copy the linklink copied!2. The future of work: What do we know?

This chapter discusses the key megatrends that are transforming the labour market and analyses their implications for job quantity, job quality, and inclusiveness, the three key dimensions of the OECD Jobs Strategy framework. Despite growing anxiety about potential job destruction driven by technological change and globalisation, a sharp decline in overall employment seems unlikely. There are, however, increasing concerns about the quality of some new jobs. This may increase disparities among workers if large segments of the workforce are unable to benefit from the good opportunities the economy generates. The most important challenge for policy makers is to prevent such growing disparities. Failing to do so will result in a future of work with deeper social cleavages and increasing discontent, which could have negative ramifications for productivity, growth, well-being, and social cohesion.

The statistical data for Israel are supplied by and under the responsibility of the relevant Israeli authorities. The use of such data by the OECD is without prejudice to the status of the Golan Heights, East Jerusalem and Israeli settlements in the West Bank under the terms of international law.

Key findings

The world of work is changing. Technological progress, globalisation and ageing populations are re-shaping the labour market. At the same time, new organisational business models and evolving worker preferences are contributing to the emergence of new forms of work. This chapter provides an overview of these changes and highlights the key challenges for policy makers.

Despite widespread anxiety about potential job destruction driven by technological change and globalisation, a sharp decline in overall employment seems unlikely. While certain jobs and tasks are disappearing, others are emerging, and overall employment has been growing.

As these transformations occur, a key challenge lies in managing the transition of workers in the different industries and regions that are hard hit by the megatrends towards the new opportunities that are opening up.

There are growing concerns about the quality of jobs. The purchasing power of wages has been stagnating for many workers and job stability has been declining. Moreover, different forms of non-standard employment have risen in a number of countries. While diversity in employment contracts can provide welcome flexibility for firms and some workers, important policy challenges remain in providing high-quality jobs to non-standard workers.

Most importantly, without immediate policy action, labour market disparities are set to increase further, as the costs of the structural adjustments occurring in the world of work are not shared equally. Job losses are concentrated among certain groups of workers and in some regions, and some workers suffer disproportionately from poorer job quality than others. Failing to address such growing disparities will result in deeper social divisions, with adverse implications for growth, productivity, well-being, and social cohesion.

These challenges do not lie on a distant horizon. The future is now as the transformations documented in this chapter are already taking place. In fact, some of them have been occurring for a few decades already. Some of the challenges they entail have therefore been in need of policy action for quite some time, but many countries have been slow to respond. Other challenges, however, are gaining strength now or remain difficult to foresee given the uncertainty about future changes in the world of work. In this context, responsible policy making should aim to enhance the resilience of the labour market, effectively preparing for a range of potential futures.

The adverse effects on the labour market associated with these deep and rapid structural changes are not inevitable, and policy can and should play an important role in shaping the future of work. Steering these changes will require a whole-of-government approach, engaging with the social partners, and civil society.

copy the linklink copied!Introduction

The world of work is undergoing significant changes. Technological progress, globalisation and ageing populations are some of the most cited trends shaping the labour market along with efforts to mitigate the effects of climate change. At the same time, new organisational business models and evolving worker preferences are contributing to the emergence of new forms of work that depart from the traditional norm of permanent full-time dependent employment.

Many of these changes are seen as potentially very disruptive. However, concerns about disruptive global trends are not new. Ever since the Industrial Revolution, fears of technology-induced job losses have been common in the public debate. In the 1930s, John Maynard Keynes warned of “a new disease… namely, technological unemployment” (Keynes, 1931[1]). Two years before, the U.S. Republican Party pledged to fortify “certain industries which cannot now successfully compete with foreign producers because of lower foreign wages and a lower cost of living abroad” (Republican Party, 1928[2]). A few decades later, concern about automation was so great that in 1961 US President Kennedy created an Office of Automation and Manpower in the Department of Labor, identifying “the major domestic challenge of the sixties: to maintain full employment at a time when automation, of course, is replacing men.” And governments in many countries have been increasingly concerned about rapid population ageing, especially (though, not exclusively) in light of the risks it poses for the sustainability of their social security systems and for economic growth.

Despite such fears, employment in OECD countries has grown steadily over the past decades. Labour markets have evolved to include social groups that were previously left out, most notably many women. Undoubtedly, many workers have been adversely affected by the decline of certain industries – and much of the focus of this chapter is precisely on those who have suffered most from the changing economy – but the fear that the future may hold fewer job opportunities than the past has so far not materialised.

Is this time different however? A number of authors have argued that the speed and intensity of technological progress is increasing and that the new wave of transformation may have more disruptive consequences for workers (Brynjolfsson and McAfee, 2011[3]; Mokyr, Vickers and Ziebarth, 2015[4]). Such worries are increasingly widespread and a large share of the population in a number of countries is concerned about the negative impacts of automation on jobs (Pew Research Center, 2018[5]).1 Moreover, public concerns have been heightened as recent trends threaten to affect people who have been historically sheltered from economic changes, including white-collar workers with relatively high levels of education and secure jobs.

In response to these concerns, this chapter offers an extensive analysis of how labour markets are changing and, in particular, a deeper investigation of the risks of job automation. On the positive side, it finds that technological progress offers new employment opportunities and that a significant risk of high technological unemployment is unlikely. However, without immediate policy action, disparities among workers may rise and social cleavages may deepen between those who gain and those who lose from the ongoing changes in the world of work. In a number of areas, the key policy challenges are well-established, though many countries have been slow to respond. Recent labour market developments, such as transformations linked to automation, the decline in unionisation, and the rise of new forms of work, are exacerbating these challenges and emphasise the need for timely, deliberate, and decisive responses to shape a better future of work for all.

The analysis focuses on three key megatrends affecting the labour market today and in the years to come: technological progress and the digital transformation, globalisation, and demographic changes. Some account is also taken of the role of other trends, such as climate change and new forms of work organisation.

This chapter provides a brief discussion of the main stylised facts that emerge from the OECD’s analysis of how the world of work is changing and identifies the key policy challenges addressed in the next chapters.2 It begins with an overview of the megatrends affecting labour markets. The discussion is then structured around the three pillars of the OECD Jobs Strategy for assessing labour market performance – job quantity, job quality, and inclusiveness – to identify key outcomes of interest (OECD, 2018[6]). The fourth pillar of the Jobs Strategy, labour market resilience and adaptability, is mainstreamed in the policy recommendations by promoting greater flexibility to respond to future changes in the world of work.

copy the linklink copied!2.1. An overview of the megatrends transforming labour markets

2.1.1. New technologies are rapidly permeating the world of work

Over the past two to three decades, the pace of technological progress and the speed of its diffusion across countries have been startling. For instance, while it took over seven decades for phone penetration to go from 10% to 90% in US households, it took only about fifteen years for mobile phones and just over 8 years for smartphones.3 Such technological leaps have had major impacts on the way people work and live.

The growth in information and communication technologies (ICT) use in the workplace provides a clear indication of how quickly new technologies permeate the workplace. From 1995 to 2007, the level of ICT capital services per hour worked more than doubled in every country analysed before growing at a slower pace (Figure 2.1). There are, however, substantial country differences in the pace of technology adoption. While in Hungary, Japan, and Slovenia, ICT levels increased by just over 150% over the period, the increase was as much as 300% in the Netherlands, the Czech Republic, Ireland, and Germany and above 350% in the United States, Belgium and the United Kingdom.

The diffusion of industrial robots perhaps best epitomises technological penetration and fears of job automation in the workplace. While robots have been on factory floors for decades, their diffusion has recently accelerated and spread beyond manufacturing. As one example, supermarkets have started to employ robots as shop assistants, and a number of companies are piloting cashier-less stores – e.g. Browne (2018[7]). The capabilities of robots are also expanding within the manufacturing sector. For example, certain robots are now able to move by themselves around the factory floor (Brynjolfsson and McAfee, 2014[8]). Data from the International Federation of Robotics show that orders of industrial robots have increased fivefold between 2001 and 2017, and such a trend is projected to accelerate further (Figure 2.2).4 Coupled with the increasing share of national income going to capital (as opposed to labour, as discussed below), such a trend directly fuels an important policy debate on the concentration of capital ownership.

These are only some examples of new technologies that have emerged and had an impact on the world of work. Going forward, further leaps in the development of artificial intelligence (AI) are likely to have applications in a broad range of domains, encroaching upon many more tasks that previously could only be performed by humans, with the potential to drive as-yet unforeseen changes in the world of work.

2.1.2. The world has become an increasingly integrated place

In conjunction with the diffusion of new technologies, the world economy has become increasingly integrated through international trade. As a share of GDP, international trade has risen across the OECD area in recent decades (Figure 2.3), and many emerging economies have become major players in the world market, both as exporters and importers. Industrial production has become increasingly integrated at the international level, with the world economy organised in global value chains (GVCs) whereby the different stages of the production process are distributed across countries and regions.

The integration of product, service, financial and technology markets fundamentally impacts labour markets around the world. It allows for and encourages greater specialisation in what gets produced and how it is produced with consequences for the skills workers require and the types of jobs that are created. Overall, more jobs are created through trade than are lost. For example, it has been estimated that, on average, 42% of business sector jobs in OECD countries were sustained by consumers in foreign markets in 2014 (OECD, 2017[9]). Yet the actual and potential negative effects of trade on certain occupations and local markets deserve careful scrutiny by policy makers as this constitutes the main cause of a growing discontent with globalisation worldwide.5 Such discontent is often intertwined with the fear of automation. Since technological progress and globalisation have historically progressed hand in hand and reinforced each other, it is difficult to isolate their individual effects (OECD, 2017[10]).

Note: ICT: information and communication technologies. ICT capital intensity per hours worked refer to the CAPIT_QPH variable in the EU KLEMS database. Data for Canada are taken from the World KLEMS database. Data series were extended using growth of the numerator and denominator of the ICT intensity ratio using the various releases of the EU KLEMS database (2009, 2013, and 2016). The 2009 EU KLEMS release covers the largest number of countries, covering the period from 1995 to 2007. Additional data were taken from later releases of EU KLEMS for the following countries: Austria, Belgium, the Czech Republic, Denmark, Finland, France, Germany, Italy, the Netherlands, Slovenia, Spain, Sweden, the United Kingdom and the United States. Values for Denmark have been adjusted to account for abnormally large increases in ICT intensity within the mining industry.

Source: EU KLEMS growth and productivity accounts, World KLEMS.

*: forecast

Source: International Federation of Robotics (IFR), https://ifr.org/.

Source: OECD (2019[11]), Trade in goods and services (indicator), https://doi.org/10.1787/0fe445d9-en.

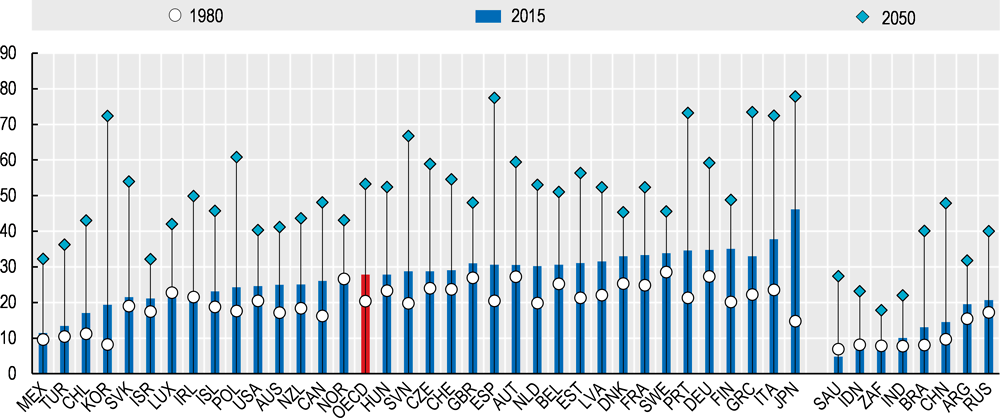

2.1.3. OECD countries are ageing

The transformation of the labour market is occurring against the backdrop of rapid population ageing in both advanced and some emerging economies. In 1980, there were 20 persons aged 65 and over for every 100 people of working age (20-64) on average across the OECD (Figure 2.4); by 2015 this number had risen to 28 and it is projected to almost double between 2015 and 2050 (OECD, 2017[12]). The challenge of rapid population ageing is particularly acute in Greece, Italy, Japan, Korea, Portugal and Spain, as well as in China. In contrast, emerging economies such as Indonesia, South Africa, and India will continue to face the demographic challenge of integrating large numbers of young people into the workforce. They will need to take advantage of the demographic dividend of a relatively young population to boost growth and prepare for the transition to a much older population.

The effects of technological progress and its global diffusion will further contribute to population ageing. Largely as a result of technological advances that increased productivity and living standards, as well as raising the quality and availability of health care, average life expectancy at birth increased across the OECD from 69 years in 1965 to 80 years half a century later.6 Going forward, scientists anticipate that new gene-editing technologies could lead to further improvements in the diagnosis and treatment of diseases, leading to longer life expectancies (Broad Institute, 2018[13]; Sanders, 2016[14]). Stronger research networks on a global scale and, more generally, the diffusion of knowledge across the world will allow these advances to reach an ever greater share of the global population, as incomes and access to health care increase in emerging economies.7 But such improvements are not inevitable, as some changes in lifestyle resulting in a rising incidence of obesity and overuse of opioids have slowed or even halted the rise in life expectancy in a few advanced economies (OECD, 2018[15]).8

These demographic trends affect the labour market in terms of technology adoption and consumption patterns. In countries with ageing populations, shortages of qualified labour may arise as the number of older workers retiring rises relative to the number of young people entering the labour market. These shortages may in turn lead to faster automation or stronger pressures to attract immigrant workers. Acemoglu and Restrepo (2017[16]) show that countries with the most rapidly ageing populations have also been among the fastest to adopt industrial robots (and consequently they suggest that an ageing population may not necessarily be a harbinger of slower economic growth). Ageing will also have a direct impact on consumption: demand is likely to shift from durable goods (such as cars) towards services (such as health care). As preferences adjust, so too will trade and the relative importance of different industries.9 All of these factors will have an impact on skill demands and the types of jobs that will be created.

Note: The old-age dependency ratio is defined as the number of people aged 65 and over per 100 people of working-age (20-64).

Source: United Nations World Population Prospects: The 2017 Revision, https://population.un.org/wpp/.

2.1.4. The global population will increase and migration pressures are likely to grow

As people live longer across the world while fertility rates remain high in a number of developing countries, the global population is expected to increase further. According to the United Nations’ 2017 World Population Prospects, the expected global population will be 9.7 billion in 2050, a 30% increase from 7.5 billion today.10 Whereas developing countries will account for the bulk of this increase, the population of OECD countries is expected to increase by less than 10%, from 1.3 billion to 1.4 billion people.

Thus, depending on infrastructure, economic opportunity, and policy choices, migration flows may radically change the makeup of the population in advanced economies. As one example, over half of workers in the Silicon Valley with a degree in science, technology, engineering or mathematics (STEM) are foreign born (Melville, Kaiser and Brown, 2017[17]). In 2017, about 258 million people around the world were living outside their country of birth, and about half of all these migrants were living in OECD countries (OECD, 2018[14]). In 2017, more than 5 million people settled permanently in the OECD. In addition, more than 4 million temporary foreign workers were recorded in OECD countries in 2016 in order to fill skills shortages, and more than 3 million international students are enrolled in a higher education establishment in an OECD country. Given the widening demographic imbalances described above, migration flows may further intensify in the coming decades and pose fundamental policy challenges.

With respect to the issues addressed in this chapter, while migrants may help countries with ageing societies to overcome skill shortages, they are also heavily exposed to some key risks. First, in the majority of OECD countries migrants are more concentrated than natives in jobs at high risk of automation. In European OECD countries, for instance, 47% of foreign-born workers are in occupations that primarily involve routine tasks and most exposed to automation (OECD, 2017[18]). Second, migrants are more likely to be in low-skilled jobs, which are frequently of low-quality, despite their relatively high educational level (OECD, 2018[19]).

copy the linklink copied!2.2. Job quantity: The ongoing transformations are unlikely to result in fewer jobs

Are we headed towards a jobless future? In advanced economies, where the impacts of automation and globalisation have been felt most strongly, this question has generated the most anxiety in the debate on the future of work. Rapid progress in the ability of machines and artificial intelligence (AI) to automate an ever-widening number of job tasks performed by humans has the potential to accelerate the substitution of labour with capital and to induce significant productivity gains, requiring less labour input into the production process. At the same time, rapid globalisation has moved many jobs from advanced economies to countries with lower labour costs. Rapid population ageing could give rise to labour shortages and spur the adoption of new technologies and job automation. Together with digitalisation and globalisation, it could result in a larger number of older workers being displaced from their jobs because of skills obsolescence. For these reasons, some have come to fear that advanced economies may be headed towards a future with fewer jobs (e.g. Frey & Osborne (2017[20]); Brynjolfsson & McAfee (2011[3])).

While it is impossible to know exactly what the future will hold, the OECD’s analysis suggests that a substantial contraction of employment is unlikely as a result of digitalisation and globalisation. The forces at play do not just destroy jobs, they also create and transform them. Historically, the net effects of major technological revolutions on employment have been positive, and there are few signs of this trend changing radically in the years to come. Indeed, recent OECD estimates find that only 14% of existing jobs are at risk of complete automation (Nedelkoska and Quintini, 2018[21]) rather than close to 50% as some other research has suggested (Frey and Osborne, 2017[20]).

However, since experts are not in agreement on the speed at which technology may be replacing work in the coming decades, responsible policy making should aim to enhance the resilience of the labour market, effectively preparing for a range of potential futures. Moreover, regardless of how overall job quantity will evolve, significant risks of decreasing job quality and increasing disparities among workers loom large and should be the key focus of policy makers. Finally, while the risk of an overall drop in employment is limited at the aggregate level, certain industries and regions may see net declines in the number of jobs available and policies are required to facilitate labour mobility and respond to regional disparities. These challenges will be the focus of the next two sections.

2.2.1. In spite of the continuous transformation of the labour markets, employment has historically been growing

Despite periodic waves of anxiety regarding labour displacement due to technological progress and globalisation, most OECD countries have seen their employment rates – the share of people of working age in employment – on an upward trajectory over past decades with the notable exception of the United States (OECD, 2018[22]) (Figure 2.5). In fact, labour demand rose strongly in line with the increase in labour supply as a result of a greater participation of women and older people. In the United States, the participation rate of women increased from 42% in 1960 to 68% in 2017. Across the OECD, female labour force participation grew by 10 percentage points since the early 1980s (from 54% in 1983 to to 64% in 2017). Countries such Spain and Ireland, where female labour force participation grew from less than 40% to more than 65% over this period, experienced the most striking results in this respect. On the other hand, a number of OECD countries there is still ample scope for further rise in women’s participation (in Turkey, for example, fewer than 4 in 10 women participate in the labour market, relative to about 8 in 10 men).

Note: Brazil data for 2000 and 2010 are from 2001 and 2011 respectively. Mexico data for 1990 are from 1991. South Africa data for 2000 are from 2001. The OECD average in the unweighted average of OECD member countries in the year indicated.

Source: OECD Employment Database, www.oecd.org/employment/database.

The increase in overall employment has occurred in parallel with rapid technological progress. The previous section offered an overview of the significant rise in ICT, in the use of robots at work, and the increasing deployment of artificial intelligence (AI). Such technologies have been directly responsible for substantial job destruction, sometimes contributing to significant employment decline in certain industries, ranging from textile production to complex electrical equipment manufacturing (OECD, 2017[10]). At the same time, by increasing productivity and raising incomes, they have generated additional demand for goods and services that has given rise to even more jobs (see Box 2.1 for a fuller discussion of the mechanisms through which technological progress destroys and creates jobs). Recent research indicates that the digital revolution has contributed significantly to job creation: 4 out of 10 jobs were created in digitally-intensive industries over the past decade (OECD, 2019[23]).

Technological progress has also contributed to higher female employment. Since women have historically borne the brunt of domestic work, increased productivity in home production (e.g. thanks to washing machines, dishwaters, etc.) is among the factors that may have contributed to the increase in their participation in the labour market. Moreover, in the past, automation has disproportionately impacted jobs typically held by men (e.g. factory workers, construction workers), while jobs in which women are overrepresented (e.g. health workers, service workers) have been buffered to a larger extent (OECD, 2017[24]). This trend, however, is changing. Recent OECD work shows that the expected risk of job displacement due to automation in the coming decades does not show significant differences by gender (OECD, 2017[24]).

Similarly, trade openness has historically gone hand-in-hand with increasing employment, despite the disruptive effects that import competition has had on specific industries. In a review of 14 multi-country econometric studies on the relationship between trade and economic performance, Newfarmer and Sztajerowska (2012[25]) find no negative impacts of trade on job quantity. On the contrary, greater openness to trade can play an important role in creating better jobs, increasing wages in both rich and poor countries, and improving working conditions. The risk of focusing on aggregate outcomes, however, is to overlook that technological progress and trade openness have not benefited all workers equally and have had strong negative impacts on certain industries and regions. This is a key challenge facing policy makers and represents one of the central issues highlighted in this report.

As technological progress marches on, celebrity entrepreneurs like Bill Gates and Richard Branson have echoed Keynes’ alarms over technological unemployment (Gates, 2017[26]; Branson, 2017[27]). While it is true that workers are displaced by new technologies, there are various channels through which technology may actually boost employment and, historically, net changes in employment have been positive in the long run. Recent OECD work finds that 40% of jobs created between 2005 and 2016 were in digitally intensive industries (OECD, 2019[23]).

A variety of evidence supports concerns that automation will cause job displacement. Recent technological progress, particularly in artificial intelligence (AI), is rapidly extending the range of tasks machines can perform and, according to some analysis, this may put a significant share of jobs at risk of automation (as discussed above). A decline in the labour share of national income across the OECD has also been attributed in part to technological change. Increasing market shares are being captured by firms that employ relatively little labour in their production process (see the discussion on “superstar firms” and “winner-takes-most dynamics” below), and in some countries it is becoming more common for companies to be organised as networks of contractors and sub-contractors who substitute some of their permanent employees (Autor et al., 2017[28]; Weil, 2014[29]). In fields like manufacturing, where a relatively large share of routine jobs are prone to automation, many workers have seen their jobs change radically or disappear altogether (Autor, Dorn and Hanson, 2013[30])

Despite these developments, prominent labour economists point to a range of countervailing forces through which technology creates new jobs. This may help to explain why, despite the displacement effects of technological progress, employment in OECD countries has historically increased on average. This framework is based on recent work by Autor and Salomons (2018[31]), Acemoglu & Restrepo (2018[32]), Acemoglu & Restrepo (2017[33]), Bessen (2017[34]).

First, technological progress can generate more jobs than it destroys within a given industry. Taking a historical perspective that spans the last two centuries, Bessen (2017[34]) clearly shows that a number of industries, including textiles, steel and automotive, experienced strong employment growth during periods of rapid technological progress and productivity growth, which could have been feared to cause a net job loss. A modern example from one specific industry is the technology developed by ride-hailing apps, which can help to improve the matching process between drivers and passengers and thus reduce the cost of ride-hailing services. By making it more convenient and cheaper for customers to use this form of transport, those apps may expand the market, creating additional demand and more jobs than they destroy (though some concerns may exist about the quality of the new jobs, as discussed in the next section). Some evidence in support of this hypothesis exists in the United States (e.g. Hathaway & Muro (2016[35])), but further investigation will be required to prove it conclusively and for a wider range of markets.

Another possibility is that by increasing productivity and reducing prices, certain technologies have a positive impact on employment in industries other than the ones when they are deployed (Autor and Salomons, 2018[31]). By increasing productivity and decreasing consumer prices in one industry, such technologies boost consumer income and increases demand (and employment) in other industries. An example, in this case, are large supermarket chains, which introduced a new business model that generated considerable economies of scale and led to lower prices, allowing consumers to increase their spending in other industries.

Thirdly, automation can lower input costs for downstream industries, leading to output and employment growth in those industries. A clear example, in this case are bulk suppliers of consumer and producer goods which exploit technology that facilitates transport, packaging, inventory management, etc. to lower prices. This helps buyers to save on per-item costs and enables downstream companies to lower their own prices increasing demand for their goods, and allowing them to hire more people.

The three channels above all operate by increasing productivity and generating new income that can be used to expand consumption. Similar examples can be found throughout the economy and span a range of industries. In addition, entirely new jobs may be created as a result of innovation, either to complement machine capabilities within existing occupational categories (e.g. new types of teachers who blend in-class and computer-based learning) or in entirely new fields (e.g. social media managers, internet of things architects, AI experts, user-experience (UX) designers, etc.). This framework is also consistent with recent empirical work by Moretti (2012[36]; 2010[37]) who shows that the creation of jobs in the ICT sector can have large multiplier effects in local labour markets (for each additional job in a high tech company in a local community, five additional jobs outside high-tech are created in the same community).

While the mechanisms above may lead to an overall increase in employment, the importance of public policy to cushion the displacement effects of technology should not be downplayed, particularly because such risks are not distributed evenly across countries, regions, and socio-demographic groups. Rather, the displacement effects of automation have a disproportionate impact on certain industries, regions and disadvantaged groups, while new jobs are often generated elsewhere and may not be accessible to displaced workers. For example, the initial wave of industrial robots primarily affected manufacturing processes, and workers who generally perform routine non-cognitive tasks (Autor, 2015[38]). While new job opportunities primarily arose in the service sector (as discussed below). If current trends continue, the already-high levels of inequality that characterise many OECD countries may worsen, which will, in turn, stunt potential consumption, productivity, and economic growth (OECD, 2015[39]).

Another megatrend that is expected to affect jobs in the coming decades is the transition towards a low-carbon economy. In light of growing concerns about climate change and global warming, a number of countries have committed to strategies for limiting average global temperature increases to 1.5 degrees Celsius above pre-industrial levels (United Nations, 2016[40]). This will result in job losses in industries involving carbon-intensive emissions but create jobs in new forms of greener energy production and in energy conservation. Estimates of total job reallocation, however, suggest that the transition towards a green economy will have relatively low impacts on total job quantity — the difference between job creation and job destruction amounts to about 0.3% of employment in OECD countries and 0.8% in non-OECD countries (Château, J., Bibas and Lanzi, 2018[41]; Botta, 2018[42]; Château, Saint-Martin and Manfredi, 2011[43]).11 In fact, the overall impact on employment might be positive. The greenness of jobs index (goji) developed using German data, for instance, suggests that Germany’s transition to a greener economy has been correlated with higher employment growth and a slight increase in wages (Janser, 2018[44]). Yet, as for the impact of trade openness, the estimated job losses from green policies will be concentrated in specific industries and types of work, possibly fostering inequality (as discussed in the previous section).

2.2.2. Is this time different? The recent wave of anxiety regarding automation

While the historical evidence suggests that broad technological unemployment and a large negative impact of globalisation on overall employment are unlikely, the most recent wave of anxiety regarding automation is fuelled by the perception that technological change is faster paced and broader based than in the past, making more jobs automatable than previously thought (Brynjolfsson and McAfee, 2011[3]; Mokyr, Vickers and Ziebarth, 2015[4]). Some authors have even argued that in some cases automation may be excessive, with firm leaders inefficiently over-investing in adopting the latest technologies, and under-investing in preparing for the jobs of tomorrow and helping workers prepare for them, with the consequence of generating negative externalities for society at large (Acemoglu and Restrepo, 2017[45]; Acemoglu and Restrepo, 2018[32]).

In light of these concerns, several authors have attempted to predict what share of jobs may be automated as a result of new technologies permeating the workplace. A widely cited analysis in this field is the one by Frey and Osborne (2017[20]), who estimate that almost half of all jobs (47%) in the United States are at risk of being substituted by computers or algorithms within the next 10 to 20 years. These estimates are constructed using experts’ assessment of the probability that different occupations can be automated.12 Critics of these large estimates argue that occupations as a whole are unlikely to be automated, as not all workers in the same occupation perform the same tasks and hence face the same risk of their jobs being automated (Autor and Handel, 2013[46]). For example, the job of one worker may involve more face-to-face interaction or autonomy than the job of another worker in the same occupation. This may partly explain why the predictions of Frey and Osborne about the pattern and depth of job automation have not yet shown up in the labour market (Manning, forthcoming).13

2.2.3. The latest OECD results show that around 14% of jobs are at risk of complete automation but many more will be affected by deep changes

An alternative approach to estimate the number of jobs at risk of automation is to directly analyse the task content of individual jobs instead of the average task content within each occupation (Arntz, Gregory and Zierahn, 2016[47]; Nedelkoska and Quintini, 2018[21]).14 Using this approach, the OECD estimates that the share of jobs at high risk of automation (i.e. those with a probability of being automated of at least 70%) is around 14%, on average, across the OECD (Figure 2.6). The figures for individual countries range from 6% in Norway to 34% in the Slovak Republic. These figures, however, only capture potential job destruction and do not account for the (possibly larger) number of jobs that technology generates (see Box 2.1; and Box 2.2 for a focus of this discussion on emerging economies).

In addition, a large share of existing jobs may change substantially in the way they are carried out. The OECD estimates that 32% of jobs, on average across the OECD, may see a large share of their tasks be automated while entirely new tasks may emerge (Figure 2.6). The analysis also highlights that the risk of automation is higher among low-skilled workers, which may further increase disparities in the labour market (Nedelkoska and Quintini, 2018[21]).

While the risk of automation may not be as high as thought by some, it is essential to recognise that there is considerable uncertainty around these estimates. The consequence of such uncertainty is that responsible policy making should be prepared for a range of possible future outcomes and aim to increase the resilience of the labour market in the face of future transformations. In this regard, providing workers with adequate training opportunities throughout their careers will play a crucial role. According to the OECD Survey of Adult Skills (PIAAC), more than 50% of the adult population, on average in 28 OECD countries, can only carry out the simplest set of computer tasks, such as writing an email and browsing the web, or have no ICT skills at all (OECD, 2016[48]). Existing systems of adult education are often unable to bridge disparities among workers and may, in fact, contribute to widen them, as higher-skilled workers typically receive more training (OECD, 2013[49]). How to make adult learning systems more effective and inclusive is the subject of Chapter 6.

Note: Jobs are at high risk of automation if the likelihood of their job being automated is at least 70%. Jobs at risk of significant change are those with the likelihood of their job being automated estimated at between 50 and 70%. Data for Belgium correspond to Flanders and data for the United Kingdom to England and Northern Ireland.

Source: OECD calculations based on the Survey of Adult Skills (PIAAC) (2012), http://www.oecd.org/skills/piaac/; and Nedelkoska, L. and G. Quintini (2018[21]), “Automation, skills use and training”, OECD Social, Employment and Migration Working Papers, No. 202, https://doi.org/10.1787/2e2f4eea-en.

The literature on the impact of automation on jobs is largely focused on advanced economies. Emerging economies, however, have very different initial conditions, including a different occupational mix, higher costs of information and communication technologies (ICT) capital, and greater skills shortages (Maloney and Molina, 2016[50]). The key question is whether, in such a context, the job opportunities created by new technologies will outweigh the loss of manufacturing jobs due to automation.

Based on their current stage of development, emerging economies face a higher predicted risk of automation. As economies develop, the industry mix of employment follows a predictable path, shifting labour from low-productivity activities, often in agriculture, to higher-productivity activities, mostly in the manufacturing and in the service sectors. In most emerging economies, agriculture and low value-added industries still make up a large share of employment. Hence, estimates based on occupations (The World Bank, 2016[51]) and more recent ones based on tasks (Nedelkoska and Quintini, 2018[21]) or work activities (McKinsey Global Institute, 2017[52])15 show that emerging economies face a higher risk of automation than more advanced ones. However, the picture is mixed and varies by income level, with countries like China, the Russian Federation, Turkey and Mexico facing a higher proportion of jobs that are potentially at risk of automation.

Nevertheless, while many jobs are “technically automatable”, automation may not be yet economically attractive in many emerging economies. As many emerging economies still have a productive structure biased towards small and medium-sized enterprises (SMEs), the resources that are necessary for costly investments in advanced technology are out of reach for most entrepreneurs. Furthermore, the incentive to innovate is dampened by skills shortages and by the relative abundance of cheap unskilled labour in young and rapidly expanding populations.

Source: The Boston Consulting Group (2015[53]), The Shifting Economics of Global Manufacturing: How a Takeoff in Advanced Robotics Will Power the Next Productivity Surge, https://www.slideshare.net/TheBostonConsultingGroup/robotics-in-manufacturing.

The potential disruptions, however, could be significant. As the cost of industrial robots continues to decline and labour costs increase, the cost savings of using technology to replace labour are starting to become significant also in emerging economies. While the Boston Consulting Group predicts that countries with very low labour costs and expanding young workforces like India and Indonesia will not benefit from replacing humans with robots in the near future, such savings will amount to more than 5% in countries like the Russian Federation and Brazil, reaching up to 18% in China by 2025 (Figure 2.7). In addition, re-shoring of production to advanced economies may contribute to job losses in emerging markets. Although the evidence on re-shoring is still limited and mixed, some signs of this process are already visible, as a number of manufactures are choosing to relocate their production nearer their domestic markets (De Backer et al., 2016[54]). Increasing labour costs and the falling cost of technology may continue to fuel this process, potentially leading some emerging countries to experience premature deindustrialisation, which may leave them in a middle-income trap (Rodrik, 2016[55]). Depending on their occupational and industrial makeup (and on their stage of development), different countries will be impacted at different points in time. Policy makers in emerging economies should start preparing well in advance. Given the lack of adequate safety nets and retraining systems, the effects on workers’ welfare may be significant and foster increased social tensions.

Source: Alonso-Soto (forthcoming[56]), Technology and the future of work in emerging economies: What is different?

2.2.4. The mere existence of a new technology does not imply that it will become pervasive and replace humans at work

An important caveat that needs to be attached to any estimate on the risk of job loss due to automation is that technological diffusion depends on a host of factors that may speed it up or slow it down. Failing to recognise the impact of these different forces may mean falling prey to technological determinism, the idea that technology determines the development of society, its labour market, social structure, and cultural values. While this is certainly true to some extent, other factors, including active policy making and social preferences, play a crucial role. The fact that a technology exists does not necessarily imply that it will spread and change the way people live, and more specifically, the way people work. In fact, existing evidence reveals that the spread of technology is highly heterogeneous across countries, industries, and firms. Constraints to broader technology diffusion may help explaining why technological progress has not translated into productivity gains in recent decades (OECD, 2018[57]).

A number of factors may favour or hinder the spread of different technologies. Above all, market forces driving the relative prices of capital and labour play an important role in determining the profitability of investing in labour-replacing technologies. Countries with relatively low labour costs, for instance, have witnessed a slower process of automation and, also for that reason, do not display a similar pattern of job polarisation as higher industrialised countries (OECD, 2017[10]).

Institutional norms and regulations – for example, product and labour market regulations as well as safety, medical and ethical standards – may prevent certain technologies from becoming prominent in certain countries. Recent OECD evidence shows that certain labour market institutions, including the rate of unionisation and employment protection legislation (EPL), can mediate the effects of technology and globalisation on job polarisation – the fall in the share of middle-skilled jobs relative to low- and, most prominently, high-skilled jobs (OECD, 2017[10]).16

Finally, consumer and societal preferences, as well as ethical norms, will play a crucial role in determining the diffusion of labour-replacing technology. In this regard, an interesting example comes from Eurobarometer data on people’s preferences regarding the deployment of robots in different industries. While the majority of respondents would be happy for robots to be used in areas such as manufacturing and space exploration, the views are much more negative regarding the use of robots in health care and education.

These countervailing trends of market forces, institutional frameworks, and consumer preferences argue against technological determinism: the mere existence of a technology does not imply that it will necessarily become pervasive nor that it will be adopted to replace humans at work (rather than to complement them).

2.2.5. While the number of employed workers may not have fallen, an increasing number of them are under-employed

While overall employment might not be negatively affected by the megatrends, there has been a rise in under-employment.17 Much like employment, changes in under-employment are generally cyclical. However, the gradual post-industrial growth of industries facing volatile demand even over the very short term (such as accommodation and food services) has exposed more workers to the risk of fewer and more variable hours (see Chapter 3). There is some evidence that the global financial crisis has exacerbated this shift. Under-employment rose sharply in many countries hit hard by the crisis, and has been slow to return to pre-crisis levels.

The risk of under-employment has increased for all workers in recent times, but, on average across the OECD, the increase has been larger for the young and those with low or medium education (Chapter 3). Across countries, women remain at a much higher risk of under-employment than men, but men – and in particular those with less than tertiary education – have seen significant increases in the probability of being under-employed. Whereas trends in under-employment among women have varied across countries, men have experienced increases in almost all of the countries examined.

copy the linklink copied!2.3. Job quality: A future of better opportunities or increased risks for workers?

Technological progress can improve job quality by increasing productivity and earnings, reducing exposure to dangerous, unhealthy and tedious tasks, as well as by granting many workers greater flexibility, autonomy, and work-life balance. New technology may also allow greater use of high-performance work practices that are typically associated with greater job satisfaction. In addition, globalisation and international trade can help “export” better working conditions through greater integration in global value chains (GVCs).

However, the greater job instability that often characterises new, non-standard forms of employment (including, but not exclusively, in the so-called “gig economy” – see Box 2.3) may result in a loss of well-being for workers in the absence of policies which guarantee adequate rights and protections for these workers (see Chapter 4). This is an important concern in countries where non-standard forms of work are proliferating and where firms increasingly rely on networks of contractors and sub-contractors, rather than on their permanent workforce, to perform many functions (giving rise to the definition of the “fissured workplace”).18, 19

“Non-standard” employment is an umbrella term, which typically covers all temporary, part-time and self-employment arrangements, i.e. everything deviating from the “standard” of full-time, open-ended employment with a single employer – see e.g. OECD (2014[58]).

However, people generally have something more specific in mind when they talk about “new forms of employment” and the resulting challenges in the context of the future of work. Often, what falls in the category of “new forms of employment” are situations in which workers are less well covered than standard employees by existing labour market regulations and social protection programmes – partly because they have developed at the fringes of existing legislation. For example, this tends to exclude “traditional” part-time and temporary work because the rights and benefits for these forms of employment are now broadly in line with those of full-time and permanent workers. Traditional forms of self-employment may also not be seen as a “new” form of employment because it is accepted that there is an element of entrepreneurial risk – i.e. in return for potentially high rewards, there is a greater element of risk that does not need to be insured against by society.

In contrast, “new” forms of work is often used to refer to: platform work (i.e. transactions mediated by an app or a website which matches customers with workers who provide services); temporary contracts of very short duration; contracts with no guaranteed and/or unpredictable working hours (on-call and zero-hours work); and own-account work more generally (i.e. self-employed workers with no employees) – see Chapter 4.

Technology and globalisation may also have an adverse impact on working conditions. By facilitating closer monitoring of workers, new technologies may reduce workers’ autonomy and increase the risk of job strain. Such adverse impacts may be further worsened by import competition, which may increase the risk of a “race to the bottom” in terms of labour standards and job quality, counteracting the positive effects of international trade on job quality mentioned above.20 Overall, the net impact of globalisation on job-quality worldwide is difficult to identify precisely and may differ across countries.

This section discusses the different forces that are likely to affect the quality of jobs in the future of work. In doing so, it connects with the broader OECD agenda on job quality, which resulted in the release of the OECD Job Quality framework (OECD, 2014[58]). It shows that while the megatrends can potentially have positive impacts on key dimensions of job quality, these gains have not been uniform across the workforce, especially in non-standard jobs.

2.3.1. Wages have been stagnating for a large share of the population over the past decade

Both trade openness and technological progress have contributed to increase workers’ earnings and living standards, on average. However, for large segments of the labour force, earnings in recent years have been stagnating despite a recovery in employment after the global economic and financial crisis (OECD, 2018[22]). In OECD countries, annual growth in nominal hourly wages dropped from 4.8% on average in the pre-crisis period to 2.1% in recent years. Real wage growth decreased by 1 percentage point over the same period. Salary dynamics in low-pay jobs have been a key driver of the overall decline in wage growth. In particular, there has been a significant worsening in average earnings of part-time jobs relative to those of full-time jobs, which is associated with the rise of involuntary part-time employment in a number of countries, discussed below.

2.3.2. Jobs have become less stable

Another key dimension of job quality is labour market security, which is closely linked to job stability. Recent OECD work shows that over the past two decades job stability has decreased on average, although with considerable differences across countries – as discussed in Chapter 3 and in Falco, Green and MacDonald (forthcoming[59]). The evidence in this respect is nuanced, but clear. Average job tenure, a direct indicator of job stability, measuring the amount of time spent in one’s current job, has increased on average. This is, however, the result of an ageing population, as a larger share of older workers in the workforce is mechanically associated with higher average tenure-levels. Once ageing is accounted for, job stability has decreased in the majority of OECD countries. The trend is particularly evident among less educated workers and it is not exclusively concentrated among youth. Prime-age and older workers with lower levels of education have also experienced increased instability in their jobs. Chapter 3 discusses this trend in detail and investigates whether decreased job stability can be ascribed to increased risks for workers or better opportunities for mobility and career progression.

2.3.3. The impacts of globalisation on job quality are mixed

Turning to the link between trade and job quality, a number of competing factors are at play. On the one hand, trade openness may be conducive to higher earnings. Indeed, there is evidence that export-driven industries tend to pay higher wages.21 On the other hand, with regard to job security, greater openness to trade and integration in GVCs may lower it by increasing the risk of job displacement due to offshoring or outsourcing (Acemoglu and Autor, 2010[60]; OECD, 2017[10]). For example, when Chinese factories began undercutting production in the United States, workers in the affected industries faced a higher risk of job loss (Autor, Dorn and Hanson, 2013[30]), resulting in higher job insecurity and, therefore, lower overall job quality.

The megatrends can also impact job quality by directly influencing working conditions and the quality of the working environment. With regard to trade, the main risk is that firms use GVCs to jettison workers in countries with high labour standards and move production to areas where labour standards are lower. For example, if welders in Germany see their jobs go to emerging economies with lower health and safety standards, global job quality may fall. Such concerns find some support in the literature, but the existing evidence is still too limited to draw firm conclusions.22 On the other hand, globalisation and international trade can help “export” better working conditions, especially as multinational companies face increasing consumer pressure and closer international scrutiny of their work environment (OECD, 2008[61]). If the latter effect could be strengthened, international trade could effectively widen global access to good jobs. The OECD Guidelines for Multinational Enterprises and the OECD Due Diligence Guidance for Responsible Business Conduct are prime examples of instruments aimed at improving labour standards through global supply chains (OECD, 2011[62]; 2018[63]).

2.3.4. Technological progress has historically helped improve working conditions

Technological progress has considerable potential to improve working conditions. Across a number of industries, tasks have been automated that formerly required hard physical labour, were often performed in strenuous or even dangerous conditions, and could increase stress and alienation.

One clear illustration of how onerous tasks may disappear is the transformation of agriculture. Between 1991 and 2017, the share of global employment in this sector fell from 43.3% to 26.5% (ILO, 2018[64]), thanks to massive diffusion of productivity-enhancing technologies, ranging from tractors and combine harvesters to more recent innovations such as robo-pickers of fruits and vegetables (ILO, 2018[65]). Many agricultural jobs were of very low quality, involving physically onerous and repetitive tasks, sometimes combined with abusive working conditions (ILO, 2015[66]) and little access to social protection, training opportunities and collective representation. Similarly, technology currently helps workers to perform some of the most dangerous and hazardous tasks in the manufacturing and construction sectors. This welcome development directly contributes to improving working conditions and safety at work.

2.3.5. But greater use of technology can also have a negative impact on job quality in certain occupations

In some cases, however, technology in the workplace can reduce job quality. For instance, greater use of computers and digital technologies to standardise and monitor tasks may limit workers’ autonomy and independence, two key markers of high-quality employment (Weil, 2014[29]; OECD, 2014[58]), but the literature is not unanimous in finding evidence of these negative aspects. Menon et al. (2018[67]), for example, find evidence of a positive effect of computer use on autonomy in Europe. Some authors have been discussing new forms of “digital Taylorism” in which employees enjoy very limited control over their work – for a survey, see Gallie (2013[68]). Many cases of such developments exist throughout the economy, for example in industries like retail and logistics. Employees who work in the warehouses of large logistics companies can be micro-managed (e.g. receiving instructions via headphones) and their productivity can be closely monitored, raising pressure and stress. Looking ahead, some firms are assessing the possibility of introducing wearable devices that would allow close monitoring of workers’ movements on the company floor. Such tight control standards have generated much controversy as they can directly harm job quality.23

Perverse effects of technology on autonomy and discretion are not limited to low-skilled workers. Recent studies find that interconnected devices afford professionals greater control over the pace and organisation of their work, but also create the expectation of constant availability by colleagues and clients, reducing discretion (Mazmanian, Orlikowski and Yates, 2013[69]). Some countries have reacted against these changes. France, for instance, recently passed a law that requires companies with more than 50 employees to grant workers the “right to disconnect” (by not expecting them to respond to emails) outside of regular working hours (de Guigné, 2016[70]).24 At the same time, some executives have embraced new technologies for enabling “work-life integration” and improved flexibility (Lebowitz, 2018[71]). However, the literature is not unanimous in highlighting the negative aspects of technology on working conditions.

2.3.6. Platform work: greater flexibility vs digital Taylorism

The rise of platform work has thrown a spotlight on the impact of technological progress on job quality. Platform work encompasses a broad range of activities, which have in common the use of online platforms to connect the demand and supply of particular services.25 The services provided by digital labour platforms can be broadly distinguished as services performed digitally (i.e. micro tasks, clerical and data entry, etc.) or services performed on-location (i.e. transport, delivery, housekeeping, etc.), as outlined in a recent report by the Joint Research Centre of the European Commission (Biagi et al., 2018[72]). In some cases, the function of the platform goes beyond its mediating role and includes providing workers with an online environment and with the necessary tools to conduct their work.

One of the positive aspects of platform work is the increased efficiency of the matching process, which may help to alleviate problems such as frictional unemployment and skills mismatches. In many OECD countries, unemployment coexists with firms recurrently complaining about not being able to find workers to fill vacancies. Platforms can help employers find workers for tasks that their existing employees cannot perform (Manyika et al., 2015[73]). Another positive aspect of platform work, often cited by workers, is greater flexibility. In the EU Collaborative Economy and Employment (COLLEEM) survey, flexibility was the most cited motivation for engaging in platform work (Biagi et al., 2018[72]). In countries with a high incidence of informal employment, platform work can represent a route to formalisation (Box 2.4).

However, work through platforms can sometimes impose severe limitations to workers’ autonomy, which may have negative impacts on their job quality and well-being. While platform workers are often classified as self-employed and can in principle choose their own hours, demand may de facto be highly concentrated in certain parts of the day. Many workers cannot set their own pay rate, which is imposed by the platform, and face restrictions over other aspects of their work organisation, including the use of uniforms and stringent instructions regarding the way the work is carried out. Finally, platform work allows for close monitoring and levels of micro-management that would be difficult to attain in the absence of the new technologies (but which are by no means exclusive to platform work, as exemplified by the case of retail and logistics discussed above). For instance, employers can use monitoring software by companies like Crossover, which takes periodic photos through the user’s webcam to verify freelancer productivity (Solon, 2017[74]). And workers who do not perform well can be automatically excluded (see also Chapter 4).

While some of these factors may generate greater efficiency and productivity, benefiting consumers (chiefly through lower prices, as well as higher service quality and availability), the result is that some if not much platform work may in fact be far from flexible and may not provide workers with the autonomy and discretion they might wish for.

The potential downsides of certain types of platform work are not limited to the risk of job strain and poor working conditions but also include the risk of low (and uncertain) earnings. Some platforms, for instance, operate globally across very different labour markets. This might induce a race to the bottom in workers’ pay.26 Moreover, since platform workers are frequently classified as self-employed, they also face challenges with regard to the adequacy of social protection, collective representation, and employment protection. These problems are not unique to platform work and they may apply to a different degree to many non-standard workers (i.e. those with contracts that fall outside the “standard” of full-time permanent employment). As such, they will be discussed below. While the jury is still out on the potential advantages and drawbacks of platform work, it is important to underscore that the risks for job quality are not inevitable and can be overcome through careful policy action.

2.3.7. Work through platforms is still a limited phenomenon

How big is employment in the platform economy? Existing evidence in this respect is still scant and imprecise, largely because standard labour force surveys do not capture the phenomenon effectively. The available data, however, indicates that this segment of the labour market is still very small.

A recent survey of 14 European countries indicates that less than 2% of the entire labour force, on average, mentions platform work as their primary activity (Biagi et al., 2018[72]). Furthermore, this is likely to be an overestimate due to the features of the survey design, which is based on an online tool that tends to over-represent the most technologically savvy part of the population. Most of the other existing studies covering a range of countries have typically produced estimates that vary between 0.5% and 3% of the labour force – see OECD (2018[6]) for a survey of the literature). The most recent evidence from the United States, for example, indicates that platform workers accounted for 1% of total employment in May 2017 (BLS, 2018[75]).

Work through digital platforms is becoming increasingly important in emerging economies. Well-known international platforms such as Uber, Cabify, and Airbnb are becoming more established in the emerging world. For example, Uber’s second largest market is Brazil and there were nearly 50 000 registered drivers and two million active users in Chile by 2017 (African Development Bank Group et al., 2018[76]). In addition, there is a growing number of active local companies in these markets (Sundararajan, 2017[77]).

To date, the debate surrounding platform work has largely focused on more advanced economies, where the emergence of platforms has sparked concerns about precarisation of labour, challenges for social protection and, more generally, for job quality (see Section 2.3.6).

Similar concerns apply in emerging economies, but one additional element plays an important role in those countries: the high incidence of informal employment (OECD, 2015[78]). In such a context, the platform economy may constitute an opportunity for many workers to formalise, since it can reduce the costs of formalisation and improve monitoring of economic activity through the digitalisation of transactions.

A good example of the potential benefits of platform work for formalisation is from Indonesia, a country where almost 60% of the workforce is working in the informal sector (OECD, 2015[78]) and where at least a third of formal jobs are of poor quality (Fanggidae, Sagala and Ningrum, 2016[79]). In a recent study, Fanggidae, Sagala and Ningrum (2016[79]) interviewed 205 drivers of “ojek” (motorcycle taxis) active on one of the rental platforms available in Jakarta (mainly “GoJek” and “Grab Bike”). Although limited in time and space, the results of the study show that platform work is not always synonymous with worse working conditions. Notably, the study highlights the role played by the platforms in facilitating access to social protection for workers. For example, GoJek offers help to its drivers to subscribe to the government health insurance program, while at Grab Bike workers are automatically enrolled in the government's professional insurance programme.

While this is only one example and additional research in this area is needed, it clearly highlights that by reducing the costs of formalisation, platforms can be an important bridge towards formality. Policy makers could go further and mandate platforms to collect personal income taxes and social security contributions on behalf of the workers (OECD, 2019[80]).

Of course, platform work is not a panacea for the problem of informality, if anything because the sector is still very small. Curbing informality in emerging economies requires a comprehensive three-pronged approach that not only aims to reduce the costs of formalisation, but also increase it perceived benefits (e.g. by improving service delivery, and linking social security contributions to the benefits received) and improves enforcement mechanisms (see OECD (2015[78]) for a detailed discussion).

Source: Alonso-Soto (forthcoming[56]), Technology and the future of work in emerging economies: What is different?

Source: http://ilabour.oii.ox.ac.uk/online-labour-index/. For further details, see Kässi, O. and V. Lehdonvirta (2016[81]), “Online Labour Index: Measuring the Online Gig Economy for Policy and Research”, Munich Personal RePEc Archive.

Also, while the platform economy may have grown fast, there are signs that its growth may already have started to slow down. Data produced by the Oxford Internet Institute provides an indication of the growing importance of online work (one type of platform work which is carried out entirely online). This Online Labour Index (OLI) is based on real-time data from five of the world’s largest English-language online labour platforms (Kässi and Lehdonvirta, 2016[81]). Despite its limitations and its focus on one particular kind of platform work, the indicator provides an indication of recent trends. Between May 2016 and May 2017 platform work grew by over a third. Since then, however, there was strong volatility and a flattening of the long-term trend (Figure 2.8).

Most vacancies are posted from OECD countries, particularly in the United States, but the majority of workers are based in non-OECD countries, with India being a particularly important player (OECD, 2018[82]). This global dimension of platform work and the risk of a race to the bottom in terms of labour standards for certain segments of this market indicate that coordinated action among countries is required.

2.3.8. More generally, non-standard work constitutes an important policy concern

The recent interest in the (still small) platform economy risks detracting from a more general and relevant issue: the significant (and in some countries growing) incidence of non-standard work more generally, and its potentially negative implications for job quality. Non-standard forms of employment encompass all forms of work that deviate from the “standard” of full-time, open-ended contracts with a single employer (see Box 2.3 for a detailed explanation). They include, therefore, workers with temporary jobs, part-time contracts, and those who are self-employed. Non-standard jobs are not necessarily of lower quality than standard jobs. The work of a high-skilled professional, for instance, may be non-standard since it falls into the category of self-employment, but might be characterised by high and stable earnings, as well as by good working conditions. Across countries, however, an association exists between many forms of non-standard work and poorer job quality, in the form of lower wages, less employment protection, reduced (or no) access to employer and social benefits, greater exposure to occupational safety and health risks, lower investments in lifelong learning, and low bargaining power of workers – e.g. OECD (2014[58]). For this reason, monitoring trends in non-standard work becomes crucial to assess developments in job quality. In the majority of OECD countries, non-standard work encompasses a significant share of the labour force (over a third), but recent trends have not been uniform.

2.3.9. Temporary employment has risen in one half of OECD countries, with a very marked upward trend in some of them

In around half of OECD countries, there has been a long-term upward trend in temporary employment. The growth of fixed-term employment has been particularly marked in countries like France, Italy, Luxembourg, the Netherlands, Poland, Portugal, the Slovak Republic, and Spain prior to the crisis (Figure 2.9). In the countries where the share of fixed-term contracts has fallen, the reduction has typically been small (with the exception of Greece, Japan, and Turkey). The share of contracts of very short duration (zero to three months) in fixed-term employment, a category that often concerns policy makers, shows a somewhat heterogeneous trend. In just over half of OECD countries, this share has increased. Yet, with the exception of the Baltic countries and Belgium, in the countries where it decreased, that trend was essentially due to the expansion of fixed-term contracts of longer duration.27 Finally, employment through temporary work agency (TWA) has grown in most OECD countries.28 Since the expansion of fixed-term employment has occurred in several countries prior to the 2000s, it is important to remark that it may only be partly attributable to the megatrends analysed in this report, and may in fact be the result of policy choices that facilitated the diffusion of temporary contracts.

Note: Data are for 1987 instead of 1986 for the Netherlands and Spain; 2001 instead of 2000 for Australia, Poland and the United States.

Source: OECD Employment Database, www.oecd.org/employment/database.

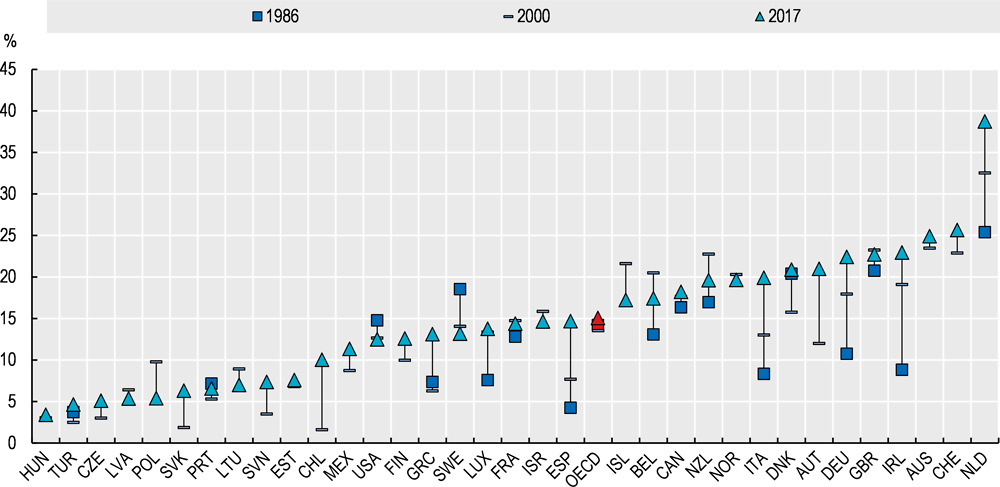

2.3.10. Part-time has grown and it is increasingly involuntary

Part-time employment has risen in most OECD countries over the past few decades, with a few notable exceptions including Iceland, Poland and Sweden (Figure 2.10). This is often viewed positively, especially since the rise in part-time employment has been associated with more women entering the labour market, and it has allowed individuals to find a better work-life balance. For some workers, however, part-time employment is involuntary and reflects the difficulty to find full-time jobs. Chapter 3 offers a discussion of this phenomenon within a broader analysis of under-employment.

The share of involuntary part-time in total part-time dependent employment has risen in two thirds of OECD countries for which data are available, although there have been declines in countries like Belgium, Poland and in Germany (since 2010). While in some countries this increase in involuntary part-time will have been partly crisis-related (e.g. Portugal, Spain, Italy and Greece), in most countries one can observe a longer-term trend increase.29

Note: Part-time employment is defined using a common cut-off of 30 hours per week usually worked in the main job. Data are for 1988 (instead of 1986) for Turkey; 1985 (instead of 1986) for Sweden, Spain and the Netherlands; and 2001 (instead of 2000) for Australia.

Source: OECD Employment Database, www.oecd.org/employment/database.

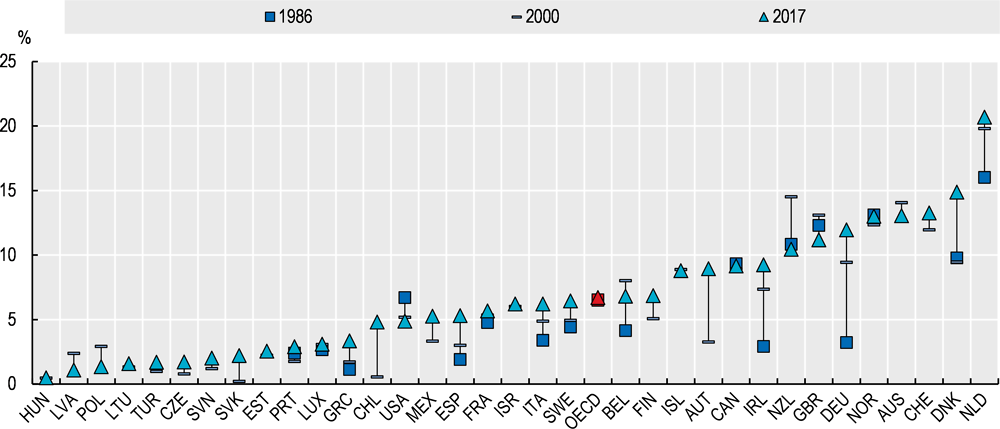

2.3.11. Short part-time and on-call labour have risen in many countries

In around one-half of OECD countries with available data, there has also been a rise in “short part-time” (i.e. individuals working 20 hours per week or less) (Figure 2.11).30 The share of short part-time is particularly high in the Netherlands (21% of dependent employment), Denmark (15%), Switzerland (13%) and Australia (13%). In some countries, there has been a fall in the share of short part-time, including Australia, Latvia, Poland, the United Kingdom, and the United States. When interpreting these trends, one should bear in mind that in some countries the rise of short part-time may be an enabling factor for some workers seeking greater flexibility (e.g. to cope with family responsibilities, combine work and study, etc.). The available data do not allow a clear distinction between these different interpretations.

This rise might be partly driven by increases in very atypical contracts (on-call and zero-hour work), but the evidence in this respect is mixed.31 Many countries have special forms of atypical part-time contracts which either involve very short part-time hours or no established minimum hours at all – such as “on-call” work and “zero-hour” contracts (Messenger and Wallot, 2015[83]) – and several of these have experienced rapid growth in recent years. In Australia, one in four workers is a casual worker, and over half of casual employees report having no guaranteed hours (Campbell, 2018[84]). In Italy, there were around 295 000 workers employed by means of an “on call” contract in 2016 (INPS, 2017[85]).32 In the Netherlands, according to a study commissioned by the ILO, on-call work is the fastest-growing type of flexible work arrangement. In 2016, there were 551 000 on-call workers in the Netherlands, making up about 8% of the workforce (Burri, Heeger-Hertter and Rossetti, 2018[86]).33 In the United Kingdom, nearly 3% of people in employment (about 900 000 people) said that they were on a zero-hour contract at the end of 2016. 34 This figure represents a 29% increase over that of 2014 (ONS, 2017[87]; Adams and Prassl, 2018[88]).35 In the Republic of Ireland, a 2015 study roughly approximates the employed population reporting variable hours at 5.3% – acknowledging that this population may include permanent and temporary workers whose hours vary (O’Sullivan et al., 2016[89]).36

Note: Data are for 1987 instead of 1986 for Spain, Sweden and the Netherlands; 1989 instead of 1986 for Norway; and 2001 instead of 2000 for Australia. Short part-time is defined as usually working 1-19 hours per week.

Source: OECD Employment Database, www.oecd.org/employment/database.

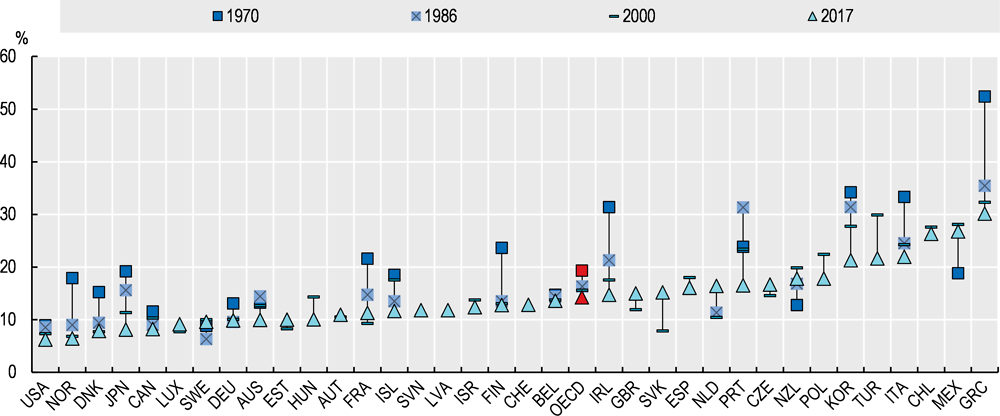

2.3.12. Self-employment is on a long-term downward trend, with some notable exceptions

There has been a long-term decline in self-employment as a share of total employment across the OECD over the past four decades, which can be observed in the majority of countries (Figure 2.12). This may be surprising and in contrast with the perception that new technologies and work models ought to facilitate the rise of independent work. Much of this trend, however, is related to the long-term decline in the agricultural sector, which predominantly occurred during the earlier part of the period. Since 2000, the incidence of self-employment has remained stable in the majority of countries.

Yet in some countries, there have been increases in self-employment, particularly in recent years. These countries include the Netherlands, the Slovak Republic and the United Kingdom.37 On the one hand, growing self-employment could be viewed as a sign of booming entrepreneurship. On the other hand, it can be linked to more precarious working conditions that may reduce job quality. This risk is particularly high for the self-employed without employees (also known as own-account workers or solo self-employed). There is no clear trend across OECD countries in the share of own-account workers in total employment in recent decades, but there have been substantial increases in countries like the Netherlands, the Czech Republic, the Slovak Republic and the United Kingdom (OECD, 2018[6]).

Note: Data are for 1971 instead of 1970 for New Zealand and Greece; 2003 instead of 2000 for Luxembourg; and 2015 instead of 2017 for Latvia.

Source: OECD Employment Database, www.oecd.org/employment/database.

2.3.13. Dependent self-employment and false self-employment are becoming more common