverty (Figure 1.3). The middle class has rapidly expanded and now numbers more than 50 million people (World Bank, 2018c). Poverty remains more acute in rural areas, where access to income-generating opportunities is more limited. The government provides income support to poor households, including through cash transfers, a food subsidy programme, subsidised health insurance and a Village Fund, which aims to foster rural economic development. Public expenditure on social assistance more than tripled in real terms over 2005-16 (World Bank, 2017), strongly benefitting from a reduction in fossil-fuel subsidies (Chapter 2).

Income inequality, as measured by the Gini coefficient, has increased significantly over the last two decades, but started declining in 2015. It remains higher than the OECD average (see Basic statistics) but lower than in many neighbouring countries, including China, the Philippines, Malaysia, Singapore and Thailand. Fiscal policy has not been very successful in sharing the benefits of growth more widely: it is estimated that taxes and public expenditure reduce Indonesia’s Gini coefficient by only 0.04 points, compared to 0.18 points in South Africa (World Bank, 2018d). Regional income disparities are large, with per capita GDP in Jakarta and resource-rich provinces like East Kalimantan, Papua and Riau being significantly above the national average (Annex 1.A). High income levels in resource-rich provinces have not yet translated into lower poverty rates and higher household consumption, as a large portion of commodity revenue flows outside provinces (World Bank, 2016a; OECD, 2015; OECD, 2016a).

1.2.4. Administrative structure

Indonesia has 34 provinces, 410 districts (known as regencies) and 98 cities. Each province, district and city has its own administration,2 which has the right to establish local regulations. Subnational administrations have wide autonomy except on matters reserved for the central government.

Since 2001, Indonesia has undergone far-reaching political, administrative and fiscal decentralisation. As a result of this reform, provincial and local governments have gained more authority, including for natural resource management. The number of provincial and local regulations and policies have since increased significantly. The 2014 Law on Local Government strengthened provinces’ role in development, spatial planning and land administration. However, environmental management at the provincial and local levels is inconsistent. The 2009 Law on Environmental Protection and Management (LEPM) increased the power of the environment ministry to oversee compliance monitoring and enforcement activities by provincial and local governments. In recent years, the Ministry of Environment and Forestry (MoEF) has increasingly used such “second-line” enforcement, particularly in the environment sector. In 2015-16, 231 administrative sanctions were imposed as a result of these activities.

1.2.5. Population and urbanisation

With a total population of 264 million, Indonesia was the world’s fourth most populated country in 2017. Annual population growth has declined since the mid-2000s, but remains above 1%. The population is projected to reach 305 million in 2035 (MoEF, 2017a) and 319 million in 2050, according to OECD estimates. The population density is higher than in the OECD (see Basic statistics), although there are wide regional variations (Annex 1.A). The island of Java alone has 56% of the population, and the island of Sumatra a further 22%. Indonesia continues to urbanise at a steady pace. In 2017, 55% of the population lived in urban areas, up from 45% in 2005 (World Bank, 2018b). Urban areas face strong and mounting congestion costs, as evidenced by unmet demand for affordable housing and high traffic congestion levels (World Bank, 2018c). Access to basic facilities such as clean water, sanitation and electricity remains poorer in rural, especially remote and hard-to-access areas. An estimated 50 million to 70 million Indonesians live in customary or traditional (adat) communities (IWGIA, 2018).

Public health has improved markedly. The development of health care centres has made health services more accessible to the poor. Life expectancy at birth has increased by two years since 2005, while infant mortality has declined by 36% (World Bank, 2018b). Other health indicators are yet to improve, though: the maternal mortality ratio remains high at 126 deaths per 100 000 live births, and about one under-5 Indonesian out of three is affected by stunting (the world’s fifth highest prevalence rate). This is mostly due to malnutrition and limited access to improved sanitation and drinking water sources. Public spending on health, at 1.4% of GDP, is low compared to other middle-income countries. The gradual deployment of health insurance to attain universal cover by 2019 should further improve health outcomes (OECD, 2018b).

A massive increase in public education expenditure has helped boost primary school attendance to nearly universal education, as well as double teachers’ salaries and lower the teacher/student ratio. Still, expenditure remains low and inefficient by international standards. Improving teaching quality remains a challenge (World Bank, 2018d). The 2015 Programme for International Student Assessment (PISA) and a 2016 national test showed that three-quarters of 15-year-olds lacked basic science, mathematics and reading skills. PISA scores are similar to other developing countries, but show wide differences between cities and villages and between income groups (OECD, 2016a). Overall, half of 25- to 34-year-olds have not attained upper secondary education, which is twice the G20 average, although below Mexico (52%), China (64%) and India (64%) (OECD, 2018c).

1.2.6. Progress towards the Sustainable Development Goals and environmental quality of life

Indonesia has integrated Sustainable Development Goals (SDGs) into its national development vision, plan, policies and programmes (Chapter 2). It enacted a presidential regulation aimed at meeting the country’s SDG commitments and established a national co-ordination team within the Ministry of National Development Planning (BAPPENAS). On the Sustainable Development Solutions Network’s SDG Index, Indonesia performs well on poverty reduction and some per capita-based environmental indicators such as CO2 and SO2 emissions; it performs worse on access to water, sanitation and clean energy, as well as biodiversity-related metrics such as deforestation and species loss. Overall, the index ranked Indonesia 100th out of 157 countries in 2017, below peers such as Malaysia (54th), Thailand (55th), Singapore (61st), Viet Nam (68th) and the Philippines (93rd) (Bertelsmann Stiftung, 2017).

Indonesia’s Happiness Index ranking indicates that Indonesians are satisfied overall with their lives (BPS, 2018a). Education and household income are the two biggest areas of concern. Satisfaction with the state of the environment has marginally increased since 2014 and is high in all provinces, including those where environmental pressures are high. The Gallup World Opinion survey also revealed that a large majority of Indonesians were satisfied with air and water quality in 2014. This is at odds with the actual state of air and water bodies, and water-related infrastructure, in some areas.

The main indicator Indonesia uses to evaluate overall environmental performance is the Environmental Quality Index (EQI), introduced in 2009. A composite index with a value ranging from 0 (worst) to 100 (best), determined for both the provincial and national levels, it is based on a weighted average of three other indices: those for land cover (40%) and air and water quality (30% each). The national EQI oscillated around 64 points in 2013-16 (with a peak of 65.5 in 2015), a level classified as “bad” and below the target of 65.5 to 68.5 points set in the 2015-19 National Medium-term Development Plan (RPJMN). It has improved since 2016, but a change in methodology complicates comparisons with previous values or the 2019 target (BAPPENAS, 2017).3 Aggregate indices such as the EQI have the benefit of conveying a clear and simple message. However, condensing information about complex and multidimensional issues such as environmental quality increases the sensitivity of data deficiencies and risk of misinterpretation. It is important for Indonesia to complement EQI statistics with more disaggregated and accessible data, which could include environmental headline indicators.

Stronger efforts appear to be needed to raise the level of public environmental knowledge and awareness. Indonesia committed to providing environmental education in Law No. 32/2009 on Environmental Protection and Management. It also joined in the UN Decade of Education for Sustainable Development (2005-14). Law No. 32/2009 also includes the right to environmental information. In practice, however, many key company-level environmental data are not systematically and proactively disclosed (or reactively made available upon request) (WRI, 2017a). State of Environment reports used to be published almost annually but stopped in 2013 with the merger of the environment and forestry ministries. The MoEF still publishes an annual statistical report, but it does not cover all environmental media and lacks historical information. Regular publication of national and provincial State of Environment reports could help raise public environmental awareness. To enhance environmental education among the young, the MoEF launched the Adiwiyata eco-school programme in 2006, aiming to encourage schools to develop environment-friendly policies, integrate environmental issues into curricula and encourage participation-based environmental activities.

1.3. Transition to a low-carbon and energy-efficient economy

1.3.1. Energy structure, use and intensity

Indonesia has abundant energy resources and is among the world’s major energy producers and exporters. In 2016, it was the world’s fifth largest coal producer (and second largest exporter, after Australia), twelfth largest natural gas producer (and eleventh largest exporter) and second largest biodiesel producer after the United States (IEA, 2018). Nearly half of domestically produced energy is exported. Formerly a large crude oil exporter, Indonesia became a net oil importer in 2004, reflecting resource depletion and rapidly growing domestic demand. Net oil imports have more than doubled since 2000. Energy policy thus has a strong focus on energy security and self-sufficiency.

Energy mix

Indonesia’s energy mix relies on fossil fuels. They accounted for more than two-thirds of total primary energy supply (TPES) in 2016, including oil at 33% and coal and natural gas at 17% each (Figure 1.4). Renewable energy sources make up the remaining third, with primary solid biofuels (such as firewood for cooking) accounting for 24% of TPES. Modern renewables, excluding primary biofuels, accounted for 9.6%, mostly geothermal (8%), liquid biofuels (1%) and hydro (0.7%); energy from wind, solar and waste is negligible (0.001%). Since 2005, the use of modern renewables has increased only moderately (by 8.3 Mtoe), while fossil-fuel use has expanded nearly five times as much (by 38.1 Mtoe), driven by an increase in the use of coal (+77%) and natural gas (+32%) (IEA, 2018).

Indonesia’s carbon intensity of electricity generation is among the world’s highest. Electricity production relies almost exclusively on fossil fuels (87% of generated power in 2016). The use of coal has more than doubled since 2005 in absolute terms, increasing its share in total power generation to 54% in 2016 (Figure 1.4). Most coal-fired power plants use subcritical technology, i.e. the least efficient and most polluting form of coal-fired generation. The use of natural gas, which emits significantly less CO2 than coal per kilowatt hour, has nearly tripled, increasing its share to 26% of generation. The share of renewables in power generation decreased to 12.8% in 2016, one of the lowest values among OECD and G20 economies (Figure 1.4).

Aligning Indonesia’s energy policies with GHG emission reduction targets will be essential for achieving the country’s green growth objectives. The 2014 National Energy Policy (Kebijakan Energi National, or KEN), Indonesia’s overarching energy policy document, focuses on re-establishing Indonesia’s energy independence, which means minimising oil consumption while increasing exploitation and consumption of domestic coal, natural gas and renewables. KEN aims to reduce the share of oil in TPES to 25% by 2025 and source at least 30% from coal, 22% from natural gas and 23% from “new and renewable energy”4 (GoI, 2014a). In absolute terms, this means nearly doubling coal use (compared to 2015 levels), almost doubling natural gas use and increasing the use of renewables more than sixfold. The government justifies the continued focus on coal by citing a need to provide to affordable electricity for all. While most new coal-fired power plants are expected to be more efficient than the current fleet (based on supercritical or ultra-supercritical technology), the strong focus on coal for power generation puts into question the coherence of energy policy with climate change objectives (Section 1.3.3). Indonesia plans to review its targets in the new energy policy to better balance the goals of energy self-sufficiency and low-carbon development.

Deployment of renewable energy sources

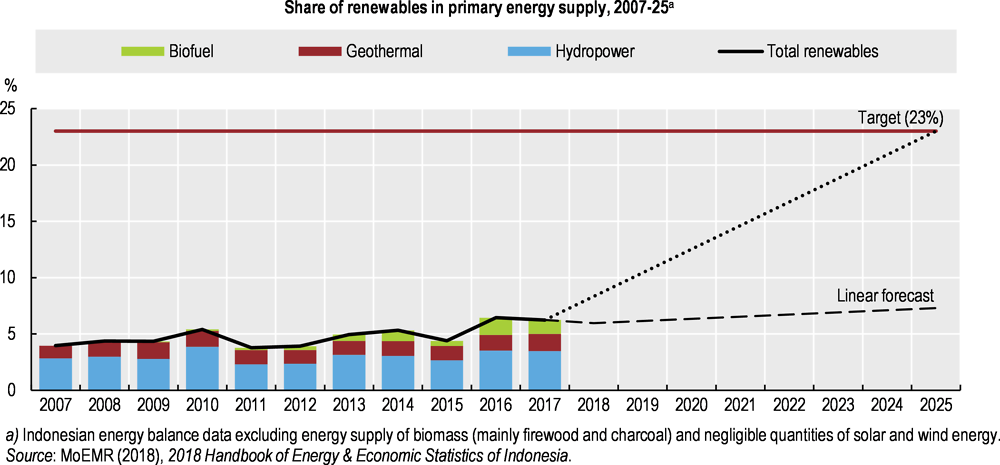

Indonesia has some of the world’s greatest potential for geothermal energy and hydropower, as well as abundant biofuel, tidal, solar and wind power resources. However, less than 2% of its renewables potential has been developed (Table 1.1). By national definitions,5 renewables excluding biomass accounted for 6.2% of TPES in 2017, up from 4% in 2007 (MoEMR, 2018). The increase was driven by liquid biofuels, supported by subsidies and ambitious blending mandates (Chapter 2), as well as additional hydropower and geothermal energy generation. Small wind and solar capacity started to be developed in the late 2000s, but their share in power generation remains negligible. In July 2018, the president inaugurated the country’s first large-scale wind farm (75 MW) in South Sulawesi.

Achieving the ambitious target of sourcing 23% of TPES from new and renewable energy sources by 2025 will require more effective policies. If renewables’ share in TPES increases at the same pace as over 2007-17, Indonesia will fall far short of its target (Figure 1.5). In the power sector, the share has actually decreased in recent years. The government has put in place several incentives to encourage renewables development, including feed-in tariffs, tax breaks and technology-specific funds, but these have not brought about investment as hoped due to financial, regulatory and technical barriers. Frequent policy changes around supportive measures and lack of strong political commitment have depressed investor confidence. While fossil-fuel subsidies have been markedly reduced (to 1.2% of GDP in 2017), they continue to disadvantage renewables vis-à-vis fossil fuels, coal in particular (Chapter 2).

Energy demand and intensity

Strong economic growth, rising living standards, population growth and rapid urbanisation have led to a continuous increase in energy consumption. Electricity consumption has nearly doubled since 2005, outpacing GDP and population growth (Figure 1.6). Most energy is consumed by the residential sector, followed by transport and industry (Figure 1.6). According to OECD projections, energy demand will double by 2040 and triple by 2060. Electricity demand is projected to double by 2030 and quintuple by 2060.

Energy intensity remains relatively low by international comparison. Energy supply per unit of GDP is 20% below the OECD average and lower than in China, India, Malaysia, Thailand and Brazil, for example (IEA, 2018). Energy supply per capita is 80% below the OECD average and considerably lower than in China, Malaysia, Thailand and Brazil (although not India). Per capita supply has increased by 11% since 2005, in part reflecting government efforts to improve energy access across the archipelago.

As GDP growth outpaced that of energy use, Indonesia’s energy intensity has improved by 27% since 2005 (3% annually, on average). This means the country is on track to surpass its target of decreasing energy intensity by 1% annually to 2025, set in 2005 in the Energy Conservation Master Plan. Further improving energy efficiency would bring large economic and environmental benefits, reducing the need to expand energy supply and curbing rising GHG emissions from energy use. Reaping these benefits will require better enforcement, greater stringency and broader scope of energy efficiency measures (Chapter 2). The manufacturing, service and transport sectors still show considerable potential for higher efficiency, as they lag behind international best practice benchmarks and often regional comparative benchmarks (Mersmann, Wehnert and Andreeva, 2017). The city of Jakarta has set a target of reducing energy consumption by 30% by 2030, compared to business as usual.

Access to energy

Indonesia has made major strides in increasing access to electricity and cleaner energy sources. The electrification rate rose from 53% in 2000 to over 91% in 2016 (BPS, 2018b), driven by government financial support to expand the electricity grid and disseminate solar-powered lamps (IEA, 2017).6 Wide regional disparity remains, with electrification being virtually universal in western Indonesia (e.g. in Jakarta) but as low as 42% in Papua (Annex 1.A). Countrywide, more than 10 million people still lack electricity access. Renewables have great potential for enhancing energy access in isolated and rural off-grid areas while providing co-benefits in the form of reduced air pollution and GHG emissions (for example, by displacing cooking wood, kerosene and diesel).

Access to cleaner cooking fuels has also improved considerably. The number of people without such access has declined by 55% (more than 100 million people) since 2000. This was driven by both urbanisation and policy efforts promoting a switch to liquefied petroleum gas (LPG), natural gas and electricity, including through the Kerosene-to-LPG Conversion Program (Chapter 2). The impact of these programmes has been more limited in rural areas, however, and about 25 million households (40% of all households) still rely on traditional biomass, especially wood, for cooking. Indoor air pollution caused by the use of solid cooking fuels is estimated to have resulted in over 45 000 premature deaths in Indonesia annually, with women and children particularly affected (WHO and UNDP, 2009). Other estimates are as high as 165 000 premature deaths per year (IRENA, 2017), more than double the estimated annual deaths from outdoor air pollution (Section 1.3.4).

1.3.2. Transport

The transport sector is defined by geography: the Indonesian archipelago is spread out over vast distances, making several areas difficult for movement of people and goods and costly to access. Improving connectivity across the country and integrating remote and frontier regions is therefore a government priority, with development of maritime transport being a key component.

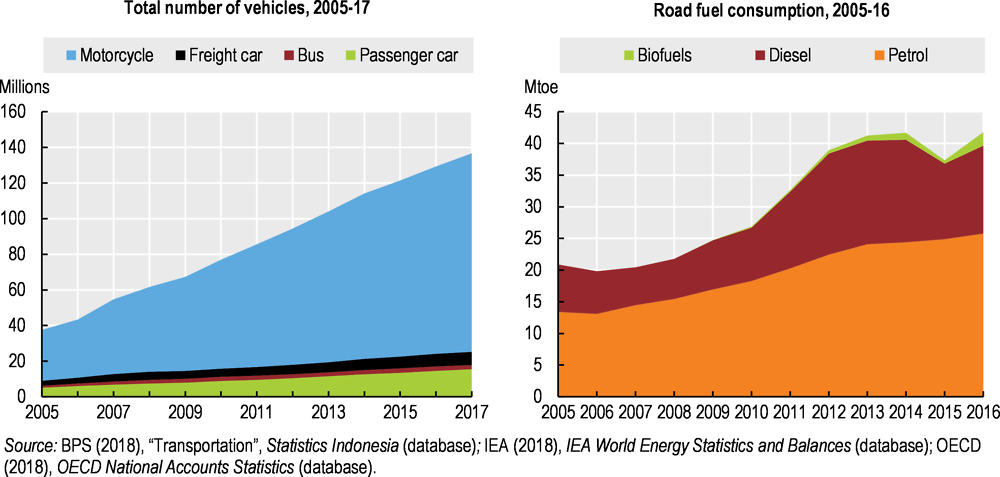

The transport sector is the second biggest energy consumer, accounting for 27% of final consumption in 2016 (IEA, 2018). Transport fuel consumption is rising fast (+86% over 2005-15), as are CO2 emissions (+82%). Road is the dominant transport mode for both freight and passengers (Table 1.2), accounting for nearly 90% of both energy use and CO2 emissions from transport. Air and rail passenger transport is gaining in importance, with air growing from 27 million passengers in 2006 to 96 million in 2016, and rail from 12 million to 35 million (World Bank, 2018; BPS, 2018c). Sea transport is important for freight and is relatively well developed, while inland waterway transport is limited to parts of eastern Sumatra and Kalimantan (Cekindo, 2018a). The RPJMN aims for a shift from road to rail and shipping.

The number of vehicles on the streets has increased massively. The average annual growth in passenger car numbers was above 10% between 2005 and 2016, while motorbike numbers rose by 12% annually (Figure 1.7). With 55 cars per thousand inhabitants, Indonesia’s vehicle ownership remains below the OECD average, although the gap is much narrower when motorbikes are included. Petrol is the dominant fuel in road transport, accounting for 64% of fuel use in the sector, while diesel accounts for 34% and biofuel for 3% (Figure 1.7). Ambitious biofuel blending requirements (Chapter 2) and a series of fiscal incentives will raise this last share further. The government aims to increase the number of electric vehicles, but development of the market has been slow (Chapter 2).

The rapid growth of the vehicle fleet, coupled with insufficient road infrastructure expansion and limited spending on public transport and transport demand management, has caused crippling congestion in cities. Jakarta was considered the world’s third most congested city in 2017, after Mexico City and Bangkok (TomTom, 2018). The capital’s traffic congestion was estimated to have caused economic losses of IDR 67 trillion (USD 5 billion) that year, or IDR 100 trillion (USD 7 billion) for the greater metropolitan area (BPTJ, 2017). Road occupancy, measured as vehicle kilometres per paved lane kilometre, is estimated to be the world’s second highest. As a consequence, about one-third of Indonesian fuel use is wasted in stationary traffic (IEA, 2015).

Recent increases in public infrastructure investment (e.g. in mass rapid transit and light rail transit) in Jakarta and a few other major cities is showing some positive impact in reducing congestion and logistics costs. Jakarta is also implementing an odd-even licence plate rule to limit the number of cars on the roads, although the policy risks encouraging the purchase of a second car by those who can afford it. As Chapter 2 notes, vehicle taxes are high, but are not an incentive to buy lower-emission vehicles. There is scope to strengthen standards for fuel efficiency and vehicle emissions, especially for trucks, to reduce GHG and air pollutant emissions.

1.3.3. Climate change

GHG emission profile

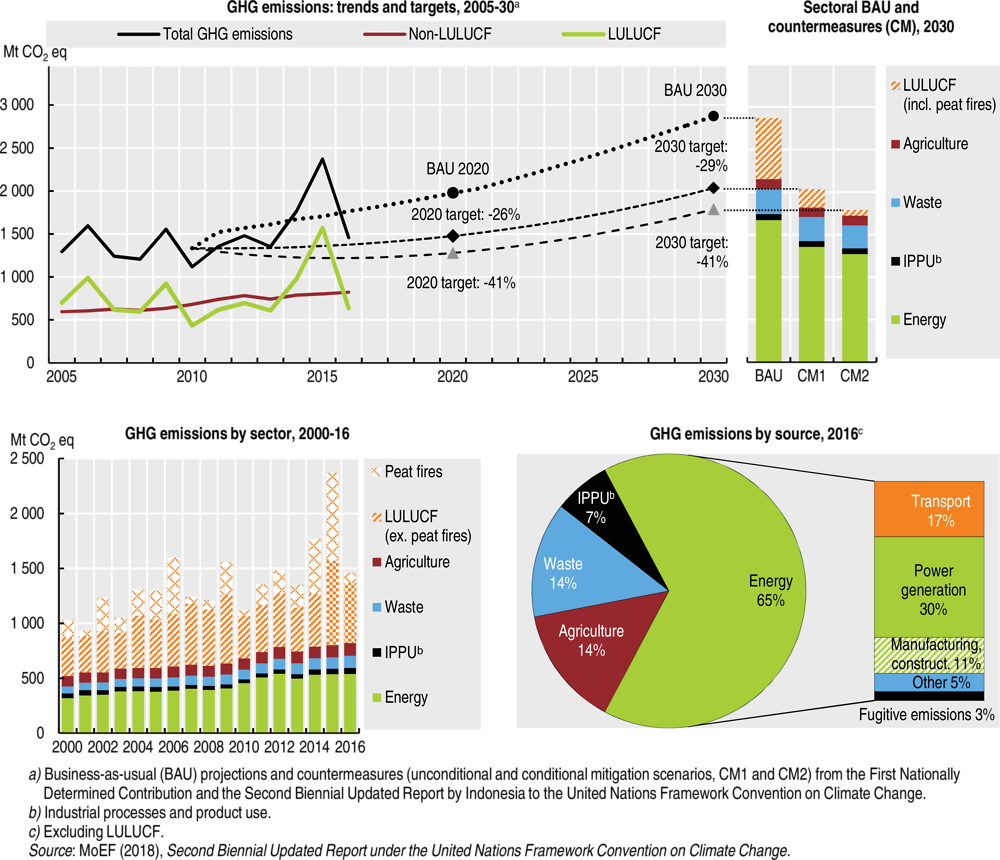

The latest available national GHG inventory reported that GHG emissions, including land use, land-use change and forestry (LULUCF), reached 1 458 million tonnes of CO2 equivalent (Mt CO2 eq) in 2016 (MoEF, 2018a). This makes Indonesia one of the world’s ten largest emitters (WRI, 2018a). GHG emissions increased by 42% between 2000 and 2016, or 2.2% per year, on average. OECD countries reduced emissions by 6.7% over the same period (OECD, 2018d). CO2 is the main GHG, contributing 82% of total emissions, while methane contributed 13% and nitrous oxide 4.3% (MoEF, 2018a).

LULUCF emissions dominate Indonesia’s GHG emission profile, although levels of CO2 emitted and sequestered by the sector fluctuate significantly from year to year (Figure 1.8). LULUCF emissions are mainly caused by conversion of carbon-rich forest and soil to agriculture (particularly oil palm plantations) and logging (particularly timber harvesting), as well as forest and peat fires. Peatland burning and decomposition have a double effect on climate change, as these areas hold significant carbon stocks (Chapter 3). In 2015, a year with an extremely dry rainy season connected to a strong El Niño event, LULUCF emissions reached 1 569 Mt CO2 eq, more than Indonesia’s total emissions in 2016 (and more than Germany’s or Japan’s emissions). On average, Indonesia’s LULUCF emissions are among the highest in the world, although data are difficult to compare.

Aside from LULUCF, energy is the largest sector for GHG emissions, accounting for 37% of total GHG emissions in 2016 (or 65% of emissions excluding LULUCF). The remainder is from agriculture (14%), waste (14%) and industrial processes (7%) (MoEF, 2018a). Emissions from the energy sector increased by nearly 70% between 2000 and 2016 (Figure 1.8). Energy-related emissions mainly come from fuel combustion for power generation (which accounted for 30% of emissions excluding LULUCF in 2016), transport (17%) and manufacturing and construction (11%); smaller shares come from the residential sector, petroleum and gas refining, fugitive emissions and other sources (Figure 1.8).

Indonesia has achieved a relative decoupling of economic growth from GHG emissions: emission intensity declined between 2005 and 2016, both including and excluding LULUCF emissions (-38% and -24%, respectively). Excluding LULUCF, the emission intensity is similar to the OECD average; including LULUCF it is nearly twice the OECD average. Emissions per capita have increased by 29% since 2005, but are still low by international comparison (OECD, 2018d). Per capita emissions are expected to continue to grow to 2030, according to government projections.

Indonesia has strengthened its GHG emission inventory arrangements through regulations and other measures.7 Continued efforts are needed to synchronise provincial GHG emission data and improve their quality. Official data on provincial GHG emissions are collected through a system called SIGN SMART but not synchronised, monitored, or linked with national targets. Data compiled by the World Resources Institute (WRI) suggests most emissions originate in North Sumatra province (likely due to significant deforestation), followed by Riau, East Java, Central Kalimantan and Lampung. Deforestation is the largest emission source in most provinces, but energy-based emissions dominate in at least ten provinces, including several in Java (WRI, 2018c). Central Kalimantan registers the highest emissions relative to population and GDP.

Indonesia’s online monitoring, evaluation and reporting system, PEP online, provides data and monitoring and evaluation processes for mitigation and adaptation action plans. It includes a provincial breakdown for potential emission reductions from implementation of mitigation activities. In addition, the National Registry System compiles climate action, resources and potential emission reductions from climate action conducted by national and subnational government as well as private and civil society actors. These systems could be integrated and synchronised to monitor progress against Indonesia’s climate targets.

Mitigation targets

In 2009, Indonesia adopted a voluntary target of reducing emissions by 26% from a business-as-usual (BAU) scenario by 2020 using domestic efforts. A further 15% reduction target (taking total reduction to 41%) is conditional on receipt of adequate international support. This pledge was confirmed in Presidential Regulation No. 61/2011 on the National Action Plan for Reducing Greenhouse Gas Emissions (RAN-GRK). Indonesia’s Nationally Determined Contributions (NDC) set an unconditional reduction target of 29% of BAU by 2030 and a conditional reduction target of up to 41%, subject to international assistance for finance, technology transfer and capacity building. Indonesia ratified the Paris Agreement in October 2016. Work is ongoing with respect to development of mitigation scenarios beyond 2030.

The latest BAU scenario, reported in the second Biennial Update Report under the United Nations Framework Convention on Climate Change (MoEF, 2018a), projects emissions in 2030 at 2 869 Mt CO2 eq, more than 1 000 Mt CO2 eq above current levels. This scenario translates into unconditional maximum emission targets of 1 581 Mt CO2 eq for 2020 and 2 035 Mt CO2 eq for 2030 (Figure 1.8). The steep increase in the baseline is driven by emissions from energy use, which are projected to more than triple over 2016-30, replacing LULUCF as the largest emitting sector by the mid-2020s. Even in the most ambitious mitigation scenario (the -41% target), energy emissions would nearly double from current levels (Figure 1.8). This has caused criticism of Indonesia’s NDC ambition as “highly insufficient” in terms of the global goal of limiting warming to 2°C (CAT, 2017). Indeed, the BAU scenario can be considered conservative, as it assumes there would be no additional renewables capacity after 2010 and no energy efficiency improvements, for example (Mersmann, Wehnert and Andreeva, 2017; IRENA, 2017).

The government reported that annual emissions in 2010-16 were below BAU except in 2014 and 2015, when emissions from peat fires peaked. In 2016, emissions were 14% below BAU, meaning Indonesia was about halfway to achieving its 2020 target (MENKO, 2018). At the same time, the government acknowledged that more effort was needed to bring emissions from forestry and energy on track to meet the 2030 target (MENKO, 2018). This is in line with WRI projections (2017b), which suggested that emissions from the land-use and energy sectors alone were likely to miss the 29% reduction target for 2030 if existing policies (as of late 2017) were not strengthened.

Climate policy

The RAN-GRK forms the cross-sector framework for Indonesia’s climate strategy. Formulated by BAPPENAS, in co-operation with other ministries, it includes 50 mitigation plans for five sectors: agriculture, forestry and peatland, energy and transport, industry, and waste. Provincial action plans were also developed, with BAPPENAS mandated to co-ordinate their evaluation and review, in collaboration with the Ministry of Home Affairs and the MoEF. The government is reviewing the RAN-GRK in the context of the 2030 commitment in the NDC, which sets the framework for climate action after 2020. The government plans to mainstream the 2030 target into the 2020-24 RPJMN, which is expected to become the country’s first low-carbon plan (Chapter 2). Indonesia has made progress with respect to the regulatory and planning framework for climate finance, for example with the development of climate budget tagging, green budgeting and planning, and the issuance of green bonds (Chapter 2).

Mitigation policy is chiefly focused on land use. The RAN-GRK allocated 88% of emission reduction to 2020 to the forestry and peatland sector (and only 5% to energy and transport), while the NDC expects land use and forestry to deliver about 60% of the 2030 target (MoEF, 2015a; MoEF, 2017a). Indonesia has taken important steps in addressing land-based emissions, such as updated forest and peatland regulations (including a moratorium on new peatland conversion permits), better law enforcement, a new focus on social forestry and enhanced efforts to control forest and peat fires (Chapter 3). The government committed to reduce deforestation and to restore 12 million ha of degraded land and 2 million ha of peatland. Thanks to these measures, the forestry sector was the biggest contributor to emission reduction in 2016 and 2017. Still, the 2030 mitigation target for the forestry sector appears quite ambitious, requiring almost zero net emissions by 2030 under the 41% reduction scenario (Figure 1.8). Reaching this target will require strengthened forest governance and compliance with land-use regulation. Extending and strengthening the forest and peat moratoriums (which prohibit issuance of new licences on primary forest and peatland) is widely recognised for its large, cost-effective mitigation potential (WRI, 2017b; JICA/DNPI, 2014).

Efforts to decarbonise the energy sector need to accelerate. The focus of mitigation has been on fuel switching, energy efficiency and public transport (MoEF, 2017a). At the same time, plans to expand coal-fired power generation potential drastically reduce the sector’s mitigation potential and risk locking-in high-carbon infrastructure on a large scale and for decades to come. The Intergovernmental Panel on Climate Change (2018) noted that investment in unabated coal would need to halt by 2030 to be consistent with the 1.5°C scenario; its use in power generation would need to stop by 2050. Setting targets for energy sectors (power generation, transport, etc.), broken down into short-term goals and clear responsibilities for different actors, could help structure and accelerate the energy transition. Phasing out fossil-fuel subsidies and pricing carbon emissions from energy use would contribute to better alignment of energy and climate policy objectives (Chapter 2).

Indonesia established the National Council on Climate Change in 2007 as an inter-ministerial co-ordination body for climate change policies and positions, headed by the president. In 2015, it became part of the Directorate General of Climate Change in the newly established MoEF, along with Indonesia’s REDD+ body, the aim being to make climate policy co-ordination more effective. As in many countries, climate policy is fragmented across institutions, including the MoEF, BAPPENAS (which retains the legal mandate to co-ordinate the RAN-GRK), the Ministry of Finance (which oversees climate finance) and line ministries.

Continued efforts are needed to build a strong monitoring, reporting and verification (MRV) system. The MoEF has developed a national carbon accounting system that can provide the basis for a strong MRV system. Efforts are underway to enhance the flexibility of this system to fit policy requirements, produce UNFCCC-compliant reports, develop projections to support NDCs, and support broader land-use planning and tracking of policy outcomes, including co-benefits. The government recognises the need to improve the calculation of GHG emissions, the annual baseline and sectoral reduction targets to provide a credible reference making it possible to track progress and assess climate policies’ effectiveness (MENKO, 2018). Tracking progress towards the reduction targets has not been straightforward because the BAU scenario, on which the mitigation targets are based, has been updated several times. Hence the sectoral mitigation targets do not match the legal target of 41% but add up to 38% instead. Work to address this discrepancy is ongoing.

Climate change vulnerability and adaptation policy

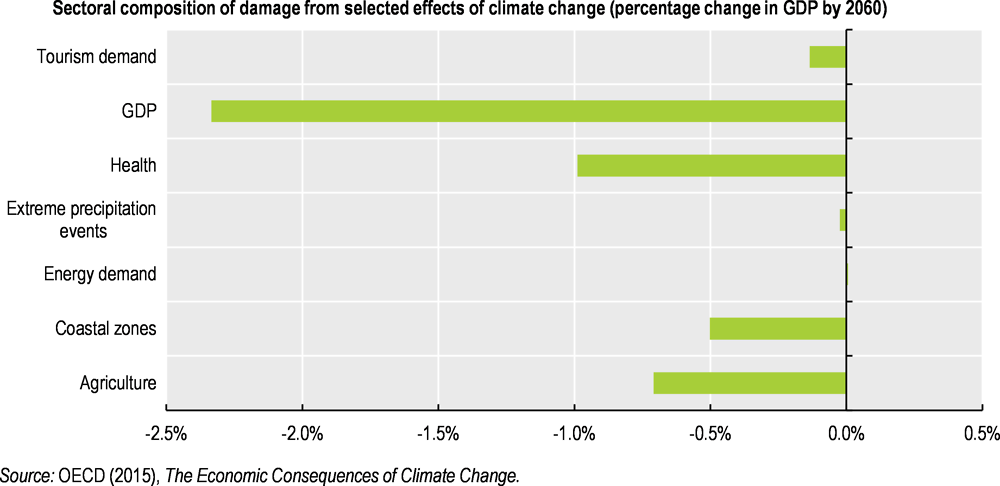

Indonesia’s geographical and socio-economic conditions make it vulnerable to natural disasters, including extreme weather and climate change (MoEF, 2017a). While its climate has historically been affected by decadal variability, influenced by the El Niño and El Niña Southern Oscillation, long-term temperature and rainfall trends are rising. Climate-related disasters, such as floods and landslides, have increased, especially on the islands of Sulawesi, Kalimantan and Sumatra. Projections indicate that surface temperatures will continue to increase until 2100; rainfall will become lower during dry season and stronger during rainy season and transition periods.8 Extreme climate-related events are therefore expected to become more frequent and intense. The OECD projects that overall climate change damage will reach about 2.3% of GDP by 2060. Most of the damage is expected to stem from the impact on health, agriculture and coastal zones (Figure 1.9). Sea level is projected to rise between 0.6 cm and 1.2 cm per year, which could cause flooding of productive coastal zones that are home to more than 180 million Indonesians (MoEF, 2017a; World Bank, 2018e).

The 2014 National Action Plan for Climate Change Adaptation (RAN-API) is under review. It identified 43 adaptation programmes in four areas: economic resilience (food resilience and energy independence), livelihood resilience (health, residential areas and infrastructure), ecosystem resilience and resilience of specific locations (cities, coastal areas and small islands). It also aims to strengthen support such as capacity building, planning and budgeting, and monitoring and evaluation. Like the RAN-GRK, the RAN-API is co-ordinated by BAPPENAS. Provinces are expected to develop their own action plans, but uptake has been slow, with only eight provinces having adopted one so far. To accelerate the process, the MoEF issued a regulation in 2016 providing guidance on the formulation of local adaptation action plans. A vulnerability index, currently under construction, could be used to develop a comprehensive, evidence-based adaptation strategy that is based on vulnerability assessments, includes milestones and can be monitored and broken down subnationally.

1.3.4. Air pollution

Emission of atmospheric air pollutants

According to the EDGAR global emissions model, local air pollutant emissions increased over the 2000s, although slower than GDP growth (Figure 1.10). Growth was strongest for emissions of nitrogen oxides (NOX) and sulphur oxides (SOX), reflecting vehicle fleet growth (as well as poor fuel quality and vehicle standards) for NOX and expansion of coal-fired power generation for SOX. Large forest and peat fires (neither of which are considered in the model) lead to pollution peaks in Indonesia and neighbouring Malaysia and Singapore, although efforts to reduce fires have started to bear fruit (Chapter 3). Peat fires are of particular concern, as they cause up to 90% of haze and release three to six times more particulate matter (PM) than fires on other types of soil (World Bank, 2016b).

National data on pollutant emissions are limited. Operators of large facilities (that are subject to emissions regulations) are obliged to equip their facilities with emission controls and report the results to the local government, with a copy to the MoEF. In practice, however, the MoEF mainly relies on a voluntary performance assessment programme, PROPER (see Box 2.5 in Chapter 2), to assess and monitor air pollution from industry. The establishment of an electronic environmental reporting system for PROPER-participating companies in early 2018 is expected to improve data collection. It could build the basis for a comprehensive national inventory of stationary-source air emissions. In addition, emission inventories have been developed for 11 cities since 2010. Emissions from mobile sources are not collected systematically.

Ambient air quality

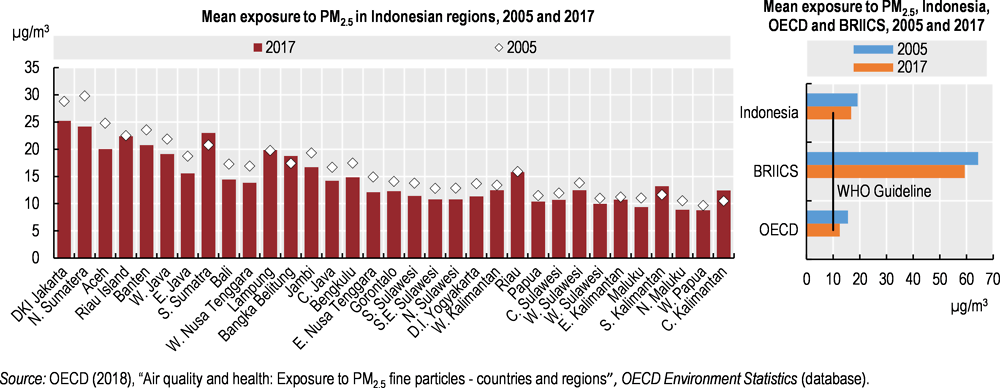

OECD data based on satellite observations suggest that 95% of the population is exposed to harmful levels of air pollution, i.e. more than 10 µg/m3 of PM2.5, which is the World Health Organization (WHO) guideline value (OECD, 2018e).9 Exposure to air pollution varies significantly across the country (Figure 1.11). Jakarta has had the highest exposure rates over much of the past decade, and provinces on Sumatra and Kalimantan experience high peak exposures during forest fires. In 2017, national mean exposure to PM2.5 reached 16.7 µg/m3, above the OECD average, though much below those of other emerging economies such as India and China. The Indonesian Air Quality Index (AQI), the main domestic indicator of air quality (a 0- to 100-scale composite index), deteriorated in the early 2010s, but has improved in recent years. In 2017, it reached 87, above the government’s target value of 84 for 2019 (MoEF, 2017b).10

The number of premature deaths related to ambient PM2.5 and ozone pollution has risen steadily to reach more than 200 per million inhabitants in 2017 – a value that remains below the OECD average (380 premature deaths) and the ASEAN average (260 premature deaths) (OECD, 2018e). The associated health cost and economic consequences were valued at 1.2% of GDP. The World Bank (2016b) estimates that the large 2015 forest and peat fires alone cost Indonesia at least USD 16 billion (equivalent to 1.9% of GDP) and caused 500 000 cases of acute respiratory infection. Acid rain, an indicator of declining air quality associated with NOX and SOX pollution, is becoming a concern, affecting water ecosystems, soil and buildings (Yudha, 2017).

Indonesia’s air quality monitoring system, run by the MoEF, has two components: i) the National Air Quality Monitoring System (AQMS), which continuously monitors CO, SO2, NO2, ozone, PM10 and PM2.5 concentrations in 14 large cities; and ii) “passive sampling” at roadsides in about 50 cities.11 The MoEF is increasing the number of cities in the AQMS, aiming to reach 45 cities by 2019. By early 2019, 49 stations had been installed in 40 cites. Other national, local and non-government institutions conduct air quality monitoring but do not always share the collected data (OECD, 2016b).

Main policies and measures

Government Regulation No. 41/1999 on Air Pollution Control, complemented by ministerial regulations, specifies ambient air quality standards for all major pollutants, as well as emission standards for industrial activities and motor vehicles. Air quality standards are generally less stringent than global WHO guideline values (OECD, 2016b) and some emission standards are more lax than international best practice. For example, PM standards for new coal-fired power plants are three times higher than in India, and ten times higher than in the EU (Table 1.3). Standards for the pulp and paper industry are also low by international comparison. In a welcome step, emission standards for the cement industry were raised in 2017 and the government plans to update standards for coal-fired power plants in 2019. In addition, in March 2017, the MoEF signed a long-awaited regulation stipulating Euro 4 emission standards for four-wheel vehicles. Since 2005, Indonesia had used Euro 2 for passenger cars and Euro 3 for motorcycles, one of only three Asian countries to do so. It is one of the few countries still using RON 88 petrol (locally known as “premium”), a low-quality fuel that contributes to air pollution (Ompusunggu, 2017).

As part of its overall goal to improve air quality, Indonesia set a target of reducing air emissions by 15% between 2014 and 2019, to be achieved through reductions at both stationary and mobile sources. To support emission reductions by industry, the government issued technical guidelines and launched a Green Boiler Program to encourage companies to improve their boilers’ performance. However, participation has been relatively low (MoEF, 2016). The MoEF reported that industrial emissions declined by 10% over 2014-16, but the assessment was based on a small sample of 66 companies in the PROPER programme (MoEF, 2016). The main strategy to reduce emissions from mobile sources has been the Green Transport concept, which supports cities in shifting towards sustainable transport. The concept was tested in three cities in 2016 and the MoEF aims to increase the number to 45 by 2019. As part of the strategy, the MoEF issued guidelines on air pollution control in residential areas and developed a website presenting regencies and cities’ air quality status on a continuous basis.

To tackle air pollution in a comprehensive and integrated manner, Indonesia needs to continue improving its monitoring system for air emissions and ambient air quality. Information about emissions’ source and location is a condition for development of targeted policies, assessment of policy effectiveness, and enforcement of standards. Given their weight in emissions, road transport, power generation and agriculture deserve more policy attention. While the issuance of the Euro 4 standard is welcome, vehicle testing and enforcement remain weak (IEA, 2015). Jakarta is stepping up action in this regard. The city furthermore holds air quality forums with stakeholders, restricts vehicle circulation through an odd-even system and car-free days, and is expanding public transport and electronic pricing on highways. This will bring lessons for other cities and provinces. Industrial emissions should be monitored carefully and not only among companies participating in PROPER. Emission standards for heavily polluting industries should be raised closer to international ones, particularly those of coal-fired power plants, given the additional capacity planned for the coming decades.

1.4. Transition to a resource-efficient economy

1.4.1. Waste management

Generation, collection and disposal of municipal solid waste

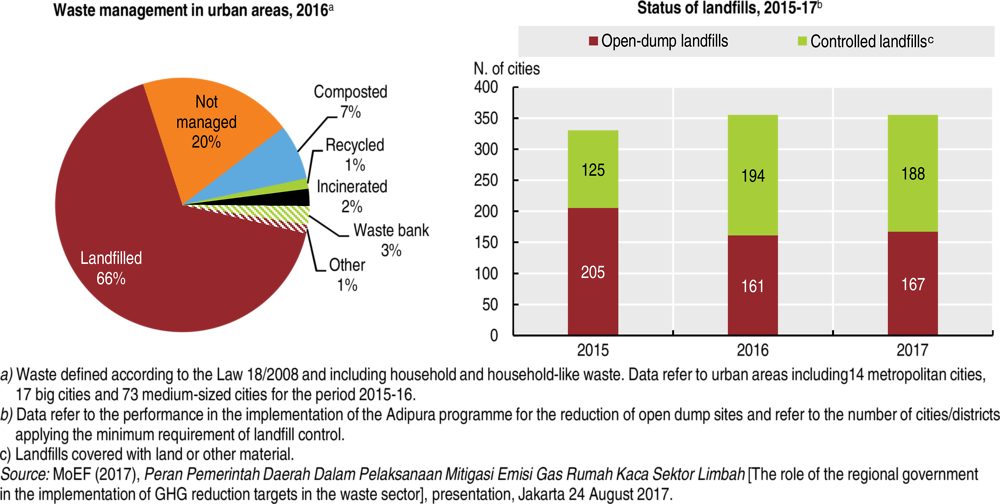

The MoEF estimates that 62 million tonnes of municipal solid waste (MSW) were generated in 2016 in Indonesian cities, roughly double the amount generated in 2006 (Cekindo, 2018b). This translates into 235 kg per capita per year, far below the OECD average of 520 kg, and roughly in line with other ASEAN countries, including Viet Nam and the Lao People’s Democratic Republic (UNEP, 2017). Data on waste generation and management in Indonesia are limited, however, and not directly comparable internationally.12 Households and offices account for half of MSW (26% and 24%, respectively), with the remainder coming from public facilities (15%) and commercial centres (14%). Waste is mostly composed of organic waste (50%), plastic (19%) and paper (11%) (MoEF, 2017a).

Waste collection services are often inadequate or inefficient. According to the MoEF, 20% of urban MSW is not managed (i.e. collected and disposed of at designated sites) but instead is burned, buried or dumped informally (Figure 1.12). As the share is much higher in rural areas, an estimated 33% of national MSW is not managed (MoEF, 2017c). Given the shortfall in waste collection, uncertainty remains as to how much waste is actually generated. Many Indonesians have no access to MSW collection; even in the biggest cities, only 70% to 85% of the area is served (MoEF, 2017). The resulting illegal burning and dumping have significant environmental, health and economic consequences from contamination of soil, air and water as well as clogging of rivers, ducts and drainage systems, which in turn exacerbates local flooding. In some cities the prevalence of unmanaged waste has become so acute that the army has been called to support cleanup (Shukman, 2018).

Appropriate waste treatment and disposal also remain a serious challenge. As in many emerging economies, landfilling is the dominant disposal type (Figure 1.12). There are a few hundred landfills across the country, nearly half of which operate as uncontrolled open dumps, although the number is decreasing. Many landfills operate near, or above, capacity limits; Jakarta’s is expected to reach capacity between 2021 and 2023, for example. Relatively small shares of MSW are composted (7%) or incinerated (2%). A small yet increasing share is managed through “waste banks” (3%), where people can exchange household waste for small amounts of money (Box 1.1). Recycling is very limited (less than 2% of managed waste). It is largely an informal-sector activity, implying that government statistics do not adequately reflect data on recycling volume and economic benefit. In 2008, there were 1.2 million waste pickers nationally, working in poor conditions and without health protection (Cekindo, 2018b). In 2018, the MoEF encouraged local governments to register waste pickers in their waste management systems so as to improve their working conditions.

Waste banks (bank sampah in Indonesian) are physical places where people can exchange waste for small amounts of money. Waste generated by households is sorted into organic and non-organic. Organic waste is composted, while non-organic waste is further sorted into three categories: plastic, paper, and bottles and metal. Households bring their sorted waste to a neighbourhood waste bank, where they make a “deposit”. The waste is weighed and given a monetary value, based on rates set by waste collectors. This amount is deposited to households’ accounts, from which they can withdraw funds as at a regular bank.

The relatively low costs associated with waste banks have enabled their rapid expansion across the archipelago. Unilever Foundation promoted one of the first waste bank initiatives in Surabaya with the installation of 20 banks in 2004 as a way to clean the city. By early 2019, there were almost 7 500 waste banks spread across 232 regencies/cities. The MoEF reports that they managed about 1.1 million tonnes of waste in 2018, or about 2% of total waste generated, up from 0.01% in 2014. Annual revenue from waste banks increased by nearly 50% since 2014, reaching IDR 30.1 billion (USD 2.1 million) in 2018. The revenue is being used to finance the operation and maintenance of the banks, although most also rely on local and/or provincial budget support. Data on how the collected waste is treated are not yet systematically collected.

The operation of waste banks has benefited from numerous innovations, including mobile waste banks that float across rivers and banks allowing trading of waste for rice or improved access to public health care programmes. Since 2018, participating households have been able to set up accounts with Bank Indonesia to save their earnings, promoting financial literacy among poorer households. In Jakarta, a regulation requires each neighbourhood to set up a waste bank. In Central Jakarta, waste volume has decreased by 35% thanks to the waste bank movement (The Jakarta Post, 2017). Many waste banks co-operate with the informal sector in sorting and processing waste. Hence it is important for local governments and neighbourhood organisations to be trained in, and enforce, labour and health standards for waste handling.

Source: World Bank (2013), Waste Not, Want Not: “Waste Banks” in Indonesia; country submission.

Marine plastic pollution

One study estimated that Indonesia was among the world’s largest contributors to marine plastic pollution, with 0.5-1.3 million tonnes of marine plastic debris a year. About 80% of it was improperly disposed waste from land (Jambeck et al., 2015). During the rainy season, large amounts of waste enter rivers and waterways and are carried to Indonesia’s coasts. With the issuance of Presidential Regulation No. 83/2018 on Marine Debris, Indonesia set a target of reducing marine waste by 70% by 2025 through awareness building, management of land-based waste, waste prevention on coasts and at sea, better financial and institutional capacity for waste management and investment in research and development. To this end, the government pledged to devote up to USD 1 billion. Achieving this goal will depend to a large extent on establishing well-functioning municipal waste collection and treatment services. The Ministry of Marine Affairs and Fisheries has already constructed waste handling facilities in ports and temporary shelters and recycling centres on small islands to reduce marine debris; the MoEF has established recycling centres in major cities and tourist destinations. Presidential Decree No. 15/2018, which aims to accelerate pollution and degradation control in the Citarum watershed, will provide valuable lessons for other priority rivers.

Main policies and measures

Indonesia has a good legal basis for waste management. The National Solid Waste Law (Law No. 18/2008) calls for sound waste handling (collection, transport, landfilling) based on the 3R approach (reduce, reuse and recycle). It requires all levels of government to develop coherent MSW plans, contribute to the financing of MSW management, and build public awareness. The law mandates waste separation as an initial step in recycling. It further stipulates that non-controlled landfills (operating as open dumps) must be closed by 2013 and that new landfills must be sanitary, avoid methane emissions, and be equipped with integrated processing facilities (MoEF, 2008). However, there is a considerable gap between the legal provisions and management practices on the ground.

Local governments are required by law to have MSW management plans, but few have consistent plans and many lack capacity and funding for their implementation. Many cities lack waste processing facilities. Finance available to local governments is insufficient, as waste charges are too low, narrowly based and weakly enforced to cover waste collection and treatment costs (Chapter 2). The national government has provided capital funding for disposal infrastructure (e.g. sanitary landfills and, more recently, waste-to-energy plants), but limited local resources and capacity for operation and management have resulted in many landfills turning into uncontrolled open dumps over time. Making national funding conditional on local performance and co-funding could help sustain the operation of new infrastructure while ensuring that national funding is complementary to sustainable local financing rather than a substitute for it. This would need to be complemented with capacity-building measures, improvement to information management and more effective co-ordination between government levels. State subsidies may be needed to get basic waste management into place where it is currently lacking.

Presidential Regulation No. 97/2017 on the National Solid Waste Management Policy and Strategy set a target of reducing 30% of waste generated by 2025 (from BAU) and handling the remainder.13 Among other matters, it calls for strengthened co-ordination between government levels, better law enforcement, increased central and regional government budgets, formation of an information system, community involvement and education, stronger involvement of the business sector, and incentives for better waste handling. It requires local authorities to develop regulations on meeting waste reduction and management targets for 2025, and make regular reports. As of early 2019, 300 cities out of 514 cities/regencies had developed local strategies, and 13 out of 34 provinces had submitted their waste management policy and strategy. The regulation addresses many barriers to more sustainable waste handling and should be implemented with priority.

Waste “exchanges” have proved to be an innovative and effective tool to speed up improvement of municipal waste services. The development of waste banks (Box 1.1) has helped engage municipalities and local communities, build awareness among citizens and start developing waste sorting and recovery capacity, while also creating socio-economic value (e.g. creating job opportunities and engaging the large informal workforce involved in waste sorting and recycling). In the city of Surabaya, people can pay for bus tickets with plastic bottles. Such initiatives can help raise citizens’ awareness of the value of waste sorting and recovery. They should be complemented with a comprehensive strategy for developing a recycling industry.

The MoEF is developing a draft roadmap for producer programmes for waste reduction, in line with the extended producer responsibility (EPR) approach. The roadmap is intended as a guideline for avoidance of plastic waste (e.g. packaging) and for product design that facilitates reuse and recycling. While it may help put in place incentives and infrastructure for waste reduction, the government should consider implementing binding EPR programmes in the medium term, at least for the most environmentally harmful products (e.g. batteries, vehicles, electronic products), so as to reduce environmental and health problems associated with landfilling them. Involvement of the informal sector in the design and implementation of such programmes will be critical to their success. Following the example of many countries (e.g. South Africa and Poland), the government is considering introducing an excise tax on plastic bags, encouraged by a successful plastic bag fee piloted in several cities in 2016,14 or gradually banning single-use plastic bags. Eighteen local governments already have such a ban in retail stores.

Hazardous and toxic waste

Control of hazardous and toxic waste (HTW) has become a major government concern, since management practices and monitoring of companies and individuals are generally poor (MoEF, 2017d). Illegal HTW dumping, such as the common practice of disposing of medical waste in municipal landfills, contributes to air and water pollution and soil contamination. Knowledge about HTW handling has improved; the number of companies monitored rose from 39 in 2012 to 295 in 2016, MoEF data show.15 Nevertheless, continued improvement is needed. In 2016, 73 million tonnes of HTW was inventoried, mostly from mining (89%), followed by infrastructure and the service sector (7%), manufacturing (2%) and agri-industry (2%). More than three-quarters (77%) of monitored HTW was handled through permitted dumping,16 with the rest being reused, processed, landfilled or exported.17

Government Regulation No. 101/2014 on the Management of Hazardous and Toxic Waste Materials emphasises the obligation for polluters to both manage the HTW they generate (either themselves or through a third party) and rehabilitate any environmental damage it causes. Local governments must carry out the rehabilitation if the polluters are unidentified. Licences for operating hazardous waste handling facilities are issued by the MoEF (MoEF, 2015b). As there is only one engineered hazardous waste landfill in the country (in West Java, western Indonesia), most hazardous waste is stored by industries on site under a five-year permit issued by the district government. Indonesia also exports hazardous waste under the Basel Convention. Support may be required by the government to build hazardous waste treatment infrastructure to cover eastern Indonesia. The government has increased resources to control medical waste from hospitals and built a first medical waste incinerator in South Sulawesi (eastern Indonesia).

Monitoring compliance with the regulation has been challenging due to a general lack of resources and capacity (MoEF, 2015c). A significant share of permit verification remains document-based and subject to fraud. Many local governments do not issue permits for (or verify) temporary storage and it is unclear what happens to the waste once the storage permit expires (MoEF, 2015b). In 2018, the MoEF increased its efforts to supervise and provide technical guidance on the matter. Still, there is a need to dedicate more resources to promote, control and enforce compliance of waste management activities with national regulations, as promoted by the OECD Council Recommendation on Environmentally Sound Management of Waste. This could include increased inspection of HTW handling facilities, capacity-building measures, clear reporting obligations and fines for non-compliance. Efforts are also needed to strengthen and implement an environmental liability regime for facilities handling dangerous substances (Box 1.2).

The 2009 Law on Environmental Protection and Management provides for strict liability for damage resulting from handling of hazardous substances and waste, whereas liability for damage from other pollution is fault-based. The national and provincial governments have a right to sue economic actors for compensation and/or to impose remediation actions for damage to the environment that is not related to private interests. Citizens can file individual and civil class action suits for compensation for environmental damage. Non-government organisations (NGOs) can file claims for environmental remediation without monetary compensation. Despite an ongoing environmental certification programme for judges (nearly 800 of whom are now certified), criminal enforcement is limited by judicial capacity and procedural constraints (Sembiring, 2017). In one verdict, the Supreme Court ordered palm oil and logging concession companies to restore damage caused by forest fires and illegal logging detected in areas where the companies operate, and to pay USD 1.3 billion in compensation. The MoEF has investigated about 600 criminal cases for environment and forestry violations since August 2015, and the national police investigated more than 150 environmental and forestry-related criminal cases.

The LEPM requires guarantee funds to be provided by individual operators for remediation of potential environmental damage. The responsible authority may contract with a third party to carry out remediation work using these funds if operators do not remedy the damage. A reclamation guarantee fund and a post-mining guarantee fund were created by a 2014 regulation of the Minister of Energy and Mineral Resources. Government Regulation No. 46/2017 on Economic Instruments in Environmental Matters stipulates that guarantee funds may be provided as a deposit, bank guarantee or insurance policy. Many of these instruments have not yet been implemented. Indonesian law does not require liability insurance cover for pollution, except for waste management companies. However, demand for voluntary environmental liability insurance could increase due to the stronger enforcement of liability in recent years: for example, the MoEF has brought substantial compensation claims, worth USD 1.3 billion, for forest fires and illegal logging.

The LEPM sets a 30-year limit on the operator’s liability for contamination after closure of an industrial site. It does not oblige the government to clean up pollution if the responsible party is unknown or insolvent, or the liability has expired, which is another barrier to remediation (Kartikasari, 2017). Remediation of contaminated sites is the responsibility of district governments, but they lack the necessary financial resources and are unwilling to identify, assess or report the sites. The central government has only just started to create an inventory of contaminated sites. There are no guidelines or standards for restoration of land, water bodies or ecosystems. Government Regulation No. 46/2017 envisages creation of a fund for remediation of environmental damage “caused by unknown sources” but does not specify whether the fund would exist at the national or provincial level, or both.

1.4.2. Chemical management

The chemical sector plays an increasingly important role in the economy. It was the fourth-largest manufacturing sector in 2015, accounting for 1.8% of GDP (BPS, 2018d). The share of chemical products in imports by Indonesia increased to 19% in 2015. Data on national production of chemicals are not available (EIBN, 2016).

Indonesia has ratified the major international chemical conventions.18 Government Regulation No. 74/2001 on Hazardous and Toxic Chemicals Management provides the basis for the management of hazardous chemicals (called bahan berbahaya dan beracun in Indonesian, or B3). It bans the export, import and use of 10 chemicals, and limits the use of an additional 45 chemicals and 209 substances listed as “usable hazardous and toxic substances”. It also requires notification of B3 chemicals prior to first import. The regulation addresses only a small subset of hazardous substances among what are likely thousands of chemicals on the Indonesian market. As the lists of B3 substances have not been updated since 2001, newer substances (including those identified for action under the Stockholm Convention) are not regulated in Indonesia.

A 2017 regulation sets out information requirements for registration and notification of B3 substances. These are rather limited (e.g. one-time registration, provision of a safety data sheet). An electronic registration system has been developed to facilitate compliance. Indonesia passed legislation to implement the Globally Harmonised System of Classification and Labelling (GHS) in 2009, which means chemicals and mixtures in the workplace, agriculture, transport and consumer sectors must be classified by industry according to the GHS, labelled and accompanied by a safety data sheet. Overall, there appears to be a need for a stronger regulatory framework addressing more hazardous chemicals. The registration and notification requirements could serve as first a step towards establishment of an inventory of chemical substances manufactured or imported in Indonesia, which would allow for systematic assessment and risk management. In the medium term, Indonesia may consider adhering to and participating in the OECD system of Mutual Acceptance of Data in chemical assessment.19

Information on the release of chemicals to the environment is scarce. There is no pollutant release and transfer registry, which would mandate public disclosure of volumes of releases of a subset of hazardous chemicals. Monitoring studies on persistent organic pollutants have shown the presence of banned pesticides and chemicals in air and/or water. This indicates a potential lack of enforcement of bans or controls of the most restricted chemicals and the need to manage chemicals that have been added to the Stockholm Convention (GoI, 2014b; Stockholm Convention, 2015; Ito et al., 2016).

Indonesia ratified the Minamata Convention on Mercury through Law No. 11 of 2017. A presidential regulation on a national action plan is under development, focusing on manufacturing, the energy sector, small-scale gold mining and the health sector. The action plan aims to eliminate mercury by 2025. It covers regulatory, data and information, technical, capacity-building and law-enforcement aspects, including development of non-mercury gold processing in small-scale gold mining, capacity building at village level, mapping of small-scale gold mining and mercury pollution, and development of mercury-contaminated soil recovery and mercury storage systems.

1.4.3. Agricultural inputs and fisheries

Agriculture and nutrient inputs

Agriculture continues to be an important driver of employment and growth, accounting for 10.5% of GDP in 2017 (excluding forestry and fisheries) and employing 30% of the workforce (Section 1.2). Rice and palm oil are the two largest commodities produced domestically, while palm oil and rubber account for more than half of agri-food exports. Indonesia has seen a strong increase in agricultural output, with average annual growth of 4% between 2005 and 2016, driven in part by productivity gains but relying mainly on conversion of forest and peatland. Total agricultural area expanded by 10% between 2005 and 2016 (FAO, 2018). There is evidence that two-thirds of new palm oil plantations came at the expense of biodiversity-rich tropical forest in 1990-2010 (OECD/FAO, 2017). The president has repeatedly issued moratoriums on new permits for concessions on primary forest land or peatland (Chapter 3).

Fertiliser consumption increased along with agricultural expansion. Application of potash fertilisers (mainly for palm oil) and phosphate fertilisers (for palm oil and rice) nearly tripled over 2005-16 (Figure 1.13). Nitrogen fertilisers, which remain the most widely used, increased by 23%. Even though the intensity of nitrogen use remains moderate by international comparison (Figure 1.13), there is evidence of over-application in some areas (e.g. Lombok island) (MoF and GIZ, 2017). Over-application of fertiliser can have a far-reaching impact on natural capital (e.g. seeping into water bodies, causing eutrophication and groundwater contamination). The government provides substantial subsidies to chemical fertiliser manufacturers (3% of public spending in 2015) to reduce the cost of fertilisers for Indonesian farmers. This risks encouraging wasteful consumption and should be replaced with other forms of agricultural support (Chapter 2).

Fisheries

Fishery activities accounted for 0.3% of GDP in 2017. Fish production nearly doubled over the past decade (+95% over 2005-16), driven primarily by quadrupling of aquaculture output (Figure 1.14). Indonesia has the world’s second largest capture fishery output and third largest aquaculture production. It is also the second largest producer and leading exporter of seaweed. Increasing domestic production has been (and remains) the main objective underpinning fishery policy. Over the coming decade, aquaculture production is expected to expand by about 37% (OECD/FAO, 2017).

Fishing and aquaculture have a strong social dimension as they support the livelihoods of about 20 million people, notably in poor and remote areas (Delpeuch, 2017). However, unsustainable intensification of aquaculture has created issues in disease management and negative environmental effects. Several fish stocks (e.g. grouper, snapper, some valuable tuna species) are overexploited, and aquaculture (notably shrimp cultivation) is a major driver of mangrove deforestation (Section 1.5). The government has a strong policy focus on fighting illegal fishing, notably by foreign vessels, and restricts the operation of large vessels (> 150 GT). However, smaller vessels (< 5 GT), which make up 95% of Indonesia’s fishing fleet, do not require fishing permits and remain largely unregulated (OECD, 2014). Indonesia is developing a roadmap to improve fishery management through quotas, capacity rules, closed seasons and zoning laws. This could help reduce pressures on fish stocks. Technology could be used more to support monitoring, law enforcement and inter-agency co-operation (OECD, 2018a).

1.5. Managing natural capital

The World Bank estimates that natural capital20 – such as forests, agricultural land, fossil fuels and minerals – accounts for about 20% of Indonesia’s total wealth, at a total value of USD 2.4 trillion (Lange, Wodon and Carey, 2018). In addition to being a direct input to the economy, Indonesia’s natural capital provides essential and valuable ecosystem services, from provision of freshwater and habitat to prevention of natural hazard and carbon storage. More sustainable and effective management of its natural capital will help Indonesia ensure that these benefits can be enjoyed for generations to come. It will also contribute to global efforts to reaching the objectives of the Convention on Biological Diversity, the Paris Agreement and the SDGs.

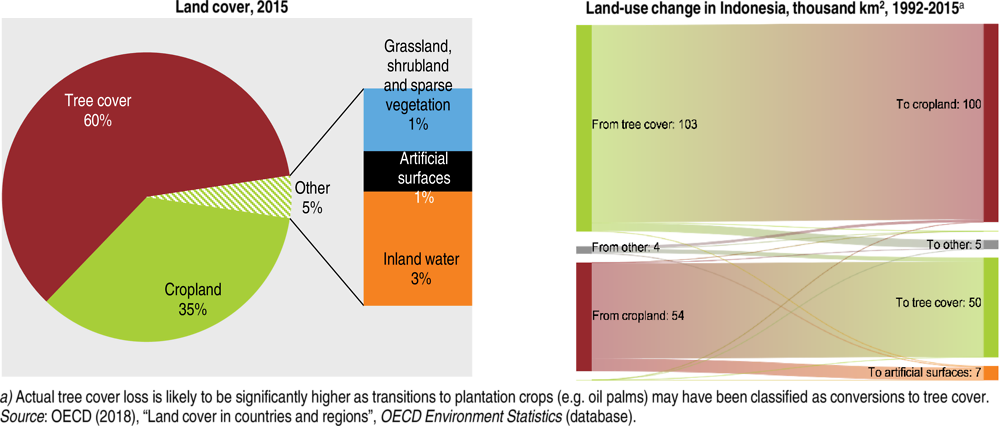

1.5.1. Physical context and land cover